Economy

International Lenders Warn on Capacity Constraints in Africa

By Dipo Olowookere

Global and African financial heads identified country risk as the biggest challenge to their ability to lend more to African countries. Speaking in Abidjan during a one-day forum on investment risks in Africa hosted by the African Trade Insurance Agency (ATI), experts acknowledged that the abundance of current liquidity in the market did nothing to alleviate the capacity constraints faced by most banks when doing business in Africa.

Lenders are bound by regulations that prevent them from lending significant amounts to sub-investment grade sovereigns, which is the case for most African countries.

Institutions such as ATI that can offer investment insurance can help to mitigate the risks and thereby bring added lending and investment capacity to African markets. Without an increased ceiling in limits, international lenders will continue to be constrained on the amounts they are able to lend both at the sovereign and corporate levels.

Experts attending the forum also noted positive movements in countries such as Ghana and Senegal for instance, which were recently put on positive watch by the rating agency S&P. This was largely based on the dividends anticipated from key infrastructure developments and investor-friendly policies. In Senegal, for example, the country has restructured its commercial laws, implemented a Public Private Partnership law that ensures all signed public contracts in the oil and gas sector are published and created a department of competition tasked with working hand in hand with investors.

Risk analysis experts at the conference cited Botswana, Côte d’Ivoire, Ethiopia, Rwanda and Zimbabwe as countries to watch in the coming months based on strong reserves in Botswana, political transitions in the case of Ethiopia and Zimbabwe, a strategy to transform its economy into a services hub in the case of Rwanda, and creating an enabling environment to attract investors in the case of Côte d’Ivoire.

Most government representatives at the meeting also noted their countries efforts to ramp up value addition in the agriculture sector along with an emphasis on removing barriers to trade within the continent.

Jean-Louis Ekra, the former President of Afreximbank observed that Africa is in fact moving in a different direction than the current protectionist tendencies of Western countries. In contrast, Africa is uniting under the banner of the African Continental Free Trade Area, which will become the world’s largest trade area.

While participants agreed that the risk perception in Africa is typically greater than the on-the-ground reality, they also recognized that making Africa less risky would require a concerted focus aimed at improving the overall business environment in order to address the risks that do exist.

According to a recent Moody’s report, 40 to 50 percent of defaults in developing markets are directly linked to country risks. During the forum, panellists discussed low-cost solutions that could help countries reduce their risk including ensuring fair adherence to existing regulations.

“One of our roles at ATI is to educate governments to make them aware of the elements that international investors consider in their assessment of country risks. If countries are made aware that any drastic changes they make to legislation, for instance, could be a key political risk factor, they may make better choices and create more fertile environments for the private sector,” commented John Lentaigne, ATI’s Chief Underwriting Officer. He added that “a stable investment climate can be demonstrably and directly linked to growth.”

Despite Africa’s perceived risks, ECGC, India’s export credit agency and international broker, BPL Global, who have a combined $142 billion worth of exposures, noted a relatively low claims and reasonable recovery experience in Africa.

Out of BPL’s $42 billion in current exposures which is insured with international investment risk providers 8 billion of this exposure is in Africa, where the company has historically recorded USD230 million in claims of which $123 million has subsequently been recovered.

International lenders and insurers commented on the importance of ATI’s participation to make projects bankable through its preferred creditor status and relationships with African governments. This was seen as ATI’s core value proposition.

In his address to participants, Pierre Guislain the Vice-President responsible for Private Sector, Infrastructure and Industrialization of the African Development Bank noted the Bank’s commitment to transform the relationship with ATI into a strategic partnership that can leverage its reach and help countries accelerate regional integration.

ATI, a multilateral investment and trade credit insurer posted record results in 2017 for the sixth consecutive year with $10 million in profits representing a 55 percent increase over 2016 and $2.4 billion in gross exposures.

By Adedapo Adesanya

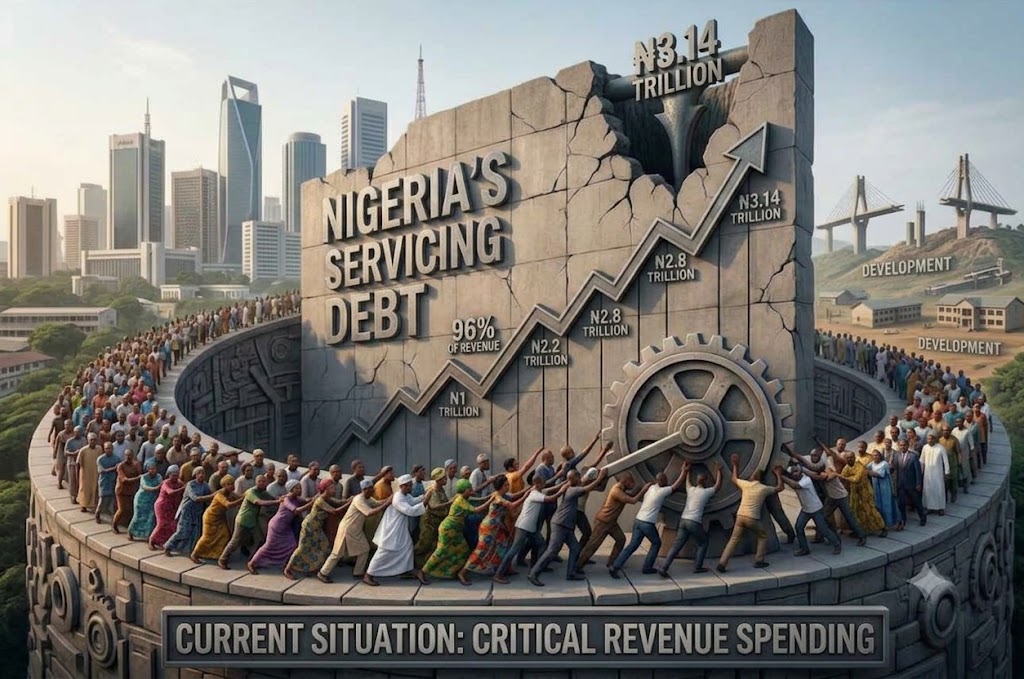

The federal government spent N3.14 trillion on servicing its domestic debt in the first quarter (Q1) of 2026, according to the Debt Management Office (DMO).

The figure, contained in the DMO’s latest domestic debt service report for Q1 2026, comprised N2.97 trillion in interest payments and N169.68 billion in principal repayments.

According to the report, the government spent N741.82 billion on domestic debt service in January before the figure rose to N967.67 billion in February.

Debt service increased further to N1.43 trillion in March, bringing total spending for the quarter to N3.14 trillion.

The March figure represented a 47.7 per cent increase from the N967.67 billion recorded in February and was 92.7 per cent higher than the N741.82 billion spent in January.

The debt office said interest payments accounted for approximately 94.6 per cent of the total domestic debt service during the quarter.

Treasury bills accounted for the largest share of interest payments at N1 trillion, while interest payments on Federal Government bonds stood at N1.96 trillion.

The government also paid N4.24 billion in interest on FGN savings bonds during the period.

The debt management body said the principal component of the debt service comprised N169.68 billion in repayments on local-denominated promissory notes.

Overall, domestic debt service rose significantly throughout the quarter, with March alone accounting for nearly half of the N3.14 trillion spent between January and March.

By Aduragbemi Omiyale

The Director-General of the Securities and Exchange Commission (SEC), Mr Emomotimi Agama, has outlined how the Federal Capital Territory Administration (FCTA) can leverage Nigeria’s capital market to raise long-term funds for critical infrastructure projects instead of relying solely on annual budgetary allocations.

According to Mr Agama, the capital market offers the FCT a sustainable financing model for roads, rail, housing, water, transport and other infrastructure through instruments such as infrastructure bonds, green bonds, real estate investment trusts (REITs), asset recycling and tokenised municipal securities.

Speaking at the Abuja Business and Investment Summit and Expo (ABIE 2026) in Abuja, the SEC chief noted that Abuja’s development demonstrates that economic growth is driven by investment, stressing that “cities are not built by budgets alone. Cities are built by capital markets.”

He advised the FCT to establish a long-term infrastructure bond programme backed by dedicated revenue sources such as ground rents, tenement rates, tolls, parking fees and land-use charges, noting that this would enable the territory to finance major projects without overburdening annual budgets.

“A budget can only spend what a single year has collected. A bond can spend what 30 years will collect,” Mr Agama said, explaining that infrastructure projects generate long-term economic value that can be used to service debt over time.

The SEC boss said the territory could also access cheaper financing through green and sustainability-linked bonds for projects including mass transit, light rail, solar-powered street lighting, waste-to-energy facilities and water infrastructure.

He further proposed the creation of an FCT Real Estate Investment Trust to unlock value from Abuja’s extensive property portfolio while giving ordinary Nigerians an opportunity to invest in the city’s real estate market.

Mr Agama also urged Abuja Investments Company Limited (AICL) to consider listing some of its businesses or establishing a listed infrastructure fund, saying this would raise capital without increasing government debt while improving corporate governance and transparency.

On the long-abandoned Millennium Tower project, he said the estimated over N400 billion completion cost should not be viewed as a budgetary burden but as an investment opportunity that could be financed through a special purpose vehicle and offered to investors via the capital market.

“The question is not whether Nigeria can afford the Millennium Tower. The question is whether we will let ordinary Nigerians own it,” he said.

Mr Agama further proposed an asset recycling programme under which completed income-generating public assets, including terminals, markets, commercial properties and the International Conference Centre, could be securitised or concessioned to institutional investors, with proceeds reinvested in new infrastructure.

He also called on the FCT to pioneer a regulated tokenised municipal bond programme that would allow citizens to invest as little as N10,000 through mobile phones in specific infrastructure projects.

According to him, the recently enacted Investments and Securities Act (ISA) 2025 has strengthened the legal framework for sub-national governments to access the capital market while providing enhanced investor protection and clearer regulation of digital assets.

Mr Agama disclosed that Nigeria’s capital market has grown significantly, with total market capitalisation exceeding N217 trillion as of May 2026, comprising about N160.5 trillion in equities and N56.7 trillion in bonds.

He said recent reforms, including the migration to a T+1 settlement cycle and regulatory measures to deepen market participation, have improved market efficiency and strengthened investor confidence.

The SEC DG assured the FCTA of the commission’s readiness to provide technical support for structuring and registering capital market instruments, saying the agency would work closely with the territory to unlock financing for infrastructure projects.

He added that Nigeria’s capital market remains critical to mobilising domestic savings for national development, insisting that “money is not scarce; delivery capacity is scarce, and financing follows delivery capacity.”

By Adedapo Adesanya

MTN Nigeria Communications Plc is awaiting regulatory approval from the Central Bank of Nigeria (CBN) to complete the planned transfer of a 60 per cent stake in its fintech businesses to its parent company, MTN Group, before the end of 2026.

The transaction involves MoMo Payment Service Bank Limited (MoMo PSB) and Y’ello Digital Financial Services Limited (YDFS), two businesses within MTN Nigeria’s financial technology portfolio.

The development follows the company’s earlier announcement in April that MTN Group, through its fintech subsidiary, would acquire a 60 per cent stake in both companies for N95.5 billion, as part of a restructuring aimed at reducing MTN Nigeria’s exposure to the loss-making fintech operations.

Under the proposed structure, MTN Nigeria would retain a 40 per cent interest, while MTN Group Fintech would hold 60 per cent.

The company had said the transaction would be implemented in two phases, with the second phase involving the creation of a financial holding company, Fintech HoldCo, which would ultimately own 100 per cent of MoMo PSB and YDFS.

However, the completion of the restructuring is subject to CBN approval, which Business Post gathered is expected to be concluded in the second half of 2026.

The proposed transaction is designed to redistribute the financial and operational risks associated with the fintech businesses between MTN Nigeria and its parent company.

MTN Nigeria had explained that the restructuring would allow MTN Group Fintech to share future capital requirements, losses, regulatory obligations and execution risks associated with the businesses, while MTN Nigeria would maintain a significant minority stake.

The planned investment has an implied value of N152.06 billion in capital injection into the fintech companies, with the N95.5 billion transaction value based on an intra-group debt-free and cash-free valuation.

MoMo PSB operates as a payment service bank, providing services including deposits, payments, transfers and digital wallets to individuals and small businesses through digital and mobile platforms.

YDFS, meanwhile, operates as a licensed super-agent, providing agency banking services such as cash deposits, withdrawals and bill payments through the MoMo network.

MTN’s decision to restructure the businesses comes as the telecommunications company continues to invest heavily in its core connectivity operations amid growing demand for data and digital services.

MTN Nigeria also said it had invested more than N1.6 trillion in network infrastructure since the beginning of 2025, including N620.5 billion in the first half of 2026 alone.

The company’s data business has also expanded significantly, with data revenue rising by 38.4 per cent to N1.70 trillion in the first half of 2026, overtaking voice revenue of N993 billion.

The growth in data services has been supported by a 9.3 per cent increase in active data subscribers to 55.7 million, while smartphone penetration rose to 66.4 per cent.

MTN’s Chief Financial Officer, Mr Modupe Kadri, said the company remained focused on maintaining investment in its core operations while managing cost pressures and strengthening its balance sheet.

The company’s fintech restructuring therefore comes against the backdrop of a broader strategy to optimise its businesses, allocate capital more efficiently and ensure that investments are aligned with areas offering stronger growth prospects.

Once approved by the CBN, the transaction will allow MTN Nigeria to reduce its direct financial exposure to the fintech businesses while retaining a 40 per cent stake and continuing to participate in their future growth.

The company is expected to provide further updates on the transaction as the regulatory approval process progresses, with completion targeted before the end of 2026.