Economy

Firm Unveils Volatility Index for Nigerian Stock Market

By Quantitative Financial Analytics

Stock market volatility is one of those words that are being thrown around every now and then when describing stock market behaviours.

For example, on January 29, 2016, The Vanguard had an article entitled, “Stock Market Volatility – Operators Seek Govt Intervention Fund”, and On November 11, 2017, it also had another article, The ‘Big Oil’ and market volatilities”.

In the same way, ThisDay newspaper, on June 23, 2014 wrote “Stock Market Volatility Persists”. Even on LinkedIn pages, people write about market volatilities like the one written by Rotimi Fakayejo, MD Enterprise StockBrokers Plc on September 9, 2015, who posted the article “Gainers & Losers of the volatility of the Nigerian Bourse” on his LinkedIn page.

The Guardian on its business page wrote, “Equities rise on the Exchange amid volatility” on February 8, 2015.

Those are excellent articles both in content and intent although some made it look like market volatility is necessarily a bad thing. But one thing lacking in the articles is the quantification of how volatile the Nigerian market had been or was expected to be.

There have been various explanations for increased or subdued volatilities in the market as some of those articles opined. One reason is the arrival of new and unanticipated information that tends to or alters the expected return on a stock.

News items like the Brexit, the Chinese contagion, escalation of the US-North Korea impasse can have remarkable effects on market volatility. Changes in volatility can even emanate from changes in investors’ behaviours like when investors panic in anticipation of an election result or FED or Central bank decisions on interest rates, etc.

Volatility does not imply that the market is collapsing; rather, it implies that the market is behaving in such a way that it is more difficult to make accurate predictions about the market based on currently prevailing data and information.

Depending on one’s investment strategy and horizon and subject to the availability of tradable financial instruments, investors can manage and even profit from volatility.

In more advanced markets with tradable financial products like variance and volatility swaps, volatility may present opportunities for profit.

It follows therefore that knowledge of volatility of returns in stock markets’ behaviour is of paramount importance to investors because such knowledge helps investors to know or gain more information on the data generating such returns.

Knowing how volatile the stock market has been or is expected to be, guides investors in their decision-making process as such knowledge enables them to access both the return potential of the market as well as the uncertainty of such returns.

Volatility is the “magnitude of movements regardless of direction” and stock market volatility relates to the magnitude of price changes without paying attention to whether the change is up or down.

Stock market volatility is captured by two broad measures: implied and realized volatility. Realized volatility differs from implied volatility.

While implied volatility is a forward-looking measure, realized volatility is historical or backward looking.

Implied volatility answers the question, what is the expected volatility of the market in so and so time while realized volatility answers the question, what was or is the actual market volatility in so and so period.

While realized volatility is based on the actual movement of an underlying, implied volatility is based on a value derived from associated options prices. Realized volatility measures real risk while implied volatility measures anticipated risk.

Indices that measure volatility abound the world over especially in more advanced markets. The Chicago Board of Exchange (CBOE)’s VIX, otherwise called the fear gauge, measures implied volatility in the US market while India VIX is a volatility index based on the NIFTY Index Option prices in India and is meant to measure implied volatility in Indian stock market.

In the UK, implied volatility is measured with the FTSE IVI and is based on the index’s underlying option prices. In abundance also are realized volatility measures in more advanced markets like those calculated by S&P Dow Jones.

Currently, there is no index that measures implied or realized volatilities of the Nigerian stock market. The absence of an implied volatility measure is understandable as such is derivable from options and options are non-existent in the Nigerian market.

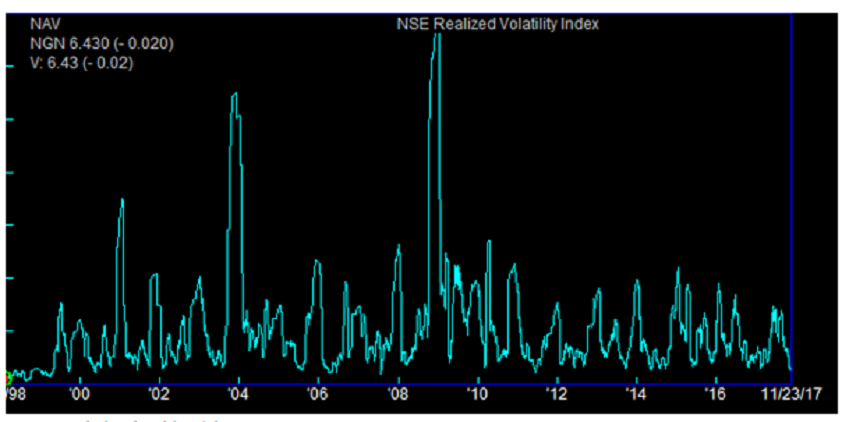

Realized volatility on the other hand, is derivable from historical data. To fill this gap, analysts at Quantitative Financial Analytics have come up with a Realized Volatility Index for the Nigerian Market.

The index is a one-month look back volatility measure of the NSE All Share index, (hereinafter called the underlying index). It assumes a 21-day monthly trading period and multiplies the result by 100 to reflect the index as a percentage.

The index is calculated daily and for all the trading dates that its underlying index (ASI) is calculated. The index has been calculated from 1998 to present and gives a bird’s eye view of the most and least volatile periods of the Nigerian stock market.

Comparatively speaking, the S&P 500 1-month realized index as at November 22, 2017 was 5.85, down from 5.87 the previous day while the Quantitative Financial Analytics (QFA) Nigeria All Share Index realized volatility index for corresponding period was 6.45, down from 6.55 the previous day.

Now, it is easy to talk about market volatility in Nigeria with some specifics and ability to compare with other markets and periods, at least in realized terms.

Quantitative Financial Analytics continues to add value to the Nigerian market with its many analytics.

It will be recalled that not long above, it rolled out its Fixed Income Analytics Report, which is a report with robust data and information on sovereign and corporate bonds trading in the Nigerian market.

For more information on the index and other reports, please contact us at an*******@****************ia.com

By Adedapo Adesanya

Sahara Upstream, a Nigeria-focused crude producer, has deployed a new 380,000-barrel tanker to boost exports from the OML 18 block as part of a wider push by domestic operators to invest in infrastructure and lift output and exports for Africa’s biggest oil producer.

The MT D Adesanya, which can hold more than 62,000 cubic metres of crude, will operate alongside the MT D Bayero, receiving crude from shuttle vessels at Bonny Anchorage, one of Nigeria’s main crude export hubs, before transferring it to the FSO Cawthorne storage facility.

Sahara said the tanker would help cut turnaround times, currently about 30 to 48 hours, and support a planned 50 per cent increase in exports from the block’s current level of about 950,000 barrels per month.

The block currently produces about 36,000 barrels per day, according to data from the Nigerian Upstream Petroleum Regulatory Commission (NUPRC), with Sahara targeting output of 60,000 barrels per day.

OML 18 is one of the Niger Delta’s oldest producing assets. It began production in 1970 and contains an estimated 1.5 billion barrels of oil equivalent in reserves.

Shell, Total and Eni sold their combined interests to Eroton in 2015 as part of a broader shift toward domestic ownership in Nigeria’s upstream sector.

This development comes as Sahara Upstream is deepening its exploration and production footprint through Asharami Energy Limited (AEL), its upstream E&P business, which says it is targeting 350,000 barrels of oil per day by 2030 through its subsidiary, Enageed Resources Limited (ERL).

The growth target comes as AEL also marks a major safety milestone, achieving 6 million Lost Time Injury (LTI)-free man-hours in its OML-148 operations — reinforcing the company’s commitment to operational excellence and safety leadership.

According to Asharami Energy, the milestone reflects its ability to execute complex operations safely, in line with Sahara’s Beyond XXX vision, which builds on the group’s 30-year legacy of responsible enterprise while marking its next chapter of impact, innovation, and sustainable growth.

The developments position Sahara Upstream and its subsidiaries among the domestic operators driving increased investment in Nigeria’s oil and gas infrastructure, as the group works to scale up production and exports for Africa’s biggest oil producer.

By Aduragbemi Omiyale

One of the leading energy firms in Nigeria, Aradel Holdings Plc, has expressed its desire to optimise its enlarged portfolio and improve operational efficiency in the second half of 2026.

The company is planning to build on the success it recorded in the first half of the year, where it grew its revenue by 577 per cent to N2.5 trillion from N368.1 billion in H1 2025.

The significant rise in earnings was driven by higher production volumes together with stronger realised crude oil and gas prices, with the average at $90.4/bbl and $2.08/mmscf, respectively.

In the period under review, the Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA) increased by 688 per cent to N1.4 trillion from N176.4 billion in the corresponding period of last year, while the operating profit surged by 789 per cent to N1.1 trillion from N118.6 billion due to higher revenue and crude handling income at N149.8 billion, partly offset by underlift cost and general and administrative costs.

The net cash generated from operations was N975.6 billion between January and June 2026 versus N140.8 billion in the same period of 2025, reflecting the cash generation of the enlarged organisation.

The net debt contracted by 70 per cent on a year-to-date basis to N46.5 billion from N475.1 billion as of December 31, 2025.

Aradel, in the period under consideration, improved its post-tax profit by 30 per cent to N191.0 billion from N146.4 billion, a development that impressed its chief executive, Mr Adegbite Falade, who said, “A firmer price environment supported performance, generating net cash from operating activities of N975.6 billion and a closing cash balance of N1.7 trillion.”

“Our enlarged portfolio provides more opportunities to generate stronger cash flow and returns for shareholders and unlocking that potential is our main focus.

“We reaffirm our full year production guidance of 110 – 140 kboepd and remain committed to operating responsibly in a changing energy landscape and to delivering lasting value for our stakeholders,” he stated.

By Dipo Olowookere

Investors on the Nigerian Exchange (NGX) Limited bought and sold 5.119 billion shares worth N404.762 billion in 285,223 deals last week. This was significantly higher than the 4.433 billion shares valued at N306.143 billion traded in 255,589 deals in the preceding week.

This surge in activity level was driven by First Holdco, AVA Capital, and Access Holdings, which accounted for 2.308 billion units sold for N224.773 billion in 27,359 deals, contributing 45.09 per cent and 55.53 per cent to the total trading volume and value, respectively.

Data showed that financial equities led the activity chart with 3.918 billion units valued at N271.428 billion in 123,514 deals, contributing 76.55 per cent and 67.06 per cent to the total trading volume and value, respectively.

Services stocks followed with 203.203 million units worth N3.061 billion in 18,333 deals, and consumer goods shares closed with a turnover of 191.283 million units valued at N13.203 billion in 30,730 deals.

In the five-day trading week, 33 equities appreciated versus 57 equities a week earlier, 56 equities depreciated versus 38 equities in the previous week, and 58 equities remained unchanged versus 51 equities in the preceding week.

The best-performing equity last week was CMFC, which chalked up 22.78 per cent to trade at N3.88, Thomas Wyatt gained 20.66 per cent to close at N4.38, Consolidated Hallmark grew by 19.60 per cent to N8.36, Lasaco Assurance rose by 18.68 per cent to N2.16, and VFD Group increased by 12.21 per cent to N11.95.

On the flip side, the worst-performing equity was ABC Transport, which decreased by 18.44 per cent to N5.75. Fortis Global Insurance shrank by 16.13 per cent to N2.34, Tripple Gee slipped by 15.54 per cent to N2.88, Veritas Kapital slumped by 15.38 per cent to N1.43, and International Breweries crashed by 13.87 per cent to N11.80.

At the close of business for the week, the All-Share Index (ASI) succumbed to selling pressure, as it shed 0.84 per cent to settle at 245,283.68 points, while the market capitalisation retreated by 0.79 per cent to N158.326 trillion.

Similarly, all other indices finished lower apart from the premium, insurance and sovereign bond indices, which appreciated by 0.02 per cent, 1.72 per cent and 0.27 per cent, respectively.