Economy

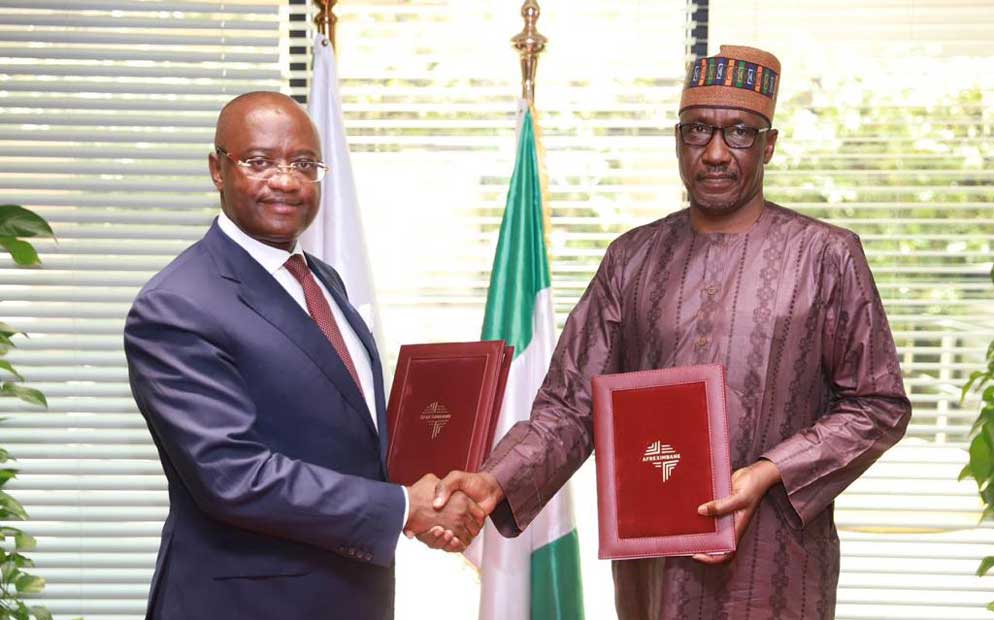

NNPC Gets Afreximbank $3bn Emergency Loan for Naira Stability

By Adedapo Adesanya

The Nigerian National Petroleum Company (NNPC) Limited and Africa Export-Import Bank (Afreximbank) have jointly signed a commitment letter and term sheet for an emergency $3 billion crude oil repayment loan.

The signing, which took place on Wednesday, August 16, at the bank’s headquarters in Cairo, Egypt, will provide some immediate disbursement that will enable the NNPC Limited to support the federal government in its ongoing fiscal and monetary policy reforms aimed at stabilising the exchange rate market.

The country is about $3 billion deep in debt to trading houses and oil majors for crude oil swap arrangements, through which the country imports petroleum products.

The country is also said to be over six months behind schedule for the repayment in crude.

The direct sale direct purchase (DSDP) initiative is an agreement that allows the sale of crude oil to refiners, who will in turn supply the country with an equivalent worth of petroleum products.

Through the DSDP arrangement, Nigeria exchanges petroleum products for crude cargoes with major trading houses and international oil majors, including BP, TotalEnergies, Vitol, and Mercuria.

The decision to pay cash for petrol imports follows the federal government’s removal of petrol subsidy and the subsequent issuance of petrol importation licences to interested companies — displacing NNPC Limited as the sole importer of petrol.

The country has also faced recent headwinds in the forex market after the Central Bank of Nigeria (CBN) liberalised the local currency that included collapsing all segments of the foreign exchange market into the Investors and Exporters’ (I&E) window and the reintroduction of the “willing buyer, willing seller” model at the window.

However, this didn’t lead to the elimination of the other markets as illiquidity at the official market sent those in need of the FX to other alternative segments like the parallel market and the Peer-2-Peer (P2P) segment.

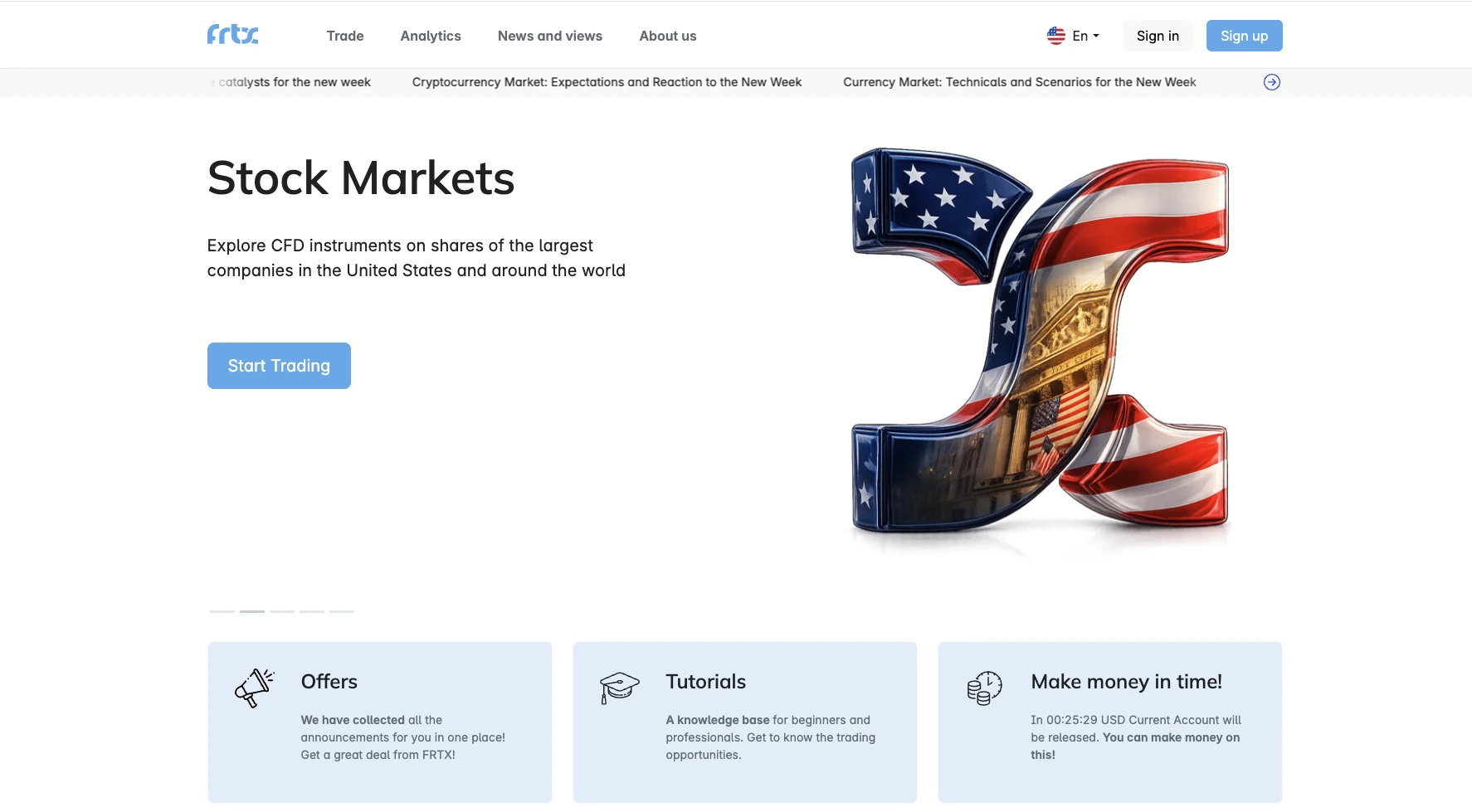

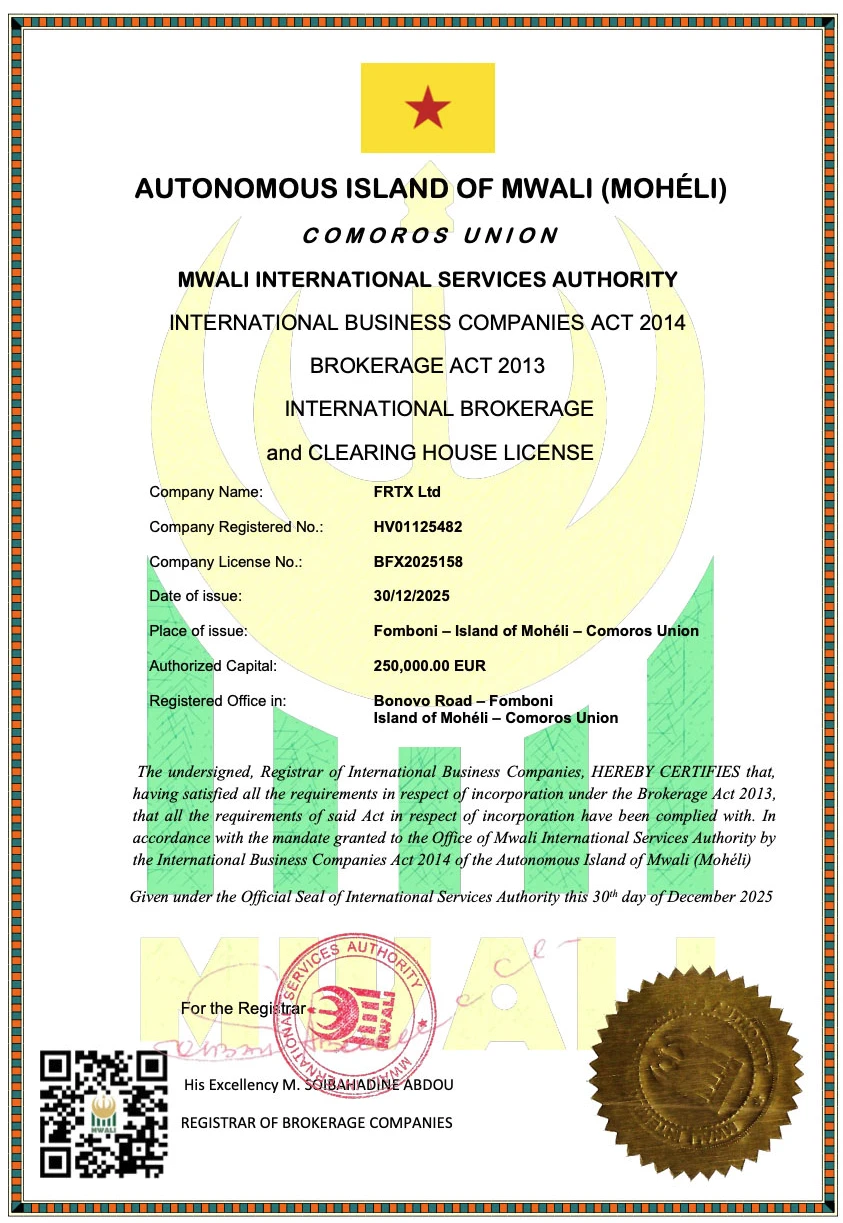

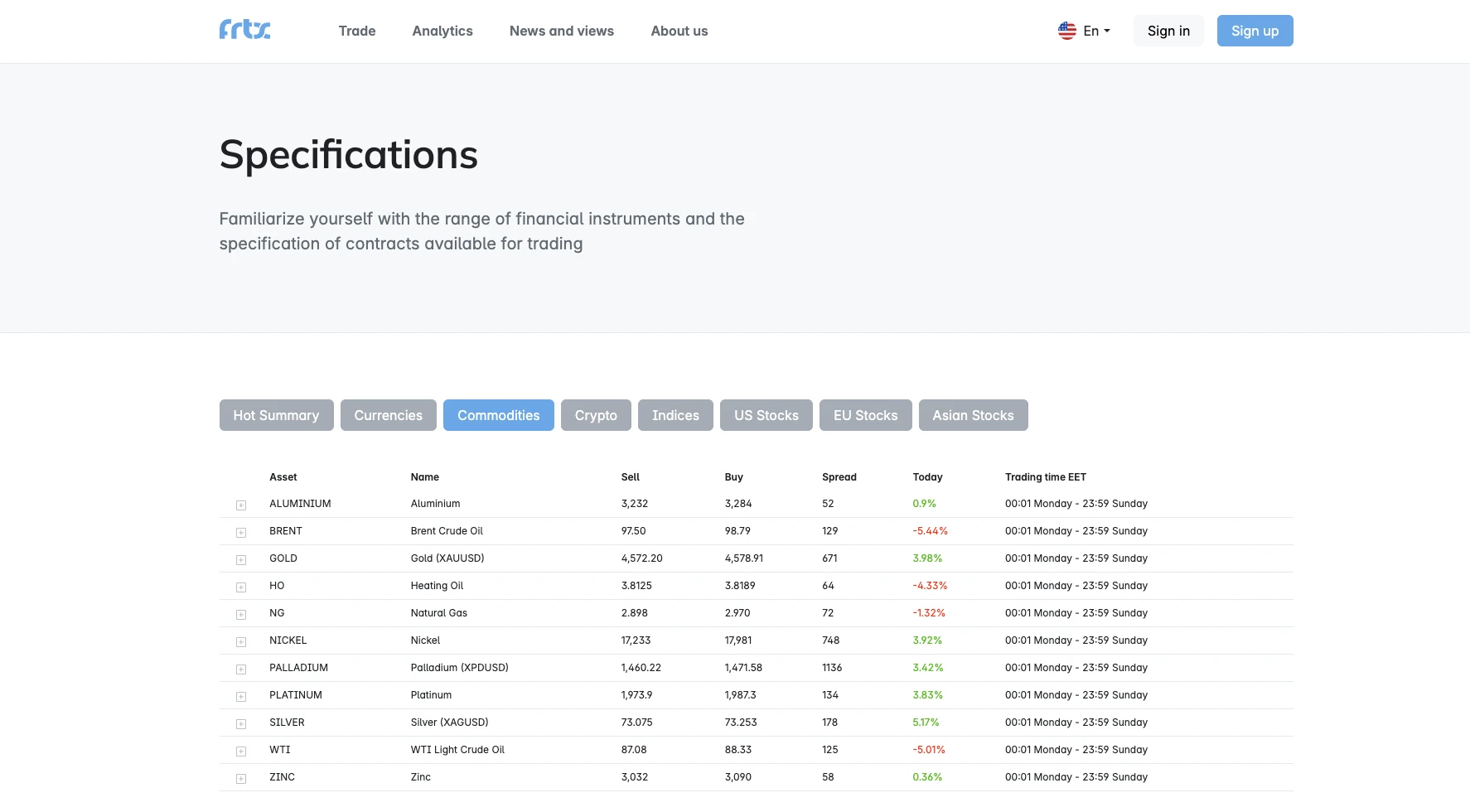

When FRTX is viewed through the lens of product structure rather than emotion, the service presents a fairly clear offering: browser-based CFD trading, a broad mix of instruments, account-type selection based on client goals, and an additional layer of conditions for more active users. On its website, the company states that the FRTX brand and its related resources are operated by FRTX Ltd, registered under number HV01125482 and licensed by the Mwali International Services Authority as an international brokerage company under license number BFX2025158.

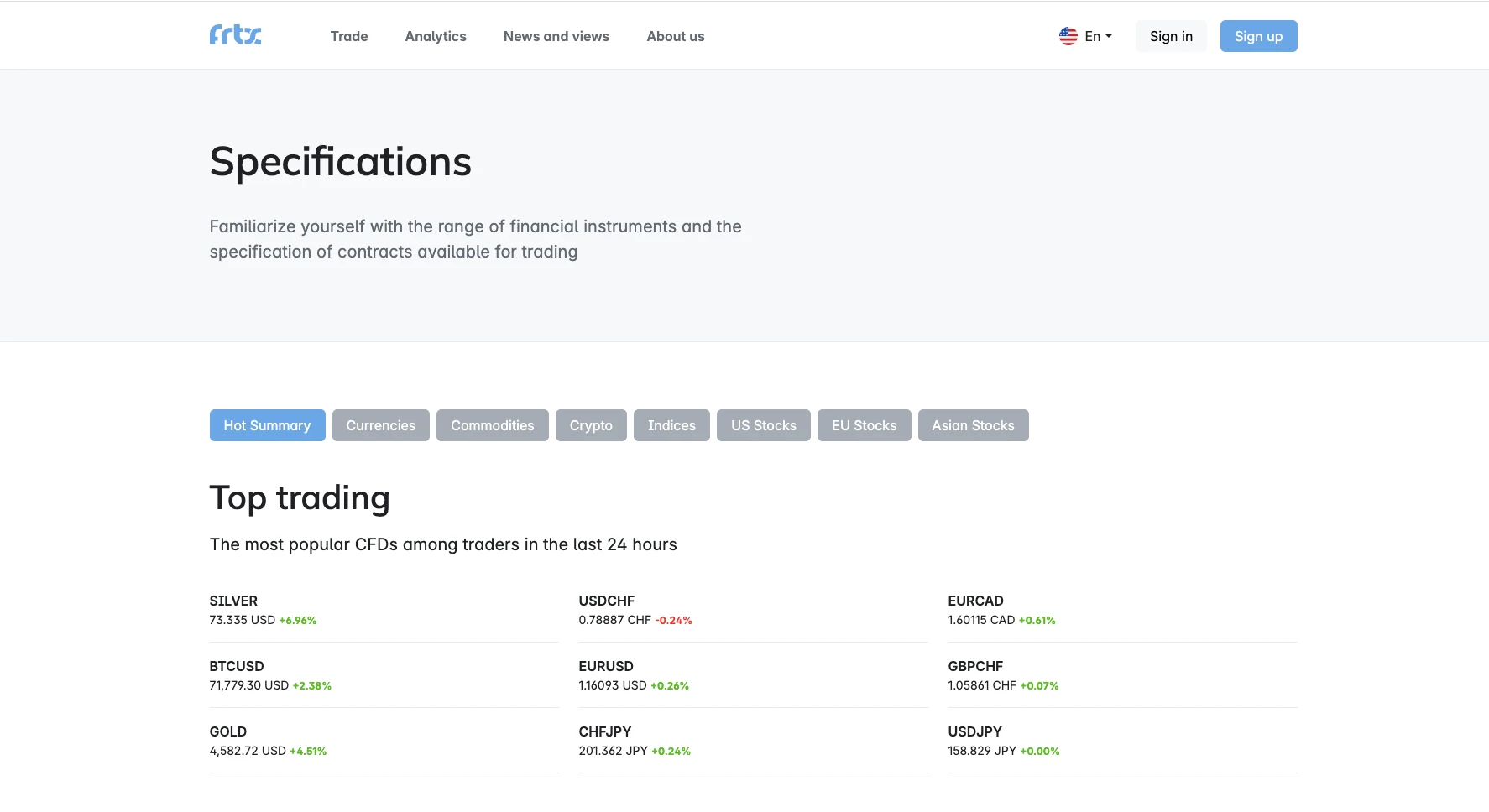

The same website also highlights 200+ trading instruments, browser-based access, and leverage from 1:10 to 1:1000 upon request, which sets the framework for the overall product model.

In terms of market coverage, FRTX appears to offer a fairly broad CFD lineup. On the “How We Work” page, the company specifically lists CFDs on commodities, metals, currencies, crypto-assets, and securities. The descriptions in those sections mention natural gas and oil, gold, silver, and palladium, currency pairs, widely known crypto-assets such as Bitcoin, Ripple, and Ethereum, as well as shares of major global companies. The homepage complements that picture with a broader statement about trading CFDs on stocks, commodities, currencies, and other financial instruments. For a review article, this is a meaningful advantage: the product basket does not look decorative, but genuinely multi-layered.

It is also worth noting that FRTX does not separate the platform from the trading conditions as if they were two unrelated worlds. FRTX Web is presented as a browser-based solution for desktop and mobile devices with a quick trading panel, an order book with real-time quotes, built-in market forecasts, and an economic calendar. As a result, the instruments, the analytics layer, and the actual point of trade execution are presented as one integrated environment rather than a patchwork of disconnected functions. For a brokerage product, that creates a more cohesive impression: when the platform and the trading terms follow the same logic, the service feels more structured.

The account model is also presented without unnecessary theatrics. On the accounts page, the service does not try to sell a dozen dramatic account names. Instead, it keeps the idea simple: users select an account type based on their goals, while the differences between account types are reflected in additional benefits such as enlarged cashback, monthly interest, and bonuses on replenishment. The same section also outlines the onboarding path: registration, verification, opening a trading account, funding it, and then working through the platform. In a review context, this reads as a sign of product discipline: the focus is placed not on flashy labels, but on what the client actually receives depending on account level or activity.

As for the trading conditions themselves, FRTX’s public presentation focuses on several clear parameters. The website refers to floating spreads, low commissions, and leverage of up to 1:1000. It also emphasizes high liquidity, the ability to trade on both rising and falling prices of the underlying asset, and mentions instant execution and fast withdrawals as part of the broader user proposition. In neutral analytical terms, this looks like an attempt to build a classic retail CFD model: a wide choice of markets, floating spreads, a relatively low commission barrier, and flexibility in leverage.

The loyalty program also remains a visible part of FRTX’s commercial logic rather than something hidden in the background. On the dedicated page, the company refers to bonuses of up to 100% on deposits, cashback of up to 100% of commissions for active traders, and monthly interest of up to 5% per month on available account balances. At the same time, the website includes an important qualification: the exact scale of these benefits depends on account type, current terms, and the loyalty program documentation, while the monthly interest feature is explicitly marked as not a banking product or service. For a review, this is a useful detail: the offer is presented in an attractive way, but not entirely without conditions and clarifications.

Taken together, FRTX appears, at the product-structure level, to be a service that aims to offer more than just one core function. It combines account selection, CFDs across several asset classes, browser-based trading, integrated analytics, and bonus mechanics for more active clients. That internal coherence is what creates the most favorable impression in a neutral review: the service does not look like a one-page offer, but rather like a more complete system with its own internal logic. The fact that the company also publishes its registration and licensing details on the website adds further weight to that presentation rather than relying on marketing language alone.

At the same time, the final assessment still has to remain grounded. FRTX operates in leveraged CFD trading, which means the strengths of its product structure always exist alongside the risk profile of the instrument itself. The website explicitly states that trading in financial markets and derivatives with leverage involves a high level of risk and may result in losses exceeding the initial deposit. That is why the strongest version of this review is not one that tries to label the service “perfect,” but one that describes it more precisely: FRTX appears to be a structured brokerage product with a broad CFD offering and a clearly organized conditions framework, but it should still be evaluated through the lens of the user’s own risk profile and careful reading of the company’s documentation.

This material is for informational purposes only and does not constitute investment advice. Trading CFDs and other leveraged derivative instruments involves a high level of risk and may not be suitable for all users.

By Adedapo Adesanya

The Nigerian Upstream Petroleum Regulatory Commission (NUPRC) has taken steps to ensure that approval for permits is done within hours of application to drive investments into the country’s energy sector

The upstream oil sector regulator is slashing the time it takes to approve applications to revive idle oil wells from weeks to hours as Nigeria, which is Africa’s top crude producer, seeks to take advantage of high energy prices triggered by the conflict in the Middle East.

Bloomberg quoted people familiar with the process as saying the country is also fast-tracking approvals for evacuations and barges at production facilities and export terminals to let barrels get to buyers quickly, as buyers turn to suppliers such as Nigeria and Angola on the African continent.

The US-Israel war on Iran and its countermeasures, including the blockade of the Strait of Hormuz, which handicapped about 20 per cent of crude and liquified natural gas (LNG), have driven oil prices above $100 per barrel.

Citing a spokesman from NUPRC, it was said “speedy approvals” were being given “for all activities that could increase production.”

The recent surge in applications has come from mostly local oil companies seeking to re-enter old wells, with the regulator cutting down an approval process that previously took anywhere from two to six weeks to encourage activities.

Repairing older or suspended wells for production is cheaper compared with drilling new wells, which can take years of planning, with any potential crude taking an average of four weeks to reach the surface.

This is coming after the chief executive of the Nigerian National Petroleum Company (NNPC) Limited, Mr Bayo Ojulari, said the country is ready to increase oil production by about 100,000 barrels per day over the next few months to make up for the crude shortfall resulting from the US-Israel war on Iran.

“We are building that capacity,” he said, though he added “we are not like Saudi (Arabia), but we can contribute,” he said on Monday.

By Adedapo Adesanya

Four stocks weakened the NASD Over-the-Counter (OTC) Securities Exchange by 0.22 per cent on Tuesday, March 24, with Friesland Campina Wamco Nigeria Plc leading the pack after shedding N7.83 to trade at N108.73 per share compared with the previous day’s N116.00 per share.

Further, Food Concepts Plc lost 37 Kobo to close at N3.00 per unit versus Monday’s closing price of N3.37 per unit, Riggs Ventures Plc depreciated by 10 Kobo to 90 Kobo per share from N1.00 per share, and Industrial and General Insurance (IGI) Plc dipped by 4 Kobo to 53 Kobo per unit from 57 Kobo per unit.

Consequently, the market capitalisation of the NASD bourse went down by N5.40 billion to N2.477 trillion from the previous session’s N2.482 trillion, and the NASD Unlisted Security Index (NSI) fell by 9.08 points to 4,140.30 points from 4,149.38 points.

Business Post reports that despite the loss, the trading platform witnessed the rise in the share prices of four securities, led by Okitipupa Plc, which gained N13.50 to sell at N250.00 per share compared with the previous day’s N236.50 per share. Central Securities Clearing System (CSCS) Plc added N2.61 to close at N78.94 per unit versus N76.33 per unit, First Trust Mortgage Bank Plc appreciated by 19 Kobo to N2.08 per share from N1.89 per share, and Impresit Bakalori Plc improved by 18 Kobo to N2.01 per unit from N1.83 per unit.

Tuesday’s trading data showed that the value of transactions increased by 518.9 per cent to N45.6 million from N7.37 million, and the volume of trades increased by securities rose by 126.34 per cent to 933,125 units from 412,260 units, while the number of deals went down by 9.4 per cent to 29 deals from 32 deals.

CSCS Plc remained the most traded stock by value (year-to-date) with 39.1 million units worth N2.4 billion, trailed by Infrastructure Guarantee Credit Plc with 400 million units valued at N1.2 billion, and Okitipupa Plc with 6.4 million units traded for N1.2 billion.

Resourcery Plc maintained its position as the most traded stock by volume (year-to-date) with 1.1 billion units exchanged for N415.7 million, followed by Infrastructure Credit Plc with 400 million units sold for N1.2 billion, and Geo-Fluids Plc with 131.2 million units transacted for N505.8 million.

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism10 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz3 years ago

Showbiz3 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn

Pingback: NNPC Gets Afreximbank $3bn Emergency Loan for Naira Stability – African Budget Bureau