Banking

Online Loans in Nigeria—from the Beginnings to the Present

In the past, borrowing money meant waiting in stuffy office branches where you might not get the needed money. Nowadays, the world is moving forward, and we have the opportunity to take advantage of today’s digital advances to get money instantly, wherever we are. Just type “Get a loan” in your browser search engine, and you will get dozens of results with companies that offer loans in just a few taps of your mobile phone screen.

Waiting in a bank vs. an instant loan

In the past, you had to make an appointment at a bank or wait in a long line to be called by a loan officer. In addition, you required collateral, official employment, and a large package of documents. Nowadays, you don’t even have to imagine such a tedious task because with the widespread use of the Internet. You can simply choose a lender through advertising, searching on the Internet, or through friends who have already used the services of online companies and can advise you.

Fintech in Nigeria

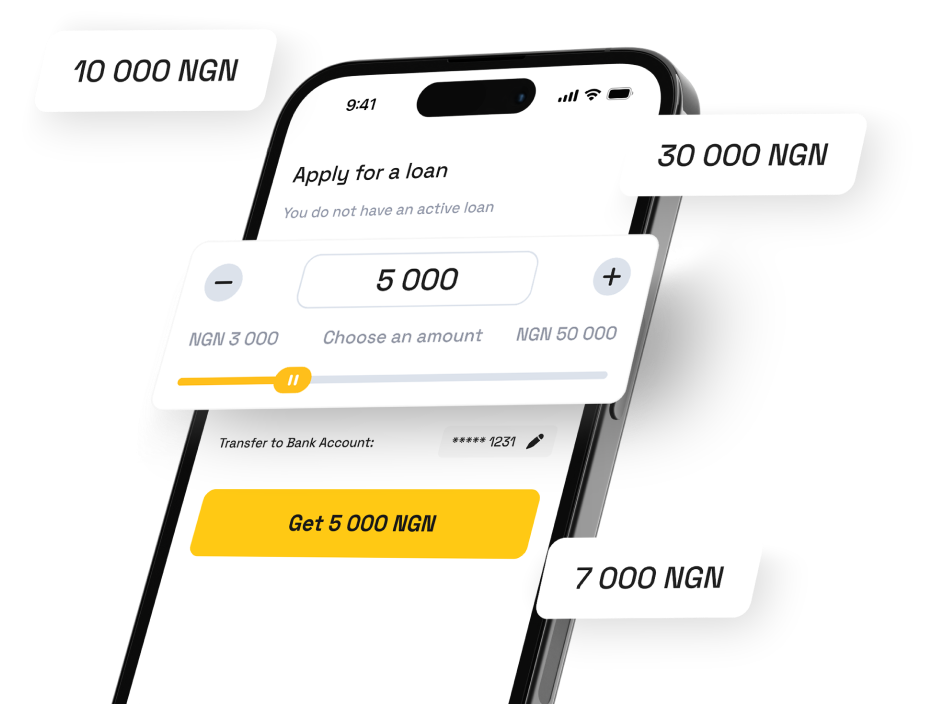

Fintech is a breakthrough of the 21st century. It has expanded the horizons of loan users by creating platforms such as CashX, Carbon, FairMoney, and Branch. Customers instantly caught the wave and preferred these companies because of their reliability and ease of access to funds.

For example, CashX offers online loan in Nigeria from ₦5000 to ₦300,000. In addition, the company guarantees fast processing of applications: only 15 minutes — no physical documents required — and the money is already in your bank account. Carbon is a preferred choice for those looking for savings and investment options. Older companies such as FairMoney and Branch also use a similar methodology.

Real-life examples of when online loans are the best option

For example, Adanna owns a beauty salon in Lagos. Business is hard, and people often don’t want to do serious business with her because there is still a perception that women are better off doing light work or housework. But no, Adanna is determined to move up the career ladder and make her hair salon one of the best in the city. She turned to CashX, got a loan for her supplies (dye, brushes, cosmetics, etc.) and had funds left over to promote her brand through social media targeting. She invested wisely and repaid the company’s debt on time, as she only required the money to pursue her brilliant ideas. Furthermore, she is a talented and hardworking person herself, so she knows how to invest money in a way that makes it work for her. She quickly gained a clientele through advertising and hired a few more assistants because she couldn’t handle the influx of customers. And now her business is booming. Adanna’s story is just one of many.

You can get money not only for business. Most of us have faced situations where things get tough, and we urgently need money. There are many situations when loans become lifelines and provide great opportunities.

Look for reliable companies

Here are four of the best companies currently operating in the Nigerian financial market, and we’ll briefly introduce each of them.

- CashX: a young company whose main goal is to satisfy the needs of consumers in a way that competitors cannot. Comfortable conditions, easy access, and fast money transfers.

- Carbon: a well-known and trusted company.

- FairMoney: perfect for small needs.

- Branch: a company with good support on all issues, often offering effective advice on their social media.

Why do Nigerians frequently apply for online loans?

They always know what to expect. No collateral is required, the application process is easy, and the user’s account contains comprehensive information on how much and when to return the money. Customers can take out a loan for any purpose: from buying a crib for a child to starting a business. The only advice that applies not only to fintech companies but also to cooperation with banks: always take only the amount that you can comfortably and timely repay. This is your area of responsibility.

On the future of online lending in Nigeria

Fintech is rapidly gaining momentum; therefore, more and more companies will appear every year. The competition will become even higher, and brands will fight for customers. This is beneficial for users, as they will be able to choose the best financial assistance and use the money on the most favorable terms. There will be personalized offers, additional discounts, new functionality, etc. And of course, all of this will be regulated by the Central Bank of Nigeria (CBN) for security and to ensure the best experience for Nigerians.

By Adedapo Adesanya

The Nigeria Deposit Insurance Corporation (NDIC) says it has paid the insured deposits of about 700,000 customers of the defunct Heritage Bank and has commenced the reimbursement of depositors of 46 microfinance banks (MFBs) whose operating licences were recently revoked by the Central Bank of Nigeria (CBN).

The chief executive of NDIC, Mr Oludare Sunday, made this known on Wednesday during a retreat for members of the House of Representatives Committee on Insurance and Actuarial Matters in Lagos.

He said the corporation immediately began settling the insured deposits of customers after the CBN revoked the licences of the 46 microfinance banks and appointed the NDIC as their provisional liquidator.

“We are working on those. The CBN revoked the licences, and we were appointed as the provisional liquidator. We have started paying depositors of those banks, and gradually we intend to cover all the insured depositors,” he said.

Mr Sunday explained that the NDIC’s responsibility extends beyond paying insured deposits to recovering outstanding loans owed to the failed institutions and disposing of their assets to generate funds for the settlement of uninsured depositors.

“Our function as liquidator involves the payment of guaranteed sums. Thereafter, we go after those who owe the institutions and have not paid. We also ensure that we sell the available assets and realise their investments towards paying the uninsured portion of the deposits. So, we have started paying the guaranteed deposits. What we are doing now is also realising the assets of those institutions,” he stated.

Although he declined to disclose the exact number of depositors of the failed microfinance banks who had been reimbursed, Sunday said the Corporation was working with the Nigerian Interbank Settlement System (NIBSS) to identify depositors through their Bank Verification Numbers (BVN) to ensure seamless payments.

“So, the more accounts we discover, the more payments we make,” he added.

Providing an update on the liquidation of Heritage Bank, the NDIC chief said about 700,000 depositors had already received their insured deposits, while efforts were ongoing to trace other customers whose identities could not be verified from available records.

He attributed the challenge to legacy accounts created before the introduction of the BVN system, as well as incomplete customer records inherited from banks that were later merged into Heritage Bank.

“If you know Heritage Bank, you know it is an amalgamation of several banks, including the acquisition of Enterprise Bank in 2014. So, if you think of banks like Guardian Express and Spring Bank, they are all part of Heritage Bank.

“There are depositors we have not been able to trace, and this is an opportunity for them to come forward. I am sure many of us did the National Youth Service Corps (NYSC) and may have left some money in an account, but there was no BVN then.

“Even the addresses we had were sometimes things like ‘opposite filling station.’ How do you trace such a person? Once they come forward, and for those we have been able to identify from the institution’s database, we have been paying them,” he explained.

Mr Sunday added that the Corporation would continue to recover outstanding loans and dispose of Heritage Bank’s assets to generate funds for the payment of liquidation dividends to depositors whose balances exceeded the insured limit.

Earlier in his remarks, he described the NDIC as a critical pillar of Nigeria’s financial safety net, stressing the need for stronger collaboration between regulators and the National Assembly as the banking sector responds to recapitalisation efforts and rapid financial technology developments.

According to him, while the ongoing banking recapitalisation programme has strengthened the resilience of financial institutions, it must be complemented by sound corporate governance, effective risk management, strict regulatory compliance and robust supervision to safeguard long-term financial system stability.

He also disclosed that more than 98 per cent of depositors, representing over 281 million accounts across insured financial institutions, are fully protected under the NDIC’s deposit insurance scheme.

By Adedapo Adesanya

Zenith Bank Plc is investigating an incident involving unauthorised access to customers’ data, noting that the breach does not involve financial information and has not compromised its banking services or digital channels.

In an email sent to customers on Wednesday, the bank stated that the incident was part of a broader global cyberattack affecting multiple international organisations across various sectors.

The lender stated that it immediately activated its incident response protocols and intensified its cybersecurity and remediation efforts upon discovering the incident.

“This incident is part of a broader, global cyber-attack targeting multiple international organisations across various sectors. Upon discovery, we promptly activated our incident response protocols, cybersecurity actions and remediation efforts,” the bank said.

The bank reassured customers that its banking services and digital channels remain secure and fully operational.

As a precautionary measure, Zenith Bank advised customers to remain alert to potential phishing attempts and other forms of social engineering.

“As a precaution, we encourage our customers to remain vigilant against phishing emails, text messages, or phone calls, and never to disclose their password, PIN, One-Time Password (OTP), or other security credentials to anyone,” the bank said.

The incident is the latest in a series of cybersecurity challenges facing Nigerian financial institutions, with banks in recent months suspending their social media operations over impersonation and other fraudulent activities.

Earlier in April, the Nigeria Data Protection Commission (NDPC) said it was investigating alleged data breaches involving Sterling Bank, Remita and the Corporate Affairs Commission (CAC).

Nigerian banks have long been prime targets for cybercriminals because of the vast amounts of customer data and financial transactions they handle every day.

While many attacks have traditionally sought to steal funds, cybercriminals are increasingly targeting personal information, which can be used for identity theft, phishing schemes, account takeovers and other forms of financial fraud.

Cybersecurity threats have increasingly targeted Nigerian banks in recent years. In 2025, Union Bank of Nigeria warned customers about fraudulent websites and phishing campaigns designed to steal login credentials and personal information by impersonating the bank.

In August 2024, Guaranty Trust Bank experienced a domain-related security incident that temporarily disrupted access to its official website, although the lender assured customers that their deposits and banking services remained secure while it resolved the issue.

By Adedapo Adesanya

The chairman of First HoldCo Plc, Mr Femi Otedola, has affirmed plans to increase his 26 per cent holding in the organisation to 51 per cent, confirming a planned takeover of Nigeria’s oldest banking institution.

Mr Otedola spoke in an exclusive interview with Nairametrics published on Monday, giving a rare direction following recent speculations about the financial institution.

The milestone followed a series of share acquisitions, as Mr Otedola sought to tighten his grip as the company’s largest shareholder following the recent acquisition of additional shares worth N222.21 billion.

In the interview, the mogul said he has invested more than N600 billion of his personal wealth in First HoldCo, describing the move as a “long-term generational commitment” rather than another turnaround investment he would eventually exit.

Responding to speculation that he intends to consolidate his position in the group, Mr Otedola hinted that his investment journey is far from over.

“My investment threshold is always over and above 51 per cent,” he said. “One of my key investment principles is that firm shareholder control, with due regard for minority interest, is a key ingredient to executing reforms and restructuring to deliver value to all stakeholders.”

The businessman said the same strategy had guided his investments in African Petroleum Plc, later renamed Forte Oil Plc, where he gradually increased his shareholding from 28 per cent to 75 per cent before exiting the company in 2019.

He said he also increased his stake in Geregu Power Plc from 51 per cent to 95 per cent before reducing it to 77 per cent after the company’s public listing.

“I am on the same trajectory with First HoldCo Plc,” Mr Otedola said.

“To date, I have invested over N600 billion of my personal wealth in First HoldCo Plc — a figure that speaks not to speculation, but to unflinching confidence in the institution’s future, fundamentals and an unwavering personal commitment to its success.”

Mr Otedola said his decision to invest in First HoldCo came at a time when the institution was facing one of the most challenging periods in its history.

The billionaire steadily increased his investment in the group, accelerating his share purchases in 2026. His stake grew from 6.68 billion shares (15.95 per cent) in June 2025 to 8.06 billion shares by March 2026, then to 9.28 billion shares by June after acquiring about 1.22 billion shares in one quarter. A further purchase through Calvados Global Services last month lifted his holdings above 10 billion shares for the first time.