Economy

Nigeria, SA, 3 Others Attract 58% FDI Projects in Africa

By Dipo Olowookere

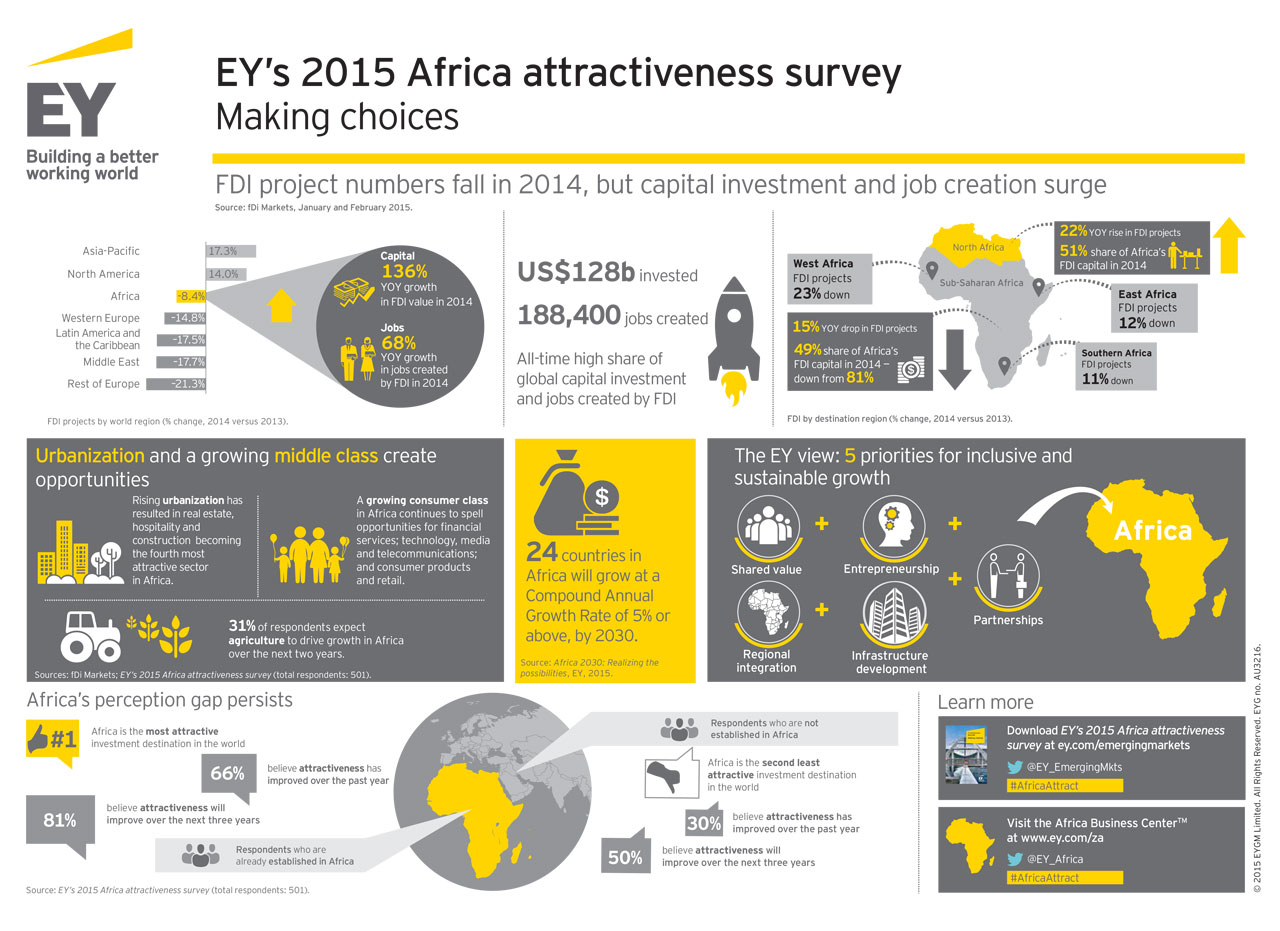

A total of 676 foreign direct investment (FDI) projects were attracted by Africa in 2016, out of which Egypt, Kenya, Morocco, Nigeria and South Africa (the key hub economies) collectively attracted 58 percent, an EY Africa Attractiveness report has disclosed.

However, the report named South Africa as the largest FDI hub in Africa.

The latest Africa Attractiveness, seen by Business Post, provided an analysis of FDI investment into Africa over the past ten years.

The 2016 data showed a decline of 12.3 percent from the total of number of FDI projects attracted the previous year by Africa.

Also, the FDI job creation numbers declined by 13.1 percent, but the capital investment rose by 31.9 percent during the period under review.

The surge in capital investment was primarily driven by capital intensive projects in two sectors, namely real estate, hospitality and construction (RHC), and transport and logistics. The continent’s share of global FDI capital flows increased to 11.4 percent from 9.4 percent in 2015. This made Africa the second-fastest growing FDI destination by capital.

Commenting on the report, Africa CEO at EY, Ajen Sita, noted that, “This somewhat mixed picture is not surprising to us. Investor sentiment toward Africa is likely to remain somewhat softer over the next few years.

This has far less to do with Africa’s fundamentals than it does with a world characterised by heightened geopolitical uncertainty and greater risk aversion. Investors with an existing presence in Africa remain positive about the continent’s longer-term investment attractiveness, but they are also cautious and discerning.”

Asia-Pacific investors are bullish on Africa

In a sign of ongoing diversification of Africa’s FDI investors, more than one fifth of FDI projects and more than half of capital investment into Africa came from Asia-Pacific in 2016, an all-time record. Most notably, Chinese FDI into Africa increased dramatically, making the country the single largest contributor of FDI capital and jobs in Africa in 2016.

Foreign investors refocus on Africa’s hub economies

South Africa remains the continent’s leading FDI destination, when measured by project numbers, increasing 6.9 percent. Morocco regained its place as Africa’s second largest recipient with projects up by 9.5 percent, followed by Egypt, which attracted 19.7 percent more FDI projects than the previous year.

New investment hubs appear in East and West Africa

Although foreign investors still favour the key hub economies in Africa, a new set of FDI destinations is emerging, with Francophone and East African markets of particular interest.

Despite having a 31.7 percent decline in FDI projects in 2016, and weak growth in recent years, West Africa’s second largest economy, Ghana, remains a key FDI market. The country’s improving macro-economic environment and strong governance track record has seen Ghana rise to fourth position in the EY Africa Attractiveness Index (AAI). The index was introduced in 2016, to measure the relative investment attractiveness of 46 African economies based on a balanced set of shorter and longer-term metrics.

Staying in West Africa, Cote d’Ivoire also features in the top 10 of the AAI, and with a 21.4 percent jump in FDI projects in 2016, this illustrates that it’s becoming a country more favoured by investors.

Also in the west, Senegal has emerged as a potential major FDI destination although this is not reflected in its current FDI numbers. It does however rank strongly on the AAI 2017, taking eighth position, due to its diverse economy, strong strides in macro-economic resilience and progress in improving its business environment.

Economy

SHR Miner offers free cloud mining services for BTC, XRP, and DOGE holders, with potential earnings of up to $6,770 or even more

As cryptocurrencies gain increasing popularity worldwide, more and more investors are seeking ways to generate a steady stream of passive income without the need for expensive hardware or specialized skills.

SHRMiner’s new free mining service allows holders of BTC, XRP, DOGE, LTC, and DOGE to easily earn passive income without expensive equipment or specialized technical knowledge.

In the rapidly evolving world of cryptocurrency, simplicity and high returns are paramount. For those seeking an accessible, entry-level investment method to generate a steady income with minimal effort, cloud mining undoubtedly presents a highly attractive option. This article will delve into the concept of cloud mining, using the leading brand SHRMiner as a case study to demonstrate how it can help you achieve daily earnings of $7,770—or even more.

The Appeal of Cloud Mining

Due to its ease of use and convenience, cloud mining has long been highly favored by cryptocurrency enthusiasts. Unlike traditional mining, it requires no expensive hardware, specialized technical expertise, or constant monitoring. Cloud mining simplifies the process, enabling anyone—regardless of their level of experience—to participate in the cryptocurrency revolution. Instead of investing in costly mining equipment and managing complex systems, users simply lease mining algorithms from remote data centers to earn a share of the profits.

Recently, the UK-based cloud mining platform SHRMiner officially launched a new “free cloud mining service.” Designed specifically for holders of mainstream cryptocurrencies—such as BTC, XRP, DOGE, LTC, and ETH—this service offers users a new opportunity to participate in cryptocurrency mining with no barriers to entry.

Meanwhile, SHRMiner has also launched a new mobile application, enabling users to manage their mining activities anytime, anywhere—effectively ushering in the “era of mobile mining.”

SHRMiner: The Perfect Blend of Laziness and Profit

SHRMiner takes the simplicity of cloud mining to the extreme, making it the ideal choice for novice users. The platform’s user-friendly interface ensures that even newcomers to the world of cryptocurrency can get started with ease. For SHRMiner, simplicity is not a weakness, but rather the path to success. As a pioneer in cloud mining services, SHRMiner operates over 150 mining farms worldwide—equipped with more than 600,000 mining devices powered entirely by modern renewable energy sources—and has earned the trust and support of over 5 million users thanks to its stable returns and robust security.

How can SHRMiner serve as a source of passive income?

The entire process takes just three simple steps to start earning income:

- Register an Account

By visiting the SHRMiner official website, users can register a free account in less than 2 minutes and receive a $15 sign-up bonus. This bonus helps users quickly experience the platform’s services and earn $0.60 per day from the free trial contract.

- Select a Cloud Mining Plan

Choose a cloud mining plan that aligns with your needs and budget. The platform offers a wide range of flexible plans—ranging from $100 to $200,000—to accommodate the diverse investment goals of different users.

- Start Earning

Upon purchasing a contract, earnings are automatically settled within 24 hours, requiring no additional management or manual intervention. Users may withdraw their earnings to their cryptocurrency wallet addresses at any time to suit their needs, or they may choose to reinvest their profits to capitalize on the power of compound interest.

The primary advantage of this model lies in its significant lowering of the barrier to entry. Users need not research specific mining hardware models or hash rate configurations, nor do they need to set up their own system environments; they simply need to register an account, deposit assets, and select a mining plan to begin generating returns.

SHRMiner Platform Advantages:

⦁ Supports daily automatic settlements.

⦁ Requires no additional electricity or maintenance costs.

⦁ Utilizes advanced ASIC mining hardware, powered by renewable energy sources including hydroelectric, wind, and solar power.

⦁ Supports multi-currency mining: Earn major cryptocurrencies such as BTC, XRP, ETH, DOGE, USDC, USDT, SOL, LTC, BCH, and more.

⦁ Features SSL encryption and DDoS protection, along with a real-time earnings dashboard for convenient monitoring of mining performance.

⦁ 100% Remote Access: Enjoy full access without the need for physical hardware via the SHRMiner app or web browser, complemented by 24/7 online technical support.

⦁ Affiliate Program: Refer friends to earn commission rewards of up to 4.5%, with the opportunity to receive additional bonuses of up to 30,000.

Examples of Common Contracts:

| Contract Name | Price | Profit | Days | Principal+TotalReturn |

| NewUserExperienceAgreement | $100 | $4 | 2 | $100+$8 |

| Bitdeer Sealminer A2 Pro | $500 | $6.25 | 5 | $500.00 + $31.25 |

| Litecoin Miner L9 | $1000.00 | $13.00 | 10 | $1000.00 + $130 |

| Bitcoin Miner S21 XP Imm | $5000.00 | $70.00 | 25 | $5000.00 + $1750 |

| Bitcoin Miner S21e XP Hyd | $10000.00 | $150.00 | 35 | $10000.00 + $5250 |

| ANTSPACE HW5 | $50000.00 | $900.00 | 45 | $50000.00 + $40500 |

After purchasing a contract, earnings will be automatically credited to your account within 24 hours. (Hash rate, investment amount, duration, and earnings vary for different contracts. For more contract information, please visit the official SHRMiner website or click on “Contract Details” to view.)

Unimaginable money-making opportunities

What sets SHRMiner apart is its extraordinary daily passive income potential; users have the opportunity to earn $8,900—or even more—every day, thereby realizing their dream of getting rich online. Imagine generating substantial income without the need for constant effort or complex setups—that is precisely what SHRMiner offers.

Safety and Sustainability

In the mining sector, trust and security are paramount; SHRMiner fully recognizes this and places user safety at the forefront. Committed to transparency and legitimacy, SHRMiner ensures that your investments are protected, allowing you to focus on profitability. All mining facilities utilize clean energy, making our cloud mining operations carbon-neutral. By harnessing renewable energy, we safeguard the environment from pollution while delivering superior energy efficiency.

in short

If you are looking for ways to generate passive income, cloud mining is an excellent choice. When utilized effectively, these opportunities can help you effortlessly accumulate cryptocurrency wealth on “autopilot,” requiring only a minimal time commitment. At the very least, they should be far less time-consuming than any form of active trading. Passive income is the ultimate goal for every investor and trader, and with SHRMiner, maximizing your passive income potential has never been easier.

If you would like to learn more about SHRMiner, please visit its official website: https://shrminer.com

By Aduragbemi Omiyale

The implementation of a fully electronic registration process for capital market operators has been commenced by the Securities and Exchange Commission (SEC).

This is deployed through the regulator’s ePortal. It allows Capital Market Operators (CMOs) to complete designated registration processes online, covering application submission, regulatory review, approvals and communication of decisions, thereby eliminating manual processing for the services included in the current phase.

It was stated that the implementation is being carried out in phases to ensure a smooth transition for market participants while maintaining the stability and integrity of regulatory processes.

This system enables designated regulatory services to be completed entirely online as part of efforts to modernise Nigeria’s capital market and improve regulatory efficiency.

The current phase is limited to post-registration services for existing Capital Market Operators, as applications for the registration of new entrants into the Nigerian capital market are not yet covered.

According to the SEC, the commencement of electronic processing for new registration applications will be announced at a later date.

The commission stated that the commencement of this policy marks another milestone in its digital transformation agenda and its drive to build a technology-driven regulatory environment.

This initiative is expected to simplify regulatory interactions, reduce administrative bottlenecks, shorten processing timelines and provide applicants with greater visibility into the status of their applications.

It will also improve operational efficiency while strengthening regulatory oversight through standardised workflows, electronic documentation, secure digital record management and enhanced audit trails.

The SEC explained that the e-registration platform aligns with its strategic objective of leveraging technology to improve market efficiency, enhance the ease of doing business and deliver better services to stakeholders.

According to the regulator, beyond improving efficiency, the platform will enhance the integrity of regulatory processes by reducing delays associated with paper-based documentation and improving the quality of regulatory data for decision-making.

It noted that the digital platform would also provide a stronger foundation for regulatory analytics and future innovations aimed at improving oversight of Nigeria’s capital market.

“The new platform represents a major step towards creating a seamless digital regulatory ecosystem that enhances operational efficiency while strengthening regulatory effectiveness,” the agency said in a statement on Wednesday, urging operators to familiarise themselves with the new platform and comply with implementation timelines to ensure a seamless transition to the electronic registration process.

By Adedapo Adesanya

Dangote Petroleum Refinery has formally approached Nigeria’s Securities and Exchange Commission (SEC) to begin the regulatory process for its planned initial public offering (IPO), paving the way for what could become Africa’s largest stock market listing, according to a report by BusinessDay.

The newspaper reported that the refinery’s advisers are already working with company officials and the SEC to process the application, with the regulator expressing confidence that there are no obstacles likely to delay the transaction.

Speaking in an interview with BusinessDay, the Director-General of the SEC, Mr Emomotimi Agama, said the commission stands ready to address any issues that may arise during the approval process.

“If any issue arises, SEC will resolve it. That is why the SEC exists,” Mr Agama was quoted to have said.

Although no official listing date has been approved, the refinery is still targeting a September debut on the Nigerian Exchange (NGX) Limited. There are also plans for a multi-African bourse listing.

The planned IPO is expected to rank among the largest equity offerings ever seen in Africa and would mark one of the most significant additions to Nigeria’s capital market in recent years.

The listing also aligns with ongoing efforts by regulators to encourage major privately owned companies to go public and deepen the country’s equity market.

The application comes after several months of preparatory engagements involving Dangote Refinery, its advisers and the SEC.

Mr Agama noted that the company’s early engagement with the regulator has helped streamline the approval process, adding that the commission intends to encourage similar collaboration for future listings.

Meanwhile, the SEC has concluded investigations into the unauthorised promotion of the refinery’s proposed IPO by some market participants before regulatory approval had been obtained.

According to Mr Agama, sanctions are being imposed on those found to have breached the rules, although he declined to identify the affected entities.

This comes after the company raised about $2.5 billion has been raised by from its private equity placement.

The exercise attracted broad participation from international and African institutional investors, sovereign-related investment vehicles, development finance institutions, strategic partners, and individual investors.

Notable participants included the Africa Finance Corporation (AFC) and India Infra Buildco, an investment vehicle facilitated by the African Export-Import Bank (Afreximbank), reflecting deep and diversified confidence in DPRP’s long-term prospects.

The transaction is believed to be Africa’s largest publicly disclosed primary equity private placement, marking a significant milestone in the history of the organisation and demonstrating strong investor confidence in the refinery’s long-term growth strategy, including raising its current capacity from 700,000 barrels per day to 1.4 million barrels per day.