Economy

API Architecture: The Invisible Engine Powering Modern Banking

By Echezona Agubata

Banking has evolved far beyond the days of paper ledgers and long queues. Today, it’s a dynamic force driving Nigeria’s economy, responding to customers in real time, and powering digital innovation. The unsung hero behind this transformation is the Application Programming Interface (API)—a tool that lets bank systems communicate seamlessly with each other and external partners.

In Nigeria’s fast-growing digital finance landscape, APIs are the invisible engine enabling banks to offer instant balance checks, process payments at retail checkouts, or verify identities for loan approvals. The secret to their success? A robust API architecture, the structured framework that makes banking secure, scalable, and innovative.

Picture API architecture as a bridge connecting islands of financial services. It allows banks to share data securely. In Nigeria, where digital banking is literarily booming, APIs let banks like Coronation Merchant Bank expand services without rebuilding infrastructure. This flexibility fuels innovation, enabling tailored solutions for everyone from small businesses to large corporations.

The Central Bank of Nigeria (CBN) along with Industry players ensure this ecosystem is secure and trustworthy. Its regulations mandate standards like OAuth 2.0 for authentication, tokenization to protect data, and encrypted channels to safeguard transactions. Real-time monitoring and customer consent protocols further build trust, ensuring data is shared only with permission. These rules aren’t just technical or ethical—they’re the backbone of Nigeria’s open banking system, fostering collaboration and innovation.

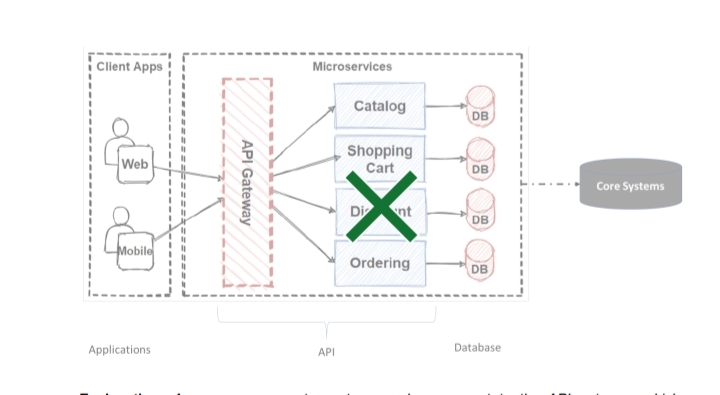

How do APIs work? Imagine a well-orchestrated machine. The API acts as

● A Gateway: the gatekeeper to a product. It authenticates requests and ensures only authorized people are granted access to the product. It also helps limit the number of requests that can be made for the product at any given time. For instance, when a bank’s mobile app requests a customer’s transaction history, the transaction history API (as a gateway) verifies access (both customer and mobile app) before treating the transaction history request.

- A Guide: the protocol or security who ensures that even authenticated users are only allowed to access products and data that they are authorized to have

- A Funnell: the pipe that ensures that authenticated users access products and data from known locations/sources to known destinations

- An Agent: the agent that ensures that applications regardless of the service offering have access to data/products in the same way as every other application. This gives unified experience across respective platforms that are consuming the service/data offered by the API

Here’s a simplified view of the flow:

Explanation: An app or corporate system sends a request to the API gateway, which authenticates and routes it. The orchestration layer processes it using endpoints, pulling data from the core system via middleware.

The orchestration layer (behind the gateway) breaks services—like catalog, shopping cart, or ordering—into modular endpoints, like building blocks online shops can share securely. The modular endpoints connect these APIs to core systems, translating the requests into formats that can be processed by the core system. Companies also provide developer portals with clear documentation and sandbox environments, simplifying integration for partners.

This architecture can be built for scale. Banks process millions of transactions daily using load balancing to scale out resources, and distribute traffic in a dynamic fashion. This architecture could incorporate the use of in-memory databases and Queueing technologies to cache frequently used data for swifter processing. More so, this introduces rate limiting features which help isolate any problem areas without affecting the entire service as a whole.

Challenges abound. One of such is the existence of legacy systems as many banks and organizations often rely on decades-old mainframes (core systems), thus requiring a middleware solution to bridge old and new systems—a complex but critical step. Another recent challenge is the need to enforce data privacy expectations, this has made encryption and data masking a necessary action. Encryption in itself comes with its own attendant side-effects especially where applied on data without proper service governance. It can slow performance, so banks and organizations use caching and optimized data flows to balance speed and security. Compliance with CBN guidelines and Nigeria’s data privacy laws demands robust

consent management and audit trails. Versioning APIs (e.g., /v1/payments) prevents disruptions when systems evolve.

Real-world examples highlight APIs’ impact. Coronation Merchant Bank built the Dangote ISOP Collection API to streamline payments for Dangote’s distributors. These payments were previously riddled with slow reconciliations and delayed cash flow. The API integrates payments directly into Dangote’s ERP system and thereby automating the process, reducing errors, and strengthening business ties. Another bank used a KYC API to verify customer identities for loan applications, cutting onboarding time while meeting CBN standards. A third example involves a major Nigerian bank’s payment API, which enables instant corporate transfers for retailers, ensuring funds clear in seconds during peak sales.

APIs are also driving open finance. The CBN’s 2023 guidelines expand APIs to cover credit, investment, and insurance data, enabling embedded finance—loans at retail checkouts or savings tools linked to salary accounts. This makes banking invisible yet ever-present, blending into daily life.

The future is exciting. Banks are adopting API-first design, prioritizing APIs as core interfaces for faster innovation. AI-driven APIs are emerging, enabling fraud detection or tailored loan offers. Blockchain-based APIs promise secure cross-border payments. Event-driven architectures, using tools like Kafka, process real-time events like transaction alerts, boosting efficiency.

At Coronation Merchant Bank, our APIs are business enablers. Our custom solutions, like the Dangote integration, solve real-world problems, while our investment banking desk advises on capital raising and partnerships, helping clients stay competitive. APIs lower barriers, drive growth, and deliver seamless experiences for customers.

Nigeria’s financial future isn’t about who holds the most assets—it’s about who builds the strongest connections between data, money, and people. API architecture is the invisible engine powering that future, creating a connected, inclusive banking ecosystem.

By Dipo Olowookere

The first trading session of the week on the floor of the Nigerian Exchange (NGX) Limited ended in the green territory on Monday, with a 1.20 per cent rise.

This was buoyed by the gains recorded by Airtel Africa and other equities, according to analysis of data harvested from the Customs Street yesterday.

During the trading day, the consumer goods index grew by 0.76 per cent, enough to offset the losses recorded by the other sectors.

The insurance counter shrank by 1.64 per cent, the banking space lost 0.24 per cent, the energy sector contracted by 0.09 per cent, and the industrial goods segment retreated by 0.05 per cent.

When trading activities ended for the day, the All-Share Index (ASI) was up by 2,956.15 points to 248,529.75 points from 245,573.60 points, and the market capitalisation gained N1.909 trillion to finish at N160.422 trillion compared with the previous session’s N158.513 trillion.

Fortis Global Insurance expanded by 10.00 per cent to N2.86, Chams surged by 9.80 per cent to N4.48, NAHCO jumped by 9.29 per cent to N153.00, Airtel Africa soared by 8.59 per cent to N6,300.00, and Sovereign Trust Insurance rose by 6.59 per cent to N1.78.

Conversely, AVA Capital shed 10.00 per cent to N9.90, Ecobank decreased by 9.92 per cent to N64.95, Caverton crashed by 9.09 per cent to N5.00, Ikeja Hotel slipped by 8.41 per cent to N43.00, and FTN Cocoa dropped 8.37 per cent to trade at N8.10.

A total of 23 equities were on the gainers’ chart yesterday, while 37 equities ended on the losers’ table, indicating a negative market breadth index and weak investor sentiment.

As for the activity log, the trading volume remained elevated, though lower than the preceding session, as it receded by 26.67 per cent to 1.1 billion units from 1.5 billion units. The trading value, however, increased by 1.12 per cent to N27.0 billion from N26.7 billion, while the number of deals advanced by 39.00 per cent to 59,185 deals from 42,580 deals.

Consolidated Hallmark was the most active stock yesterday, with a turnover of 354.1 million units valued at N1.5 billion, Fortis Global Insurance traded 307.3 million units worth N818.3 million, Access Holdings exchanged 48.1 million units for N1.4 billion, Chams transacted 37.4 million units worth N163.3 million, and First Holdco sold 35.8 million units valued at N5.1 billion.

By Adedapo Adesanya

Oil prices traded 5 per cent higher on Monday after Iran and the United States argued about demands for compensation, further stalling a possible deal to reopen the Strait of Hormuz.

Brent crude futures chalked up $4.17 or 4.99 per cent to sell at $87.72 a barrel, while the US West Texas Intermediate (WTI) crude futures surged $3.95 or 5.05 per cent to $82.13 per barrel.

Iran said the US must lift sanctions on it and meet other conditions for reopening the vital waterway, which carried a fifth of the world’s oil and liquefied natural gas before the start of the Middle East conflict in late February.

Meanwhile, US President Donald Trump said Iran must pay compensation for “all of the people that they have killed and gravely wounded.”

This comes as the Middle East country said it was nearing a final pact with Oman to define new shipping lanes through the strait but repeated that the US must meet other conditions, including compensation and an end to sanctions and military threats before the strategic waterway is reopened.

In a further threat to supply, the Iran-aligned Houthis said they had struck Saudi Aramco’s Jazan refinery on Sunday. Saudi Aramco has postponed the restart of the 400,000-barrel-per-day refinery to August 30 after two Houthi attacks in recent weeks.

ADNOC, a state-owned oil company in the United Arab Emirates, said on Friday that 15 of its vessels had been attacked while transiting the Strait of Hormuz since the beginning of the conflict.

Meanwhile, Ukraine’s military continued to attack Russia’s energy infrastructure, hitting the Taneco oil refinery in Tatarstan and the ZapSibNeftekhim petrochemical plant in Russia’s Tyumen region.

On the US supply side, stocks of crude oil in the Strategic Petroleum Reserve (SPR) fell by about 6.1 million barrels to 298.7 million barrels last week, the lowest level since January 1983.

Bank of America (BoFA) warned that oil prices could continue climbing into the winter if the US and Iran fail to reach an agreement reopening the Strait of Hormuz, with severe shortages already emerging in diesel, petrol, and global natural gas markets.

Mr Francisco Blanch, Bank of America’s head of commodities and derivatives research, told CNBC on Monday that only around 5 to 10 ships per day are currently passing through Hormuz, compared with roughly 140 before the war. With some crude now being rerouted through Saudi Arabia and the UAE, traffic would need to recover to around 80 to 100 ships per day just to stabilise energy markets.

By Adedapo Adesanya

The Senate Committee on Banking, Insurance and Other Financial Institutions has called for stronger collaboration among financial sector regulators and other stakeholders to strengthen Nigeria’s financial system and support sustainable economic growth.

The committee made the call during an expanded stakeholders’ engagement in Lagos, attended by the leadership of the Central Bank of Nigeria (CBN), Nigeria Deposit Insurance Corporation (NDIC), Asset Management Corporation of Nigeria (AMCON), National Insurance Commission (NAICOM) and Nigeria Export-Import Bank (NEXIM), among other industry stakeholders and financial experts.

Chairman of the committee, Mr Adetokunbo Abiru (Lagos East), who was represented by Mr Osita Izunaso (Imo West), said stronger legislative reforms and regulatory collaboration were necessary to reposition Nigeria’s financial architecture for long-term economic prosperity.

Mr Abiru said the financial sector remained critical to investment, job creation, business expansion and macroeconomic stability, stressing that its ability to mobilise savings, channel credit to productive sectors, facilitate investment and manage risks was fundamental to sustainable economic growth.

He said the current economic realities required closer collaboration between the legislature and financial regulators, noting that challenges confronting the sector were interconnected and could not be effectively addressed through isolated interventions.

The lawmaker identified inflationary pressures, global economic uncertainties, cybersecurity threats, low insurance penetration and the need to diversify Nigeria’s export base as some of the challenges requiring coordinated policy responses.

He said the engagement was aimed at generating practical solutions to strengthen the country’s financial architecture and support sustainable economic growth.

According to him, monetary policy, financial safety nets, banking institutions, the insurance industry and export finance were interdependent components of a stable financial system and must therefore be strengthened collectively.

The Commissioner for Insurance and Chief Executive Officer of the National Insurance Commission (NAICOM), Mr Olusegun Ayo Omosehin, said the Nigeria Insurance Industry Reform Act (NIIRA) 2025 had contributed significantly to stabilising and repositioning the insurance sector.

Mr Omosehin disclosed that 43 insurance companies had successfully recapitalised, describing the development as a major milestone for the industry.

He commended Abiru and members of the committee for their role in advancing insurance sector reforms and urged the House of Representatives to expedite action on the relevant insurance reform bill to enable it to receive presidential assent and become operational.

Representatives of the CBN Governor and the Managing Directors of AMCON, NEXIM and NDIC also commended the Senate committee for its oversight and legislative support, saying its interventions had strengthened the agencies’ capacity to discharge their statutory mandates.

The engagement, held under the theme, Strengthening Financial System Architecture for Sustainable Economic Growth and Stability in Nigeria, also featured presentations by Professor Uche Uwaleke, President of Capital Market Academics of Nigeria (CMAN); Professor Biodun Adedipe, Chief Consultant, B. Adedipe Associates Limited; and Dr Tilewa Adebajo, Chief Executive Officer of CFG Advisory.

The experts presented policy recommendations on key issues affecting Nigeria’s financial system, with emphasis on financial stability, investment and sustainable economic growth.

Mr Abiru said the Senate would continue to engage financial regulators and other stakeholders to deepen financial inclusion, strengthen public confidence in financial institutions and improve regulatory effectiveness.

He said the broader objective was to position Nigeria’s financial system to compete more effectively in the global economy while remaining resilient and responsive to the country’s economic transformation agenda.