Economy

Dangote Cement Production Hits 45.8m MT per annum

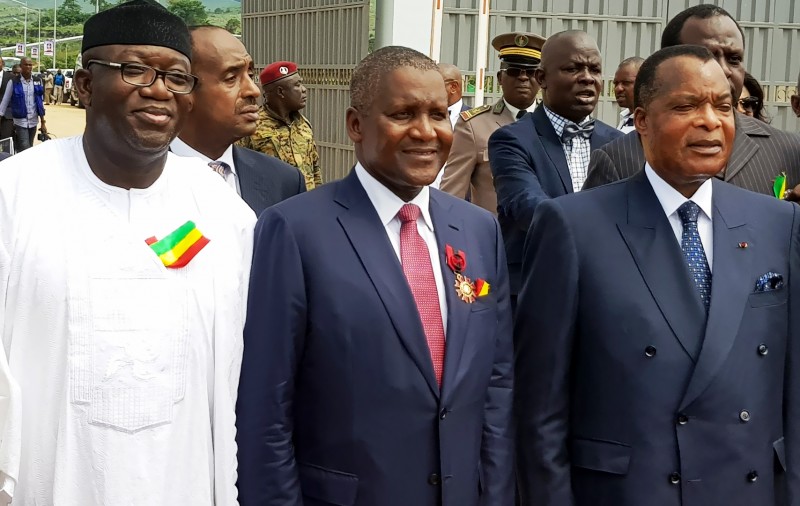

By Dipo Olowookere

Africa’s richest man, Mr Aliko Dangote, has disclosed that one of his companies, Dangote Cement Plc, has grown its total production capacity across Africa to 45.8 million metric tonnes per annum.

The Nigerian businessman said this figure was correct as at the end of May 2017, making the firm one of the biggest cement producers on the continent.

Speaking on Thursday at the launch of his 1.5mtpa capacity cement plant in Mfila, Congo Brazzaville,

Mr Dangote noted that his aspiration is to rank among the top 10 cement producers in the world by 2020.

The new plant estimated at $300 million has potentials for about 1000 direct employment and thousands of several other indirect jobs.

Mr Dangote, who is the Chairman of Dangote Cement Plc, in his address, said his company was delighted to have completed the plant on schedule, saying the addition of Dangote Cement’s 1.5 million metric tonnes per annum plant has more than doubled the total cement production capacity of Congo-Brazzaville, which now stands at 2.550 million metric tonnes per annum, far in excess of national demand.

“It is envisaged that this will contribute substantially to the availability and affordability of cement in the country and the Republic of the Congo will no longer need to depend on imports to bridge the gap between demand and supply.

“It is our hope that the inauguration of the plant will boost Congo’s economy, conserve foreign exchange that would otherwise have been spent on imports for the country, and create employment opportunities down the value chain,” he stated.

Mr Dangote commended the Congolese government noting that the bold economic reform measures put in place by President Denis Sassou Nguesso administration have been quite salutary. “The construction industry, which is a major sector of the economy, is a beneficiary of his policies, and has been receiving the attention of investors. We believe that our investment will contribute to Congo-Brazzaville’s current economic renaissance under the leadership of the President Nguesso.”

He pointed out that his organization received tremendous support and encouragement both from the government and the people of Congo-Brazzaville, right from the conceptualisation stage of our project, to its final completion, and commissioning.

In appreciation of the good gesture of the government and the people, Dangote disclosed that without waiting to stabilise production, the Cement company had already commenced CSR projects with the construction of a road with a length of 30km around Yamba, which would have cost the local government approximately 240 million CFA to execute.

He stated further “we have also disbursed scholarships for students and we are also building a school and renovating a hospital within our host communities. Apart from these, we have repaired a dilapidated bridge on a major highway at a cost of $300,000, to enable heavy duty vehicles to cross the bridge. As a policy, we also ensure that we give priority to qualified indigenes from our local host communities in our recruitment drive.”

Also speaking at the commissioning, President of Congo, Mr Denis Sassou Nguesso, described the investment as an industrial revolution, sort of, within the Economic Community of the Central African States (CEMAC), saying his country was happy to host the investment.

According to him, his government has observed the operations of Dangote Cement in other African countries and it has helped buoy their economies by sparking off other allied industries expressing the hope that Congo situation would not be an exception.

The Congolese President described the coming on stream of the Dangote cement as timely and encouraging because it is starting operations at a time the total government revenues have plummeted by 31.3 percent and revenues from the oil sector have fallen 65.1 percent since 2015 due to a slide in global crude prices.

On his part, President Muhammadu Buhari, who was represented at the event by the Minister of Mines and Steel Development, Mr Kayode Fayemi, commended Mr Dangote and his cement company for championing economic renaissance of Africa with the construction of cement plants across several African countries saying the sterling accomplishment makes the Dangote Cement brand, and indeed Mr Dangote himself, worthy ambassadors of Nigeria.

President Buhari said his government has consistently supported and encouraged the Dangote Group in its quest to contribute its quota to the economic emancipation of the African continent, which is blessed with a plethora of natural resources.

“I believe that it is only home-grown practical solutions that can address the myriad issues plaguing Africa today and one of such challenges that Africa has been grappling with for decades is the infrastructure deficit.

“I am confident that massive investments in cement production, which is a key driver of infrastructural development, will contribute in no small measure, to addressing this perennial problem,” he said.

President Buhari recalled with satisfaction that local cement manufacturers such as Dangote Cement, Lafarge and BUA, have exploited one of the solid minerals, limestone which is a basic input for cement production and which Nigeria has in abundance, in different parts of the country to achieve self-sufficiency in local cement production in 2015, and is now a net exporter of the product.

“The backward integration policy of the Federal Government in the cement sector, which was launched in 2002, has contributed to this success story by successfully substituting imports with local production, we have saved over $2billion spent on cement importation into Nigeria, annually.

“We have also started using cement for road construction in the country due to its numerous advantages over the more common bituminous road. Again, in this area, Dangote Cement is leading the charge, through AG-Dangote, its joint venture with Andrade-Gutierrez, a construction giant in Brazil,” Nigeria’s President stated.

Dangote Cement commissioned its cement plants in four African countries namely: Ethiopia, Zambia, Cameroun and Tanzania.

The Congo-Brazzaville plant, which began operations in the third quarter of 2017, will be the fifth cement plant that would be inaugurated in the last two years.

By Adedapo Adesanya

The National Insurance Commission has issued new guidelines for the collection, management, and administration of the Insurance Policyholders’ Protection Fund.

In a circular issued to all insurance institutions on Tuesday, the regulator also set May 31, 2026, as the deadline for insurers to submit their assessment returns for the 2025 financial year.

Recall that on August 5, 2025, President Bola Tinubu signed into law the Nigerian Insurance Industry Reform Act ( NIIRA 2025).

This landmark legislation repeals the Insurance Act 2003, and consolidates related provisions, ushering in a modern regulatory framework. It lays a strong foundation for sustainable growth and increased investment in the country’s insurance sector.

The commission said the guidelines were issued in exercise of its powers under the 2025 Act and other existing insurance laws and regulations to provide regulatory clarity, improve guidance, and ensure ease of compliance across the industry.

According to NAICOM, the guidelines establish a comprehensive structure for the operation of the IPPF, which serves as a statutory safety net to protect insurance policyholders in the event of distress or insolvency of a licensed insurer or reinsurer. The framework also provides direction on the reimbursement of loans by insurers and reinsurers.

NAICOM stated, “The guidelines ensure regulatory clarity, guidance and ease of compliance, as it provides a comprehensive regulatory framework for the collection, management, and administration of the Fund, which serves as a statutory safety net designed to protect insurance policyholders against distress and insolvency of a licensed insurer or reinsurer, including guidance for the reimbursement of loans by an insurer or reinsurer.

“Please be informed that the IPPF Assessment Returns in respect of the year 2025 shall be submitted to the Commission not later than 31st May 2026, while subsequent submissions shall be in line with Section 4.3 of the Guideline on Insurance Policyholders Protection Fund.”

By Adedapo Adesanya

The Dangote Refinery on Wednesday returned the petrol price to N1,200 per litre, less than 24 hours after it increased it by 5 per cent.

The private refinery had raised the ex-depot price by N75 on Tuesday, citing pressure from volatile global oil markets, but quickly brought it back to N1,200 per litre from N1,275 per litre.

The swift downward review is directly linked to a sharp drop in international crude prices. Brent crude has plunged to $95.05 per barrel, after a 13 per cent decline, while the US West Texas Intermediate (WTI) crude closed at $97.18, recording nearly a 14 per cent drop.

This development comes after US President Donald Trump announced a conditional two-week ceasefire with Iran, which eased fears of immediate supply disruptions in the global oil market.

“This will be a double-sided CEASEFIRE!” Trump said on social media, marking a sharp reversal from his earlier warning that “a whole civilisation will die tonight” if Iran failed to comply with US demands.

Iran’s Foreign Minister, Mr Abbas Araqchi, confirmed that the country would halt attacks provided strikes against Iran cease and transit through the Strait of Hormuz is coordinated by Iranian forces.

Despite the breakthrough, tensions remain elevated across the region, with several Gulf states reporting missile launches, drone activity, or issuing civil defence warnings.

While oil prices have fallen back below $100, they remain significantly elevated after surging by a record amount in March. Market analysts noted that regardless of how successful the ceasefire is, geopolitical risk related to the Strait of Hormuz is likely to remain elevated for the foreseeable future under the control of Iran.

By Adedapo Adesanya

Crude oil deliveries from the Nigerian National Petroleum Company (NNPC) Limited to the Dangote Petroleum Refinery doubled in March, boosting prospects for improved fuel availability.

This was revealed by the chief executive of Dangote Industries Limited, Mr Aliko Dangote, on Tuesday, when he received the Deputy Secretary-General of the United Nations, Mrs Amina Mohammed, at the industrial complex in Ibeju-Lekki, Lagos.

While speaking on feedstock supply, Mr Dangote commended the NNPC for increasing crude deliveries to the refinery in March, noting that volumes rose to 10 cargoes—six supplied in Naira and four in Dollars—to support domestic fuel availability, according to a statement by the Refinery.

“Last month, they gave us six cargoes for Naira and four cargoes for Dollars,” he said.

Despite the improvement, Mr Dangote noted that the supply remains below the 19 cargoes required for optimal operations, with the refinery continuing to bridge the gap through imports from the United States and other African producers.

He also expressed concern over the unwillingness of international oil companies operating in Nigeria to sell to the refinery, stating that their preference for selling crude to traders forces it to repurchase at higher costs, with broader implications for the economy.

Mr Dangote added that the refinery is seeking increased access to domestically priced crude under local currency arrangements as part of efforts to moderate fuel costs and enhance long-term energy and food security across the continent.

On her part, Mrs Mohammed underscored the strategic importance of Dangote Industries Limited -particularly Dangote Fertiliser Limited—in addressing Africa’s mounting food security challenges, while calling for stronger global partnerships to scale its impact.

Mrs Mohammed said the United Nations would prioritise amplifying scalable solutions capable of mitigating the continent’s food crisis, describing Dangote’s integrated industrial model as a critical pathway.

“I think the UN’s job here is to amplify and to put visibility on the possibilities of mitigating a food security crisis, and this is one of them,” she said. “I hope that when we go back, we can continue to engage partners and countries that should collaborate with Dangote Industries.”

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism10 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz3 years ago

Showbiz3 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn