Banking

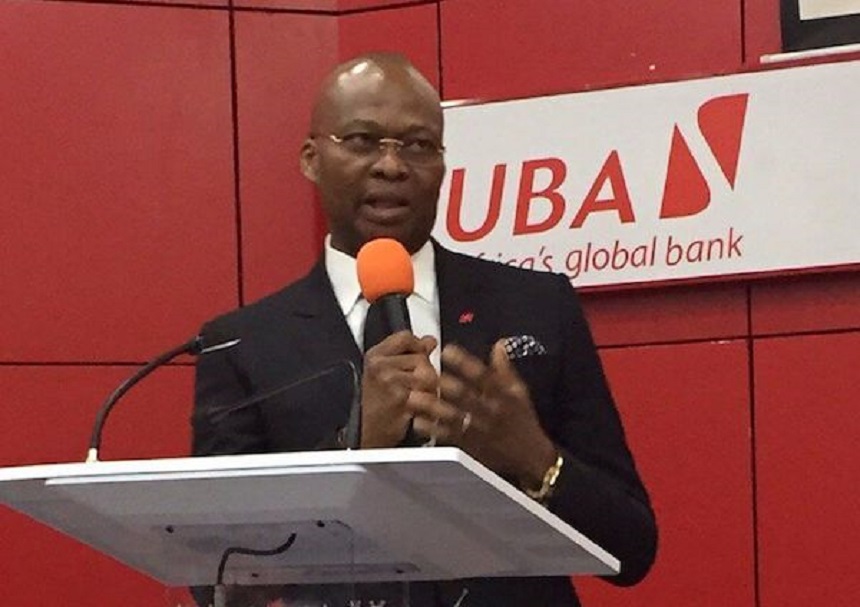

Uzoka Leads UBA Team to World Economic Forum In Davos

By Dipo Olowookere

Chief Executive Officer of United Bank for Africa (UBA) Plc, Mr Kennedy Uzoka, has led a senior executive team of the pan-African financial institution to the annual meeting of the World Economic Forum (WEF), which began on Tuesday, January 17, 2017 in Davos, Switzerland.

At the summit, the UBA delegation will interact with global business and political leaders with the hope expanding the scope of the firm.

The delegation also includes Group Head of Correspondent Banking Sola Yomi-Ajayi and Head of Embassies and Development Organisations( EMDOs), Dupe K. Olusola, responsible for relationships with multilateral and development organisations.

UBA has established itself as one of Africa’s leading financial institutions, with presence in 19 African countries, as well as globally in London, New York and Paris.

The WEF will provide a forum for UBA to build engagement with international institutions.

Despite the strong economic headwinds across Africa currently, the Group has committed to increasing its pan-African footprint.

Its strengths in corporate banking, payment technology, trade finance, and its millions-strong customer base make UBA a natural partner for global businesses focused on the African opportunity.

Speaking on the event, UBA CEO, Mr Kennedy Uzoka emphasised that, “It is critical that UBA joins world business and political leaders to discuss issues central to the progress of our world, and with specific relevance to the continent of Africa.

“UBA is the natural partner for those seeking access to Africa’s business opportunities – we look forward to engaging with the world’s business community – to show that Africa is open to business and that UBA is ready to partner.”

By Modupe Gbadeyanka

A partnership to expand opportunity, entrepreneurship, and sustainable livelihoods for young people across Africa has been signed by Access Bank and King’s Trust International (KTI).

The cooperation marks a significant milestone in advancing cross‑sector collaboration to address youth unemployment, foster entrepreneurship, and drive inclusive growth across Africa.

Under the agreement, Access Bank will support the delivery of KTI’s programmes that empower young people across several African countries, supporting them to gain skills and find pathways into meaningful employment and self-employment across Africa.

It was learned that the collaboration brings together KTI’s expertise in youth development with Access Bank’s pan‑African reach and long‑standing commitment to inclusive and sustainable growth.

Through this alliance, the two organisations will work to equip young people with the skills, confidence and support needed to build successful futures through employment and entrepreneurship.

“At Access Bank, we believe that empowering young people is fundamental to Africa’s sustainable growth. Our partnership with King’s Trust International reinforces our commitment to entrepreneurship, job creation and inclusive development, while enabling us to play a purposeful role in shaping the continent’s future,” the chief executive of Access Bank, Mr Roosevelt Ogbonna, stated.

The chief executive of KTI, Mr Will Straw, while also commenting, said, “This partnership with Access Bank reflects a shared commitment to unlocking the potential of young people across Africa. By combining our experience in youth development with Access Bank’s scale and leadership across the continent, we can create meaningful pathways to opportunity and long‑term impact.”

The signing ceremony was witnessed by senior leaders and representatives from both organisations, alongside distinguished guests, including Mr Aigboje Aig‑Imoukhuede, who is the co-Chair of KTI Africa Advisory Board and Chairman of Access Holdings Plc.

By Aduragbemi Omiyale

Mr Kennedy Onuwa Okwudili has been appointed to the board of Zenith Bank Plc as an executive director with effect from May 1, 2026.

A statement signed by the company secretary, Mr Michael Otu, disclosed that the appointment aligns with the financial institution’s “tradition and succession strategy of grooming leaders from within” to strengthen its executive management further.

He is joining the board with over 25 years of cognate banking experience spanning credit and marketing, treasury, compliance, as well as operations and has at different times worked in various zones and departments of the lender.

Mr Okwudili graduated with a Bachelor of Science (Honours) in Accounting from the University of Maiduguri, Nigeria, in 1998, with a Second Class Upper Division. He obtained a Master’s of Business Administration (MBA) from Ahmadu Bello University, Zaria, Nigeria, in 2008 and a Master’s of Science in Accounting from Veritas University, Abuja, Nigeria, in 2021.

He is a Fellow of the Institute of Chartered Accountants of Nigeria (ICAN), 2013, and also a Fellow of the Chartered Institute of Bankers of Nigeria, 2024. He is an Associate of the Chartered Institute of Taxation of Nigeria (CITN), 2016.

The banker has attended several executive education programmes both within and outside the country, including Senior Leadership Development Programme at the Lagos Business School, Corporate Directorship Programme at the Harvard Business School and Oxford Advanced Management and Leadership Programme at the University of Oxford, SAID Business School.

He is currently the President of Catholic Bankers Association of Nigeria (CBAN) and a member of the Noble Order of the Knights of St. John International (KSJI).

By Aduragbemi Omiyale

A high-level virtual webinar focused on helping public institutions to strengthen revenue systems, improve fiscal transparency, and build smarter digital structures for collections, oversight, and accountability is being planned by Fidelity Bank Plc.

This event is slated for Tuesday, March 24, 2026, under the theme Digital Fiscal Transparency: Unlocking Sub-national Opportunities for International Partners.

The programme will bring together a cross-section of public sector leaders, development institutions, heads of parastatals and agencies, as well as financial experts, to explore practical solutions for stronger public finance management.

It is expected to offer timely insights into how modern revenue infrastructure can help institutions improve efficiency, drive accountability, and support better fiscal outcomes.

The webinar will address key issues facing many public institutions today, including revenue leakages, fragmented collection channels, weak visibility into revenue performance, poor reconciliation processes, and the growing need for more transparent and technology-driven systems.

“As public institutions seek ways to improve internally generated revenue and strengthen public trust, there has been a renewed focus on fiscal transparency.

“This is particularly important in the face of recent macro and micro economic developments with many public sector agencies under pressure to do more with limited resources,” the Divisional Head of Public Sector at Fidelity Bank, Mr Richard Madiebo, said.

“It is against this background that we have conceptualised this session with a particular focus on how digital platforms can support structured invoicing, seamless collections, payment automation, contractor disbursement transparency, real-time revenue oversight, amongst other pertinent areas of revenue mobilisation and administration in Nigeria,” he added.

“The webinar forms part of our commitment to provide practical solutions that support public sector transformation and stronger sub-national development. This is in line with Fidelity Bank’s mandate to help individuals to grow, businesses to thrive, and economies to prosper,” Mr Madiebo further disclosed.

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism10 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz3 years ago

Showbiz3 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn