Economy

Nigeria’s Inflation Bites Harder, Jumps to 20.52% in August 2022

By Adedapo Adesanya

Nigeria’s inflation hit an almost 17-year high as the price of goods and services surged further by 20.52 per cent in the month of August 2022 from 19.64 per cent recorded in the previous month.

This represents the highest rate since September 2005, according to the Consumer Price Index (CPI) report by the National Bureau of Statistics (NBS) on Thursday.

The data showed that Nigeria’s CPI rose by 20.52 per cent year-on-year in August 2022 and on a month-on-month basis, the index rose by 1.77 per cent compared to the 1.82 per cent increase recorded in the previous month.

Also, the urban inflation rate stood at 20.95 per cent, 3.36 per cent higher than the 17.59 per cent recorded in August 2021. The rural inflation rate in August 2022 was 20.12 per cent on a year-on-year basis; 3.69 per cent higher than the 16.43 per cent recorded in August 2021.

In the report, the NBS disclosed that food inflation rose to 23.12 per cent in August 2022, representing a 1.1 percentage point increase compared to 22.02 per cent recorded in the previous month.

On a month-on-month basis, the food inflation rate stood at 1.98 per cent, 0.07 per cent lower than the 2.04 per cent recorded in the previous month.

According to the NBS, the rise in food inflation was caused by increases in prices of bread and cereals, food product, potatoes, yams, and other tubers, fish, meat, oil, and fat.

Meanwhile, the average annual rate of food inflation for the 12-month period ending August 2022 over the previous 12-month average was 19.02 per cent, which was a 1.48 per cent decline from the average annual rate of change recorded in August 2021 (20.50 per cent).

The ‘’All items less farm produce’’ or core inflation, which excludes the prices of volatile agricultural produce stood at 17.20 per cent in August 2022 on a year-on-year basis; up by 0.94 per cent when compared to 16.26 per cent recorded in July 2022.

On a month-on-month basis, the core inflation rate was 1.59 per cent in August 2022. This was down by 0.17 per cent when compared to 1.75 per cent recorded in July 2022.

Notably, the highest increases were recorded in prices of Gas, Liquid fuel, Solid fuel, Passenger transport by road, Passenger transport by Air, fuel and lubricants for personal transport equipment, Cleaning, Repair, and Hire of clothing.

In August 2022, all items inflation rate on a year-on-year basis was highest in Ebonyi (25.33 per cent), Rivers (23.70 per cent), Bayelsa (23.01 per cent), while Jigawa (17.30 per cent), Borno (17.56 per cent) and Zamfara (18.04 per cent) recorded the slowest rise in headline Year-on-Year inflation.

Meanwhile, food inflation on a year-on-year basis was highest in Kwara (30.80 per cent), Ebonyi (28.06 per cent) and Rivers (27.64 per cent), while Jigawa (17.77 per cent), Zamfara (18.79 per cent) and Oyo (19.80 per cent) recorded the slowest rise on year-on-year food inflation.

By Adedapo Adesanya

Crude oil deliveries from the Nigerian National Petroleum Company (NNPC) Limited to the Dangote Petroleum Refinery doubled in March, boosting prospects for improved fuel availability.

This was revealed by the chief executive of Dangote Industries Limited, Mr Aliko Dangote, on Tuesday, when he received the Deputy Secretary-General of the United Nations, Mrs Amina Mohammed, at the industrial complex in Ibeju-Lekki, Lagos.

While speaking on feedstock supply, Mr Dangote commended the NNPC for increasing crude deliveries to the refinery in March, noting that volumes rose to 10 cargoes—six supplied in Naira and four in Dollars—to support domestic fuel availability, according to a statement by the Refinery.

“Last month, they gave us six cargoes for Naira and four cargoes for Dollars,” he said.

Despite the improvement, Mr Dangote noted that the supply remains below the 19 cargoes required for optimal operations, with the refinery continuing to bridge the gap through imports from the United States and other African producers.

He also expressed concern over the unwillingness of international oil companies operating in Nigeria to sell to the refinery, stating that their preference for selling crude to traders forces it to repurchase at higher costs, with broader implications for the economy.

Mr Dangote added that the refinery is seeking increased access to domestically priced crude under local currency arrangements as part of efforts to moderate fuel costs and enhance long-term energy and food security across the continent.

On her part, Mrs Mohammed underscored the strategic importance of Dangote Industries Limited -particularly Dangote Fertiliser Limited—in addressing Africa’s mounting food security challenges, while calling for stronger global partnerships to scale its impact.

Mrs Mohammed said the United Nations would prioritise amplifying scalable solutions capable of mitigating the continent’s food crisis, describing Dangote’s integrated industrial model as a critical pathway.

“I think the UN’s job here is to amplify and to put visibility on the possibilities of mitigating a food security crisis, and this is one of them,” she said. “I hope that when we go back, we can continue to engage partners and countries that should collaborate with Dangote Industries.”

By Aduragbemi Omiyale

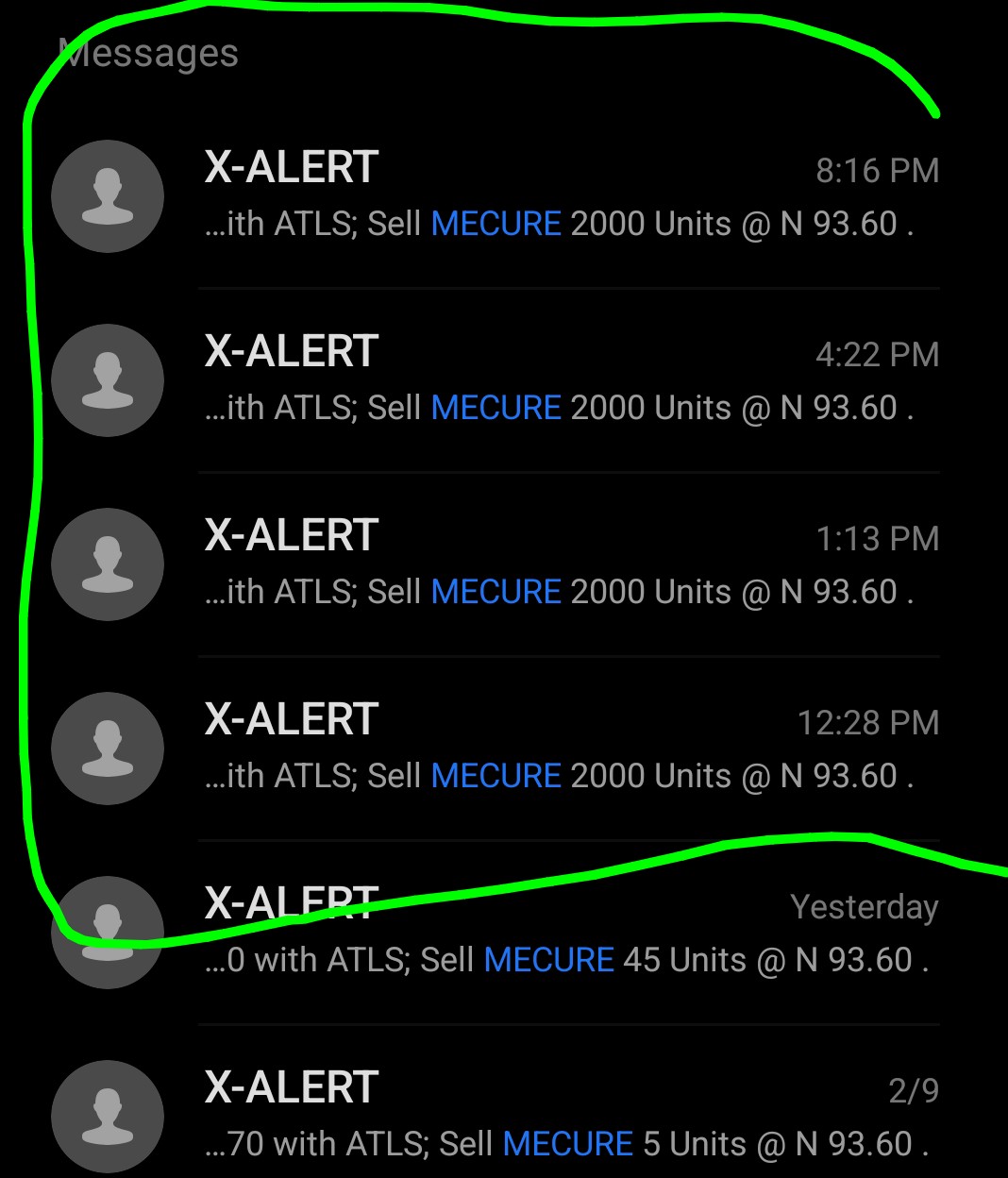

The Securities and Exchange Commission (SEC) has approved a 50 per cent hike in the X-Alert service fee per transaction in the Nigerian capital market.

The X-Alert fee is a flat rate charged for sending real-time SMS/email notifications for transactions to investors from both buy and sell sides.

It was introduced by the Nigerian Exchange (NGX) to replace percentage-based charges, aimed at increasing transparency and reducing total transaction costs for investors.

Investors were earlier charged N4 per SMS, but the country’s apex capital market regulator has approved a 50 per cent increase in X-Alert service fee, meaning the new rate is N6 per SMS.

Business Post gathered from one of the players in the ecosystem that the effective date for the new price was Thursday, March 26, 2026.

“We wish to inform you of a revision to the X-Alert (SMS) service fee applicable to transactions executed on the Nigerian Exchange (NGX).

“Following approval by the Securities and Exchange Commission (SEC), the X-Alert fee has been reviewed upward from N4.00 to N6.00 per transaction,” the notice sighted by this newspaper read.

By Adedapo Adesanya

Nigeria’s economy is projected to remain resilient in the face of mounting global uncertainties, with the World Bank forecasting a 4.2 per cent growth rate in 2026.

However, the global lender has warned that rising fuel costs and persistent inflation, worsened by geopolitical tensions in the Middle East, could undermine household incomes and slow poverty reduction.

Speaking in Abuja, the bank’s lead economist for Nigeria, Mr Fiseha Haile, noted that while the ongoing US-Israel-Iran conflict has pushed up prices, overall economic activity has remained largely intact.

“Overall business activity has been expanding over the past few months, suggesting the impact on growth has been relatively contained. But the shock is still being felt through higher inflation,” Mr Haile said.

According to him, business activity has continued to expand in recent months, indicating that the broader impact on growth has been “relatively contained,” even as inflationary pressures intensify.

Nigeria’s inflation rate, though significantly reduced from around 33 per cent in December 2024 to 15.06 per cent in February 2026, remains elevated compared to regional peers.

“Inflation is still elevated and under increasing pressure, and that poses risks to incomes and poverty reduction,” Mr Haile said.

The renewed surge in fuel prices, reportedly rising by over 50 per cent during the Iran conflict, has had a ripple effect on transportation, food, and production costs, amplifying the cost-of-living crisis.

The World Bank urged Nigerian authorities to adopt prudent macroeconomic measures, including tightening monetary policy, avoiding blanket subsidies, and saving windfalls from higher oil prices to strengthen fiscal buffers.

It also recommended reconsidering restrictions on fuel imports as a potential tool to ease inflationary pressures.

The economic reforms under President Bola Tinubu — including the removal of fuel subsidies, exchange rate unification, and tax restructuring — were acknowledged as ambitious steps aimed at stabilising the economy.

These reforms have contributed to improved external buffers, with rising foreign exchange reserves and reduced volatility.

Additionally, Nigeria’s fiscal deficit stood at 3.1 per cent of GDP in 2025, while the debt-to-GDP ratio declined for the first time in a decade.

Yet, the World Bank cautioned that tighter global financial conditions could still pose risks to capital inflows, borrowing costs, and remittances.

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism10 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz3 years ago

Showbiz3 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn