Economy

West African Economies’ Risk-Reward Score Improve

By Dipo Olowookere

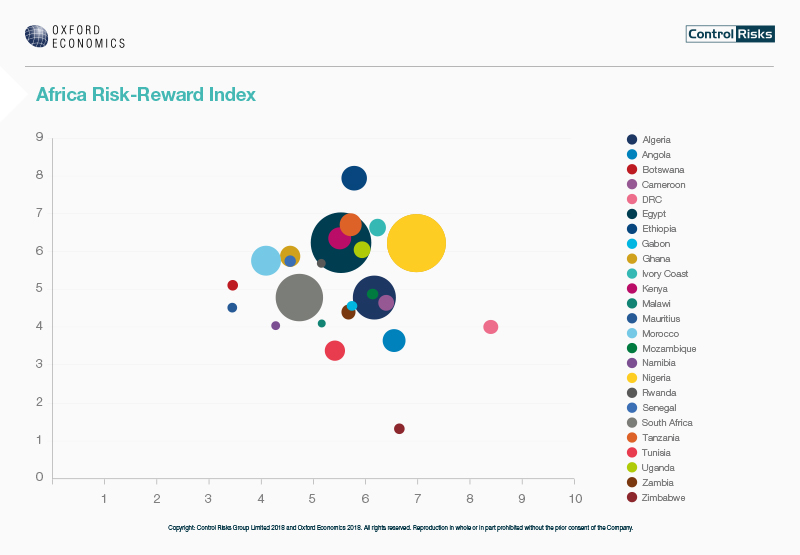

Increased political stability, improved commodity prices and effective public economic reforms led to an improvement of the risk-reward score in several West African economies, according to the 2018 Africa Risk-Reward Index from Control Risks and Oxford Economics.

Ghana leads these positive developments for West Africa, recording the strongest improvement in its risk-reward score in Africa, after Zimbabwe and Egypt. Both Nigeria and Senegal benefit from a greatly improved risk score.

Tom Griffin, Senior Partner for West Africa at Control Risks, comments that, “In 2017 many West African governments have embarked on an impressive journey to implement the right reforms for economic growth and improvement of investors’ confidence.

“Since coming to power in January 2017, Ghana’s government has continued to undertake a programme of macroeconomic reforms which have focused on reducing the deficit and external debt. In the last year, this had a particularly positive impact on issues such as credit and exchange risk.

“At the same time, Ghana has attempted to improve the business environment for investors by reducing the bureaucratic and taxation burden, as well as laying out plans for further investment activity in the oil and gas and manufacturing sectors.

“In Nigeria, the recently initiated Economic Recovery and Growth Plan has begun to tackle some of the economy’s challenges, including corruption and an infrastructure deficit.

“The plan has also sought to remove bottlenecks to improve the ease of doing business, which in turn boosts investors’ confidence.

“In the last three years, Senegal’s Emerging Senegal Plan has already led to steady growth, reaching close to 6.4% in 2017.

“The reduction in its risk score is one of the most positive changes in the 2018 Africa Risk-Reward Index and can be explained by structural reforms to improve the business environment, strengthened macro-economic fundamentals and a controlled debt management policy.”

Further findings of the report showed that Angola’s leadership change has not yet improved its reward score, but its risk score has gone down: Angola’s new president, João Lourenço, has acted with remarkable speed and decisiveness to consolidate his authority. Efforts to dismantle his predecessor’s networks have provided new opportunities for foreign investment in sectors previously dominated by companies linked to the former president and his family. Combined with an improved regulatory environment, investors can seek opportunities predominantly in the oil and gas, diamond, and telecommunications sectors. Reward score: 3.65 / risk score: 6.55.

South Africa – slightly increased reward score and reduced risk score as political uncertainty eases: Investor confidence has increased since Cyril Ramaphosa assumed the presidency in February 2018. The implementation of policies – intended to consolidate fiscal expenditure and tackle corruption in public institutions and state-owned enterprises – increases opportunities for doing business in South Africa. But deeply entrenched patronage networks and electoral pressure ahead of the 2019 general elections will contribute to a slow recovery of South Africa. Reward score: 4.78 / risk score: 4.74

Kenya’s reward score remains one of the highest in sub-Saharan Africa, but the government’s external debt burden raises concerns: Winning the election in 2017, Kenya’s leading Jubilee Party of Kenya continues its pro-business policies. However, concerns arise over the government’s external debt burden, with a new USD 2bn Eurobond issued in February even as the proceeds of a previous issue have yet to be fully accounted for. Furthermore, improving relations between the government and the opposition will be instrumental in ensuring that political tensions do not undermine economic growth, and more prudent fiscal and macroeconomic policies are needed to maintain positive economic prospects. Reward score: 6.36 / risk score: 5.51

Côte d’Ivoire, with a forecasted real GDP growth rate of 7% in 2018, continues its impressive economic recovery, but great challenges remain: With reforms to the business environment and efforts to bring foreign investors back after the 2010-2011 crisis, Côte d’Ivoire has achieved amongst the highest growth rates in the world in recent years, and sectors such as construction, telecommunications, banking and retail have seen considerable growth. However, severe obstacles to a full recovery persist, including political interference and corruption, socioeconomic discontent, shortcomings in security-sector reform, and growing competition ahead of the potentially volatile 2020 presidential poll. Reward score: 6.51 / risk score: 6.24.

Senegal – growing investment and a reduced risk score presage continuous growth: Under the Emerging Senegal Plan, growth has increased steadily over the last three years, reaching close to 6.4% in 2017. Growing exports, a more diversified economy and increased interest from large international investors as a result of the promising offshore oil and gas discoveries make Senegal one of the poster children in sub-Saharan Africa. The reduction in its risk score is one of the most positive changes in the 2018 Africa Risk-Reward Index. Reward score: 5.76 / risk score: 4.56

Morocco – economic reforms improve the country’s resilience and make its exports more competitive, but social discontent remains a challenge: With one of the lowest risk scores on the 2018 Africa Risk-Reward Index and a relatively stable reward score, Morocco’s economic reforms prove to be a success. Medium-term growth will be enhanced by continued reforms to facilitate foreign investment, access to finance, quality of education and the business environment, as these represent the primary constraints to competitiveness and doing business. However, social-economic unrest over poor living conditions persists particularly in interior regions. Reward score: 5.77 / risk score: 4.10.

By Aduragbemi Omiyale

Between $30 billion and $50 billion in investments are anticipated from 22 major offshore projects by the Nigerian Upstream Petroleum Regulatory Commission (NUPRC) from now till 2030.

Speaking at the Society of Petroleum Engineers’ Nigeria Annual International Conference and Exhibition (NAICE 2026) in Lagos on Wednesday, the chief executive of NUPRC, Mrs Oritsemeyiwa Eyesan, said since 2022, successive licensing rounds have opened access to some of Nigeria’s most prospective oil and gas acreages.

She made reference to the recent 2025 Licensing Round where 31 companies emerged successful bidders for 37 oil and gas blocks after progressing through a robust, data-driven and technology enabled evaluation process.

Mrs Eyesan said the 2026 Licensing Round, which is set to commence soon, is showing greater promise thanks to the transparency that has characterised licensing rounds.

“With preparations already underway for the 2026 Licensing Round, Nigeria is demonstrating that investment certainty is no longer an aspiration; it is becoming an enduring feature of our regulatory framework,” the NUPRC boss stated.

The agency’s chief, who was represented at the event by the Executive Commissioner for Development and Production, Mr Enorense Amadasu, the expected investments are expected to increase production, create jobs and strengthen energy security.

“Since 2024, the NUPRC has approved over $57 billion in Field Development Plan (FDPs) some of which have translated to Final Investment Decisions. Twenty-two major offshore projects are expected between 2026 and 2030 with an estimated investment potential of $30–50 billion.

“Beyond increasing production, these investments will create jobs, expand infrastructure, strengthen energy security and reinforce Nigeria’s position as a leading global upstream investment destination,” she stated.

She noted that besides developing its proven reserves, Nigeria is building a resilient energy future by maintaining a strong pipeline of exploration opportunities that will sustain long-term growth and energy security.

Mrs Eyesan said infrastructure deficit continues to undermine Africa’s promising potential, stating that, Nigeria is, however, addressing this challenge through a series of strategies.

“We are expanding gas gathering systems, processing facilities, pipelines and export infrastructure, while promoting shared facilities, open access, third party access and field tiebacks to reduce costs, speed up project delivery, maximise the use of existing infrastructure and help bring stranded oil and gas resources into production,” the NUPRC boss stated.

Besides these infrastructure strategies, Mrs Eyesan said stronger collaboration among government, security agencies, operators, host communities and private partners; as well as the Host Community Development Trust had led to an improvement in the protection of critical energy assets which had ultimately made Nigeria’s upstream sector more resilient.

By Adedapo Adesanya

Pathway Advisors Limited has launched a N25 billion Series 3 Commercial Paper (CP) issuance for Zeenab Foods Limited, with proceeds expected to strengthen the agro-processing company’s working capital and support its short-term funding needs.

The offer, which is being issued under Zeenab Foods’ N50 billion Commercial Paper Programme, opened for subscription on August 4 and will close on August 10, 2026. Issue and settlement are scheduled for August 11, while the commercial paper will mature on August 10, 2027.

Acting as the lead arranger and issuing house, Pathway Advisors structured the 364-day instrument at a discount rate of 19.69 per cent, translating to an effective yield of 24.50 per cent. The offer has a minimum subscription of N5 million, with additional investments accepted in multiples of N1,000.

Founded in 2011, Zeenab Foods operates across rice milling, the export of processed agricultural commodities, and the supply of food products to international donor organisations, including the United Nations World Food Programme (UN-WFP). The company runs processing facilities in Abuja and Kano, while maintaining export liaison offices in Changsha, Guangzhou and Shanghai in China, as well as Dubai in the United Arab Emirates.

The company has received strong investment-grade ratings from leading credit rating agencies. Agusto & Co. assigned it a short-term rating of A1 and a long-term rating of A-, while DataPro Limited rated it A1 for the short term and A+ for the long term.

According to the transaction details, Zeenab Foods has maintained a strong repayment record under both its previous N20 billion Commercial Paper Programme and the current N50 billion programme. Since 2024, the company has redeemed multiple commercial paper series ahead of maturity, reinforcing investor confidence in its financial position.

The firm has also continued to expand its production capacity to meet growing demand. Its rice milling facility now has an installed capacity of 180 metric tonnes per day following a 50 per cent expansion completed in 2025, with average capacity utilisation standing at about 85 per cent.

Zeenab Foods has also positioned itself to benefit from policy changes in Nigeria’s agricultural sector. Following the federal government’s ban on raw shea nut exports in August 2025, the company leased a shea butter processing facility in Ogun State with an initial capacity of 100 metric tonnes per day. It plans to expand the facility to 300 metric tonnes daily while diversifying into soya oil processing, edible oil refining and cocoa butter production.

The organisation also expects continued growth from its long-standing relationship with the UN-WFP, supported by sustained humanitarian food demand across the Sahel region.

Pathway Advisors Limited, a Securities and Exchange Commission-regulated issuing house and financial advisory firm, said it remains focused on facilitating access to capital for businesses and supporting sustainable economic growth across key sectors of the Nigerian economy through its capital-raising and advisory services.

As MSMEs across the South-East seek opportunities for growth, market expansion and cross-border trade, Stanbic IBTC, in partnership with the Anambra State Government, convened the Nigeria Business Summit Regional Tour in Onitsha to equip businesses with practical solutions for sustainable growth.

The summit, organised in collaboration with the Anambra State Ministry of Commerce, Industry and Trade, brought together government officials, business leaders, trade associations, development partners and entrepreneurs to explore practical pathways for economic growth, business sustainability and increased participation in local and international trade.

Speaking at the event, which took place on Wednesday, 29 July 2026, Honourable Nonso Chukwuma Ebonwu, Commissioner for Commerce and Industry, Anambra State, highlighted the importance of stronger partnerships between government, financial institutions and the private sector in creating an environment where businesses can thrive and contribute meaningfully to economic growth.

“Sustainable economic development requires strong partnerships between the public and private sectors. Financial institutions such as Stanbic IBTC have an important role to play by providing not only access to finance but also business advisory services, capacity building and the knowledge that enables businesses to grow sustainably,” he said.

Given Onitsha’s strategic position as a commercial hub, discussions centred on access to finance, enterprise development, business sustainability and opportunities for expansion into new markets. Stanbic IBTC’s Trade Team also provided practical insights into trade and export opportunities available to businesses operating within the South-East’s manufacturing and distribution value chains, highlighting strategies that can help enterprises improve competitiveness and unlock new growth opportunities.

Commenting on Stanbic IBTC’s commitment to supporting Nigerian businesses, Chuma Nwokocha, Chief Executive, Stanbic IBTC Holdings, said:

“We recognise the critical role businesses play in driving economic growth, creating jobs and fostering innovation. Supporting their growth remains central to our purpose of driving Africa’s growth, and we will continue to provide the solutions, partnerships and platforms they need to thrive.”

Also commenting on Stanbic IBTC’s support for Nigerian businesses, Remy Osuagwu, Executive Director, Business and Commercial Banking, Stanbic IBTC Bank, said:

“Our commitment to supporting businesses is unrelenting. Through strategic partnerships and platforms such as the Nigeria Business Summit Regional Tour, we are connecting entrepreneurs to the knowledge, networks and financial solutions needed to scale their businesses and compete more effectively in today’s evolving marketplace.”

The summit also highlighted Stanbic IBTC’s focus on providing businesses with access to the capital, insights and connections needed to achieve sustainable growth. This commitment aligns with the strategic direction of the bank’s Enterprise Banking business, led by Olajumoke Bello, as Stanbic IBTC continues to deepen engagement with MSMEs and growth-focused businesses across Nigeria.

The Onitsha engagement builds on successful editions of the Nigeria Business Summit Regional Tour previously held in Katsina, Aba and Ibadan. Through the initiative, Stanbic IBTC continues to work with public and private sector stakeholders to equip entrepreneurs with practical insights, strategic partnerships and business solutions that support sustainable growth.