Feature/OPED

Nigeria Green Bonds: Completing the Task of Issuance

By Esther Agbarakwe

The Paris Agreement signed and ratified by President Muhammadu Buhari in March of 2017 has an often-overlooked yet critical provision. In article 2 it outlines the aims of the agreement, one of which is “Making finance flows consistent with a pathway towards low greenhouse gas emissions and climate-resilient development”.

The Federal Ministry of Environment (FMEnv) under the leadership of the Hon Minister of State for Environment, Ibrahim Usman Jibril has significantly progressed a process that started in September of 2016 with a stakeholders forum that attracted key development partners, capital market operators and public sector institutions.

The initiative has resulted in a plan to issue a program of N150 billion in green bonds over the next few months with a pilot issue of N12.384 billion in the 3rd quarter of 2017 and the balance over the course of the budget year. Collaboration between Ministry of Environment and Finance continues to pull together the institutional partners necessary to achieve what would be Nigeria and Africa’s first sovereign green bond and the worlds 3rd.

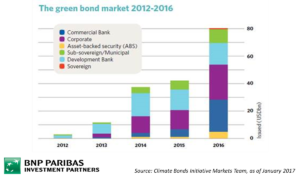

Growth of the Global Green Bond Market

The global market for green bonds took off in 2005 with an issuance by the European Investment Bank (EIB), since then the market has grown significantly to an annual issuance market last year of USD80 billion. Green bonds are like regular bonds, with a slight difference – they can only be used to fund projects that have been identified to have environmental benefits and their contribution to emissions reduction clearly articulated.

The global market for green bonds is expected to exceed last year’s amount and China remains a dominant participant in the market. Issuances to date have been largely by corporates and parastatals with the first sovereign issuance in November of last year for Eur750m by Poland and a follow on by France in January of 2017 for Eur7 billion. Commitments by signatory nations in the Paris agreement are expected to boost this market as resources are redirected toward development objectives that are sustainable from a climate perspective and contribute to global reduction in emissions.

Federal Ministry of Environment Preparation

The Ministry of Environment as custodian of the nations commitments under the United Nations Framework Convention on Climate Change (UNFCCC) has provided considerable direction to the process of issuance to ensure that the key elements needed for identification of projects that will meet the green credentials are in place.

In November of 2016 the Ministry issued its Green Bond Guidelines drawing from the International Capital Market Association (ICMA) Green Bond Principles (GBP). Working through the Inter-Ministerial Committee on Climate Change (ICCC), it engaged various Federal Government Ministries Departments and Agencies (MDAs) to identify projects with green credentials that will provide the foundation for issuance of the green bond.

In agreement with the Minister of Finance (MOF), the projects are required to be included in the budget approved by the National Assembly and assented to by the President.

Inter Agency Participation

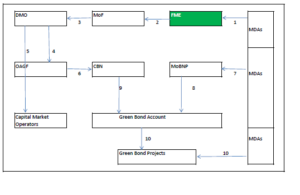

The Debt Management Office (DMO) as key issuer of FG debt is the key liaison with the Ministry of Environment. A Green Bond Account to hold the resources was recently created by the Central Bank of Nigeria (CBN) after approval from the Office of the Accountant General of the Federation (OAGF).

Frequent engagement between FMEnv and the Budget Office of the Federation (BOF) within the Ministry of Budget and National Planning (MOBNP), with the June 13th signing of the 2017 budget by the Acting President, Professor Yemi Osibanjo has affirmed the allocations to the identified projects.

The projects are Energizing Education Program (EEP) for N9.5 billion, the Renewable Energy Micro Utility (REMU) for N475m and the FMEnv’s Afforestation Program for N2.3 billion for a total of N12.38 billion.

The Green Bond Advisory Group

To enable the Federal government draw on a wide arrange of expertise in progressing and developing the issuance of the green bond, the Ministry of Environment and Finance established the Green Bond Advisory Group (GBAG).

The GBAG is made up of development partners (World Bank, DfID, AfDB, & IFC), Capital Market Operators (Nigeria Stock Exchange, Capital Assets, Chapel Hill Denham & Stanbic IBTC) and Climate Bonds Initiative, London.

The GBAG meets frequently with its first meeting in January of 2017 leading to a conference on green bonds in Lagos in February of 2017 at which the Acting President was a key note speaker. The GBAG remains the interface between the development partners and the capital market in ensuring the pilot issuance of the green bond happens in the 3rd quarter of 2017

Benefits to DMO Debt Strategy

The DMO has disclosed its strategy to be the restructuring of the Federal Government’s debt portfolio to replace short tenured bonds with long tenor and high rates with lower rates.

This strategy includes the tapping of the international capital markets and a green bond issuance with the right framework will provide a credible platform to tap into the global market for green bonds.

The London Stock Exchange (LSE) has indicated a willingness to participate in the green bond advisory group to provide necessary guidance to the FG to achieve this objective.

Benefits to the Economic Recovery & Growth Plan

The recent launch of the government’s Economic Recovery & Growth Plan (ERGP) has key objectives that are a catalyst for the issuance of the green. In addition to having as its objective the meeting of some of the goals in the United Nations Sustainable Development Goals (SDGs), it also has as an objective the issuance of a green bond to fund projects that have environmental benefits.

Some of the objectives in the ERGP include; identification of revenue flows to government, job growth and creation. Population impact and improvement in livelihoods are articulated in the targets of the individual projects to be funded by the green bond.

Summary

To deliver on the Nigeria’s Nationally Determined Contribution (NDC) will require a fundamental re-orientation of financial flows within the economy.

Capital will need to flow toward low-carbon, climate resilient opportunities and away from carbon intensive, polluting activities or those that exacerbate climate vulnerability leading to poverty, insecurity and reduced health quality.

The issuance of the green bond will begin the process of green the federal budget and the capital market. It will also demonstrate to the global community Nigeria’s commitment to achieving its targets in the NDCs.

For the FGs debt portfolio it adds to the cocktail of capital products that are being explored in ensuring resources are available to fund the FG annual budget.

On a strategy level it provides a platform for DMO to achieve the objective of extending tenor of the FG debt portfolio and also reduce interest cost. It would also establish a framework by which sub nationals and corporate can tap into the green bond market.

Esther Agbarakwe works with the Federal Ministry of Environment

By Blaise Udunze

Could it be said that Nigeria’s true identity today represents a country suffering and grappling with soaring inflation, mass unemployment, failing public infrastructure and multidimensional poverty despite almost three decades of enormous public revenue inflows? With the look of things, one question therefore deserves urgent national attention. Without missing any words, what exactly has government at all levels done with the trillions of naira shared through the Federation Account Allocation Committee (FAAC)?

One obvious fact is that since the return to democratic governance in 1999, Nigeria has witnessed a remarkable expansion in federal revenue sharing since the existence of this country.

Findings based on monthly allocations reported by FAAC and the National Bureau of Statistics (NBS) showed that over the past 27 years, the FAAC has distributed an estimated N160 trillion among the Federal Government, the 36 states and the 774 local governments. The obvious here is that the figure represents one of the largest transfers of public resources in Nigeria’s history.

One would definitely assume that, since the removal of the fuel subsidy in June 2023, government revenues have risen dramatically. Not to miss out on other gains from crude oil earnings, statutory revenue, Value Added Tax (VAT), exchange-rate adjustments, electronic money transfer levies, customs collections and other federally collected revenues, resulting in unprecedented monthly FAAC allocations.

In 10 years alone, FAAC distributed approximately N25.58 trillion to the three tiers of government, with states and the FCT receiving about N13.8 trillion during the period. One would also wonder that since President Bola Tinubu assumed office in May 2023, more than N56 trillion has been distributed through FAAC.

Surprisingly, amidst it all, in just over three years, President Tinubu’s administration has presided over FAAC distributions amounting to approximately 35 per cent of the estimated N160 trillion shared since the return to democracy in 1999. In other words, more than one in every three naira ever distributed through FAAC over 27 years has been shared under the current administration. But this recent figure represents only a fraction of the larger national story.

The more important question is not simply how much money has been shared. The question is what Nigeria has built with more than N160 trillion in public allocations over nearly three decades.

What is of concrete concern is that the sheer size of N160 trillion is difficult to comprehend until placed beside Nigeria’s major economic indicators.

Nigeria’s total public debt stood at approximately N149.39 trillion as of March 31, 2025. This means that the estimated FAAC allocations shared since 1999 are larger than the country’s entire current debt stock. While FAAC funds cannot directly be compared with debt because they serve different fiscal purposes, the comparison highlights a critical reality that shows that Nigeria has generated and distributed enormous financial resources, yet still carries one of Africa’s largest debt burdens.

The comparison with national budgets is equally revealing. Come to think of it, Nigeria’s proposed N58.18 trillion 2026 budget represents one of the largest annual spending plans in the country’s history, whilst the cumulative FAAC allocations since 1999 are equivalent to almost three times the size of Nigeria’s 2026 federal budget.

No doubt, the implication is profound. A country that has shared resources equivalent to several annual national budgets should reasonably demonstrate significant improvements in infrastructure, healthcare, education, electricity, industrialisation and citizens’ welfare. But the reality remains different.

One thing is obvious today and cannot be disputed by the political players, both past and present: Nigeria continues to struggle with poor roads, unreliable electricity, inadequate healthcare facilities, overcrowded classrooms, high unemployment and widespread poverty.

The truth is that the comparison becomes even more striking when looking at specific sectors, as this would provide a clearer picture. Considering that Nigeria’s recent proposed 2026 budget allocates approximately N3.52 trillion for education, N2.48 trillion for health and N3.56 trillion for infrastructure, bringing the combined allocation for these three critical sectors to about N9.56 trillion. The estimated N160 trillion shared through FAAC since 1999 is more than 16 times the combined 2026 federal allocation for education, health and infrastructure.

This raises a fundamental question: if Nigeria has received resources sufficient to finance these strategic sectors multiple times over, why do citizens continue to experience declining social services?

The comparison with capital investment is also significant. Nigeria’s proposed 2026 capital expenditure of N26.08 trillion is only a fraction of the estimated FAAC allocations shared since 1999. Had a substantial portion of these revenues been consistently channelled into productive capital projects, Nigeria could have developed world-class transportation networks, reliable electricity systems, modern healthcare facilities, industrial clusters and globally competitive education infrastructure.

That is the scale of the opportunity Nigeria has had. Instead, millions of Nigerians continue asking a painful question: Where is the evidence?

Economic theory is straightforward. When governments receive large financial resources, citizens expect corresponding improvements in their standard of living. Public revenue exists to create public value, not merely to finance government administration. Imagine what N160 trillion could have achieved if strategically invested over 27 years.

Nigeria has an estimated housing deficit exceeding 28 million units. A sustained investment programme using only a fraction of FAAC resources could have delivered millions of affordable homes while creating massive employment opportunities across construction, cement, steel, furniture and logistics industries.

Strategic agricultural investment could have transformed Nigeria into a food-secure nation through irrigation systems, mechanised farming, storage facilities, rural roads and agro-processing industries.

Investment in healthcare could have ensured that every local government has functional primary healthcare centres equipped with trained personnel, essential medicines and modern facilities.

Education could have been completely transformed through improved teacher training, digital learning infrastructure, modern classrooms, research facilities and expanded access to quality education.

Nigeria’s electricity challenge could have received far greater attention through investments in transmission networks, renewable energy, gas-powered generation and embedded power solutions that would reduce the cost burden on businesses and households.

A significant portion of FAAC resources invested in small and medium-sized enterprises could have created millions of jobs, expanded local production and strengthened Nigeria’s private sector.

None of these ambitions was beyond Nigeria’s financial capacity. The resources existed. The challenge has been utilisation.

Across many states, FAAC has gradually become less of a development catalyst and more of a monthly survival mechanism. Salaries, recurrent expenditure, political appointments, administrative costs and government overheads consume substantial portions of public resources, while capital projects remain insufficient.

The dependence on FAAC has also discouraged many states from aggressively developing sustainable internally generated revenue. Many states still depend heavily on federal allocations, weakening fiscal innovation and reducing accountability. A system where governments wait monthly for federal transfers creates little incentive to build productive economies.

Ironically, decades of increased allocations have coincided with worsening economic realities. Food prices continue rising. Millions remain unemployed or underemployed. Hospitals struggle with inadequate equipment. Schools remain overcrowded. Roads continue deteriorating. Manufacturers battle high energy costs. Businesses continue closing. Families spend more of their income meeting basic needs.

This contradiction raises serious governance questions. In Nigeria’s case, painfully, revenue growth does not automatically create development. Development requires transparency, accountability, strategic planning and effective implementation.

Nigeria must therefore move beyond celebrating monthly FAAC figures and begin measuring the outcomes generated from those resources.

Every month, Nigerians hear announcements of billions and trillions shared among governments. But rarely do they hear: How many hospitals were completed? How many schools were renovated? How many kilometres of roads were delivered? How many jobs were created? How many communities gained access to clean water? How many businesses were supported?

Revenue announcements must never replace performance reports. Every state and local government should publish transparent FAAC utilisation reports showing allocations received, projects funded, costs, locations and measurable outcomes.

Technology makes this possible. Open budgeting platforms, public expenditure dashboards and digital monitoring systems can ensure citizens know how their resources are being deployed.

Transparency should no longer be optional. The Federal Government equally has a responsibility.

Higher revenues must translate into improved national infrastructure, stronger institutions, better security, industrial growth and enhanced social protection.

Nigeria cannot continue borrowing heavily while simultaneously receiving record public revenues without demonstrating corresponding developmental outcomes.

Public finance is not simply about collecting money. It is about creating lasting value. Roads improve commerce. Electricity supports industries. Education increases productivity. Healthcare strengthens human capital. Agriculture reduces dependence on imports. Digital infrastructure enhances competitiveness. These are investments that create future prosperity.

When public revenue is consumed mainly by recurrent obligations, future generations inherit debts without corresponding assets.

Nigeria must strengthen accountability institutions, including auditors-general, public accounts committees, anti-corruption agencies and civil society organisations, to monitor how FAAC resources are utilised.

Citizens also have a responsibility. Public money belongs to the people. Communities must demand evidence of projects funded by government resources.

The tragedy of Nigeria is not simply a shortage of revenue. It is the failure to convert revenue into development. Nigeria has demonstrated remarkable ability to generate public income. What remains lacking is the political discipline and institutional capacity to transform that income into national prosperity.

The estimated N160 trillion shared through FAAC since 1999 represented a historic opportunity to rebuild Nigeria’s economy and improve citizens’ lives.

Millions of jobs could have been created. Infrastructure could have been transformed. Poverty could have been reduced. Investor confidence could have strengthened. Living standards could have improved.

Instead, many Nigerians continue to experience economic hardship despite decades of enormous public revenue distribution.

History will not judge governments by how much FAAC they received. History will judge them by what those allocations built.

The real question is no longer whether Nigeria has enough money. The question is whether Nigeria has the leadership, accountability and political will to convert public wealth into public prosperity. Not to focus on using the FAAC as an electoral tool to weaponise the opposition. Until that happens, N160 trillion in FAAC allocations will remain a symbol of missed opportunity rather than a foundation for national transformation.

Blaise, a journalist and PR professional, writes from Lagos and can be reached via: bl***********@***il.com

By Gleb Tsipursky

Nigeria’s artificial intelligence conversation has moved from whether businesses will use the technology to how they can use it without creating expensive new forms of confusion. Business Post recently examined the practical barriers facing Nigerian SMEs, including infrastructure constraints, digital skills shortages, regulatory gaps, and the need for any new technology to show a visible return. That is the right frame. For a small or mid-sized business, a clever system that creates hidden rework can cost more than it saves.

The timing matters. The Deep Learning Indaba brought Africa’s machine-learning community to Lagos from August 2 to 7 under the theme of sovereign intelligence. Nigeria’s National Centre for Artificial Intelligence and Robotics is also promoting practical adoption, entrepreneurship, and locally grounded systems. The country has talent, ambition, and increasingly accessible tools. What many businesses still lack is a simple management mechanism for learning from the moments when those tools get things wrong.

Every SME adopting AI should keep an exception ledger.

An exception ledger is a short operational record of cases in which an employee had to correct, override, redo, or stop an AI-assisted task. It does not need special software. A spreadsheet can work. Each entry should answer five questions: What was the task? What did the system get wrong or leave uncertain? What did the employee do? What business consequence would have followed if nobody intervened? Does the same problem appear often enough to justify a change in the workflow?

That sounds modest, but it changes how a company measures AI. Most adoption discussions focus on usage, time saved, or the number of employees trained. Those figures reveal activity. They say little about whether the work is becoming more reliable.

Consider a distributor using AI to draft quotations. The system may save ten minutes on most quotes, but twice a week it could mix up a product specification or fail to carry through a delivery condition. If staff silently repair those errors, the company records the time savings while hiding the correction cost. The same pattern can occur in customer service, bookkeeping, marketing, procurement, recruitment, or inventory forecasting.

The ledger turns those invisible corrections into management information. If one mistake appears once, it may require no action. If the same exception appears repeatedly, managers can change the prompt, source data, approval step, software configuration, or division of responsibility between the employee and the system. The business then improves the workflow rather than merely telling staff to “be careful.”

This is particularly important in Nigeria because SMEs operate with little room for waste. Business Post’s recent coverage of responsible AI for African SMEs has emphasised that trust, security, and accountability need to grow alongside adoption. An exception ledger gives those principles an everyday operating form. It lets an owner see whether a tool is producing a manageable stream of minor corrections or creating a pattern that threatens cash, customers, compliance, or reputation.

The ledger also protects employees from a common failure in technology rollouts. When an AI system makes an error, the human reviewer can become the person blamed for failing to catch it. That creates a perverse incentive to hide problems. A formal exception process sends the opposite message: catching a failure is valuable information. Employees become sensors for workflow quality rather than the last invisible line of defence.

Managers should keep the process light. If logging an exception takes ten minutes, staff will avoid it. A useful entry should take less than a minute and use a few fixed categories, such as factual error, missing context, policy conflict, customer sensitivity, data problem, or unclear ownership. The goal is not paperwork. The goal is pattern recognition.

A monthly review can then identify three kinds of decisions. First, some tasks are safe enough for greater automation because exceptions remain rare and low impact. Second, some tasks need a stronger human checkpoint because errors are costly or difficult to detect. Third, some tasks should stay primarily human because the judgment involved cannot be reduced to a reliable rule at the current stage of the technology.

This approach also helps Nigerian SMEs avoid a false choice between moving fast and acting responsibly. Small businesses cannot afford elaborate governance structures modelled on large banks or multinational companies. They can, however, create one feedback loop that connects frontline corrections to management decisions.

That feedback loop matters as Nigeria builds a larger AI ecosystem. A country can train more engineers, expand computing capacity, develop local-language models, and encourage entrepreneurship, but adoption succeeds inside businesses one workflow at a time. The practical test is whether a system helps people complete real work with fewer errors, less rework, and clearer accountability.

Nigeria has good reasons to accelerate AI adoption. The strongest businesses will not be those that accumulate the most tools. They will be those that learn fastest from the exceptions those tools create.

Gleb Tsipursky, PhD, is a behavioural scientist, CEO of Disaster Avoidance Experts, and author of The Psychology of AI Adoption at Work: From Resistance to Results (Georgetown University Press, 2026). https://disasteravoidanceexperts.com/ai********@**********************ts.com

Feature/OPED

GLO@23: How Billionaire Otunba Mike Adenuga Built a Telecom Empire That Refuses to Sell Out

By Bodex Hungbo

In a corporate world where corporate giants regularly swap boardrooms like trading cards and sell off equity at the first sign of volatility, one legendary tycoon continues to prove that absolute control is the ultimate power move. That man is Otunba Mike Adenuga Jr., the visionary billionaire whose dense belief in indigenous enterprise gave birth to Globacom, the telecom powerhouse affectionately known across the continent as Glo.

As Globacom marks a monumental 23-year milestone, the spotlight shines brightly not only on the company’s extraordinary ascent, but on the enduring legacy of its founder. Adenuga stands as the only Nigerian to establish, nurture, and retain 100% sole ownership of a national telecommunications network; one that has evolved into one of Africa’s most recognisable, resilient, and influential brands.

While rival networks scrambled through endless corporate restructuring, foreign buyouts, hostile takeovers, and high-stakes rebrandings, “The Bull” pulled off what many in international finance considered impossible: holding complete control of Nigeria’s proudest homegrown tech giant for over two decades without surrendering a single inch of authority.

From the very beginning, Adenuga refused to follow the standard playbook written by foreign multinationals. When Globacom officially launched in August 2003, the market was heavily dominated by well-funded international operators who insisted that certain consumer-friendly models were economically impossible in Africa. Sceptics openly declared that a wholly indigenous, single-owner startup could never go toe-to-toe with established global giants.

Adenuga didn’t just compete; he single-handedly revolutionised the entire landscape.

At a time when competitors claimed that charging consumers per second rather than per minute was technically unfeasible, Glo introduced per-second billing on day one. By charging 1 kobo per second, Globacom shattered the status quo overnight, forcing the entire telecom industry to follow suit. That single disruptive move democratised mobile access, saved everyday Nigerians billions of Naira, and transformed mobile phones from luxury items for the elite into essential tools for the masses.

Adenuga’s commitment to self-reliance went far beyond marketing strategies; it was backed by monumental capital investments in hard infrastructure. To ensure that Glo would never be beholden to external actors, he funded game-changing projects directly from his own vision and capital.

Chief among these milestones was the construction of Glo-1, a multi-million-dollar, high-capacity submarine fibre-optic cable stretching over 9,800 kilometres directly from the United Kingdom to Nigeria. Single-handedly funded without taking a single dollar in foreign equity, Glo-1 provided West Africa with unprecedented broadband capacity, drastically improving internet speeds, powering corporate enterprises, and anchoring the region’s digital economy.

Alongside this undersea marvel, Globacom built an extensive terrestrial fibre-optic backbone across Nigeria, expanding coverage into underserved rural communities and providing the critical pipeline for modern data services, mobile banking, and digital commerce.

The fierce independence that defines Globacom is a direct reflection of its founder’s personal journey. Adenuga’s rise is the ultimate story of relentless African grit. Long before he was dubbed “The Bull” of African commerce, a young Adenuga drove taxis and worked security jobs in the United States to pay his way through university.

Returning to Nigeria with a sharp mind and an insatiable work ethic, he built his fortune brick by brick. He conquered hard commodities, established a presence in oil and gas with Conoil, mastered corporate banking, and ultimately turned his sight toward telecommunications. Every venture was driven by the same philosophy: absolute dedication, hands-on execution, and a fierce refusal to settle for second best.

Despite commanding a multi-billion-dollar fortune, Adenuga remains famously reclusive. Operating largely away from public cameras and party circuits, he chooses to let his work speak for him. His quiet philanthropy, strategic investments, and relentless job creation have lifted thousands of families and injected vital energy into the broader West African economy.

Beyond cell towers and fibre-optic lines, Globacom transformed itself into an iconic symbol of African pride. Recognising the power of local culture long before global streaming platforms arrived, Adenuga turned Glo into the largest single corporate promoter of African entertainment and sports.

Glo flooded the creative industry with record-breaking sponsorship deals and endorsements, signing Nollywood legends, musical powerhouses, and sports heroes as brand ambassadors. From sponsoring the prestigious CAF African Footballer of the Year Awards and the Nigerian Premier League to funding cultural festivals, comedy tours, and reality shows, Glo actively elevated African talent to global prominence.

Through these cultural investments, the brand cultivated an emotional connection with millions of subscribers, proving that an African brand could stand tall, celebrate its heritage, and deliver world-class service without losing its soul.

Industry analysts frequently cite Globacom as more than just a corporate success; it is an enduring case study in what happens when visionary local leadership is matched with long-term capital and solid determination. Over 23 years, Glo has weathered fierce market competition, rapid technological transitions from 2G to 5G, and volatile macroeconomic shifts, all while maintaining its position at the top tier of African telecommunications.

As customers, industry leaders, and well-wishers celebrate GLO@23, the milestone serves as a powerful tribute to a titan who dared to build on his own terms.

Today, Globacom isn’t merely a telecom network; it stands as living proof of African capability, self-determination, and industrial excellence. As the green network prepares for its next era of digital expansion, artificial intelligence integration, and next-generation connectivity, one truth remains crystal clear across Africa’s business landscape: The Bull is still on the throne, and his legacy is built to last.