Economy

Privatisation, Avenue for Raising Productivity Bar—Onyema

By Ahmed Rahma

The chief executive of the Nigerian Stock Exchange (NSE), Mr Oscar Onyema, has said “privatisation occupies a unique position in global economic liberalization and provides an avenue for raising the bar of productivity towards greater economic development.”

He made this disclosure during a webinar hosted by the exchange on Tuesday, November 17, 2020, in conjunction with the Nigeria Governor’s Forum (NGF) and the Nigerian Investment Promotion Commission (NIPC).

At the event themed Privatisation in Nigeria and the Outlook for Subnational Economic Development, the NSE boss stated that “in Sub-Saharan Africa between 2000 and 2008, total proceeds of privatisation were valued at $12.6 billion.”

“This contributed to the growth of the sub-region during the period. We are, therefore, excited to lay emphasis on the positive outcomes of the National Privatisation Programme in 1987, which includes the deepening and broadening of the capital market by a large body of shareholders.

“The outcomes of the programme which includes success in relieving the government of the burden of financing public enterprises, creating liquidity for the government to pay off debts and finance new expenditures, thus raising the level of investments in infrastructures,” he mentioned.

Delivering his keynote address, the Chairman of the NGF and Governor of Ekiti State, Mr Kayode Fayemi, stated that the sale of public assets has become very important at this period because both the “federal and state governments are experiencing fiscal and economic consequences occasioned by the COVID-19 pandemic which has culminated in significant vulnerabilities in our capacity to increase investment and protect business and livelihood.”

“We believe that if the private sector takes over critical segments of the economy, State Governors can focus on social investment initiatives such as health care and education.

“The discussion must, however, involve regulators and financial institutions who are central in providing a conducive environment for privatisation to work,” he concluded.

In his contribution, the Director-General of Securities and Exchange Commission (SEC), Mr Lamido Yuguda, who was represented by Executive Commissioner, Legal and Enforcement, Mr Reginald Karawusa, noted that, “Privatisation is one of such avenues governments need to explore in order to unlock economic potentials inherent in government-owned enterprises.”

The webinar several personalities contributing to the topic including the Chairman of Presidential Economic Advisory Council, Professor Doyin Salami; the Executive Secretary, NIPC, Ms Yewande Sadiku; the Governor of Lagos State, Mr Babajide Sanwo-Olu; Governor of Ogun State, Mr Dapo Abiodun; Governor of Kaduna State, Mr Nasir El-Rufai; and Governor of Bauchi State, Mr Bala Mohammed.

Others were the Director-General of Bureau of Public Enterprises, Mr Alex Okoh; CEO, Financial Derivatives and Member, Presidential Advisory Council, Mr Bismarck Rewane; CEO, Chapel Hill Denham, Mr Bolaji Balogun; MD/CEO, Nigeria Sovereign Investment Authority, Mr Uche Orji; the Partner & Chief Economist of PwC Nigeria, Dr Andrew Nevin; Chairman, Board of Directors, First Bank of Nigeria, Ms Ibukun Awosika; and CEO, InfraCredit Chinua Azubike.

By Adedapo Adesanya

Nigeria is targeting cutting port delays, reducing costs, and improving efficiency in import and export processes with the National Single Window (NSW), a major digital trade reform.

The reform initiative is designed to address cargo dwell time, eliminate multiple agency visits and process duplication, and reduce human interference and operational bottlenecks.

The Minister of Finance and Coordinating Minister of the Economy, Mr Wale Edun, speaking in Lagos, explained that the initiative, alongside the upgrade of Apapa and Tin Can Island ports, represents a turning point in Nigeria’s trade and economic trajectory.

Mr Edun said that as of 2025, cargo dwell time at Nigerian ports averages between 18 and 21 days, about 475 per cent higher than the global average of four days, resulting in high costs of doing business, delays for importers and exporters, and reduced competitiveness of Nigerian goods.

According to him, the NSW and port modernisation are part of a broader economic strategy under the leadership of President Bola Ahmed Tinubu to strengthen macroeconomic stability, improve the ease of doing business, attract and scale investment, and achieve a 7 per cent medium-term economic growth target.

He added that the reforms demonstrate a coordinated, system-wide approach to economic transformation.

“Phase 1 of the NSW directly targets the 73 per cent transaction delay component by introducing a single digital platform for trade documentation, eliminating multiple agency visits and duplicative processes, and enabling electronic submission of Licences, Permits, and Certificates (LPCOs), digital manifest processing, centralised risk management across agencies, transparent electronic payments, faster document processing, reduced human interface and bottlenecks, and more predictable and transparent timelines,” he said.

He added that the launch of Phase 1 of the NSW coincides with last week’s deal to upgrade Apapa Port (built in 1913) and Tin Can Island Port (built in 1977), describing both as coordinated reforms designed to cut cargo dwell time, reduce trade costs, and unlock economic growth.

According to the Minister of Trade and Investment, Mrs Jumoke Oduwole, the platform is scheduled to go live on Friday and will include one shipping line and one port.

“These are the kinds of game changers in terms of trade facilitation that we need,” Oduwole said, adding that it is a priority project for an economy of Nigeria’s size that is working to emphasise trading.

Mrs Oduwole said streamlining imports and exports at the ports could have a “multiplier effect” in terms of balance of trade and foreign exchange generation.

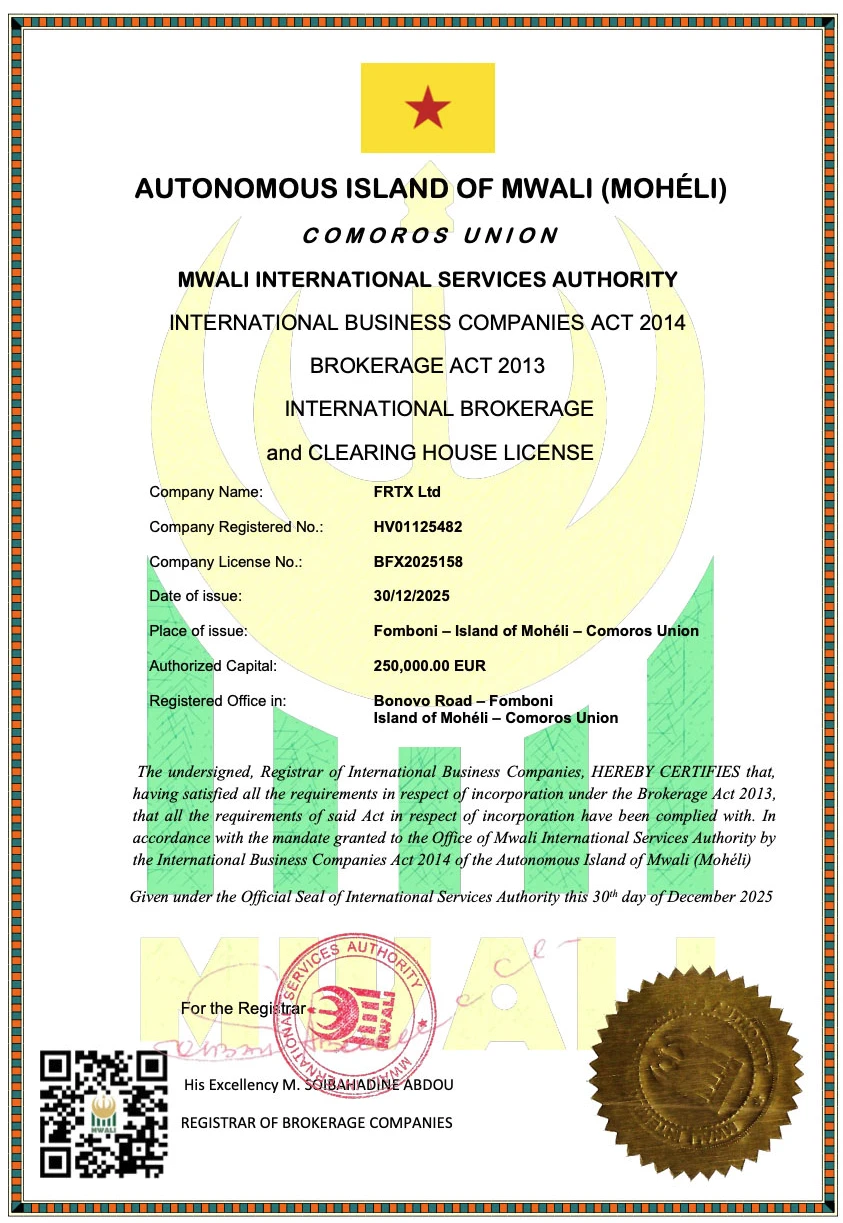

When FRTX is viewed through the lens of product structure rather than emotion, the service presents a fairly clear offering: browser-based CFD trading, a broad mix of instruments, account-type selection based on client goals, and an additional layer of conditions for more active users. On its website, the company states that the FRTX brand and its related resources are operated by FRTX Ltd, registered under number HV01125482 and licensed by the Mwali International Services Authority as an international brokerage company under license number BFX2025158.

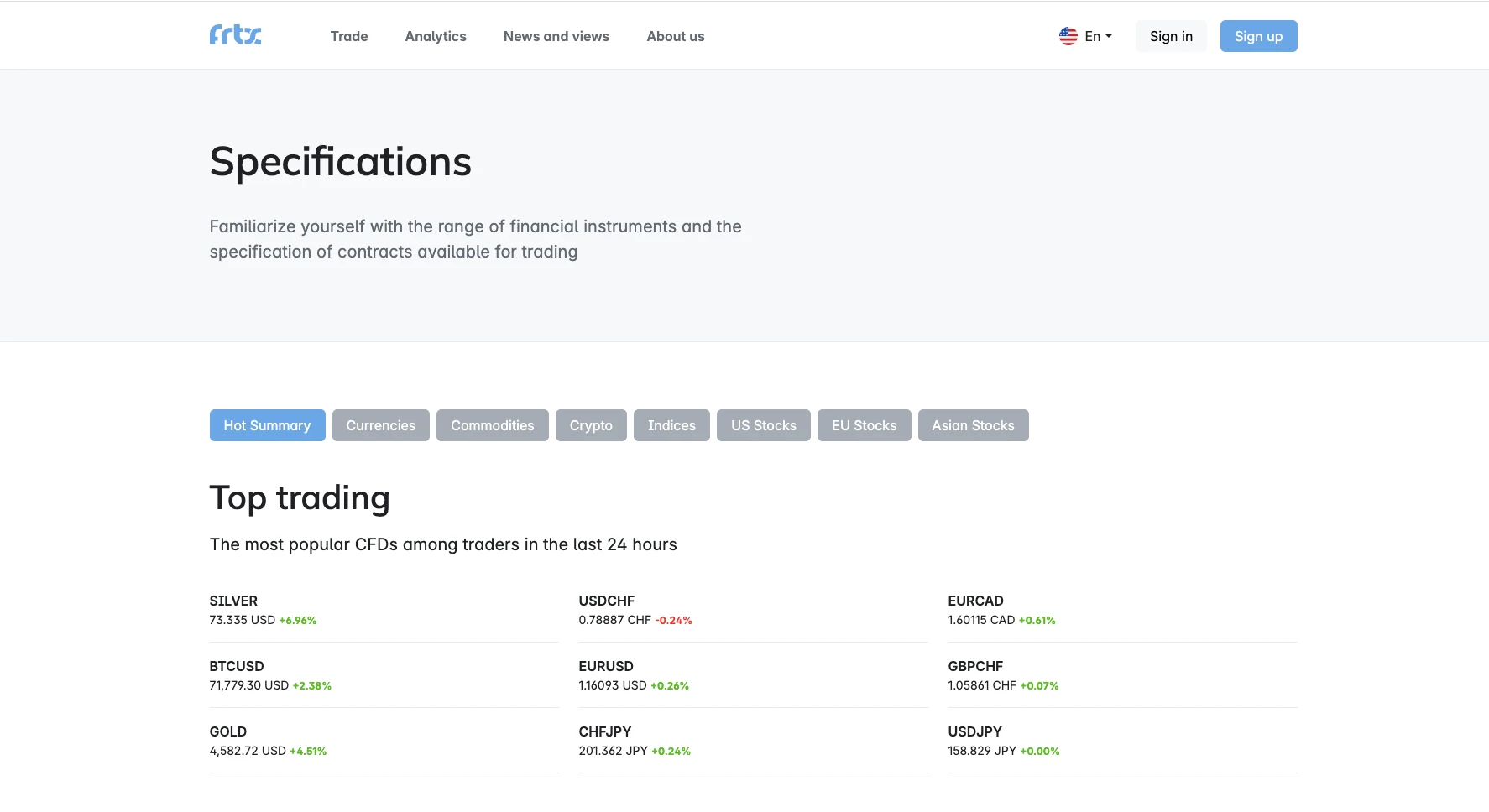

The same website also highlights 200+ trading instruments, browser-based access, and leverage from 1:10 to 1:1000 upon request, which sets the framework for the overall product model.

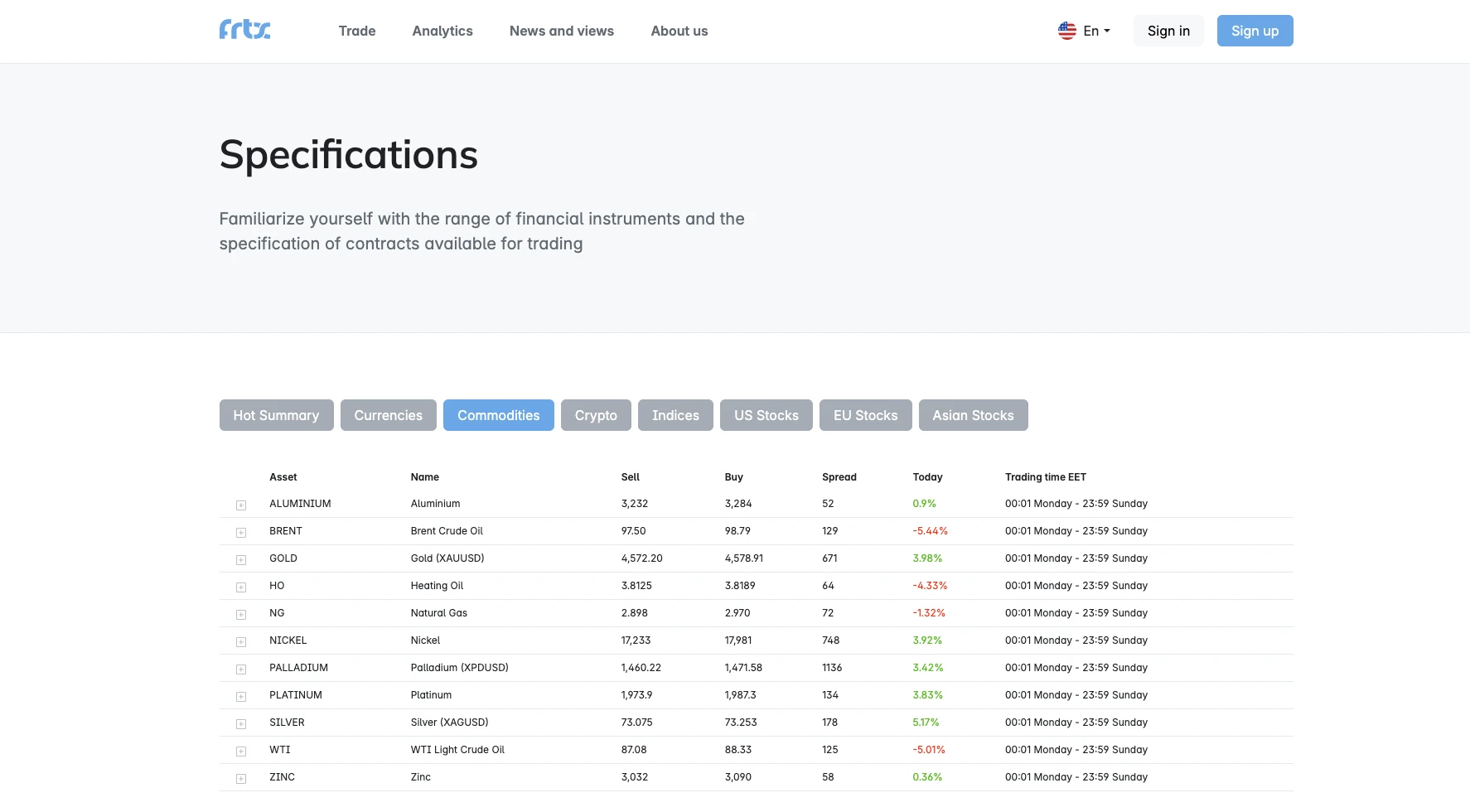

In terms of market coverage, FRTX appears to offer a fairly broad CFD lineup. On the “How We Work” page, the company specifically lists CFDs on commodities, metals, currencies, crypto-assets, and securities. The descriptions in those sections mention natural gas and oil, gold, silver, and palladium, currency pairs, widely known crypto-assets such as Bitcoin, Ripple, and Ethereum, as well as shares of major global companies. The homepage complements that picture with a broader statement about trading CFDs on stocks, commodities, currencies, and other financial instruments. For a review article, this is a meaningful advantage: the product basket does not look decorative, but genuinely multi-layered.

It is also worth noting that FRTX does not separate the platform from the trading conditions as if they were two unrelated worlds. FRTX Web is presented as a browser-based solution for desktop and mobile devices with a quick trading panel, an order book with real-time quotes, built-in market forecasts, and an economic calendar. As a result, the instruments, the analytics layer, and the actual point of trade execution are presented as one integrated environment rather than a patchwork of disconnected functions. For a brokerage product, that creates a more cohesive impression: when the platform and the trading terms follow the same logic, the service feels more structured.

The account model is also presented without unnecessary theatrics. On the accounts page, the service does not try to sell a dozen dramatic account names. Instead, it keeps the idea simple: users select an account type based on their goals, while the differences between account types are reflected in additional benefits such as enlarged cashback, monthly interest, and bonuses on replenishment. The same section also outlines the onboarding path: registration, verification, opening a trading account, funding it, and then working through the platform. In a review context, this reads as a sign of product discipline: the focus is placed not on flashy labels, but on what the client actually receives depending on account level or activity.

As for the trading conditions themselves, FRTX’s public presentation focuses on several clear parameters. The website refers to floating spreads, low commissions, and leverage of up to 1:1000. It also emphasizes high liquidity, the ability to trade on both rising and falling prices of the underlying asset, and mentions instant execution and fast withdrawals as part of the broader user proposition. In neutral analytical terms, this looks like an attempt to build a classic retail CFD model: a wide choice of markets, floating spreads, a relatively low commission barrier, and flexibility in leverage.

The loyalty program also remains a visible part of FRTX’s commercial logic rather than something hidden in the background. On the dedicated page, the company refers to bonuses of up to 100% on deposits, cashback of up to 100% of commissions for active traders, and monthly interest of up to 5% per month on available account balances. At the same time, the website includes an important qualification: the exact scale of these benefits depends on account type, current terms, and the loyalty program documentation, while the monthly interest feature is explicitly marked as not a banking product or service. For a review, this is a useful detail: the offer is presented in an attractive way, but not entirely without conditions and clarifications.

Taken together, FRTX appears, at the product-structure level, to be a service that aims to offer more than just one core function. It combines account selection, CFDs across several asset classes, browser-based trading, integrated analytics, and bonus mechanics for more active clients. That internal coherence is what creates the most favorable impression in a neutral review: the service does not look like a one-page offer, but rather like a more complete system with its own internal logic. The fact that the company also publishes its registration and licensing details on the website adds further weight to that presentation rather than relying on marketing language alone.

At the same time, the final assessment still has to remain grounded. FRTX operates in leveraged CFD trading, which means the strengths of its product structure always exist alongside the risk profile of the instrument itself. The website explicitly states that trading in financial markets and derivatives with leverage involves a high level of risk and may result in losses exceeding the initial deposit. That is why the strongest version of this review is not one that tries to label the service “perfect,” but one that describes it more precisely: FRTX appears to be a structured brokerage product with a broad CFD offering and a clearly organized conditions framework, but it should still be evaluated through the lens of the user’s own risk profile and careful reading of the company’s documentation.

This material is for informational purposes only and does not constitute investment advice. Trading CFDs and other leveraged derivative instruments involves a high level of risk and may not be suitable for all users.

By Adedapo Adesanya

The Nigerian Upstream Petroleum Regulatory Commission (NUPRC) has taken steps to ensure that approval for permits is done within hours of application to drive investments into the country’s energy sector

The upstream oil sector regulator is slashing the time it takes to approve applications to revive idle oil wells from weeks to hours as Nigeria, which is Africa’s top crude producer, seeks to take advantage of high energy prices triggered by the conflict in the Middle East.

Bloomberg quoted people familiar with the process as saying the country is also fast-tracking approvals for evacuations and barges at production facilities and export terminals to let barrels get to buyers quickly, as buyers turn to suppliers such as Nigeria and Angola on the African continent.

The US-Israel war on Iran and its countermeasures, including the blockade of the Strait of Hormuz, which handicapped about 20 per cent of crude and liquified natural gas (LNG), have driven oil prices above $100 per barrel.

Citing a spokesman from NUPRC, it was said “speedy approvals” were being given “for all activities that could increase production.”

The recent surge in applications has come from mostly local oil companies seeking to re-enter old wells, with the regulator cutting down an approval process that previously took anywhere from two to six weeks to encourage activities.

Repairing older or suspended wells for production is cheaper compared with drilling new wells, which can take years of planning, with any potential crude taking an average of four weeks to reach the surface.

This is coming after the chief executive of the Nigerian National Petroleum Company (NNPC) Limited, Mr Bayo Ojulari, said the country is ready to increase oil production by about 100,000 barrels per day over the next few months to make up for the crude shortfall resulting from the US-Israel war on Iran.

“We are building that capacity,” he said, though he added “we are not like Saudi (Arabia), but we can contribute,” he said on Monday.

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism10 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz3 years ago

Showbiz3 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn