World

Fostering Intra-African Trade: Challenges and Perspectives

By Professor Maurice Okoli

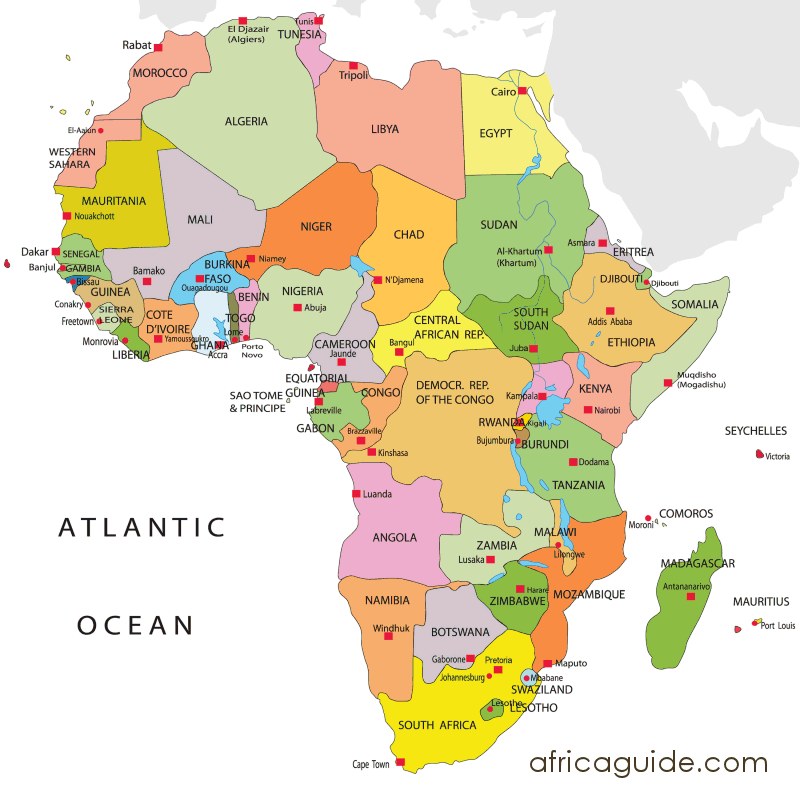

Over the past few years, African Union, the continental organization, has made intra-African trade its newest flagship and has created the Intra-African Trade Fair (IATF), which provides a unique and valuable platform for potential investors to support the continent’s transformation through industrialisation and export development, for businesses to access adequate trade and market information, and operate in an integrated single African market of over 1.4 billion people with a combined gross domestic product of over $3.5 trillion under the African Continental Free Trade Area (AfCFTA).

Organized by the African Export-Import Bank (Afreximbank), in collaboration with the African Union and the Secretariat of the African Continental Free Trade Area (AfCFTA), it was the historic third edition of the IATF, held in Cairo, Egypt from November 9-15, 2023. Under the theme The AfCFTA Marketplace, it brought together high-powered government officials, ministers, representatives of central banks, regulatory bodies and agencies, legislative authorities, commercial banks, law firms, entrepreneurs, and exporters from across Africa and beyond.

The importance of the Intra-African Trade Fair (IATF2023) was given as follows:-

(i) Promoting intra-African trade: The IATF plays a crucial role in boosting trade among African countries. Intra-African trade is generally lower compared to other regions, and the fair aims to address this by creating a conducive environment for African businesses to trade with each other.

(ii) Market Access: It provides African businesses with access to a larger market within the continent. This enables companies to expand their customer base and increase sales, ultimately contributing to economic growth.

(iii) Facilitating Networking: The fair brings together a diverse range of businesses, government officials, investors, and trade experts. This facilitates networking and partnerships that can lead to collaborations and business growth.

(iv) Showcasing African Products and Services: African businesses have the opportunity to showcase their products and services to a wider audience. This not only helps in building brand recognition but also highlights the quality and diversity of goods and services produced on the continent.

(v) Attracting Investment: The IATF attracts domestic and foreign investors interested in African markets. This can lead to increased foreign direct investment (FDI), which can fuel economic development and job creation.

In addition to establishing business-to-business and business-to-government exchange platforms for business deals and advisory services. The conference ran alongside the exhibition and featured high-profile speakers and panellists addressing topical issues relating to trade, trade finance, payments, trade facilitation, trade-enabling infrastructure, trade standards, industrialization, regional value chains and investment.

It marks one more significant step forward towards achieving economic independence which seemingly eluded the continent since 1963, the year the African organization was established and later transformed into what is popularly referred to as the African Union (AU). As stipulated by the explicit guidelines, the AU oversees and monitors the entire aspects of multifaceted development across Africa.

The AU is a sought-after platform for establishing mutually beneficial contacts and promoting bilateral relations for regional economic blocs, and dynamically developed regions such as Asia-Pacific, the United States and Canada to Latin America and Europe.

With the geopolitical changes and emerging multipolar political and economic order, Africa has become the main focal point in the world. In a practical context, Africa forms one of the current global transformations at the intersection of the past and the future. At the same time, Africa has already recognized its past of the adverse impact of resource exploitation primarily due to former leaders’ weak policies. Now it has the opportunity to make a tectonic shift and get engaged in a more equitable integrated, multipolar world.

With vigour, Africa can continue pursuing an independent continental policy to improve its economic status, and further strengthen its sovereignty with an increasing number of states in the Global South, and most probably in the East. Of course, it requires some unity in diversity in order to achieve this sustainable economic sovereignty.

The AU’s involvement in the IATF 2023 highlights its commitment to promoting economic cooperation and integration among African nations. By actively coordinating the trade fair, the AU aims to showcase Africa’s potential as a hub for intra-African trade and attract investments from both within and outside the continent.

The AU’s involvement in the IATF 2023 also signifies its recognition of the importance of regional economic integration in boosting Africa’s overall trade performance and fostering sustainable development across the continent. It can leverage its influence to facilitate discussions and negotiations on key trade, industry and tourism issues.

The vision for continental trade points to the creation of the powerful African Continental Free Trade Area (AfCFTA) in January 2021. Its primary purpose is to form a single market with a common umbrella – a borderless market allowing the free movement of goods, services and people. It is attracting external partners despite the persistent challenges and stumbling roadblocks (hurdles), the most tractable being the political disunity, divergent policies, ethnic conflicts deep-seated corruption and lack of good all-inclusive governance.

That, however, high optimism still exists. Most of the African countries are rallying around the historic decision, and frequently express the determination to join platforms, to develop targeted interactions within the framework of pan-Africanism. Several summits and conferences have been held to dialogue strategic partnerships relating to aspects of the continental economy.

Acknowledging the fact that attaining economic sovereignty includes thorough discussions on prospects for investment cooperation, industrial development, adopting new scientific technologies for modernizing agriculture and, of course, tourism and recreation for the 1.4 billion population in Africa.

In search for those aforementioned above necessitates the establishment of the Intra-African Trade Fair (IATF) and the African Continental Free Trade Area (AfCFTA). In one phrase – it remotely aims at strengthening the continental industrial base and promoting the value supply chains across Africa. At this moment, it is necessary to remember that global tensions are causing unprecedented fragmentation of trade, noting an uptick in unilateral trade restrictions and a growing trend towards consolidation of relationships within the processes of reconfiguration.

Therefore, the main challenging objective is how best to guide and better equip the private industrial and economic sectors with value chain integration strategies within the context of the AfCFTA. So we have to put emphasis on exploring the priority challenges confronting businesses and to identify targeted interventions that will support these businesses on their trading journeys in the AfCFTA.

Chief Olusegun Obasanjo, former President of Nigeria and Chairman of the IATF2023 Advisory Council, underscored the fact that intra-African trade holds the key to unlocking Africa’s true potential and fuelling economic growth, fostering industrialization and creating job opportunities for the people of the continent. “It is through this spirit of cooperation and collaboration that we will unlock the untapped potential of our continent,” he said, adding that the trade fair signified the commitment of Africa and its diaspora nations to economic integration and to their collective determination to create a prosperous future.

President Obasanjo further called on African leaders, policymakers, and representatives to foster an environment conducive to trade by eliminating unnecessary bureaucracy, harmonising regulations and investing in necessary infrastructure. IATF2023 was a stepping stone towards a future where African nations traded freely, breaking down barriers and opening doors of opportunities for all.

President and Chairman of the Board of Directors of Afreximbank, Professor Benedict Oramah, referred to the IATF as collective efforts for the stimulation of African countries’ economies and an attempt undertaken towards holistic economic recovery backed by political support. “It offers a comprehensive solution – it is not just a trade fair, but to make intra-African trade a reality, it is necessary to review border procedures, improve transport infrastructure and make effective the airline routes. The realization of the intra-African trade requires effective and regular electricity distribution and broadband connectivity, especially in industrialized and urbanized major African cities.

Kanayo Awani, Executive Vice President of the Intra-African Trade Bank at the African Export-Import Bank (Afreximbank), during special creative session held as an integral part of the third Intra-African Trade Fair (IATF2023) held in Cairo, Egypt, has underlined the catchwords such as multifaceted approach, encountering competitiveness, collaborating with business through co-financing agreements, promoting transparent financial practices and financial commitment as necessary factors for boasting sustainable entrepreneurial ventures.

For trade and investment, African countries could make use of factoring in order to take advantage of the opportunities for expanding the continent’s regional value chains, to tap into the opportunities available in the continent, especially in the context of intra-regional trade. Despite these numerous promising prospects, the economic sector grapples with challenges such as limited access to financing and business trademark infringements due to weak legal frameworks and enforcement mechanisms, according to Kanayo Awani’s explanation.

In a related discussion, Albert M. Muchanga, Commissioner for Trade and Industry of the African Union Commission, recognized the private sector and creative sector’s rapid growth and its substantial contribution to inclusive growth and sustainable development in African economies. Muchanga, however, urged African nations to translate creative potential into tangible projects, emphasizing the importance of investing in and protecting international intellectual property rights.

South African President Cyril Ramaphosa declared that South Africa was ready to work with other African countries to drive more balanced, equitable and fair trade relations for the benefit of the continent. “This Trade Fair is about building bridges. It is about connecting countries. It is about connecting people as well. Now Africa is taking concrete steps to write its own economic success story and this Intra-African Trade Fair is part of that story. Africa is opening up new fields of opportunity,” Ramaphosa asserted.

President Ramaphosa also wanted to see more made-in-Africa labels, as “this is critical if we are to change the distorted trade relationship that exists between African countries and the rest of the world. We can no longer have a situation where Africa exports raw materials and imports finished goods with those materials. By promoting trade in Africa, we strengthen our industrial base and produce goods for ourselves and each other.”

He stressed the need to “use the combination of the continent’s raw materials and industrial capacity, finance, services and infrastructure to produce quality finished goods to local and global markets. And about creating a market large enough to attract investors from across the world to set up their production facilities on the continent,” Ramaphosa said.

Most of the speakers noted the African Continental Free Trade Area (AfCFTA) must make the effort to ensure that Africa becomes a marketplace where no country is left behind, create jobs and enhance revenues for all parties. On the public sector side, governments must support local entrepreneurs to build scale, and therefore improve productivity. The implementation of initiatives most often poses difficulties and the challenges are surmountable if both public and private sectors collaborate with a common interest and a clear vision.

Looking back at its historical establishment, the AfCFTA agreement entered into force on May 30, 2019, after the treaty was ratified by 22 countries – the minimum number required by the treaty. It has the potential to generate a range of benefits through supporting trade creation, structural transformation, productive employment and poverty reduction. The AfCFTA opens up more opportunities for both local African and foreign investors from around the world. The official start of trading on January 1, 2021, signalled the commencement of Africa’s journey to market integration.

The African Union session provided a forum for exchange on what should be Africa’s immediate trade and investment priorities, to enhance Africa’s share of global trade, FDI, and ultimately the continent’s contribution to global GDP. The overall objective is to ensure that Africa strengthens its position internally from a trade and investment standpoint, which will give the continent the leverage for a strong position during its engagement at the G20. The dialogue examined how those priorities can advance intra-African trade as well as Africa’s share of global trade.

United Nations Development Programme and African Union Commission session provided a platform to drive a multi-sectoral dialogue on amplifying investment in digital infrastructure, to contribute and explore strategies that can lead to the growth of African unicorns, which in turn will create employment opportunities and drive economic growth across the continent, as well as to empower the African tech ecosystem to reach its full potential by going from 20 unicorns to 200 by 2030 and 2000 by 2063. By fostering collaboration, providing insights, and identifying actionable strategies, that discussion contributed to building a vibrant and sustainable tech ecosystem in Africa, driving economic growth, job creation, and technological innovation across the continent.

As the latest developments show, African countries have ratified the African Union protocols, making visa-free movement of people, and ultimately the introduction of the African passport that would facilitate free movement of persons in Africa. The future challenging task ahead – Africa will be able to compete globally, hence African countries must just integrate the market, something that has been evaded Africa since 1963, when forefathers hatched African Unity and established the OAU.

As a continuation of that vision, the African Union spearheads Africa’s development and integration in close collaboration with African Union member states, the regional economic communities and African citizens. The AU vision is to accelerate progress towards an integrated, prosperous and inclusive Africa, at peace with itself, playing a dynamic role in the continental and global arena, effectively driven by an accountable, efficient and responsive Commission.

The final resonating message is to leverage IATF’s combined initiatives and progress with the AfCFTA over the subsequent years. The first edition of IATF was held in Cairo under the auspices of Egyptian President Abdel Fattah El-Sisi. The Intra-African Trade Fair ended with a collective commitment to ensure economic stimulation, triggered by the business events, translates into the strengthening of the African Continental Free Trade Area (AfCFTA) and in achieving the aspirations of the African Union Agenda 2063.

Professor Maurice Okoli is a fellow at the Institute for African Studies and the Institute of World Economy and International Relations, Russian Academy of Sciences. He is also a fellow at the North-Eastern Federal University of Russia. He is an expert at the Roscongress Foundation and the Valdai Discussion Club.

As an academic researcher and economist with a keen interest in current geopolitical changes and the emerging world order, Maurice Okoli frequently contributes articles for publication in reputable media portals on different aspects of the interconnection between developing and developed countries, particularly in Asia, Africa and Europe. With comments and suggestions, he can be reached via email: markolconsult (at) gmail (dot) com

By Kestér Kenn Klomegâh

The Arab Republic of Egypt, a country spanning the northeast corner of Africa and the southwest corner of Asia, has a highly strategic location and attracts multifaceted interests of foreign players. For decades, Russia has established diplomatic relations with Egypt and has consistently sustained diverse ties with this country. It is no secret that Russia’s lust for the region is primarily due to the strategic importance of the Mediterranean Sea for investment and economic cooperation with the Maghreb region.

Determined to strengthen, particularly, economic cooperation, Russian President Vladimir Putin has maintained regular contacts with his colleague, President of Egypt, Abdel Fattah el-Sisi, mostly discussing both bilateral cooperation and broader regional developments. The current world’s geopolitical development, for instance, the United States-Israeli war on Iran in the Middle East, constitutes one theme both leaders frequently review, attempting to find long-term solutions.

On April 2, Putin met with the Minister of Foreign Affairs, Emigration, and Egyptian Expatriates of the Arab Republic of Egypt, Badr Abdelatty, in the Kremlin – the seat of Russia’s presidency. In attendance during the official talks on the Russian side were Foreign Minister Sergei Lavrov and Presidential Aide Yury Ushakov, while Egypt was represented by Ambassador Extraordinary and Plenipotentiary to the Russian Federation Hamdy Shaaban. Ultimately, there is no need to overstate the importance of this meeting.

Russia’s footprints are expanding in Egypt, highlighting the growing industrial investment and the strengthening of bilateral manufacturing ties by undertaking projects to ensure energy security. At the same time, maintaining regular dialogue remains very important for both leaders.

Putin, speaking with the three-member delegation in the Kremlin, underlined the fact that there are many promising initiatives underway, many of which are already being implemented. He has previously spoken in detail about the construction of a nuclear power plant and the construction of an industrial zone, and over ten major Russian companies have expressed interest in participating in this project.

Nuclear Plants in El-Dabaa, Egypt

The construction of nuclear plants in the city of El-Dabaa, about 320 kilometres northwest of Cairo, the capital of Egypt. It is the first nuclear power plant in Egypt, and will have four VVER-1200 reactors, making Egypt the only country in the region to have a Generation III+ reactor. On November 19, 2015, Egypt and Russia signed an initial agreement, under which Russia agreed to build and finance Egypt’s first nuclear power plant. These are now being carried out, not as a charity project, but with a loan of $28 billion. According to reports, Russia will finance 85% as a state loan of $25 billion, and Egypt will provide the remaining 15% in the form of instalments. The Russian loan has a repayment period of 22 years, with an annual interest rate of 3%.

At the meeting, Putin also raised the construction of an industrial zone in Egypt. There are many appealing and related opportunities in this, regarding having an industrial zone to be located on the banks of the Suez Canal. The industrial zone is also entering a new phase, as Russian auto-manufacturing enterprises are advancing distinctive plans to expand local vehicle production, reinforcing the country’s role as a regional manufacturing hub. The move reflects broader economic linkages between Russia and Africa, particularly in industrial development and supply chain integration.

Conveying Greetings and Reviewing the Middle East Situation

Naturally, the situation in the region remains a shared concern, according to Putin, and further hope that the ongoing conflict will be promptly resolved. “As you know, President Trump also addressed this issue yesterday. Let me reiterate that we are prepared to make every effort to help stabilise the situation and, as they say in such cases, return it to normal,” he stressed during the meeting. In this context, it is particularly important to know Egypt’s assessment as a key country in the Middle East.

Putin reminded the delegation of another Russia-Africa summit, which is planned for October 2026. With high hopes that Egypt will be represented by a strong, high-level delegation. Should the Egyptian President’s schedule allow, he would, of course, ahead of the summit, be very pleased to welcome him to Moscow. Jointly chaired by Vladimir Putin and Abdel Fattah el-Sisi, the first Russia-Africa summit, an important acute phase of the developments with Africa, under the motto of ‘For Peace, Security and Development’, was held for the first time in October 2019, in Sochi, a city located on the Black Sea coast. The idea to hold a Russia-Africa forum was initiated by President Putin at the BRICS (Brazil, Russia, India, China and South Africa) summit in Johannesburg in July 2018.

The head of the Egyptian Foreign Ministry, as traditionally expected, conveyed greetings from President El-Sisi to the Russian president and handed over a written message. President el-Sisi places great value on all aspects of the bilateral cooperation, and is extremely grateful for constructive collaboration on the El Dabaa Nuclear Power Plant, which represents a key milestone in the partnership. Despite the challenges, it is evident that the project is moving forward and will be completed by 2028.

In summary, as Egypt and Russia are reliable and time-tested partners, Putin plans to promote strategic projects, particularly in trade, economics, energy, and food security. With over 107 million inhabitants, Egypt is the most populous country in the Arab world, the third-most populous country in Africa, and the 15th-most populous in the world.

By Kestér Kenn Klomegâh

In an interview, Senator Mushahid Hussain, President of Pakistan-Africa Institute for Development and Research (PAIDR), explicitly offers a few important insights into the US-Israeli war on Iran and its implications for BRICS+ and Africa. Here are the interview excerpts:

What’s your interpretation of the US-Israel war on Iran, in the context of developments in the Middle East region?

The US-Israel illegal and unwarranted war on Iran was spearheaded by [Benjamin] Netanyahu (Prime Minister of Israel) and actively supported by [Donald] Trump (President of USA) as a Joint Operation with three fundamental goals: a) decimate the Islamic Revolutionary Regime; b) reshape the Middle East as part of Zionism’s ‘Greater Israel’ Project; c) preclude any possibility of establishing a Palestinian State with Jerusalem as its capital.

What is your assessment of Iran’s joining BRICS+ in 2025, China’s and Russia’s roles as members of this association, in this US-Israel war with Iran?

China and Russia have played, by and large, a low-key diplomatic role in supporting Iran but without any active political initiatives. BRICS is divided from within, as India is keen to curry favour with the USA and avoids close association with BRICS since the time that Trump attacked BRICS last year. But China & Russia are clear political beneficiaries of the war as American prestige is at an all-time low, having got entangled in an unwinnable war, resulting in weakening of the US ‘sole superpower’ image.

As an Asian expert, how would you characterise Africa’s reactions? And do you think that reactions were objectively authentic, basing perspectives broadly on Arab and Middle East contributions to Africa’s development?

Africa’s reactions to the war are primarily through the prism of the Global South, viewing Iran as resisting American-Israeli hegemonic designs, as, for example, manifested in two examples: South Africa’s rejection of American pressures to wean South Africa away from its support for Iran. Plus, Somalia joined Pakistan and China in supporting the Russian resolution in the UN Security Council seeking an immediate ceasefire and negotiations to halt the War, despite strident Western/US opposition to the Russian resolution.

By Adedapo Adesanya

The Director-General (DG) of the World Trade Organisation (WTO), Mrs Ngozi Okonjo-Iweala, has said the global trading system is experiencing the worst disruptions in the past 80 years.

The trade body chief warned about the consequences as the WTO ministerial conference opened Thursday in Cameroon.

“The world order and the multilateral system we know has irrevocably changed,” she said, adding: “We cannot deny the scale of the problems confronting the world today.”

The organisation’s 166 members appear deeply divided as trade ministers gather in the Cameroonian capital for the WTO’s top conference, amid global economic turmoil linked to the Middle East war.

Over four days in Yaounde, WTO members will try to revitalise an institution weakened by geopolitical tensions, stalled negotiations, and rising protectionism — against the backdrop of the war in the Middle East, which poses a serious threat to international trade.

“The scale of the problems confronting the world today, even before the conflict in the Gulf, destabilised trade in energy, fertiliser and food,” Mrs Okonjo-Iweala said.

“National governments and international institutions alike have been struggling to navigate rising geopolitical tensions, intensifying climate pressures, and rapid technological change.

“Accompanying these shifts has been an increasingly loud questioning of multilateralism,” she added.

Mrs Okonjo-Iweala said these disruptions were just one symptom of broader upheavals shaking the international order created after World War II to prevent a repeat of the disasters of the first half of the 20th century.

“It feels appropriate that at the moment when the world is in turmoil with conflict in the Middle East, Sudan, Ukraine, and elsewhere, at this time of great disruption and uncertainty, we have gathered in Africa to discuss the road ahead for the global trading system,” she said.

“Africa is the continent of the future.”

WTO ministerial conferences are typically held every two years. The current edition in Yaounde is the second to be held in Africa, after Nairobi (Kenya) in 2015.

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism10 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz3 years ago

Showbiz3 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn