Banking

Unity Bank, Providus Bank Merger Awaits Final Court Approval

By Modupe Gbadeyanka

The merger and business combination between Unity Bank Plc and Providus Bank Limited remains firmly on course, a statement from one of the parties disclosed.

According to Unity Bank, there is no iota of truth in reports in certain sections of the media suggesting that the merger process had stalled, as the transaction remains firmly on track.

It was disclosed that the necessary regulatory steps have been completed, but only a few other steps to finalise the transaction, especially the final court sanction.

There had been speculations that both lenders may not meet the new minimum capital requirement of the Central Bank of Nigeria (CBN) before the March 31, 2026, deadline.

However, it was noted that the combined capital base of Unity Bank and Providus Bank exceeds N200 billion, which is the minimum requirement to retain a national banking licence under the CBN’s recapitalisation framework.

When completed, the Unity-Providus merger is expected to deliver a stronger, more competitive, and customer-centric financial institution — one with the scale, innovation, and reach to redefine the retail and SME banking landscape in Nigeria.

“The merger with Providus Bank significantly enhances our capital base, operational capacity, and strategic positioning.

“We are confident that the combined institution will be better equipped to support economic growth and deliver innovative financial solutions across Nigeria,” the chief executive of Unity Bank, Mr Ebenezer Kolawole, stated.

Recall that a few months ago, shareholders authorised the merger between the two entities at Court-Ordered Meetings. They also adopted the scheme of merger at their respective Extraordinary General Meetings (EGMs) in September 2025,

The central bank also backed the merger, with a pivotal financial accommodation to support the transaction. The merger also received a further boost with a “no objection” nod from the Securities and Exchange Commission (SEC).

The regulatory approvals form part of broader efforts to strengthen the resilience of Nigeria’s banking system, reinforce capital adequacy across the sector, and mitigate potential systemic risks.

The development positions the combined entity among the 21 banks that have satisfied the apex bank’s new capital threshold for national banking operations.

By Aduragbemi Omiyale

It was a double honour for Zenith Bank Plc at the prestigious Euromoney Awards for Excellence 2026, clinching the biggest and most coveted national and continental awards in banking.

The lender was named Africa’s Best Bank and Nigeria’s Best Bank, the latter for the second consecutive year, at a ceremony held on Thursday, July 16, at The Peninsula London Hotel, London, England.

The Euromoney Awards for Excellence are among the most respected in the global financial industry, evaluating banks on criteria including strategy, profitability, risk management, digital transformation and impact on stakeholders. Victory at the awards is regarded as a mark of the highest distinction in global banking.

“We are deeply honoured by these recognitions from Euromoney. Being recognised as Africa’s Best Bank and Nigeria’s Best Bank reflects the trust of our customers, the dedication of our unicorn workforce, and our unwavering commitment to building a truly African global financial institution.

“These awards inspire us to do even more to deliver superior value, drive financial inclusion, and support the growth of businesses across Africa,” the chief executive of Zenith Bank, Ms Adaora Umeoji, said.

The dual recognition of Zenith Bank is a testament to its sustained excellence in financial performance, customer service, digital innovation, and its contribution to economic development across Nigeria and the wider African continent.

In this year’s edition, a record of over 770 entries were received from world-class financial institutions, including HSBC, Morgan Stanley, Citibank, Barclays, Standard Bank and DBS Bank of Singapore.

Zenith Bank has continued to deliver strong financial results while accelerating investments in technology, artificial intelligence, and digital banking solutions.

In the 2025 financial year, the bank grew gross earnings by six per cent year on year to N4.19 trillion and delivered profit after tax of N1.04 trillion, while reducing its non-performing loan ratio from 4.7 per cent to 3.8 per cent.

In keeping with its dividend policy, Zenith Bank rewarded its investors with a record-breaking total dividend of N10.00 per share (totalling N410.69 billion) for the 2025 financial year, representing a 100 per cent increase over N5.00 per share paid in 2024.

By Adedapo Adesanya

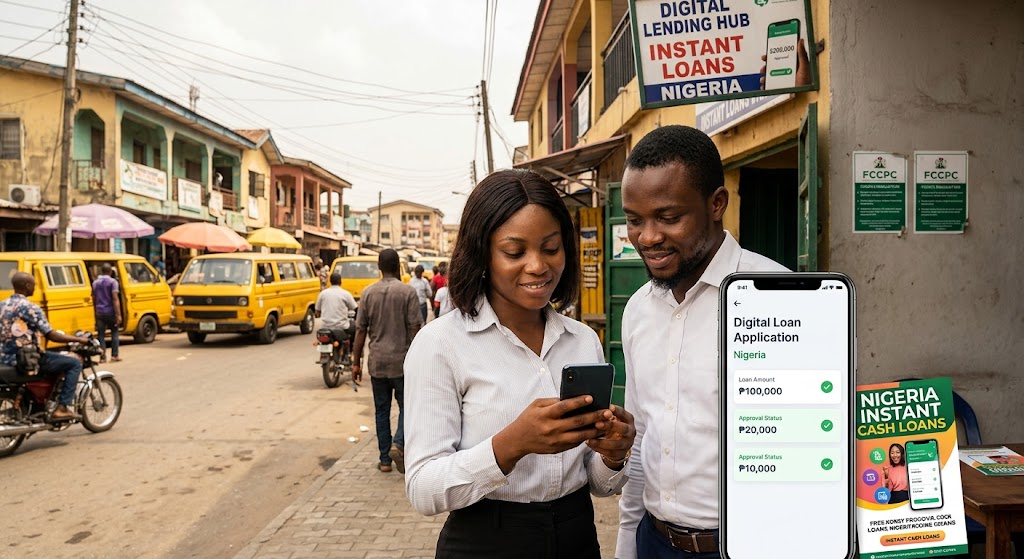

The Wireless Application Service Providers Association of Nigeria (WASPAN) has asked the Federal High Court in Lagos to suspend the enforcement of the Federal Competition and Consumer Protection Commission’s (FCCPC) Digital, Electronic, Online or Non-Traditional Consumer Lending (DEON) Regulations 2025 pending the determination of its appeal against an earlier judgment.

The application follows the dismissal of WASPAN’s substantive suit challenging the regulations, although the court made significant pronouncements on the regulatory responsibilities of the FCCPC and the Nigerian Communications Commission (NCC).

Justice Ambrose Lewis-Allagoa had ruled that the FCCPC possesses powers under Sections 104, 105, 106, and 163 of the Federal Competition and Consumer Protection Act to investigate anti-competitive conduct, protect consumers, and issue regulations.

The court also held that there was no conflict between the FCCPC Act and the Nigerian Communications Act, affirming that while the FCCPC oversees competition and consumer protection, the NCC remains the statutory regulator responsible for licensing telecommunications operators.

However, the judge clarified that “the FCCPC lacks the power to issue telecommunications licences,” adding that “nothing in the DEON Regulations creates a telecommunication licensing.”

Despite the ruling, WASPAN has filed a notice of appeal and is seeking an injunction to preserve the status quo pending the outcome of the appellate process.

In its Motion on Notice, the association asked the court for “an order of injunction restraining the Defendant whether by itself, officers, employees, agents or such other persons howsoever named from enforcing, implementing and/or otherwise giving effect to the enforcement and/or implementation of the Digital, Electronic, Online, or Non-Traditional Consumer Lending Regulations 2025” pending the hearing and determination of the appeal.

WASPAN also requested an order preventing the FCCPC from interfering with services provided by its members under the disputed regulations.

Specifically, it sought an order restraining the commission “from taking any steps towards interfering with or preventing the Plaintiff’s members from providing or continuing to provide or deploy any services or product governed by the Digital, Electronic, Online, or Non-Traditional Consumer Lending Regulations 2025.”

In addition, the association urged the court to restrain the FCCPC “from imposing any sanction, penalty, punishment or fines on the Plaintiff’s members” over any alleged non-compliance with the regulations while the appeal is pending.

According to WASPAN, the interim reliefs are necessary to preserve the subject matter of the appeal and prevent actions that could render the appellate proceedings ineffective.

Business Post reports that the latest application extends the legal battle over the FCCPC’s DEON Regulations and sets the stage for the Court of Appeal to further clarify the scope of the commission’s regulatory authority in Nigeria’s digital lending and telecommunications sectors.

By Modupe Gbadeyanka

About N2 billion is expected to be used to finance renewable energy products for customers by the end of 2026 in an effort to accelerate Nigeria’s clean energy transition.

To meet this goal, Sterling Bank is launching Sterling Solar Financing Hubs inside StarTimes retail outlets to embed on-the-spot solar financing at the point of purchase.

From the N2 billion earmarked for this initiative, N600 million has already been used up.

Under this programme, customers can now walk into participating outlets, select their preferred solar solution, receive financial guidance from dedicated Sterling Solar Financing Advisors, and begin the financing process immediately, subject to the bank’s credit assessment.

The first phase of the rollout commenced this July with five Solar Financing Hubs across Lagos, located in Lekki, Ikeja, Festac, Surulere, and Victoria Island.

The network will expand rapidly to 46 StarTimes outlets nationwide before the end of the third quarter of 2026, with a view to extending the model to more than 200 StarTimes locations nationwide.

Both parties have promised to continue working together to democratise access to clean energy financing, empowering more Nigerians to solarise their homes and businesses while contributing to a greener future.

“Sterling exists to enrich lives, and we believe that access to clean, reliable energy should be within everyone’s reach. Through this partnership with StarTimes, we are democratising access to solar by bringing financing directly to the point of need, enabling more families and businesses to transition to sustainable energy without the burden of prohibitive upfront costs. This is about unlocking opportunity, improving livelihoods, and powering Nigeria’s future,” the Divisional Head of Renewable Energy and Mobility at Sterling Bank, Mr Darlington Nwankwo, said.

Also commenting, the Vice President of StarTimes Nigeria, Mr Eric Xiao, said, “With the rollout of the Sterling Solar Financing Hubs, we are doing more than just selling solar products; we are building a sustainable energy ecosystem. By integrating StarTimes’ extensive service network with Sterling Bank’s professional financial services, we are significantly lowering the barrier for Nigerian households and small businesses to access clean energy.

“Moving forward, we will continue to deepen this partnership, ensuring that more Nigerians can enjoy reliable, affordable, and smart energy solutions, ultimately turning our vision of energy accessibility into a reality for all.”