Economy

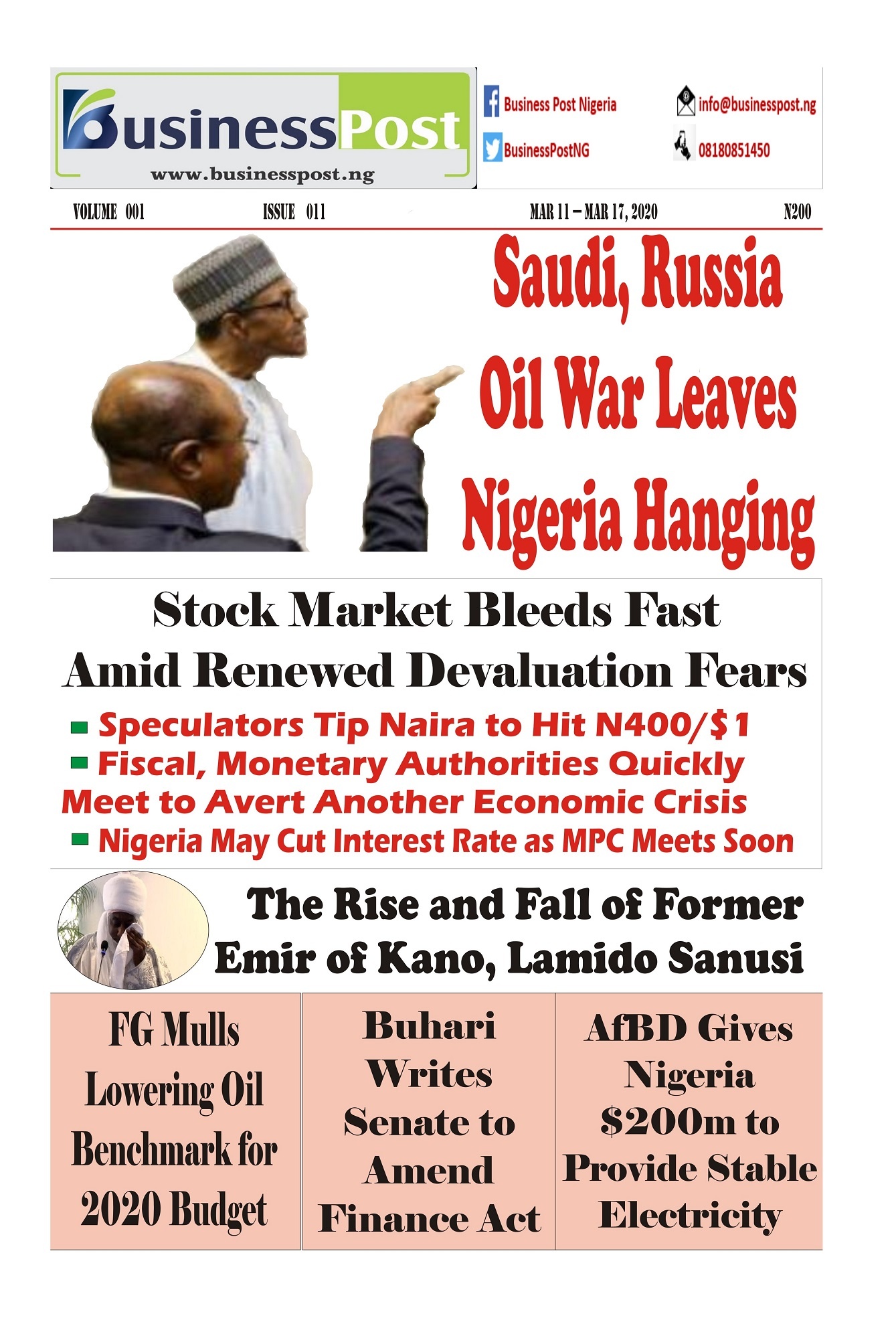

FG Mulls Lowering Oil Benchmark Below $57

By Adedapo Adesanya

Following the recent drop in the prices of crude oil at the global market, the federal government of Nigeria is considering lowering the benchmark of oil in the 2020 budget signed into law last December.

The Africa’s largest producer of the black gold pegged the average price of oil at $57 per barrel, but the disagreement between Saudi Arabia and Russia last week at a meeting of the Organisation of the Petroleum Exporting Countries (OPEC) and allies caused prices to crash to about $30 on Monday.

While Saudi wants production reduced by OPEC to help prices stay up, Russia wants members to produce at will.

Crude oil has been battered lately at the market due to coronavirus and when Russia refused to listen to Saudi on ways to salvage the situation, the Kingdom started a price war, offering the product at discounted rates.

After prices fell to more than $40 below the oil benchmark, the FG on Monday, March 9 raised an emergency committee to review the country’s N10.59 trillion Budget for the year.

The committee was set up by the President, Mr Muhammadu Buhari and is made up of the Minister of Finance, Budget and National Planning, Mrs Zainab Ahmed; the Minister of State for Petroleum Resources, Mr Timipre Sylva; the Governor of Central Bank of Nigeria (CBN), Mr Godwin Emefiele, and the Group Managing Director of the Nigeria National Petroleum Corporation (NNPC), Mr Mele Kyari.

With oil being the major key commodity that the country uses in its spending, the committee will need to revise the budget and see what necessary measures can be put in place.

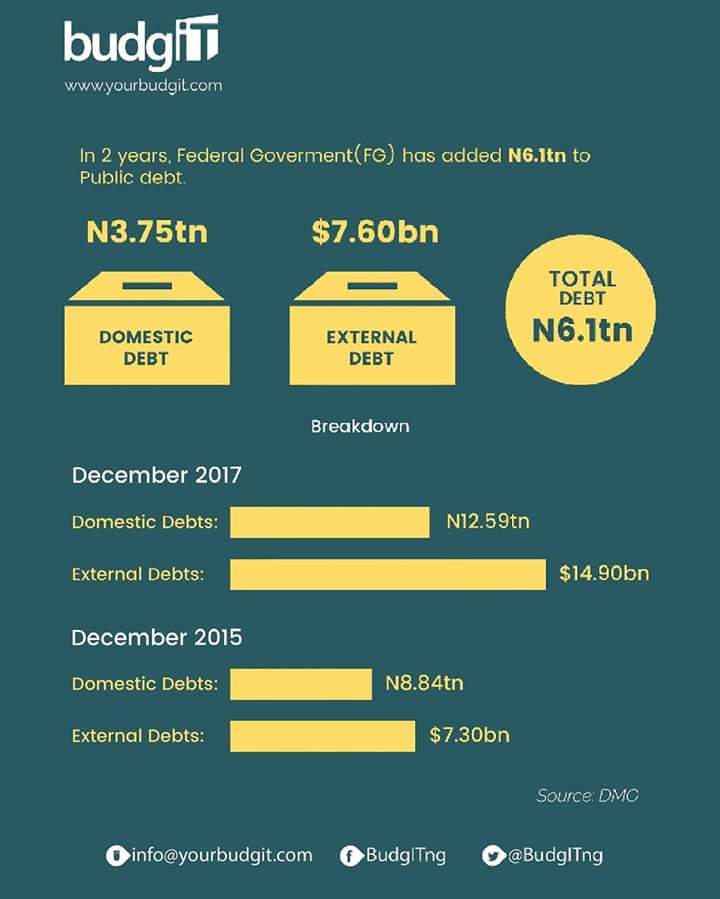

Charged with averting a replication of the 2014 oil crash which eventually led to the recession of 2016 which the country is still recovering from, Mrs Ahmed said that the committee would determine a new oil benchmark, the size of a new budget and subsequently make such new decisions public.

“But it is very clear that we will have to revisit the crude oil benchmark price that we have of $57 per barrel; we have to revisit it and lower the price. Where it will be lowered is the subject of the work of this committee.

“What the impact will be on that is that there will be reduced revenue to fund the budget and it will mean cutting the size of the budget. The quantum of the cut is what we are supposed to assess as a committee,” she said after the meeting.

During the preparation of the 2020 Budget, a crude production volume of 2.18 million barrels per day was stipulated with an oil benchmark of $57 and exchange rate of N305/$1.

In an analysis by the International Monetary Fund (IMF), it was revealed that with current market reality, Nigeria needs at least a stable oil price of $90 per barrel to balance its national budget.

The international benchmark futures, Brent Crude, as at the time of writing this report, was trading down at $37.06 per barrel.

By Adedapo Adesanya

A 10 per cent equity stake has been acquired by Odu’a Investment Company Limited in a subsidiary of FCMB Group Plc, FCMB Pensions Limited.

The move is aimed at strengthening its presence in Nigeria’s growing pension industry.

The company disclosed that the transaction was completed after receiving all required regulatory approvals from the National Pension Commission (PenCom) and the Central Bank of Nigeria (CBN), while the Securities and Exchange Commission (SEC) has also been duly notified.

Odu’a Investment said the acquisition represents a strategic investment in a resilient and steadily expanding segment of Nigeria’s financial services sector.

The company added that the deal also reinforces FCMB Pensions’ shareholder base through the entry of a long-term institutional investor.

Chairman of Odu’a Investment Company Limited, Mr Bimbo Ashiru, said the investment aligns with the organisation’s strategy of partnering with strong institutions operating in sectors critical to Nigeria’s long-term economic stability.

“This investment reflects Odu’a’s strategy of partnering with strong institutions operating in sectors that are central to Nigeria’s long-term economic stability and growth,” he said in a statement.

“The pension industry plays a critical role in mobilising long-term savings and strengthening the financial system. FCMB Pensions has built a solid platform serving contributors across Nigeria, and we see a significant opportunity to support its continued growth and impact,” he added.

Also commenting on the transaction, the Managing Director of Odu’a Investment Company Limited, Mr Abdulrahman Yinusa, described the deal as a vote of confidence in FCMB Pensions’ leadership and long-term prospects.

“Our partnership with FCMB Group Plc reflects confidence in FCMB Pensions’ strategy, leadership, and long-term potential. Together, we will work to expand its reach, support its strategic objectives, and deliver sustained value to contributors and other stakeholders,” Mr Yinusa said.

The investment brings together two established institutions with complementary strengths and a shared focus on long-term value creation. According to the company, the partnership positions FCMB Pensions to deepen market penetration and enhance service delivery within Nigeria’s contributory pension scheme.

Odu’a Investment Company Limited is an investment holding company jointly owned by the governments of the six South-West states of Nigeria.

The firm manages a diversified portfolio spanning real estate, financial services, hospitality, agriculture, and industrial investments, with a mandate to generate sustainable economic value and support regional development.

By Aduragbemi Omiyale

The chief executive of the Nigerian Exchange (NGX) Group Plc, Mr Temi Popoola, has said Nigeria’s capital market is undergoing a re-rating as global investors begin to reassess the country’s economic trajectory and investment potential.

“What we are seeing is a gradual re-rating of Nigeria. investors are beginning to look at the data more closely, the returns, the reforms, and the improving macroeconomic direction, and that is changing sentiment,” he said during a live interview on BBC Newsday in London.

He is in the United Kingdom as part of broader investor and stakeholder engagements during President Bola Tinubu’s state visit to Buckingham Palace.

Mr Popoola explained that Nigeria’s equity market has delivered strong returns in recent months, positioning it more competitively among emerging and frontier markets. According to him, this performance is helping to recalibrate long-held risk perceptions and attract renewed interest from international investors.

He added that improvements in Nigeria’s energy landscape, including increased domestic refining capacity and ongoing sector reforms, are helping to reduce the economy’s exposure to external oil price shocks, further strengthening investor confidence.

Mr Popoola emphasised that beyond short-term market movements, consistency in policy implementation will be critical in sustaining this shift in perception. “Global capital responds to clarity and consistency. As those elements become more evident, Nigeria naturally becomes more investable.”

He also highlighted the importance of sustained engagement with global financial centres, noting that platforms such as London play a key role in connecting Nigeria’s capital market to international pools of capital.

According to him, Nigeria’s evolving market structure, combined with ongoing reforms, is strengthening its position as a viable destination for long-term investment. “There is a broader recognition that Nigeria offers significant opportunities. The focus now is ensuring that this recognition translates into sustained capital flows.”

The NGX group chief concluded that Nigeria’s capital market is increasingly being viewed through a more balanced and data-driven lens, reflecting both its resilience and its long-term growth potential.

By Adedapo Adesanya

Global cryptocurrency platform, Luno, has launched a structured crypto prediction markets product in Nigeria, which will enable customers to apply their market knowledge to short-term crypto price events and earn USDC when their insights are correct.

The prediction market allows customers to express a view on whether the price of selected crypto assets, being BTC, ETH, SOL, DOGE, and XRP, will be above or below the daily price event. The market operates daily with clearly defined rules and settlement periods, offering customers structured, time-bound opportunities to act on their conviction.

Nigeria remains one of the most active crypto markets globally, with increasing demand for tools that combine simplicity and transparency. By introducing Prediction Markets focused solely on price levels, Luno aims to provide a fast, confident, and opportunity-forward format for market engagement.

Unlike traditional gaming or prediction firms like Polymarket and Kalshi, in which the odds are set by the company, Luno’s Prediction Market, powered by Limitless, is focused exclusively on crypto asset price movements within the Luno platform.

This means customers are not purchasing the underlying asset, but participating in a defined, outcome-based market that settles transparently based on real-time price data.

According to a statement, the launch reflects a broader shift in how customer behaviour is evolving in Nigeria’s growing crypto asset ecosystem, particularly as crypto asset adoption matures, many users are seeking more flexible and responsive ways to engage with markets beyond long-term holding or traditional spot trading.

Luno’s Prediction Markets product is designed to meet this demand within a familiar and regulated platform environment. The feature builds on how customers already interact with crypto asset prices – analysing charts, following market news, and forming views- and provides a structured framework for expressing those views.

According to Mr Ayotunde Alabi, chief executive of Luno Nigeria, the company is combining crypto education with a secure platform to help Nigerians confidently apply their market knowledge in a responsible and practical way.

“We are seeing a clear shift in how Nigerians want to engage with crypto assets. Many already follow price movements closely and form strong market views; we want to lead with education as well as provide a safe and secure platform to help them apply that knowledge. This feature is designed to be a natural extension for those who enjoy forecasting.

“By tying this to our ongoing educational initiatives, such as our scholarships with AltSchool, we are encouraging users to apply what they have learned about market analysis into a practical, responsible framework. Our priority is ensuring that where confidence meets opportunity, it is supported by the standards of trust our customers expect.”

Luno said it will further support the rollout with Learn & Earn educational content and tutorials explaining market mechanics and price determination. To promote informed decision-making and ensure the product is used responsibly,

Luno has embedded specific controls, including customers reading and acknowledging a risk disclosure before participating, as well as moving funds from their ordinary USDC wallet to a separate prediction wallet, which will be used to participate in prediction markets.

The firm also said that customers cannot hold both sides of the same market, in this case, Above and Below at the same time.

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism10 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz3 years ago

Showbiz3 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn