Economy

Nigeria, SA, 3 Others Attract 58% FDI Projects in Africa

By Dipo Olowookere

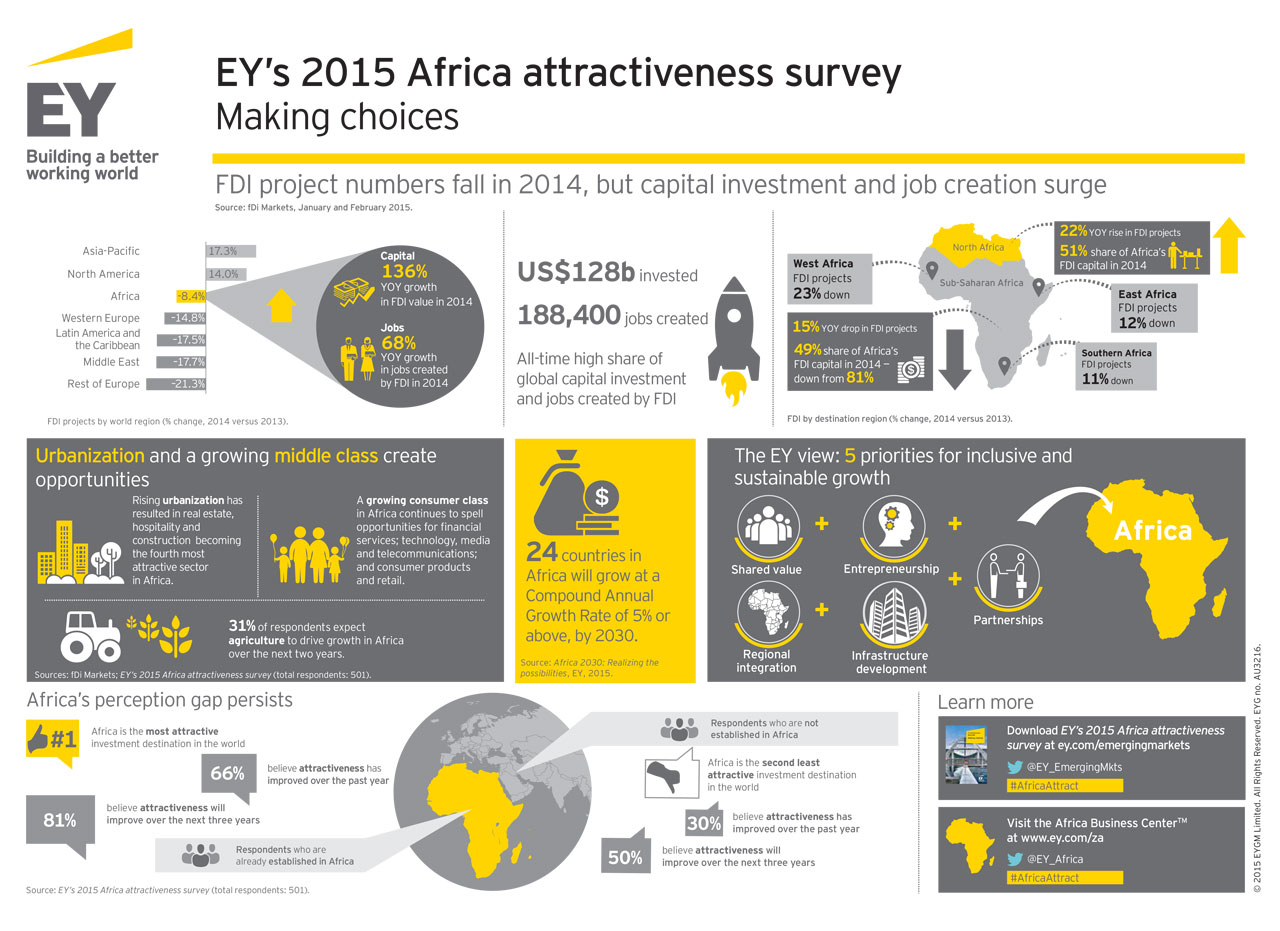

A total of 676 foreign direct investment (FDI) projects were attracted by Africa in 2016, out of which Egypt, Kenya, Morocco, Nigeria and South Africa (the key hub economies) collectively attracted 58 percent, an EY Africa Attractiveness report has disclosed.

However, the report named South Africa as the largest FDI hub in Africa.

The latest Africa Attractiveness, seen by Business Post, provided an analysis of FDI investment into Africa over the past ten years.

The 2016 data showed a decline of 12.3 percent from the total of number of FDI projects attracted the previous year by Africa.

Also, the FDI job creation numbers declined by 13.1 percent, but the capital investment rose by 31.9 percent during the period under review.

The surge in capital investment was primarily driven by capital intensive projects in two sectors, namely real estate, hospitality and construction (RHC), and transport and logistics. The continent’s share of global FDI capital flows increased to 11.4 percent from 9.4 percent in 2015. This made Africa the second-fastest growing FDI destination by capital.

Commenting on the report, Africa CEO at EY, Ajen Sita, noted that, “This somewhat mixed picture is not surprising to us. Investor sentiment toward Africa is likely to remain somewhat softer over the next few years.

This has far less to do with Africa’s fundamentals than it does with a world characterised by heightened geopolitical uncertainty and greater risk aversion. Investors with an existing presence in Africa remain positive about the continent’s longer-term investment attractiveness, but they are also cautious and discerning.”

Asia-Pacific investors are bullish on Africa

In a sign of ongoing diversification of Africa’s FDI investors, more than one fifth of FDI projects and more than half of capital investment into Africa came from Asia-Pacific in 2016, an all-time record. Most notably, Chinese FDI into Africa increased dramatically, making the country the single largest contributor of FDI capital and jobs in Africa in 2016.

Foreign investors refocus on Africa’s hub economies

South Africa remains the continent’s leading FDI destination, when measured by project numbers, increasing 6.9 percent. Morocco regained its place as Africa’s second largest recipient with projects up by 9.5 percent, followed by Egypt, which attracted 19.7 percent more FDI projects than the previous year.

New investment hubs appear in East and West Africa

Although foreign investors still favour the key hub economies in Africa, a new set of FDI destinations is emerging, with Francophone and East African markets of particular interest.

Despite having a 31.7 percent decline in FDI projects in 2016, and weak growth in recent years, West Africa’s second largest economy, Ghana, remains a key FDI market. The country’s improving macro-economic environment and strong governance track record has seen Ghana rise to fourth position in the EY Africa Attractiveness Index (AAI). The index was introduced in 2016, to measure the relative investment attractiveness of 46 African economies based on a balanced set of shorter and longer-term metrics.

Staying in West Africa, Cote d’Ivoire also features in the top 10 of the AAI, and with a 21.4 percent jump in FDI projects in 2016, this illustrates that it’s becoming a country more favoured by investors.

Also in the west, Senegal has emerged as a potential major FDI destination although this is not reflected in its current FDI numbers. It does however rank strongly on the AAI 2017, taking eighth position, due to its diverse economy, strong strides in macro-economic resilience and progress in improving its business environment.

By Adedapo Adesanya

Seplat Energy Plc has signed an agreement with the Nigerian National Petroleum Company (NNPC) Limited to sell a 10 per cent working interest in its joint venture assets for approximately $281.6 million, a move aimed at strengthening its balance sheet while boosting shareholder returns.

The Nigerian energy company, which is listed on both the Nigerian Exchange (NGX) Limited and the London Stock Exchange (LSE), announced on Thursday that its subsidiaries, Seplat Energy Offshore Limited (SEOL) and Seplat Energy Producing Nigeria Unlimited (SEPNU), reached the agreement with the Nigerian oil company following earlier discussions.

The transaction represents about 25 per cent of the gross consideration paid by Seplat for its acquisition of SEPNU, including any contingent payments.

Upon completion of the deal, SEPNU will retain a 30 per cent working interest in the joint venture and continue as operator, while NNPC Limited’s stake will increase from 60 per cent to 70 per cent. Seplat Energy will continue to own 100 per cent of SEPNU’s share capital.

The transaction remains subject to regulatory approvals and other customary closing conditions, with completion expected in the second half of 2026. The effective date has been backdated to April 1, 2026.

Seplat said it intends to deploy the proceeds in line with its capital allocation framework, splitting the funds equally between reducing debt and enhancing shareholder returns.

Subject to the completion of the transaction, the company plans to pay a special cash dividend of about $140 million, equivalent to 23.3 US Cents per share, in addition to its regular performance-based dividend.

The company also disclosed plans to reduce its gross debt by up to $300 million. It noted that $200 million of its Advanced Payment Facility (APF) had already been repaid during the second quarter of 2026, while the remaining $100 million will be settled after the transaction closes.

Seplat said the divestment would not affect production targets for the NNPCL/SEPNU joint venture in 2026, as operational performance has remained strong.

SEPNU currently contributes around 80,000 barrels of oil equivalent per day (kboepd) at the midpoint of Seplat’s 2026 production guidance of 135,000 to 155,000 kboepd. Based on the transaction’s effective date of April 1, 2026, that contribution would reduce to about 65,000 kboepd, with production guidance to be updated after completion.

Looking further ahead, Seplat said the proceeds from the sale and the lower capital expenditure associated with the reduced working interest are expected to largely offset the impact of lower cash flows from the joint venture through 2030.

Consequently, its long-term production target will be revised from 200,000 kboepd to 170,000 kboepd on a net working interest basis.

Despite the adjustment, the company reaffirmed its commitment to distribute between 40 and 50 per cent of free cash flow over the 2026–2030 period and said it remains on track to deliver at least $1 billion in cumulative shareholder distributions.

The transaction will also affect Seplat’s reserves. Based on its latest reserves assessment, the company’s 2P reserves are expected to decline by approximately 13 per cent to 872.9 million barrels of oil equivalent following completion.

Commenting on the agreement, Seplat Energy’s outgoing chief executive, Mr Roger Brown, described the NNPCL/SEPNU joint venture as one of Nigeria’s most strategically important energy assets.

“The NNPCL/SEPNU JV is one of the pre-eminent licence areas in Nigeria and of strategic importance to the country. Our relations with our partner NNPCL are strong, and we are fully aligned on the agreed work programmes.

“Together, we are focused on delivering significant value from the JV, which has responded very well to increased development activity since we became operator and has clear potential to deliver strong production growth well into the next decade,” he said.

Mr Brown added that Seplat’s strong financial position allows it to use the proceeds from the disposal to increase shareholder distributions while further reducing financial leverage, thereby creating greater cash flow flexibility for future returns.

By Aduragbemi Omiyale

A regulated infrastructure designed for the issuance, trading, clearing and settlement of tokenised securities in Nigeria has been launched by NASD OTC Securities Exchange.

This initiative is known as the NASD Digital Securities Platform and was developed with blockchain technology supplied by Blockstation Incorporated.

The platform is anticipated to kick off public market activity with its first digital securities offering in September 2026.

It was learned that the NASD Digital Securities Platform should deepen access to capital and modernise the nation’s capital markets.

This is because it supports fractional investment and improves the efficiency and transparency of securities transactions.

Its market impact will, however, depend on the quality of initial issuances, regulatory clarity, investor protection, custody arrangements, settlement reliability, secondary-market liquidity and the participation of licensed intermediaries.

The platform will enable companies to issue tokenised securities through NASD’s regulated market infrastructure while giving investors access to a new class of regulated digital investment products.

Investors will also require clear disclosure of the rights attached to each digital security, the underlying assets, valuation methodology, technology and cybersecurity risks, transfer restrictions and procedures for enforcing claims.

The initiative is the product of collaboration among NASD, technology providers, regulators and other market participants to establish what the exchange describes as a secure and trusted marketplace for digital securities.

“The NDSP introduces greater transparency, more efficient issuance and trading processes, and modern market infrastructure designed to support the next generation of regulated capital markets.

“We look forward to welcoming issuers, brokers and investors as this market continues to grow,” the acting chief executive of NASD OTC Securities Exchange, Ms Chinwendu Ekeh, commented.

Also, the chief executive of Blockstation Incorporated, Mr Jai Waterman, said, “With one of the youngest and most entrepreneurial populations in the world, Nigeria has an extraordinary opportunity to expand access to regulated capital markets.

“Enabling greater participation in capital formation is an important step toward long-term wealth creation and economic growth.

“We are proud to support NASD in introducing the NDSP and look forward to seeing the market empower the next generation of Nigerian issuers and investors.”

Also commenting, a representative of TK Tech Africa, Mr Damola Akindolire, said, “Opening a new regulated market requires close collaboration between technology providers, market operators, regulators and industry participants. Today’s announcement establishes a strong foundation for future digital securities issuances in Nigeria.”

By Adedapo Adesanya

The Minister of Finance, Mr Taiwo Oyedele, has disclosed that Nigeria’s savings from the removal of fuel subsidies and foreign exchange market reforms have largely been absorbed by higher debt-servicing costs and increased government spending.

Speaking at the Seventh Africa Emerging Markets Forum in Abuja, Mr Oyedele said the reforms introduced by President Bola Tinubu’s administration in 2023 were painful but necessary to restore macroeconomic stability after years of fiscal distortions.

President Tinubu’s subsidy removal and exchange rate liberalisation have won the backing of investors and international lenders but triggered a sharp rise in living costs, prompting questions over how the resulting savings have been utilised.

Mr Oyedele said fuel subsidies and what he described as an implicit subsidy on foreign exchange had previously cost Nigeria about five per cent of its Gross Domestic Product (GDP).

Responding to concerns over the fate of the savings, he acknowledged the public’s demand for accountability.

“I’ve heard this question so many times, and guess what? It’s a valid question,” he said, announcing that the government will soon publish a comprehensive account of how the savings had been spent.

In the meantime, he said, a significant portion had gone into servicing public debt, implementing the new national minimum wage and expanding social intervention programmes.

According to the minister, debt-servicing costs have risen sharply following the reforms, with borrowing rates increasing to as much as 24 per cent from around eight per cent previously.

“Instead of paying about eight per cent on our debts, we’re paying as high as 24 per cent. When you need to service debt, you don’t debate it. You pay, and you pay on time,” he said.

Mr Oyedele also said the government’s wage bill almost doubled after the national minimum wage was raised from N30,000 to N70,000 monthly.

He added that substantial funding had been committed to the Nigerian Education Loan Fund (NELFUND), which now provides tuition support and monthly stipends to more than 1.5 million students.

The minister rejected criticism that the reforms had failed because poverty initially worsened, arguing that temporary hardship was unavoidable after years of economic distortions.

“Before the reforms, we were printing money to spend. If you stop printing, the spending doesn’t disappear. You need to finance the money you were printing before,” he said.

He also dismissed suggestions that continued government borrowing contradicted improved revenue performance, explaining that borrowing remained necessary where approved expenditure exceeded revenue.

“If your budget is 10, your revenue target is six, and you eventually collect seven, you have exceeded your revenue target, but you still need to borrow three,” he said.

Responding to the International Monetary Fund’s 2026 Article IV assessment, Mr Oyedele maintained that the removal of fuel subsidies and adoption of a market-determined exchange rate were necessary reforms to reduce economic risks.

He said the government would measure progress through reductions in multidimensional poverty, improvements in real per capita income and declining income inequality rather than headline GDP growth alone, while insisting the reforms would ultimately translate into better living standards for Nigerians.