General

EFCC Declares MBA Forex Owner Wanted Over N231bn

By Modupe Gbadeyanka

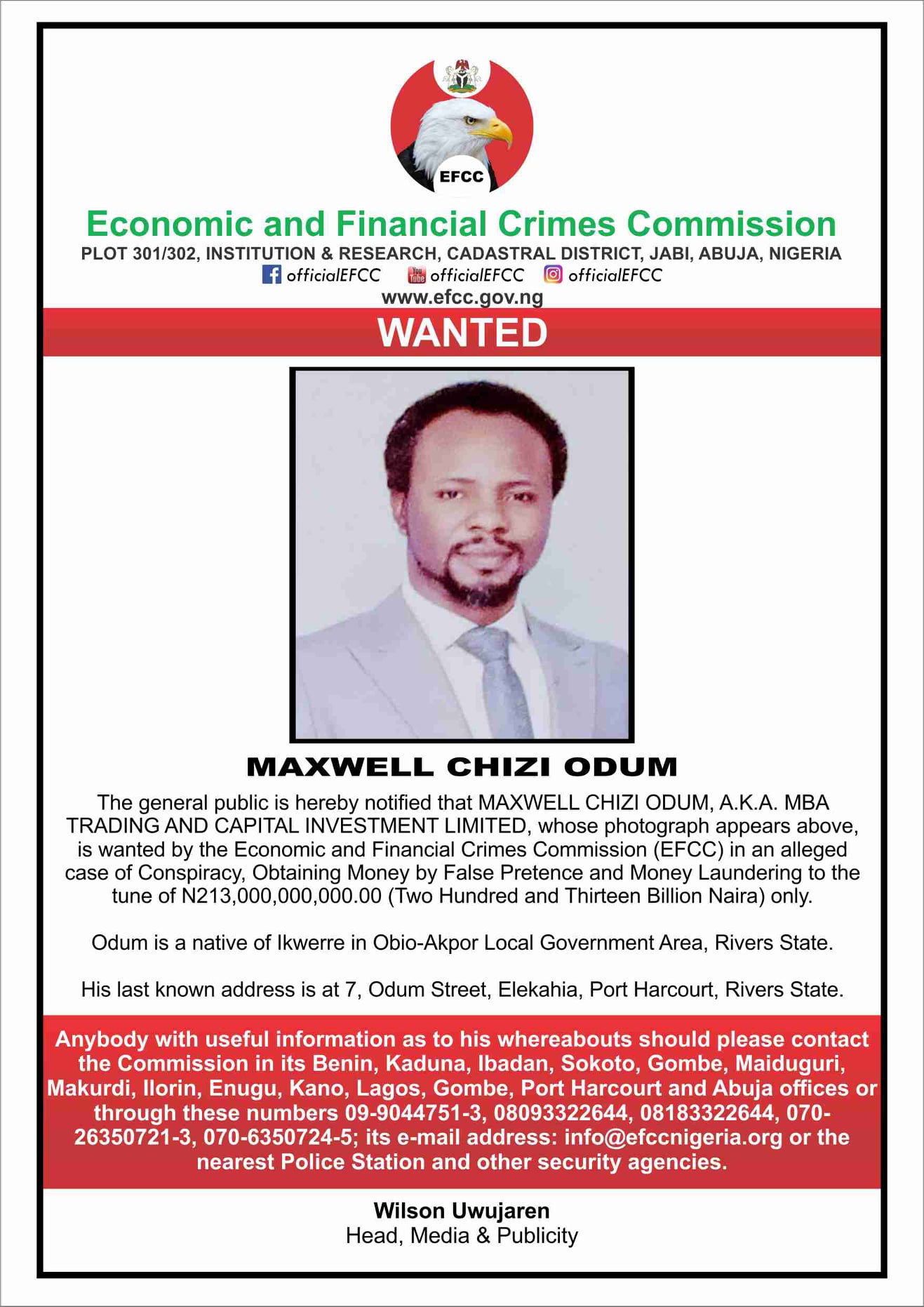

Mr Maxwell Chizi Odum, the founder and chief executive of MBA Trading and Capital Investment Limited, otherwise known as MBA Forex, has been declared wanted by the Economic and Financial Crimes Commission (EFCC).

A statement issued by the Head of Media and Publicity of the EFCC, Mr Wilson Uwujaren, confirmed this development on Wednesday.

According to the anti-graft agency, the self-acclaimed investor is wanted for allegations bordering on fraud to the tune of N213.0billion.

Members of the public with vital information that could lead to his arrest have been urged to make them available. His last known address, the EFCC said, was in Port Harcourt, Rivers State.

“The general public is hereby notified that Maxwell Chizi Odum, a.k.a. Mba Trading And Capital Investment Limited, whose photograph appears above, is wanted by the Economic and Financial Crimes Commission (EFCC) in an alleged case of conspiracy, obtaining money by false pretence and money laundering to the tune of N213,000,000,000.00 (Two Hundred and Thirteen Billion Naira) only.

“Odum is a native of Ikwerre in Obio-Akpor Local Government Area, Rivers State. His last known address is at 7, Odum Street, Elekahia, Port Harcourt, Rivers State.

“Anybody with useful information as to his whereabouts should please contact the commission in its Benin, Kaduna, Ibadan, Sokoto, Gombe, Maiduguri, Makurdi, llorin, Enugu, Kano, Lagos, Gombe, Port Harcourt and Abuja offices or through these numbers 09-9044751-3, 08093322644, 08183322644, 070-

26350721-3, 070-6350724-5; its e-mail address: [email protected] or the nearest Police Station and other security agencies,” the statement stated.

Recall that about nine months ago, MBA Forex claimed it has been unable to refund funds of investors to them because of the actions taken by the Central Bank of Nigeria (CBN).

The firm, which is involved in foreign exchange (forex) trading and investment in capital investment, said the banking sector regulator in Nigeria “suspended any dealings in our [bank] accounts.”

According to the chief executive of the organisation, Mr Maxwell Odum, “All other payment gateways we normally use for the easy payout of funds have also [been] blacklisted.”

He disclosed that this has made it quite difficult for some investors to get their money back from the company.

Mr Odum explained that the apex bank said it blocked the company’s bank accounts “to carry out some checks to ensure that we have been acting lawfully.”

However, the MBA Forex chief assured that those who invested in the firm would get their funds back as the “process has already commenced while some have already received their funds.”

By Adedapo Adesanya

President Bola Tinubu is expected to be among the leading public figures attending the next edition of the Africa CEO Forum, which will take place on May 14-15, 2026, in Kigali, Rwanda

A strong Nigerian private-sector delegation will also take part, including Mr Aliko Dangote, Mr Wale Tinubu, Mr Ofovwe Aig-Imoukhuede, Mrs Adesuwa Ladoja, Mrs Rachel More-Oshodi, Mrs Zouera Youssoufou, Mr Karim Noujaim, Mr Dany Abboud, Mr Ayo Otuyalo and Mr Chukwuerika Achum. Nigeria’s Coordinating Minister of Health and Social Welfare, Professor Muhammad Ali Pate, will also be present.

According to a statement on Tuesday, the 2026 edition will convene in Kigali to address a defining question for Africa’s future: how to achieve the scale necessary to compete, integrate and thrive in a fragmenting world.

It comes as global power dynamics continue to evolve, while the ability of Africa to rely on competitive, agile and internationally integrated corporate champions has become a defining corporate imperative. In this shifting global landscape, one lesson is clear: scale is no longer optional. It is the first line of defence.

Organised by Jeune Afrique Media Group and co-hosted by the International Finance Corporation (IFC), the Africa CEO Forum 2026 will convene Africa’s leading public and private decision-makers around a clear conviction: scale can only be achieved through shared African ownership.

The Forum will explore three strategic levers to build continental scale. First is shared equity, which will look to unlock cross-border equity investment to create multinational African champions. Mobilise African institutional capital across markets to strengthen resilience and enhance long-term returns.

Also, is shared infrastructure, which will take on designing complementary infrastructure to integrate African value chains. Champion transformative projects that serve regional, not merely national, needs and create truly connected markets.

Thirdly is shared frameworks, which is set to harmonise standards, rules and regulations to boost investor confidence and enable the free flow of capital, goods and services. Build future-proof digital rails for health, education, agriculture and cross-border payments.

Speaking on this, Mr Amir Ben Yahmed, President of the Africa CEO Forum, stated: “If Africa wants to compete in a world defined by scale, it must move beyond economic patriotism and embrace a new model: African capital investing together. Shared ownership, cross-border partnerships and continental ambition will define the economic future of Africa and the next generation of African champions.”

On his part, Mr Makhtar Diop, Managing Director at IFC, stated: “Africa has the capital and the opportunity to grow and create quality jobs. What matters now is putting that capital to work at scale. That means building trust, sharing risk, and investing across borders. The Africa CEO Forum brings leaders together to connect policy and private investment, and to help shape Africa’s next phase of growth.”

By Adedapo Adesanya

The Minister of Marine and Blue Economy, Mr Adegboyega Oyetola, has directed the Nigerian Shippers’ Council (NSC) to investigate the allegations of systemic efforts to undermine local barge operators at the nation’s seaports.

The Minister issued the directive during the recent 2026 First Quarter Citizens/Stakeholders’ Engagement, Sectoral Performance Review, and Ministerial Management Retreat of the Federal Ministry of Marine and Blue Economy, held in Lagos.

During the engagement, representatives of barge operators alleged that there was a coordinated and deliberate attempt by certain foreign interests to edge them out of business.

According to the Special Adviser to the Minister, Mr Bolaji Akinola, they claimed that these actions, if left unchecked, could significantly weaken local capacity and disrupt the balance of competition within Nigeria’s maritime logistics chain.

The operators expressed concern that policies, operational bottlenecks, and preferential treatment allegedly being accorded to some foreign-linked entities by certain terminal operators were creating an uneven playing field.

According to them, these challenges are gradually eroding their market share and threatening the survival of indigenous businesses.

Responding to the concerns, the minister emphasised the federal government’s commitment to protecting local investments and ensuring fair competition within the maritime industry.

He directed the council, as the port economic regulator, to carry out a thorough and impartial investigation into the claims.

Mr Oyetola stressed that any form of anti-competitive behaviour or policy inconsistency that disadvantages Nigerian businesses would not be tolerated.

The minister also reiterated the importance of stakeholder engagement as a platform for identifying sectoral challenges and shaping responsive policy interventions, stressing that the government remains focused on strengthening the marine and blue economy sector as a driver of national growth, job creation, and sustainable development.

By Modupe Gbadeyanka

The presidential candidate of the Labour Party (LP) in the 2023 general elections, Mr Peter Obi, has asked to know the real beneficiaries of the repeated payments made by the federal government to settle outstanding debts in the power sector.

Over the weekend, President Bola Tinubu approved the payment of N3.3 trillion for the “full and final” payment for debts in the electricity sector.

The action, according to a statement issued by the Special Adviser to the President on Information and Strategy, Mr Bayo Onanuga, was to ensure improvement in electricity supply in the country.

In a post on Tuesday, the former Governor of Anambra State questioned why the government is allegedly making the same payment it announced almost two years ago.

“On May 17, 2024, N3.3 trillion was approved for the same purpose. On July 25, 2024, another N4 trillion bond was approved to settle similar debts. There have also been other approvals in between, all targeted at addressing the same power sector liabilities.

“This raises a fundamental question: were the previous approvals mere announcements without execution?” he queried.

“During the 2023 campaign, President Bola Tinubu made a clear promise: that if he failed to deliver stable electricity, Nigerians should not re-elect him.

“Today, the reality is that power supply has worsened to the extent that there are even discussions about disconnecting the Presidential Villa from the national grid.

“Each time legitimate concerns are raised, what we see appears more like policy pronouncements than measurable progress.

“Now, again, we are confronted with another N3.3 trillion approval to settle power sector debts,” Mr Obi further said.

The chieftain of the African Democratic Congress (ADC) said, “These debts were largely accumulated under successive administrations of the All Progressives Congress between 2015 and 2025. This raises serious concerns about accountability, transparency, and effectiveness in public financial management.”

“It is important to note that government institutions and agencies, including the Presidential Villa, owe a significant portion of these debts. Year after year, budgets were made and funds appropriated. Why then were these obligations not settled when due? And from what source will this new payment be made? Are we resorting once more to borrowing to service inefficiencies?

“Key questions remain unanswered: How did the debt accrue? What is the actual total debt in the power sector? Which components of the debts are due to operators’ inefficiency and should be borne by them? Why have previous approvals not translated into tangible improvements? Who are the real beneficiaries of these repeated payments?

“Is the N3.3 trillion approved on April 6, 2026, the same as the N3.3 trillion approved in May 2024, and how does it relate to the N4 trillion bond approved in July 2024?

“Nigeria must move beyond recycled announcements and confront the power sector crisis with sincerity, transparency, and decisive reforms.

“Until we do so, we will remain trapped in a cycle of debt and darkness.

But with discipline, accountability, and the right leadership, a new Nigeria is still possible,” he wrote.

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism10 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz3 years ago

Showbiz3 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn

Pingback: Fraud, Ponzi Schemes and Terror Financing: A Story About Banking In Nigeria - West Africa Weekly