Economy

President Obama’s Speech At US-Africa Business Forum

By US Department of State

Well, good morning, everybody! Let me begin by thanking Mayor Bloomberg — not just for the introduction but for the incredible work that Bloomberg Philanthropies is doing, not just in helping this event but for all the work that you’re doing in promoting entrepreneurship and development throughout Africa.

And I’d also like to thank our co-host, and a tremendous champion of investment and engagement in Africa — my great friend, Commerce Secretary Penny Pritzker.

I also want to welcome our partners from across Africa, including the many heads of state and government leaders who are with us. And I want to acknowledge Senator Chris Coons and leaders from across my administration, who share a profound commitment to expanding opportunity and deepening relationships between our countries.

Most importantly, I want to thank all of you — the business leaders, entrepreneurs, on both sides of the Atlantic, who are working very hard every single day to create jobs and to grow economies and to lift up our people.

Now, I gave a long speech yesterday. Some of you had to sit through it. I’m going to try to be a little more concise today. I’m here because, as the world gathers in New York City, we’re reminded that on so many key challenges that we face — our security, our prosperity, climate change, the struggle for human rights and human dignity, the reduction of conflict — Africa is essential to our progress. Africa’s rise is not just important to Africa, it’s important to the entire world.

Yes, too many people across the continent still face conflict and hunger and disease. And, yes, recent years have brought some stiff economic headwinds. And we have to be relentless in our efforts to end conflicts, and improve security and promote justice. At the same time, the broader trajectory of Africa is unmistakable. Thanks to many of you, Africa is on the move — home to some of the fastest-growing economies in the world and a middle class projected to grow to more than a billion customers. An Africa of telecom companies and clean-tech startups and Silicon savannahs, all powered by the youngest population anywhere on the planet.

As President, I’ve worked to transform our relationship with Africa so that we’re working together, as equal partners.

I’m proud to be the first American President to visit sub-Saharan Africa four times; the first to visit Ethiopia and speak before the African Union; the first to visit Kenya — which I think was obligatory. I would have been in trouble if I hadn’t done that. (Laughter)

I believe I’m also the first American President to dance the Lipala in Nairobi — or to try to dance the Lipala.

And wherever I’ve gone, from Senegal to South Africa, Africans insist they do not just want aid, they want trade.

They want partners, not patrons. They want to do business and grow businesses, and create value and companies that will last and that will help to build a great future for the continent. And the United States is determined to be that partner — for the long term — to accelerate the next era of African growth for all Africans.

And that’s why, over the past eight years, we’ve dramatically expanded our economic engagement. With your support, we renewed the African Growth and Opportunity Act for another decade, giving African nations unprecedented access to American markets.

We launched Trade Africa, so that African countries can sell goods and services more easily across borders — both within Africa and with the United States. We created Doing Business in Africa campaign to help American businesses — including small businesses — pursue opportunities across Africa. And under Penny’s leadership, nearly 300 American companies have taken trade missions to Africa, with more than 8,000 African buyers attending U.S. trade shows.

If you are an African entrepreneur or an American entrepreneur looking for more support, more capital, more technical assistance, there has never been a better time to partner with the United States.

Commitments from the Export-Import Bank and the U.S. Trade and Development Agency have doubled. OPIC investments have tripled. Nearly 70 percent of Millennium Challenge Corporation compacts are now with African countries. And we’ve opened up and expanded new trade and investment offices, from Ghana to Mozambique. Through our landmark Power Africa initiative, the United States is mobilizing more than 130 public and private sector partners — and over $52 billion — to double electricity access across sub-Saharan Africa.

Meanwhile, our Global Entrepreneurship Summits in Morocco and Kenya and our Young African Leaders Initiative are giving nearly 300,000 talented, striving young Africans the tools and networks to become the entrepreneurs and business leaders of the future.

We’ve got some of those outstanding young people here today. And two years ago, I welcomed many of you to our first ever U.S.-Africa Business Forum, where we announced billions of dollars in new trade and investment between our countries.

And you can see the results. American investment in Africa is up 70 percent. U.S. exports to Africa have surged. Iconic companies — FedEx, Kellogg’s, Google — are growing their presence on the continent.

You can hail an Uber in Lagos or Kampala. In the two years since our last forum, American and African companies have concluded deals worth nearly $15 billion, which will support African development across the board, from manufacturing to health care to renewable energy.

Microsoft and Mawingu Networks are partnering to provide low-cost broadband to rural Kenyans. Procter & Gamble is expanding a plant in South Africa.

MasterCard will work with Ethiopian banks so that more Ethiopians can send home remittances.

These are all serious commitments. New relationships are being forged, and I’m pleased that, altogether, the deals and commitments being announced at this forum add up to more than $9 billion in trade and investment with Africa.

So we are making progress, but we’re just scratching the surface. We have so much more work that can be done and will be done. The fact is that, despite significant growth in much of the continent, Africa’s entire GDP is still only about the GDP of France. Only a fraction of American exports — about 2 percent — go to Africa.

So there’s still so much untapped potential. And I may only be in this office for a few more months, but let me suggest a few areas where we need to focus in the years ahead.

We have to keep increasing the trade that creates broad-based growth.

In East Africa alone, our new trade hubs have supported 29,000 jobs and helped increase exports to the United States by over a third.

So we need to keep working to integrate African economies, diversify African exports, and bring down barriers at the borders. Since we’re approaching two decades since AGOA was first passed, we’re releasing a report today exploring the future beyond AGOA, with trade agreements that are even more enduring and reciprocal.

We also have to keep making it easier to do business in Africa. We know progress is possible. A decade ago, if you wanted to start a business in Kenya, it took, on average, 54 days.

Today, it takes less than half that. And governments that make additional reforms and cut red tape will have a partner in the United States.

At our last forum, I announced the creation of our Presidential Advisory Council to guide our work together. And today, I’m pleased to welcome the newest members of our expanded council, so that more industries and insights can shape their recommendations. Feel free to find them later, bend their ear. Don’t be shy. They are excited about their work and excited to hear from you.

We also need to invest more in the infrastructure that is the foundation of future prosperity. And, as I indicated earlier, we’re especially focused on increasing access to electricity for the two-thirds of sub-Saharan Africans who lack it.

Three years after launching Power Africa, we’re seeing real progress — solar power and natural gas in Nigeria; off-grid energy in Tanzania; people in rural Rwanda gaining electricity.

This means that students can study at night and businesses can stay open. And we are not going to let up. Partners like the World Bank and the African Development Bank are mobilizing billions.

Last month, the government of Japan made a major commitment to support this work. And together with GE, today we’re launching a public-private partnership to support energy enterprises managed by women in Africa. So we’re on our way, and by 2030, I believe we can bring electricity to more than 60 million African homes and businesses. And that will be transformative.

But even if we do the infrastructure, even if we’re passing more business-friendly laws, even if we’re increasing trade, I think all of you know that we’re also going to have to keep promoting the good governance that allows for good business. Graft, cronyism, corruption — it stifles growth, scares off investment. A business should begin with a handshake and not a shakedown. (Applause)

So through our efforts like our Open Government Partnership, and our Partnership on Illicit Finance, we’re going to keep working to encourage transparency, stamp out corruption and uphold the rule of law. That’s what’s going to ultimately attract trade and investment and opportunity.

The truth is, is that those governments that are above-board and transparent, people want to do business there. People don’t want to do business in places where the rules are constantly changing depending on who’s up, who’s down, whose cousin is who. It creates the kinds of risks that scare investors away.

And finally, we need to invest more in Africa’s most precious resource, and that is its people, especially young people. Men and women; boys and girls. I’ve had the opportunity to meet the next generation of leaders and entrepreneurs — in Soweto and Dar es Salaam and Dakar.

I’ve welcomed many of them to the White House. They are spectacular. They are itching to make a difference. Their passion is inspiring. Their talent is unmatched. They are hungry for knowledge and information, and are willing to take risks. And many of them, because they’ve come from tough circumstances, by definition they’re entrepreneurial. They’ve had to make a way out of no way, and are resilient and resourceful.

So we got to continue to empower these aspiring leaders — give them the tools, the training and the support so that a few years from now, they can be sitting in this room. Because if Africa’s young people flourish, if they are getting education, if they are getting opportunity, I’m absolutely convinced that Africa will flourish as well.

And they are the future leaders that inspire me. I think of the Rwandan entrepreneur I met earlier this year at one of our entrepreneurship summits. His company is turning biomass into energy. He started his business when he was 19 years old. And a lot of folks didn’t get what he was doing or why. He made an interesting comment that sometimes in traditional cultures, in African cultures, the working assumption is, is that young people don’t know anything. And since we were in Silicon Valley when he was telling this story, I wanted to point out that folks in Africa may want to rethink that — because if you’re over 30 there, you’re basically over the hill. (Laughter)

But he kept at it. As he told me, “No matter what you’re trying to do,” you need the “motive in your mind that you want to help your society move forward.” He was doing well, but he was also trying to do good.

And that’s what this is all about. That’s the work that we’ve got to carry on. This is a U.S.-Africa business forum. This is not charity. All of you should be wanting to make money, and create great products and great services, and be profitable, and do right by your investors. But the good news is, in Africa, right now, if you are doing well, you can also be doing a lot of good. And if we keep that in mind, if we do more to buy from each other and sell from each other, if we do more to bring down barriers to doing business, if we do more to strengthen infrastructure and innovation and governance, I know we’re going to be able to move our societies and economies forward. And that will be good not just for Africa, but it will be good for the United States and good for the world.

We want Africa as a booming, growing, thriving market, where we can do business, where you’ve got a young population that is surging. And although this will be the last time I participate in the U.S-Africa Business Forum as President, I think you should anticipate that I will be continuing to work with all of you in the years to come, and I know that Penny has done a great job in working to institutionalize these efforts. And when we’ve got great partners like Mike Bloomberg and the Bloomberg Foundation involved in this, I have no doubt that this is just going to keep on growing, and we’re going to look back and say, we were on to something.

Thank you so much, everybody. Appreciate it. Keep up the great work. (Applause)

By Adedapo Adesanya

Crude oil deliveries from the Nigerian National Petroleum Company (NNPC) Limited to the Dangote Petroleum Refinery doubled in March, boosting prospects for improved fuel availability.

This was revealed by the chief executive of Dangote Industries Limited, Mr Aliko Dangote, on Tuesday, when he received the Deputy Secretary-General of the United Nations, Mrs Amina Mohammed, at the industrial complex in Ibeju-Lekki, Lagos.

While speaking on feedstock supply, Mr Dangote commended the NNPC for increasing crude deliveries to the refinery in March, noting that volumes rose to 10 cargoes—six supplied in Naira and four in Dollars—to support domestic fuel availability, according to a statement by the Refinery.

“Last month, they gave us six cargoes for Naira and four cargoes for Dollars,” he said.

Despite the improvement, Mr Dangote noted that the supply remains below the 19 cargoes required for optimal operations, with the refinery continuing to bridge the gap through imports from the United States and other African producers.

He also expressed concern over the unwillingness of international oil companies operating in Nigeria to sell to the refinery, stating that their preference for selling crude to traders forces it to repurchase at higher costs, with broader implications for the economy.

Mr Dangote added that the refinery is seeking increased access to domestically priced crude under local currency arrangements as part of efforts to moderate fuel costs and enhance long-term energy and food security across the continent.

On her part, Mrs Mohammed underscored the strategic importance of Dangote Industries Limited -particularly Dangote Fertiliser Limited—in addressing Africa’s mounting food security challenges, while calling for stronger global partnerships to scale its impact.

Mrs Mohammed said the United Nations would prioritise amplifying scalable solutions capable of mitigating the continent’s food crisis, describing Dangote’s integrated industrial model as a critical pathway.

“I think the UN’s job here is to amplify and to put visibility on the possibilities of mitigating a food security crisis, and this is one of them,” she said. “I hope that when we go back, we can continue to engage partners and countries that should collaborate with Dangote Industries.”

By Aduragbemi Omiyale

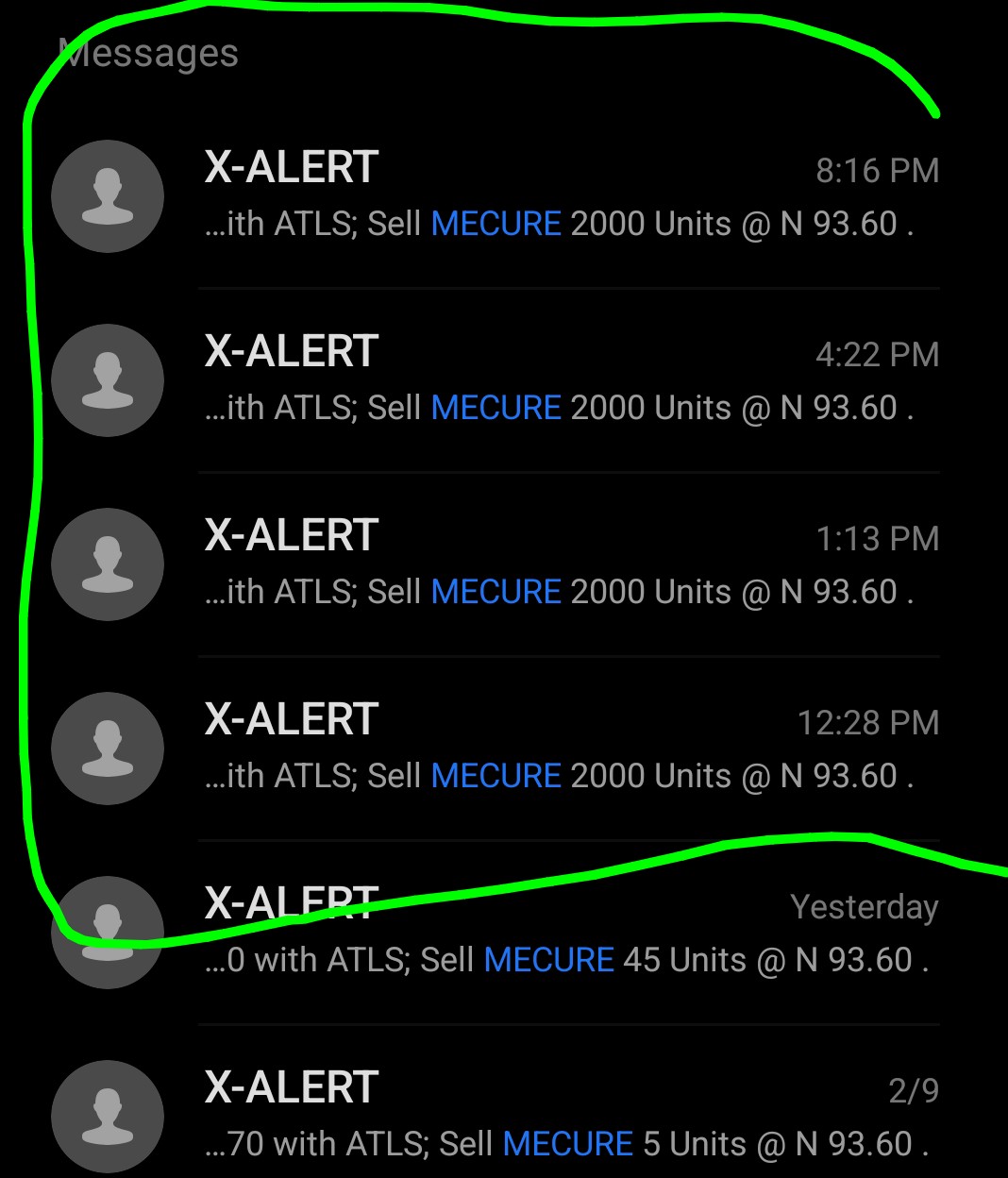

The Securities and Exchange Commission (SEC) has approved a 50 per cent hike in the X-Alert service fee per transaction in the Nigerian capital market.

The X-Alert fee is a flat rate charged for sending real-time SMS/email notifications for transactions to investors from both buy and sell sides.

It was introduced by the Nigerian Exchange (NGX) to replace percentage-based charges, aimed at increasing transparency and reducing total transaction costs for investors.

Investors were earlier charged N4 per SMS, but the country’s apex capital market regulator has approved a 50 per cent increase in X-Alert service fee, meaning the new rate is N6 per SMS.

Business Post gathered from one of the players in the ecosystem that the effective date for the new price was Thursday, March 26, 2026.

“We wish to inform you of a revision to the X-Alert (SMS) service fee applicable to transactions executed on the Nigerian Exchange (NGX).

“Following approval by the Securities and Exchange Commission (SEC), the X-Alert fee has been reviewed upward from N4.00 to N6.00 per transaction,” the notice sighted by this newspaper read.

By Adedapo Adesanya

Nigeria’s economy is projected to remain resilient in the face of mounting global uncertainties, with the World Bank forecasting a 4.2 per cent growth rate in 2026.

However, the global lender has warned that rising fuel costs and persistent inflation, worsened by geopolitical tensions in the Middle East, could undermine household incomes and slow poverty reduction.

Speaking in Abuja, the bank’s lead economist for Nigeria, Mr Fiseha Haile, noted that while the ongoing US-Israel-Iran conflict has pushed up prices, overall economic activity has remained largely intact.

“Overall business activity has been expanding over the past few months, suggesting the impact on growth has been relatively contained. But the shock is still being felt through higher inflation,” Mr Haile said.

According to him, business activity has continued to expand in recent months, indicating that the broader impact on growth has been “relatively contained,” even as inflationary pressures intensify.

Nigeria’s inflation rate, though significantly reduced from around 33 per cent in December 2024 to 15.06 per cent in February 2026, remains elevated compared to regional peers.

“Inflation is still elevated and under increasing pressure, and that poses risks to incomes and poverty reduction,” Mr Haile said.

The renewed surge in fuel prices, reportedly rising by over 50 per cent during the Iran conflict, has had a ripple effect on transportation, food, and production costs, amplifying the cost-of-living crisis.

The World Bank urged Nigerian authorities to adopt prudent macroeconomic measures, including tightening monetary policy, avoiding blanket subsidies, and saving windfalls from higher oil prices to strengthen fiscal buffers.

It also recommended reconsidering restrictions on fuel imports as a potential tool to ease inflationary pressures.

The economic reforms under President Bola Tinubu — including the removal of fuel subsidies, exchange rate unification, and tax restructuring — were acknowledged as ambitious steps aimed at stabilising the economy.

These reforms have contributed to improved external buffers, with rising foreign exchange reserves and reduced volatility.

Additionally, Nigeria’s fiscal deficit stood at 3.1 per cent of GDP in 2025, while the debt-to-GDP ratio declined for the first time in a decade.

Yet, the World Bank cautioned that tighter global financial conditions could still pose risks to capital inflows, borrowing costs, and remittances.

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism10 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz3 years ago

Showbiz3 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn