Economy

API Architecture: The Invisible Engine Powering Modern Banking

By Echezona Agubata

Banking has evolved far beyond the days of paper ledgers and long queues. Today, it’s a dynamic force driving Nigeria’s economy, responding to customers in real time, and powering digital innovation. The unsung hero behind this transformation is the Application Programming Interface (API)—a tool that lets bank systems communicate seamlessly with each other and external partners.

In Nigeria’s fast-growing digital finance landscape, APIs are the invisible engine enabling banks to offer instant balance checks, process payments at retail checkouts, or verify identities for loan approvals. The secret to their success? A robust API architecture, the structured framework that makes banking secure, scalable, and innovative.

Picture API architecture as a bridge connecting islands of financial services. It allows banks to share data securely. In Nigeria, where digital banking is literarily booming, APIs let banks like Coronation Merchant Bank expand services without rebuilding infrastructure. This flexibility fuels innovation, enabling tailored solutions for everyone from small businesses to large corporations.

The Central Bank of Nigeria (CBN) along with Industry players ensure this ecosystem is secure and trustworthy. Its regulations mandate standards like OAuth 2.0 for authentication, tokenization to protect data, and encrypted channels to safeguard transactions. Real-time monitoring and customer consent protocols further build trust, ensuring data is shared only with permission. These rules aren’t just technical or ethical—they’re the backbone of Nigeria’s open banking system, fostering collaboration and innovation.

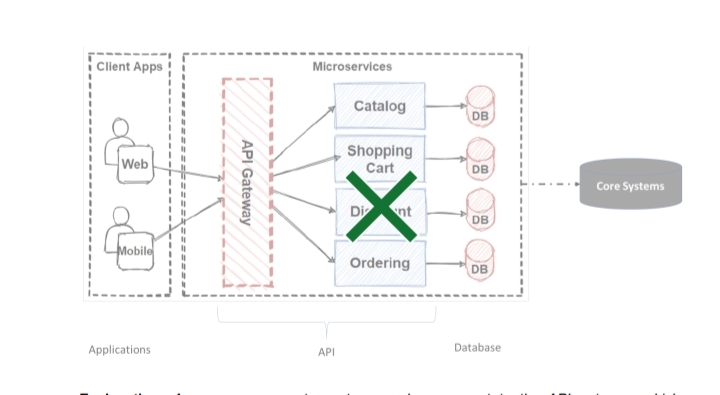

How do APIs work? Imagine a well-orchestrated machine. The API acts as

● A Gateway: the gatekeeper to a product. It authenticates requests and ensures only authorized people are granted access to the product. It also helps limit the number of requests that can be made for the product at any given time. For instance, when a bank’s mobile app requests a customer’s transaction history, the transaction history API (as a gateway) verifies access (both customer and mobile app) before treating the transaction history request.

- A Guide: the protocol or security who ensures that even authenticated users are only allowed to access products and data that they are authorized to have

- A Funnell: the pipe that ensures that authenticated users access products and data from known locations/sources to known destinations

- An Agent: the agent that ensures that applications regardless of the service offering have access to data/products in the same way as every other application. This gives unified experience across respective platforms that are consuming the service/data offered by the API

Here’s a simplified view of the flow:

Explanation: An app or corporate system sends a request to the API gateway, which authenticates and routes it. The orchestration layer processes it using endpoints, pulling data from the core system via middleware.

The orchestration layer (behind the gateway) breaks services—like catalog, shopping cart, or ordering—into modular endpoints, like building blocks online shops can share securely. The modular endpoints connect these APIs to core systems, translating the requests into formats that can be processed by the core system. Companies also provide developer portals with clear documentation and sandbox environments, simplifying integration for partners.

This architecture can be built for scale. Banks process millions of transactions daily using load balancing to scale out resources, and distribute traffic in a dynamic fashion. This architecture could incorporate the use of in-memory databases and Queueing technologies to cache frequently used data for swifter processing. More so, this introduces rate limiting features which help isolate any problem areas without affecting the entire service as a whole.

Challenges abound. One of such is the existence of legacy systems as many banks and organizations often rely on decades-old mainframes (core systems), thus requiring a middleware solution to bridge old and new systems—a complex but critical step. Another recent challenge is the need to enforce data privacy expectations, this has made encryption and data masking a necessary action. Encryption in itself comes with its own attendant side-effects especially where applied on data without proper service governance. It can slow performance, so banks and organizations use caching and optimized data flows to balance speed and security. Compliance with CBN guidelines and Nigeria’s data privacy laws demands robust

consent management and audit trails. Versioning APIs (e.g., /v1/payments) prevents disruptions when systems evolve.

Real-world examples highlight APIs’ impact. Coronation Merchant Bank built the Dangote ISOP Collection API to streamline payments for Dangote’s distributors. These payments were previously riddled with slow reconciliations and delayed cash flow. The API integrates payments directly into Dangote’s ERP system and thereby automating the process, reducing errors, and strengthening business ties. Another bank used a KYC API to verify customer identities for loan applications, cutting onboarding time while meeting CBN standards. A third example involves a major Nigerian bank’s payment API, which enables instant corporate transfers for retailers, ensuring funds clear in seconds during peak sales.

APIs are also driving open finance. The CBN’s 2023 guidelines expand APIs to cover credit, investment, and insurance data, enabling embedded finance—loans at retail checkouts or savings tools linked to salary accounts. This makes banking invisible yet ever-present, blending into daily life.

The future is exciting. Banks are adopting API-first design, prioritizing APIs as core interfaces for faster innovation. AI-driven APIs are emerging, enabling fraud detection or tailored loan offers. Blockchain-based APIs promise secure cross-border payments. Event-driven architectures, using tools like Kafka, process real-time events like transaction alerts, boosting efficiency.

At Coronation Merchant Bank, our APIs are business enablers. Our custom solutions, like the Dangote integration, solve real-world problems, while our investment banking desk advises on capital raising and partnerships, helping clients stay competitive. APIs lower barriers, drive growth, and deliver seamless experiences for customers.

Nigeria’s financial future isn’t about who holds the most assets—it’s about who builds the strongest connections between data, money, and people. API architecture is the invisible engine powering that future, creating a connected, inclusive banking ecosystem.

By Adedapo Adesanya

The NASD Over-the-Counter (OTC) Securities Exchange extended its stay in the south territory with a decline of 0.56 per cent on Wednesday, April 2.

This brought down the market capitalisation by N13 billion to N2.417 trillion from N2.430 trillion, and downed the NASD Unlisted Security Index (NSI) by 22.57 points to 4,062.87 points from the previous session’s 4,062.87 points.

It was observed that the NASD exchange ended with three price gainers and three price losers during the trading day.

MRS Oil Plc depreciated by N19.00 to close at N171.00 per unit compared with the previous price of N190.00 per unit, NASD Plc lost N4.14 to trade at N37.36 per share compared with Wednesday’s N41.50 per share, and Central Securities Clearing System (CSCS) Plc gave up N2.00 to sell at N78.00 per unit versus N80.00 per unit.

On the flip side, FrieslandCampina Wamco Nigeria Plc appreciated by 19 Kobo to N93.00 per share from N92.81 per share, Food Concepts Plc expanded by 15 Kobo to N2.87 per unit from N2.72 per unit, and Great Nigeria Insurance (GNI) Plc improved by 2 Kobo to 52 Kobo per share from 50 Kobo per share.

Yesterday, the volume of securities dipped by 91.8 per cent to 260.2 million units from 3.2 billion units, the value of securities went down by 98.1 per cent to N154.2 million from N8.3 billion, while the number of deals soared by 53.3 per cent to 46 deals from 30 deals.

GNI Plc was the most active stock by value on a year-to-date basis with 3.4 billion units worth N8.4 billion, followed by CSCS Plc with 56.9 million units valued at N3.9 billion, and Okitipupa Plc with 27.5 million units traded for N1.8 billion.

The most traded stock by volume on a year-to-date basis was also GNI Plc with 3.4 billion units sold for N8.2 billion, trailed by Resourcery Plc with 1.1 billion units exchanged for N415.7 million, and Infrastructure Guarantee Credit Plc with 400 million units transacted for N1.2 billion.

By Adedapo Adesanya

The Naira dropped N2.09 or 0.15 per cent against the United States Dollar in the Nigerian Autonomous Foreign Exchange Market (NAFEX) on Thursday, April 2, to trade at N1,380.79/$1 compared with Wednesday’s rate of N1,378.70/$1.

However, it appreciated against the Pound Sterling in the official market by N2.77 to quote at N1,824.86/£1 versus the N1,836.57/£1 it was traded at midweek, and improved its value against the Euro by N10.54 to N1,591.92/€1 from N1,602.46/€1.

Yesterday was the last trading session of the week for the local currency in the spot market, as the market will be closed on Friday and Monday for the Easter Holiday.

At the black market, the Nigerian Naira maintained stability against the greenback yesterday at N1,405/$1, but gained N8 at the GTBank FX counter to settle at N1,388/$1, in contrast to the previous session’s N1,396/$1.

Pressure eased on the domestic currency as strong policy indicators have helped calm the majority of worries within the financial systems. Particularly in the remittance segment, the apex bank has directed all International Money Transfer Operators (IMTOs) to route remittance transactions through designated Naira settlement accounts in banks, a move aimed at boosting transparency and channelling more foreign exchange into the formal market.

This helps take off pressure from the foreign reserves, which have fallen below the $50 billion mark as they are gradually decreasing rather than falling sharply.

Meanwhile, the cryptocurrency market was bullish on Thursday, as macro sentiment shifted against recent optimism after reports that Iran is drafting a protocol with Oman to manage traffic through the Strait of Hormuz, easing concerns about disruptions to a key global oil route.

The remarks came after U.S. President Trump on Wednesday night vowed to hit Iran “extremely hard” in the coming weeks and that the Strait of Hormuz would “open naturally” once the war ends.

Cardano (ADA) chalked up 1.9 per cent to trade at $0.2435, Dogecoin (DOGE) grew by 1.2 per cent to $0.0912, Ethereum (ETH) appreciated by 0.8 per cent to $2,066.37, Bitcoin (BTC) added 0.5 per cent to sell at $67,080.53, Solana (SOL) increased by 0.5 per cent to $79.91, and Ripple (XRP) jumped 0.2 per cent to $1.31.

Conversely, Binance Coin (BNB) dipped 0.7 per cent to $586.90, and TRON (TRX) depreciated by 0.3 per cent to $0.3147, while the US Dollar Tether (USDT) and the US Dollar Coin (USDC) closed flat at $1.00 each.

By Dipo Olowookere

The local stock market was relatively flat on Friday, as the bears and the bulls shared the spoils of war, though investor sentiment turned bullish compared with the preceding session’s bearish posture.

Data from the Nigerian Exchange (NGX) Limited showed that the All-Share Index (ASI) was marginally down by 4.66 points as it ended at 201,698.89 points versus Wednesday’s 201,703.55 points, and the market capitalisation slightly contracted by N3 billion to N129.806 trillion from N129.809 trillion.

Customs Street was shut on Friday because of the public holidays declared by the federal government today and next Monday.

Business Post reports that John Holt declined by 9.91 per cent to N15.45, Abbey Mortgage Bank shed 9.60 per cent to trade at N8.95, International Energy Insurance slipped by 6.48 per cent to N3.32, Chams shrank by 5.30 per cent to N3.75, and Tantalizers depreciated by 5.18 per cent to N4.03.

On the flip side, Unilever Nigeria improved by 10.00 per cent to N103.40, Fortis Global Insurance gained 9.82 per cent to trade at N1.23, Multiverse appreciated 9.81 per cent to N20.15, Legend Internet advanced by 9.38 per cent to N6.30, and Zichis grew by 9.02 per cent to N14.14.

The market breadth index was positive during the trading session, as there were 35 appreciating stocks and 24 depreciating stocks.

Yesterday, investors traded 560.0 million equities valued at N19.3 billion in 49,676 deals, in contrast to the 815.5 million equities worth N33.3 billion transacted in 52,641 deals in the preceding day, representing a drop in the trading volume, value, and number of deals by 31.33 per cent, 42.04 per cent, and 5.63 per cent, respectively.

Secure Electronic Technology dominated the activity log with 59.7 million shares valued at N61.1 million, Wema Bank exchanged 52.0 million equities worth N1.4 billion, VFD Group transacted 36.0 million stocks for N410.5 million, Access Holdings sold 35.3 million shares valued at N914.8 million, and Chams traded 31.0 million equities worth N115.0 million.

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism10 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz3 years ago

Showbiz3 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn