Media OutReach

Octa broker’s take on CBDCs vs. crypto: key insights for traders in 2025

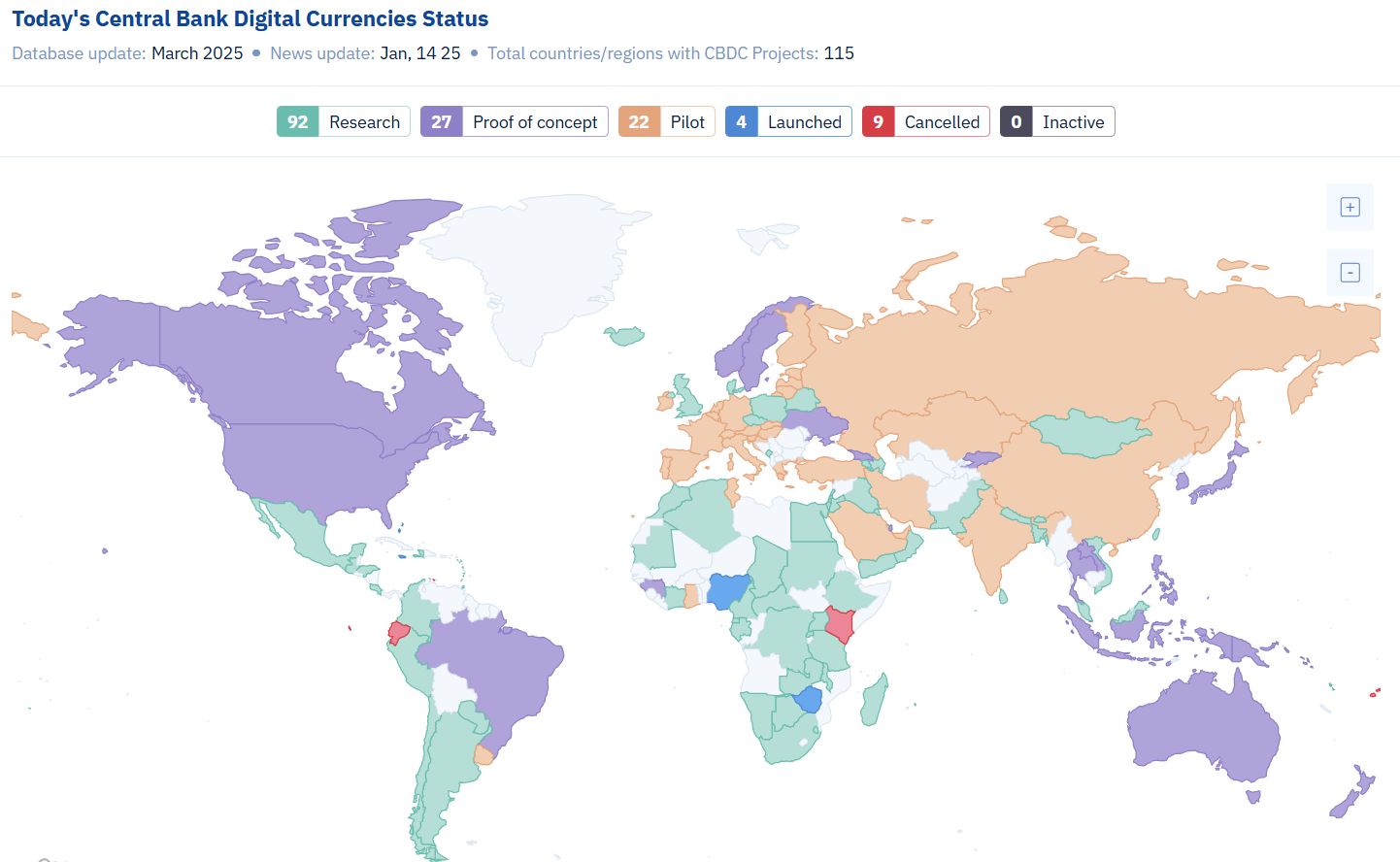

According to recent data, over 130 countries representing 98% of global GDP are now exploring CBDCs in some form, including pilots, development, or research (albeit few have fully adopted them). This rise reflects both technological momentum and regulatory intent to reclaim control over digital currency ecosystems, especially as private stablecoins and decentralised crypto assets have proliferated.

The main differences between CBDCs and cryptocurrencies

Stability and trust

While cryptocurrencies like Bitcoin or Ethereum operate in highly volatile and speculative environments, CBDCs are anchored to fiat currencies and issued by central banks. This offers higher value stability and institutional backing, reducing the risk profile for users.

Design and oversight

CBDCs are programmable but centrally managed. Governments can impose compliance measures and offer consumer protection in ways decentralised crypto systems cannot. Moreover, unlike crypto assets, CBDCs are not mined or privately issued, ensuring state control over monetary supply and transaction oversight.

Kar Yong Ang, financial market analyst at Octa, notes: ‘CBDCs offer a new model of digital liquidity—blending state trust and legal tender with tech efficiency. For traders, this opens doors to a more secure and transparent digital finance ecosystem.’

The global race to develop CBDCs and the drivers behind it

Here are three key reasons why central banks invest resources in CBDSs:

- The decline of cash and rise of digital payments. As societies increasingly favour digital over physical money, central banks face pressure to modernise public currency formats. In Sweden, for example, cash transactions make up less than 10% of payments. CBDCs are seen as a public alternative to private payment apps and platforms, ensuring monetary sovereignty in the digital realm.

- Controlling private stablecoin risks. Private stablecoins like USDT and USDC have raised concerns over systemic risk and shadow banking practices. A CBDC can serve as a stable counterbalance to these instruments, offering liquidity and legal clarity in fast-evolving financial markets.

- Financial inclusion and transparency. CBDCs can increase financial inclusion by offering digital wallets to unbanked populations, especially in developing economies. They also offer governments more visibility into money flows, enhancing tax collection and curbing illicit finance—though this has sparked debate around surveillance and privacy.

Pros and cons of CBDCs

CBDCs offer notable advantages: their value is typically pegged to fiat currencies, ensuring greater price stability than most cryptocurrencies. With full state backing, they function as legal tender and may include programmable features like conditional payments. For underbanked populations, they also present a path toward improved financial access.

However, concerns remain. Privacy is a major issue, as CBDCs could give governments visibility into personal transactions. They also pose cybersecurity risks, potentially becoming targets for large-scale attacks. Moreover, they could interfere with traditional monetary policy and financial market dynamics if not carefully designed. For instance, commercial banks could experience deposit runs if individuals perceive CBDCs as a safer alternative to traditional money for savings.

Real-world cases

Although the majority of countries still research CBDC and their application in the economy, some have already implemented them.

- Bahamas. The Sand Dollar became the first nationwide CBDC in 2020. It now serves all islands through a network of mobile-based wallets.

- Nigeria. The eNaira, launched in 2021, has seen a slow adoption of less than 0.5% as of 2025. The government continues to offer incentives to boost usage.

- China. The e-CNY has been piloted in over 25 cities and integrated into public transit and e-commerce platforms. Its scale makes it the most advanced major-economy CBDC.

Looking ahead: the road to adoption

While CBDCs promise greater efficiency and offer more tools for governments to implement social objectives, they also pose new governance challenges. To thrive, states will have to balance innovation with civil liberties, infrastructure resilience, and global interoperability. As the world of digital currencies continues to develop, CBDCs are increasingly important for progressive traders to grasp. Keeping up with developments can give a vital advantage in understanding the future of money.

___

Disclaimer: This content is for general informational purposes only and does not constitute investment advice, a recommendation, or an offer to engage in any investment activity. It does not take into account your investment objectives, financial situation, or individual needs. Any action you take based on this content is at your sole discretion and risk. Octa and its affiliates accept no liability for any losses or consequences resulting from reliance on this material.

Trading involves risks and may not be suitable for all investors. Use your expertise wisely and evaluate all associated risks before making an investment decision. Past performance is not a reliable indicator of future results.

Availability of products and services may vary by jurisdiction. Please ensure compliance with your local laws before accessing them.

Hashtag: #Octa

The issuer is solely responsible for the content of this announcement.

Octa

![]() Octa is an international CFD broker that has been providing online trading services worldwide since 2011. It offers commission-free access to financial markets and various services used by clients from 180 countries who have opened more than 52 million trading accounts. To help its clients reach their investment goals, Octa offers free educational webinars, articles, and analytical tools.

Octa is an international CFD broker that has been providing online trading services worldwide since 2011. It offers commission-free access to financial markets and various services used by clients from 180 countries who have opened more than 52 million trading accounts. To help its clients reach their investment goals, Octa offers free educational webinars, articles, and analytical tools.

The company is involved in a comprehensive network of charitable and humanitarian initiatives, including the improvement of educational infrastructure and short-notice relief projects supporting local communities.

In Southeast Asia, Octa received the ‘Best Trading Platform Malaysia 2024’ and the ‘Most Reliable Broker Asia 2023’ awards from Brands and Business Magazine and International Global Forex Awards, respectively.

The Taiwan-born pet mobility brand opens its first SoHo pop-up inside Flying Solo, bringing its Nordic-designed pet stroller collection to the heart of New York City.

NEW YORK, USA – Media OutReach Newswire – 02 April 2026 – FikaGO, the design-led pet mobility brand recognized across Asia and Europe, has opened its first New York City pop-up store inside Flying Solo in SoHo. The opening marks a deliberate move for a pet brand into one of the world’s most competitive retail districts.

Since entering the online American market in 2025, FikaGO has built a growing community of pet parents who see their animals as a central part of everyday life. Positioned as lifestyle essentials rather than conventional pet gear, FikaGO’s range of products is designed for people who want the best for their fur babies.

“We’ve always believed that pet products should not only be functional, but also beautifully integrated into everyday life.” — Eric Guu, Co-founder, FikaGO

SoHo was a considered choice: Flying Solo, with locations in New York and Paris, is known for championing independent design with a distinctly global sensibility.

The pop-up showcases FikaGO’s auto-folding Free To Go 2 in Sandy Beige, the brand’s bestselling product. All FikaGO’s products are manufactured using eco-friendly fabrics made from recycled materials, reflecting a commitment to sustainability. This includes their large-capacity Agile 2 pet strollers to their airline-approved Truffle carriers and the heavy-duty Kross pet wagon.

“Launching in SoHo is a meaningful milestone for us; it allows customers to truly experience the quality, design, and intention behind every FikaGO product.” — Eric Guu, Co-founder, FikaGO

As pet ownership rises globally, particularly among urban millennials and Gen Zs, demand for products that combine functionality, design, and lifestyle integration continues to grow. FikaGO was built for precisely this moment, and SoHo is precisely where that moment lives.

Visit the FikaGO pop-up at Flying Solo, 419 Broome Street, New York, or explore the full collection at https://us.fikago.com/.

Hashtag: #FikaGO #petmobilitybrand #petstroller #petcarrier #petwagon #petkennel #petbiketrailer

![]() https://us.fikago.com/

https://us.fikago.com/![]() https://www.facebook.com/FikaGO.US

https://www.facebook.com/FikaGO.US![]() https://www.instagram.com/fikago_us/

https://www.instagram.com/fikago_us/

YouTube: ![]() https://www.youtube.com/@fikago5910

https://www.youtube.com/@fikago5910

The issuer is solely responsible for the content of this announcement.

About FikaGO

FikaGO is a pet mobility brand founded in Taiwan, dedicated to crafting products that blend functionality, comfort, and modern aesthetics. With a presence across Asia and growing reach in Europe and the U.S, FikaGO is redefining everyday experiences between pets and their humans.

Media OutReach

Lee Kum Kee Celebrates Culinary Excellence at the Historic Hong Kong Debut of Asia’s 50 Best Restaurants 2026

From 23-25 March, Lee Kum Kee brought together top chefs, diverse cultures and industry communities through a range of thoughtfully curated experiences, bringing authentic Asian flavours to the global stage. As well as reaffirming the brand’s Asian roots and international perspective, its involvement reflected an enduring commitment to preserving culinary heritage and driving gastronomic innovation.

“Asian Flavour Duet“: A Culinary Journey Through Heritage and Innovation

Helping to build momentums for this year’s awards, Lee Kum Kee collaborated with Vicky Cheng, the acclaimed Executive Chef and owner of WING, to co-create the “Asian Flavour Duet”, a Hong Kong-style late-night supper party on 24 March. Hosted at two Hong Kong culinary landmarks, the experience unfolded in two chapters – “Paying Tribute to Heritage” and “Innovative Fusion” – and invited guests to explore the limitless possibilities of Asian flavour.

The evening began at the century-old Lin Heung Lau teahouse, a space filled with nostalgia and memories for generations of Hong Kongers. Chef Vicky reinterpreted classic Hong Kong late-night dishes using signature Lee Kum Kee sauces, while guests were immersed in the warmth of the historic venue.

The celebration then moved to Medora, Chef Vicky’s Western dining space, where an “Innovative Fusion” was revealed. He showcased his modern culinary philosophy by incorporating Lee Kum Kee sauces with contemporary techniques to create bold, unexpected dishes. Guests also enjoyed specially crafted cocktails infused with Lee Kum Kee sauces, alongside a delightful yet refined sauce-inspired gelato, demonstrating a harmonious interweaving of savoury, umami, sweetness and spice.

The multisensory journey seamlessly blended tradition with innovation, exploring the future of cuisine while highlighting Lee Kum Kee’s role as a global gateway to Asian culinary culture.

At the event, Dodie Hung, Executive Vice President – Corporate Affairs at Lee Kum Kee, commented, “Tonight, we are honoured to celebrate Hong Kong’s late‑night food culture with Chef Vicky and the global culinary community. From the legacy of Lin Heung Lau to the forward‑looking spirit of Medora, we are proud to be part of the creative journey and help showcase the depth of Asian flavours on the world stage.”

Celebrating a Gastronomic Brilliance with the Highest Climber Award Sponsored by Lee Kum Kee

During the awards ceremony on 25 March, Lee Kum Kee’s booth showcased a range of the brand’s acclaimed classic sauces and innovative products. Guests sampled specially crafted bites featuring Lee Kum Kee sauces, engaging directly with the flavours and techniques that have made the brand a trusted partner in both home and professional kitchens worldwide.

As part of the evening’s celebration of the region’s most exceptional culinary talents, the Highest Climber Award sponsored by Lee Kum Kee was presented to Lamdre in Beijing by Chef Park from Atomix (No.1 in North America’s 50 Best Restaurants 2025). Lambre was applauded for its pioneering plant-based dining space that promotes healthy, sustainable living while honouring Chinese biodiversity in its menus.

In addition, WING, led by Chef Vicky, achieved an impressive second place in 2026 Asia’s 50 Best Restaurants list. The restaurant had also previously ranked No. 11 on The World’s 50 Best Restaurants list in 2025, underscoring its continued international acclaim.

Building the Future Together: Deepening Global Partnerships

With the success of this prestigious awards ceremony in Hong Kong, China, Lee Kum Kee looks forward to deepening its collaboration with leading talents in the global culinary community. By continuing to champion Asian flavours and foster meaningful dialogue and exchange, the brand will continue to bring the spirit of Asian cuisine to kitchens and dining tables around the world.

Hashtag: #LeeKumKee #LKK

The issuer is solely responsible for the content of this announcement.

About Lee Kum Kee

Lee Kum Kee is the global gateway to Asian culinary culture, dedicated to promoting Chinese culinary culture worldwide. Since 1888, it has brought people together over joyful reunions, shared traditions and memorable meals. Beloved by consumers and chefs alike, Lee Kum Kee’s range of more than 300 sauces and condiments sparks creativity in kitchens everywhere, inspiring professional and home chefs to experiment, create and delight. Headquartered in Hong Kong, China and serving over 100 countries and regions, Lee Kum Kee’s rich heritage, unwavering commitment to quality, sustainable practices and “Constant Entrepreneurship” combine to enable superior experiences through Asian cuisine for people worldwide. For more information, please visit www.LKK.com.

About Asia’s 50 Best Restaurants

Launched in 2013, Asia’s 50 Best Restaurants aims to showcase the outstanding achievements and diverse culinary landscape of the region. The list is determined by the Asia’s 50 Best Restaurants Academy, a panel of over 350 culinary experts from across Asia who vote independently based on their specialised knowledge of the local dining scene. The Asia’s 50 Best Restaurants series includes the awards ceremony and list announcement, creating a premier networking platform for restaurateurs, media, seasoned travelers and culinary connoisseurs to celebrate the exceptional service, passion and talent in the dining industry.

- Herbert Vongpusanachai takes on the role of Senior Vice President for Commercial for the region, effective April 1, 2026

SINGAPORE – Media OutReach Newswire – 2 April 2026 – DHL Express, the world’s leading international express service provider, has appointed Herbert Vongpusanachai as Senior Vice President, Commercial for Asia Pacific, effective April 1, 2026. Herbert, who currently serves as Managing Director for DHL Express Thailand & Indochina, will be based in Singapore for his new role.

Herbert brings more than two decades of leadership experience within DHL Express, having successfully helmed multiple key markets across the region. He first joined the company in 2003 as Managing Director for Thailand & Indochina, later taking on leadership of Singapore in 2008, followed by Hong Kong & Macau in 2016. Since returning to lead Thailand & Indochina in 2020, he has driven sustained year‑on‑year profitable growth, transforming the cluster into one of the region’s key engines of expansion.

“Herbert has an exceptional track record of delivering strong business results while nurturing highly engaged teams across diverse markets. His deep understanding of our customers, collaborative leadership style, and ability to unearth opportunities in complex environments make him the ideal leader to drive our commercial agenda for Asia Pacific. I am confident that under his guidance, we will continue to accelerate sustainable growth across the region,” said Ken Lee, CEO for Asia Pacific, DHL Express.

In his new regional role, Herbert will shape and accelerate the commercial strategy for DHL Express across Asia Pacific by working with other functions to assess new sectors, routes and trade lanes with high potential for growth. He will focus on deepening customer engagement and supporting their expansion, while driving sustainable volume growth and advancing the adoption of new technologies to enhance commercial execution across markets. With his extensive country expertise and people‑first leadership style, Herbert is well‑positioned to support both regional and country teams in raising commercial performance to new levels.

“Asia Pacific remains an important anchor in global trade as seen in the latest DHL Global Connectedness Report, and this indicates the unwavering role of logistics to facilitate the flow of goods. With the newly introduced Heavyweight Express solution, which enables customers to ship heavyweight shipments with speed, certainty and reliability, I look forward to working alongside our talented teams to contribute to shaping the next chapter of DHL Express’s commercial success,” said Herbert Vongpusanachai, Senior Vice President – Commercial for Asia Pacific, DHL Express.

The latest DHL Global Connectedness Report shows that the region remains a major anchor of global commerce, with multiple economies rising in global connectedness rankings and Southeast Asia firmly establishing itself as a fast‑growing trade corridor. This also mirrors one of DHL Group’s strategies to better support 20 markets globally to accelerate growth; eight of them rest in Asia Pacific – underscoring the region’s critical role in DHL’s global network. As trade flows diversify and intra‑Asia integration deepens, this leadership appointment further strengthens DHL Express’s position in Asia Pacific.

Hashtag: #DHL

![]() https://group.dhl.com/en.html

https://group.dhl.com/en.html![]() https://www.linkedin.com/company/dhlexpress/

https://www.linkedin.com/company/dhlexpress/

The issuer is solely responsible for the content of this announcement.

DHL – The logistics company for the world

DHL is the leading global brand in the logistics industry. Our DHL divisions offer an unrivalled portfolio of logistics services ranging from national and international parcel delivery, e-commerce shipping and fulfillment solutions, international express, road, air and ocean transport to industrial supply chain management. With approximately 389,000 employees in more than 220 countries and territories worldwide, DHL connects people and businesses securely and reliably, enabling global sustainable trade flows. With specialized solutions for growth markets and industries including technology, life sciences and healthcare, engineering, manufacturing & energy, auto-mobility and retail, DHL is decisively positioned as “The logistics company for the world”.

DHL is part of DHL Group. The Group generated revenues of approximately 82.9 billion euros in 2025. With sustainable business practices and a commitment to society and the environment, the Group makes a positive contribution to the world. DHL Group aims to achieve net-zero emissions logistics by 2050.

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism10 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz3 years ago

Showbiz3 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn