Banking

EFCC Arraigns Two FSDH Merchant Bank Employees

By Modupe Gbadeyanka

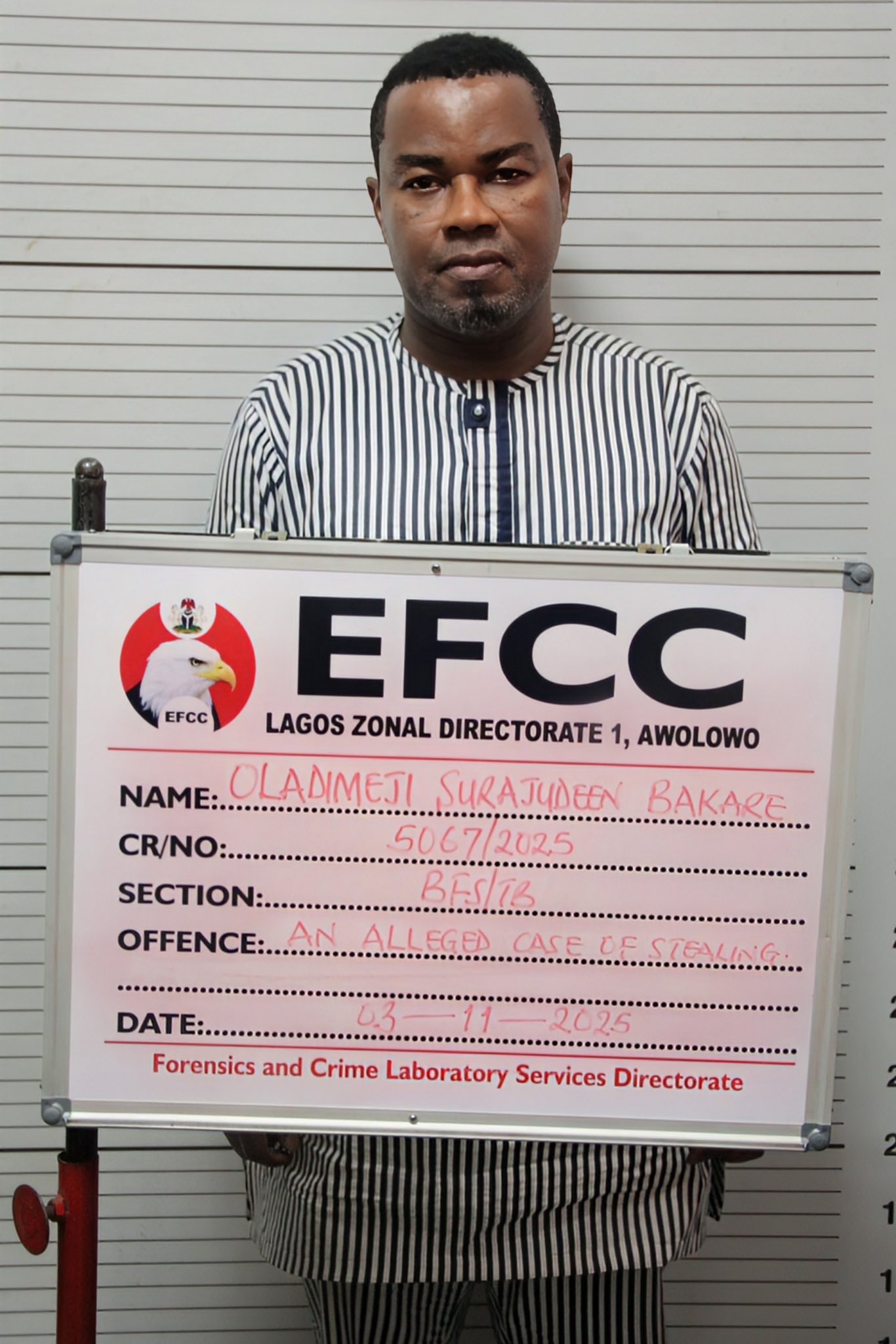

Two employees of FSDH Merchant Bank Limited, Mr Bakare Oladimeji Surajudeen and Mr James Olukayode Imokwede, have been arraigned by the Economic and Financial Crimes Commission (EFCC).

The suspects were brought before Justice Ismaila Ijelu of the Lagos State High Court sitting in Ikeja on Tuesday, March 3, 2026.

They were accused of stealing and retaining stolen property valued at about $306,667.81 and €50,250.

The EFCC, which received a petition from the lender, said its investigations showed that the suspects processed fraudulent transfers through the SWIFT platform to third parties.

The bank said an internal audit uncovered unauthorised debits totalling $306,667.81 and €50,250, equivalent to N527.4 million from its Letters of Credit (LC) payable accounts.

At the court yesterday, after the defendants pleaded “not guilty” to all 10-count charges preferred against them, the prosecution counsel, H. U. Kofarnaisa, asked for a trial date and also prayed that the defendants be remanded in a correctional facility pending trial.

Counsel to the first and second defendants, Oluwaseun Akintunde and Olajide S. Onasanya, informed the court that bail applications had been filed on behalf of the defendants and also urged the court to grant them bail on liberal terms.

They also prayed that the defendants be remanded in the EFCC custody pending the perfection of their bail conditions.

The prosecution counsel, however, opposed the prayers of the defence seeking the remand of the defendants in the EFCC custody, saying that “the EFCC detention facilities are overstretched.”

After listening to both parties, Justice Ijelu granted the defendants bail in the sum of N2 million each, with two sureties in like sum.

The court ordered that one of the sureties must be a relative who is gainfully employed. The sureties must provide evidence of tax payment in the last three years and must show proof of livelihood, with their residences verified.

The defendants were ordered to deposit their international passports with the court, and must not travel outside the country without the leave of the court.

The judge subsequently remanded the defendants in a correctional facility pending the perfection of their bail conditions, and adjourned the matter till March 25, 2026, for the commencement of trial.

Business Post reports that one of the counts said, “That you, Bakare Oladimeji Surajudeen and James Olukayode Imokwede, sometime in 2021 in Lagos within the jurisdiction of this court, dishonestly took the sum of N527,406,916.66, property of FSDH Merchant Bank Limited.”

By Adedapo Adesanya

The Nigeria Deposit Insurance Corporation (NDIC) has commenced the process of paying insured deposits to customers of the 46 microfinance banks whose operating licences were revoked by the Central Bank of Nigeria (CBN).

In a statement issued on Wednesday by the Head of Communication and Public Affairs Department, Mrs Hawwau Gambo, the corporation said it had been appointed the official liquidator of the failed banks following the CBN’s revocation of their licences, which took effect on July 1, 2026.

The NDIC said its appointment was in line with the provisions of the Banks and Other Financial Institutions Act (BOFIA) 2020 and the NDIC Act 2023.

The organisation said the affected banks have ceased to operate as licensed financial institutions and are no longer authorised to carry out banking business in Nigeria.

“The NDIC has commenced the process of the orderly closure of the failed banks with their immediate takeover, verification and payment of insured sums to eligible depositors,” the statement said.

It added that depositors and the general public would be informed of subsequent steps in the liquidation process, warning members of the public against conducting transactions with any of the affected banks following the revocation of their licences.

It also cautioned individuals against removing, concealing or tampering with the assets, records or properties of the failed institutions, noting that such actions could amount to a breach of the law and attract sanctions.

Business Post earlier reported that the CBN revoked the operating licences of the 46 microfinance banks after determining that they no longer met the regulatory conditions required to continue operations.

According to the apex bank, the affected institutions were sanctioned for various regulatory breaches, including insufficient assets to meet liabilities, operating without approval, prolonged inactivity, failure to commence business within the stipulated period and failure to maintain the minimum capital required by law.

The apex bank said the action forms part of its efforts to strengthen financial sector stability, protect depositors and ensure compliance with banking regulations.

The affected institutions are spread across several states, including Lagos, Kano, Abia, Kaduna, Kebbi, Ogun, Niger, Plateau, Rivers, Delta, Benue, Cross River, Ondo, Osun, Anambra, Oyo, Bayelsa, Abuja and Akwa Ibom.

By Modupe Gbadeyanka

Entries for the 2026 edition of the flagship innovation initiative of Wema Bank Plc, Hackaholics, themed Powering Possibilities, opened on Wednesday, July 1.

At a press conference yesterday at its head office in Lagos, Wema Bank said all young Africans with creative tech-driven solutions across Financial Inclusion, Healthcare, Digital Transformation, Education, Sustainability, Social Impact and Future of Work can apply for the programme.

It was stressed that each application is to be made via the portal at hackaholics.wemabank.com, under one of three tracks: The Startup Pitch Competition, Hackathon and the newly introduced Social Impact track.

After the closure of the application window, Hackaholics 7.0 will then proceed on a national tour, which will touch 10 pitch centres across the six geopolitical zones of Nigeria. Each pitch centre will serve as a hub for innovators within the region to pitch their creative solutions and get the opportunity to secure the top spot in their pitch centre, and ultimately, proceed to the grand finale where the winners will be announced.

“As we launch Hackaholics 7.0 today, we are opening up a new phase of opportunities for more Nigerian youth to challenge themselves, explore their creativity and become startup founders.

“I encourage every young Nigerian with a passion for innovation to leverage the opportunity that we have carefully curated through Hackaholics and get ahead of the curve in today’s dynamic work landscape.

“Together, we can continue to build an ecosystem where innovation flourishes, opportunities expand, and young people are empowered to create solutions that shape the future,” Wema Bank’s Divisional Executive for Business Support, Mr Tajudeen Bakare, stated.

Also speaking, the chief executive of Wema Bank, Mr Moruf Oseni, said, “At Wema Bank, we believe that institutions have a responsibility that extends beyond providing commercial services.

“We have a responsibility to create meaningful opportunities, provide the right resources, enable innovation to thrive, and support the ecosystems that will shape today’s youth as well as tomorrow’s economy. This sense of responsibility is what has driven the evolution of Hackaholics from inception to date.

“With Hackaholics, we have, and we are investing in the next generation of innovators, inspiring innovation that will impact lives, strengthening Nigeria’s innovation ecosystem and giving youth a platform to make meaningful use of their creativity; and the numbers continue to speak volumes.”

Launched in 2019, Hackaholics is Wema Bank’s youth- and tech-focused initiative designed to serve as a platform for young Africans with creative, game-changing, tech-driven ideas and products to bring their ideas to life.

Since its launch, Hackaholics has discovered thousands of groundbreaking solutions, supported over 10,000 startups, engaged 50,000 participants, developed over 100 solutions from scratch and disbursed $500.0 million in grant prizes to dozens of winners whose remarkable solutions have earned a top spot in the past 6 editions.

By Aduragbemi Omiyale

The operating licenses of 46 microfinance banks in the country have been revoked by the Central Bank of Nigeria (CBN).

A statement on Wednesday from the banking sector regulator disclosed that the action followed failure by the affected small lenders to comply with regulatory requirements.

The central bank said it had to enforce its powers under Sections 12 and 13 of the Banks and Other Financial Institutions Act (BOFIA), 2020, to withdraw the licenses of the banks.

“The revocation of the licenses is part of the Bank’s ongoing efforts to safeguard the stability of the financial sector, protect depositors, and ensure that licensed institutions comply with current laws and regulatory requirements,” a part of the circular dated Wednesday, July 1, 2026, and signed by the acting Director of the Corporate Communications Department of the CBN, Mrs Hakama Sidi-Ali, stated.

The apex bank listed five violations by the 46 microfinance banks, including insufficient assets to meet liabilities, closure of operations without the CBN’s approval, inactivity and cessation of financial intermediation, failure to commence operations within 12 months of licence approval, and failure to maintain minimum capital funds unimpaired by losses.

Another part of the notice disclosed that, “The revocation was approved by the Governor of the Central Bank of Nigeria, Mr Olayemi Cardoso, following the banks’ failure to meet the regulatory requirements for continued operation as licensed financial institutions.”

The affected financial institutions are;

| S/NO | MFB | CATEGORY | STATE |

| 1 | Minji-Se Churchill MFB | Tier 1 | Rivers |

| 2 | Merchant MFB | Tier 2 | Abia |

| 3 | Janmaa MFB | Tier 1 | Kwara |

| 4 | Busu MFB | Tier 2 | Niger |

| 5 | Gold MFB | Tier 1 | Lagos |

| 6 | Zain MFB (foremerly Dawakin Tofa MFB) | Tier 2 | Kano |

| 7 | Bompai MFB | Tier 1 | Kano |

| 8 | Ajwa MFB (Formerly Gezawa) | Tier 2 | Kano |

| 9 | NOW NOW DIGITAL MFB | Tier 2 | Kano |

| 10 | Crystabel Microfinance Bank | Tier 1 | Bayelsa |

| 11 | Chanelle MFB | State | Lagos |

| 12 | Abia SME MFB | Tier 1 | Abia |

| 13 | Kamba MFB | Tier 2 | Kebbi |

| 14 | Iwade MFB | Tier 2 | Ogun |

| 15 | Winview MFB | Tier 1 | Abuja |

| 16 | Zuru MFB | Tier 2 | Kebbi |

| 17 | Minjibir MFB | Tier 1 | Kano |

| 18 | Shanono MFB | Tier 2 | Kano |

| 19 | Sumaila MFB | Tier 2 | Kano |

| 20 | Rimin Gado MFB | Tier 2 | Kano |

| 21 | Mwaghavul MFB | State | Plateau |

| 22 | Sycamore MFB | Tier 2 | Kano |

| 23 | TOFA MFB | Tier 2 | Kano |

| 24 | Safegate MFB | Tier 1 | Lagos |

| 25 | Creekline MFB | Delta | Tier 2 |

| 26 | Bestar MFB | Tier 1 | Oyo |

| 27 | Livingspring MFB | Tier 1 | Cross River |

| 28 | Apple MFB | Tier 2 | Ogun |

| 29 | Stanford MFB | State | Uyo |

| 30 | Frontline MFB | Tier 2 | Anambra |

| 31 | Zafec MFB | Tier 2 | Kaduna |

| 32 | Supreme MFB | Tier 1 | Lagos |

| 33 | Bejin-Doko MFB | Tier 2 | Niger |

| 34 | Kanopoly MFB | Tier 1 | Kano |

| 35 | Bellbank MFB formerly Tsanyawa | Tier 2 | Kano |

| 36 | Yeneng MFB | Tier 2 | Plateau |

| 37 | Creditville MFB | Tier 1 | Lagos |

| 38 | MBAG MFB | Tier 1 | Lagos |

| 39 | STRAIGHT SAHARA MFB | Tier 1 | Benue |

| 40 | OURPASS MFB | Tier 2 | Ondo |

| 41 | VERDANT MFB | Tier 1 | Lagos |

| 42 | BASAWA MFB | Tier 2 | Kaduna |

| 43 | CASHA MFB | Tier 2 | Abuja |

| 44 | ESTEEM MFB | Tier 2 | Kano |

| 45 | ENTERPRENEUR MFB | Tier 1 | Lagos |

| 46 | AVANTUS MFB | Tier 2 | Osun |

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism10 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz4 years ago

Showbiz4 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn