Economy

Investors Lament Resumption of 5% VAT on NSE Transactions

By Dipo Olowookere

Some investors in the Nigerian Stock market have expressed dissatisfaction with the resumption of 5 percent Value Added Tax (VAT) commission to be charged on all transactions executed at the exchange from Wednesday, July 24, 2019.

Business Post recalls that on July 25, 2014, the federal government, through the then Minister of Finance and Coordinating Minister of the Economy, Mrs Ngozi Okonjo-Iweala, commenced the exemption of VAT payment on all NSE transactions. This exemption had a lifespan of five years, which lapses on July 24, 2019.

Already, some stockbrokers have been sending notifications to their clients, informing them that from next week, they will begin to pay extra amount of money for transactions carried out on their behalf.

“Please be notified that Value Added Tax (VAT) on commissions will now be charged on transactions conducted on the Nigerian Stock Exchange (NSE).

“The order for exemption of VAT from all NSE transactions was granted by the Coordinating Minister of the Economy and the Honourable Minister of Finance in 2014. The order became effective on the 25th July 2014 for a 5 -year period, which expires on the 24th July, 2019.

“In this regard, all dealing members of the Nigerian Stock Exchange have been notified to resume charging of VAT on all NSE transactions effective 25th July 2019.

“Subsequently, a 5% VAT on brokerage commission earned, NSE fees and CSCS fees will be restored effective 25th July 2019.

“Thank you for your valued patronage,” a notice sent to investors by one of the stockbrokers in Lagos and obtained by Business Post said.

The NSE had in a circular dated July 10, 2019 and titled NSE/RD/BDR/CIR5/19/07/10 informed stockbrokers of the resumption of the VAT payment.

“Please refer to our circular with reference BDR/CIR/GOI/10/14 dated 27 October 2014 on the above subject matter (attached as Appendix A); and the Value Added Tax (VAT) Exemption of Commissions on Stock Exchange Transactions Order (Order) granted by the Coordinating Minister for the Economy and Honourable Minister of Finance in 2014. (See, Official Gazette of the Federal Republic of Nigeria: No. 95, Vol. 101 issued on 30 July 2014).

“The Order which became effective on 25 July 2014 is valid for a period of five (5) years, and thus the exemption granted in the Order is set to expire on 24 July 2019.

“To that extent, all Dealing Members of the Nigerian Stock Exchange are to note that effective 25 July 2019, barring any further extensions from the Federal Government:

“i. VAT is to be charged on all commissions applicable to capital market transactions. These are commissions: a. earned by Dealing Members on traded values of shares; and b. payable to The Nigerian Stock Exchange (NSE) and the Central Securities Clearing System Plc. (CSCS);

“ii. The CSCS will automate the deduction of VAT charged on commissions payable to The NSE and the CSCS; and

“iii. Dealing Members are required to resume the deduction of VAT on commissions earned.

“Consequently, Dealing Members are required to engage their software vendors for the automation of VAT deductions, and communicate to their clients the above ahead of the effective date.

“Furthermore, Dealing Members are reminded to ensure that the VAT charged on the commissions earned are remitted to the Federal Inland Revenue Service (FIRS) as and when due; and that the corresponding evidence of remittance is retained for future reference,” the circular from the NSE last week had stated.

However, some investors are calling for an extension of the five percent VAT exemption, saying it would further encourage more people to consider joining the stock market at this moment.

Business Post reports that in 2014, when the federal government introduced the initiative, it was to encourage more investors into joining the capital market.

But some investors want this to continue for another five or three years.

“Government should consider extending the VAT exemption for another five or three years. The present state of the economy in Nigeria is not encouraging investment and if this exemption is not restored, I can guarantee you that more people will exit the market,” an investor at the stock market, who identified herself as Modupe Adediran, informed our correspondent.

“Since I received the notification from my stockbroker last week, I have been in a thinking mode. I cannot just imagine paying 5 percent tax on any transaction I execute in the trading of shares in my portfolio. The NSE should just fight for us by convincing the federal government to extend the exemption for another period,” another investor, who asked not to be named, told Business Post on Monday.

An official of one of the leading stockbrokers in the country, who begged for anonymity, said their hands were tied on this issue.

“There is nothing we can actually do concerning this matter because we received a circular to adhere to the directive. The best we can do to attract more investors or clients is to slightly reduce what we charge as commission. Asides that, there is nothing we can do,” the official said.

Business Post learned that the exemption can remain for another period except President Muhammadu Buhari appoints a Minister of Finance, which is likely not possible before July 24 because such person would have to be screened and confirmed by the Senate.

However, when a Finance Minister is eventually appointed by the President, the exemption can still be brought back.

By Adedapo Adesanya

Debt has emerged as a fast-growing asset class for the startup funding landscape in Africa, according to a new report by the African Private Capital Association (AVCA).

The 2025 Private Capital Activity in Africa report showed that Africa emerged as the only global region to record growth in private capital deal volume in 2025, underscoring the continent’s resilience amid a challenging global investment climate.

For startups, raising funds signals validation of their business model, market potential, and growth trajectory, while also providing the financial runway needed to scale operations, invest in innovation, and compete effectively. This can be done via a number of means, including bootstrapping, venture capital, private equity, debt financing, crowdfunding, accelerators, grants, corporate investments, initial public offerings (IPOs), and revenue-based financing, among others.

The data showed that private debt emerged as a fast-growing asset class, with deal volumes surging by 57 per cent year-on-year.

The growth was driven largely by the rising use of venture debt, positioning private debt alongside private equity and venture capital as a key financing channel in Africa.

The report put total investment at $5.1 billion, reflecting a slight dip in value but sustained investor appetite across the continent. The data showed that deal activity rose by 8 per cent year-on-year to 530 transactions, even as global deal volumes declined by 7 per cent.

IPOs also saw modest growth, with four listings completed during the year.

Domestic investors played a critical role in driving liquidity, accounting for 68 per cent of private capital acquisitions.

International investors made up the remaining 32 per cent, led by Asian strategic buyers seeking to expand their footprint in African markets.

The report highlighted a shift in strategy among fund managers, who increasingly focused on smaller mid-market deals as global financial conditions tightened.

Transactions valued between $50 million and $99 million doubled during the year, signalling a move away from larger, capital-intensive investments.

Sectoral activity remained dominated by financial services, particularly fintech, which accounted for 82 per cent of transactions within the sector.

The information sector ranked as the second most active, supporting investments across finance, healthcare, retail and logistics.

Regionally, Southern Africa maintained its position as the most active investment hub, while East and North Africa recorded strong performances, buoyed by growth in energy and information technology investments.

Africa’s exit market also showed significant improvement, with 81 exits recorded in 2025, representing a 27 per cent increase from the previous year and the second-highest level on record.

This contrasted sharply with a 15 per cent decline in global exit activity over the same period.

Trade buyers remained the dominant exit route, accounting for 38 per cent of transactions, while sponsor-to-sponsor deals reached a record 26 per cent, reflecting increased depth in the secondary market.

Despite the strong deal and exit performance, fundraising declined by 34 per cent year-on-year to $2.7 billion, mirroring global liquidity pressures.

Development finance institutions remained central to the ecosystem, contributing 64 per cent of total commitments.

However, domestic capital continued to deepen, with African institutional investors accounting for 21 per cent of commitments.

Sovereign wealth funds and pension funds led this trend, reflecting a growing shift towards locally sourced capital.

Commenting on the findings, AVCA chief executive, Mrs Abi Mustapha-Maduakor, said the data reflects a continent increasingly decoupling from global investment headwinds.

“This year’s report tells a clear story: Africa is decoupling from the global slowdown. Stronger exit performance, deeper participation from domestic institutional capital, and sustained commitments from development finance institutions all point to a maturing ecosystem,” she said.

She added that the momentum is expected to build further as investors increase exposure to sectors driving Africa’s next phase of economic transformation.

By Adedapo Adesanya

Four price gainers buoyed the NASD Over-the-Counter (OTC) Securities Exchange by 0.75 per cent on Thursday, March 26.

During the session, FrieslandCampina Wamco Nigeria Plc gained N8.87 to sell at N110.00 per unit compared with the previous day’s N101.13 per unit, Golden Capital Plc rose by 63 Kobo to N13.00 per share from N12.37 per share, Geo-Fluids Plc appreciated by 29 Kobo to N3.18 per unit from N2.89 per unit, and Industrial and General Insurance (IGI) Plc increased by 2 Kobo to 52 Kobo per share from 50 Kobo per share.

As a result, the market capitalisation added N18.91 billion to close at N2.531 trillion versus the previous session’s N2.512 trillion, and the NASD Unlisted Security Index (NSI) grew by 31.61 points to 4,230.46 points from 4,198.85 points.

The volume of securities went down by 84.4 per cent to 342,825 units from 2.2 million units, the value of securities decreased by 50.7 per cent to N23.0 million from N46.7 million, and the number of deals shrank by 27.0 per cent to 27 deals from 37 deals.

Central Securities Clearing System (CSCS) Plc remained the most traded stock by value on a year-to-date basis with 39.3 million units sold for N2.4 billion, followed by Infrastructure Guarantee Credit Plc with 400 million units valued at N1.2 billion, and Okitipupa Plc with 6.5 million units traded for N1.2 billion.

Resourcery Plc was the most traded stock by volume on a year-to-date basis with 1.1 billion units worth N415.7 million, followed by Infrastructure Credit Plc with 400 million units exchanged for N1.2 billion, and Geo-Fluids Plc with 133.0 million units transacted for N511.1 million.

After spending time reviewing the FRTX website, its platform pages, and the company’s public disclosures, my impression is that FRTX is trying to present itself not just as a brokerage brand with a landing page, but as a structured trading service built around a browser-based platform, analytics, onboarding flow, and client support. That matters because with newer financial brands, the real question is rarely whether the homepage looks polished. The real question is whether the service has enough visible structure behind the branding to feel like an actual operating environment rather than a marketing shell. In FRTX’s case, there is enough public material on the site to form a practical first impression.

The platform itself is clearly one of the central selling points. FRTX Web is presented as a modern browser terminal for CFD trading, designed to work without mandatory downloads or long setup. The site emphasizes direct browser access, desktop and mobile usability, a quick trading panel, real-time quotes in the order book, MarketCheese forecasts, a MarketCheese economic calendar, and built-in indicators for market analysis in the mobile version. From a product-review perspective, that is a sensible combination. It tells me the company understands that many users want access, analysis, and execution in one place without installing heavy software first.

What also stood out to me is that FRTX is not positioning the platform as a bare terminal. The broader website connects the trading interface to supporting sections such as Analytical Tools, Trading Ideas, the Economic Calendar, Tutorials, News and Views, FAQ, and Online Support. In practice, that gives the impression of a service trying to build a full client environment rather than relying on the terminal alone to do all the work. From a reviewer’s standpoint, that is usually a better sign than when a broker has a flashy login page but very little else around it.

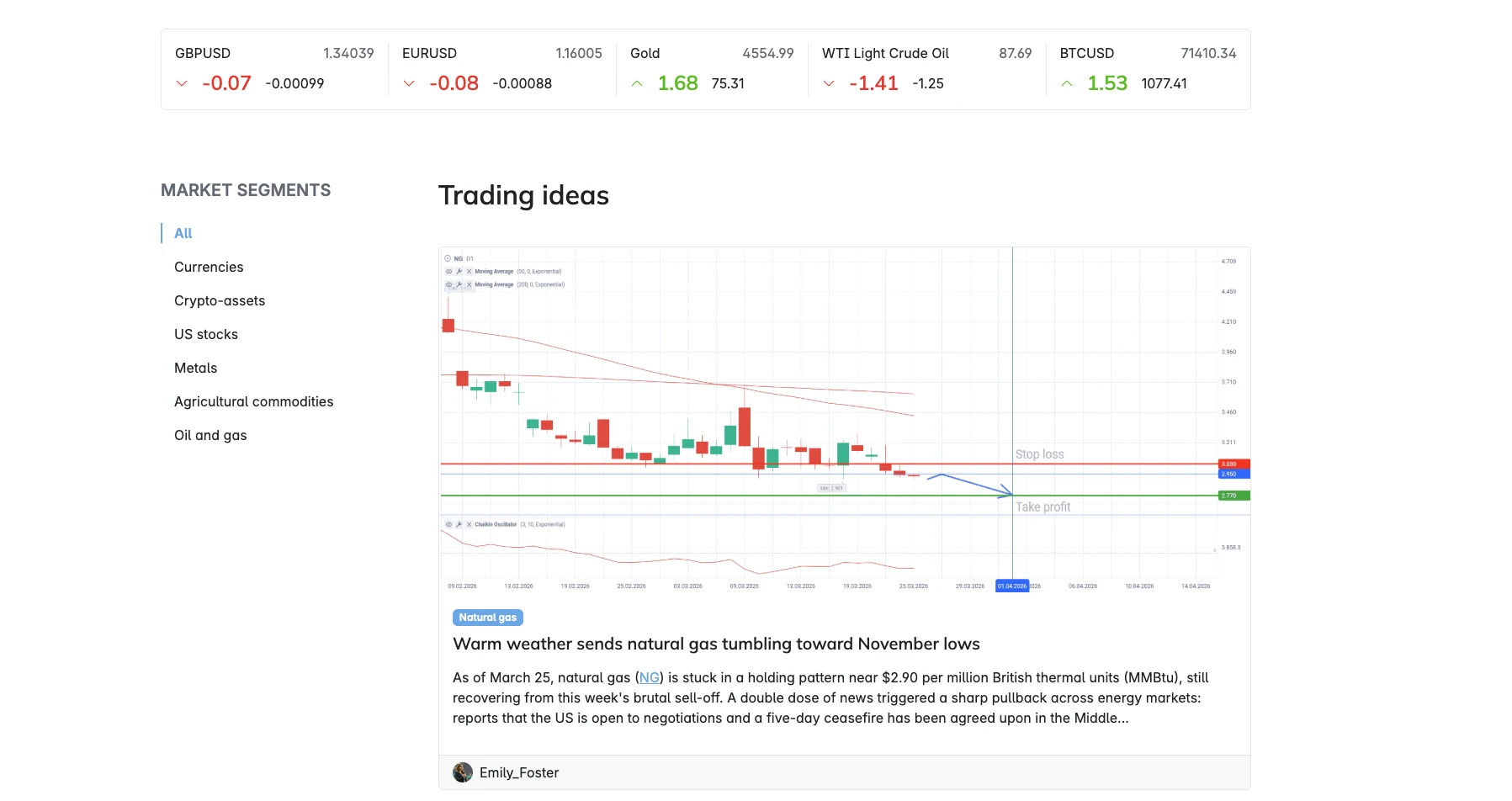

Another point in favor of the platform narrative is that FRTX does not present the terminal in isolation. The website ties the platform to a broader analytical environment. On the Analytical tools page, FRTX describes its Chart tool as a space to build lines and levels, use indicators, and analyze market behavior. The same section includes Market watch, described as a widget for tracking grouped instruments and price dynamics across different periods. This makes the platform look less like a standalone order-entry screen and more like the center of a wider trading workspace.

In terms of usability, the platform pitch is fairly direct. FRTX says the terminal can be launched on PC or in a mobile browser, with no need to download an app, and describes it as fully customizable. The homepage repeats the same practical advantages: quick start without pre-installation, access in any browser, color scheme customization, market-analysis tools, and protection from DDoS attacks. That is the kind of language I would expect from a company trying to appeal to users who care less about technical ceremony and more about speed of access and a clean workflow.

The award messaging is also very visible, and it is part of the platform story whether one likes awards or not. On the trading platform page, FRTX states that the platform received “Best Trading App” at Money Expo Mexico 2025 and “Best Trading Platform” at Wiki Finance Expo 2023 in Sydney. The homepage separately repeats the “Best Trading App of 2025 at Money Expo Mexico” line. I would not treat awards alone as the basis for judgment, but in a review they are still relevant because they show how the company is choosing to position its platform publicly.

Another point worth mentioning is the technology layer behind the experience. Based on the platform structure, browser-first workflow, integrated analysis modules, and the overall execution logic, FRTX appears to be using a mature software product from one of the established players in the trading technology market rather than trying to pass off a rough in-house prototype as a full solution. For users, that is generally a better look. It suggests the company is building on proven market infrastructure instead of improvising where stability matters most. This is an inference from the platform setup and feature mix rather than a direct statement published by FRTX, but it is a meaningful one when assessing the overall product presentation.

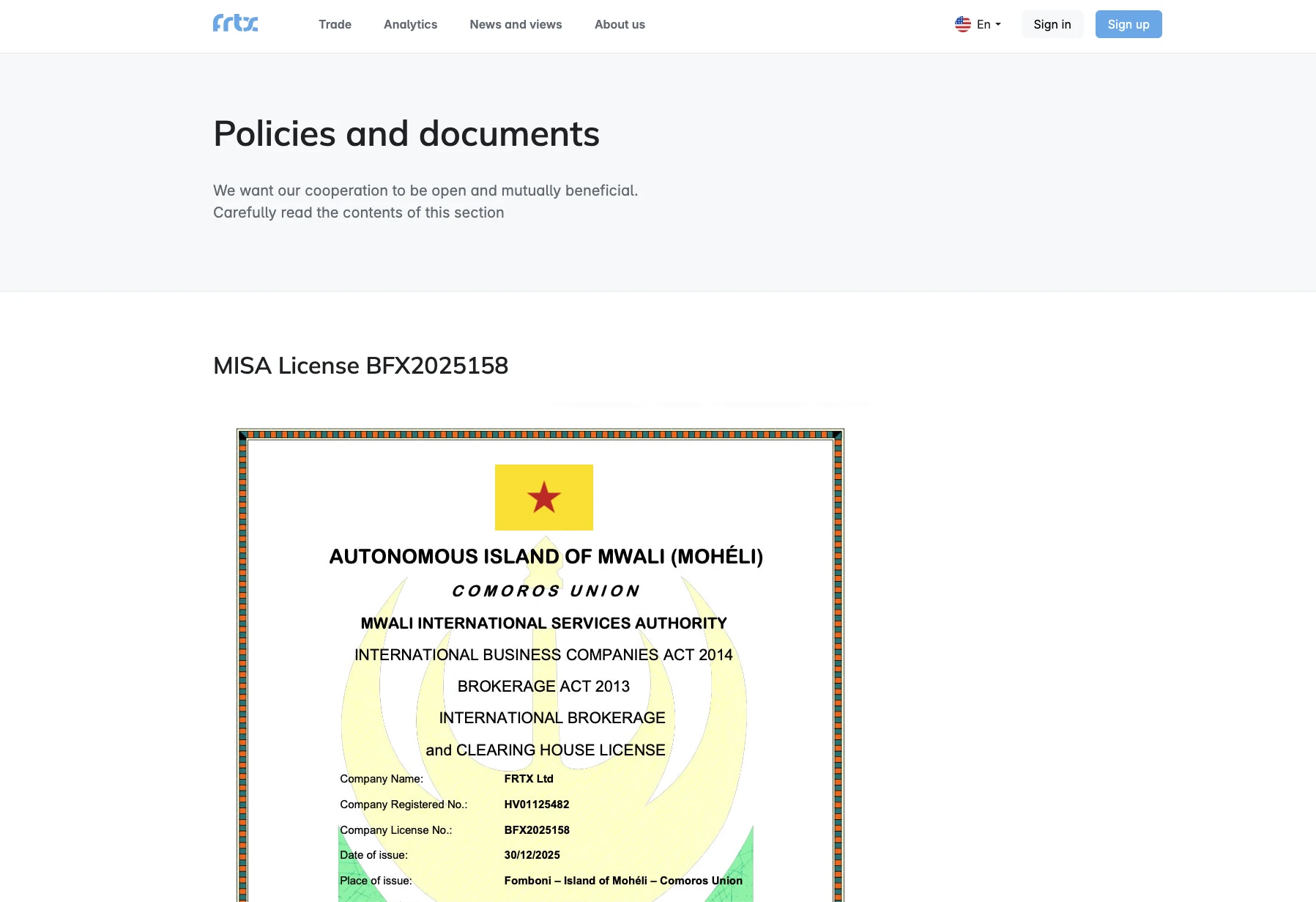

What strengthens the credibility of the overall picture is that FRTX does not rely only on platform marketing. The company also publishes public legal and licensing identifiers on the website. According to the platform page footer, the FRTX brand and the names frtx.global, frtx.org, and FRTX Web are owned and operated by FRTX Ltd, registered under number HV01125482 and licensed by the Mwali International Services Authority as an international brokerage company under license number BFX2025158. In a review context, this matters because it gives readers something concrete to verify beyond slogans and design.

The onboarding structure on the website also looks reasonably coherent. FRTX presents a path that starts with sign-up, continues through verification, then moves to account opening, funding, platform access, and eventually withdrawals. The support page adds two visible contact routes: the internal request system for clients and a callback form on the website. That does not automatically answer every operational question, but it does make the service feel more complete. A lot of online doubt around financial brands comes from missing practical detail, and here the company at least tries to show the user journey in a readable way.

That said, a serious review should keep one foot on the ground. FRTX also states that it does not provide services to citizens of the United States, Japan, Canada, Australia, the European Union, the United Kingdom, and several other jurisdictions. The site further includes a risk warning explaining that leveraged trading in CFDs and other derivatives involves a high level of risk and that losses may exceed the original deposit. In my view, this is the correct balance for a brokerage website: platform strengths and access convenience on one side, but a clear reminder that the product itself remains high-risk on the other.

My overall conclusion after reviewing the FRTX platform and website is that the brand is trying to position itself as a usable, modern, browser-first trading service with a visible support structure, integrated analytics, and publicly stated licensing details. The platform presentation is stronger than a generic brochure-style broker site, and the use of established trading technology gives the product a more mature feel. At the same time, the right way to read FRTX is not through hype but through verification: look at the legal entity, look at the license number, look at the service structure, and then decide whether the platform fits your needs and risk tolerance.

Disclaimer:

This material is for informational purposes only and does not constitute investment advice. Trading CFDs and other derivative instruments involves a high level of risk and may not be suitable for all users. Users should review the company’s terms, jurisdictional restrictions, and risk disclosures before using the service.

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism10 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz3 years ago

Showbiz3 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn