Economy

CAC Threatens to Sanction Companies With Unissued Shares

By Modupe Gbadeyanka

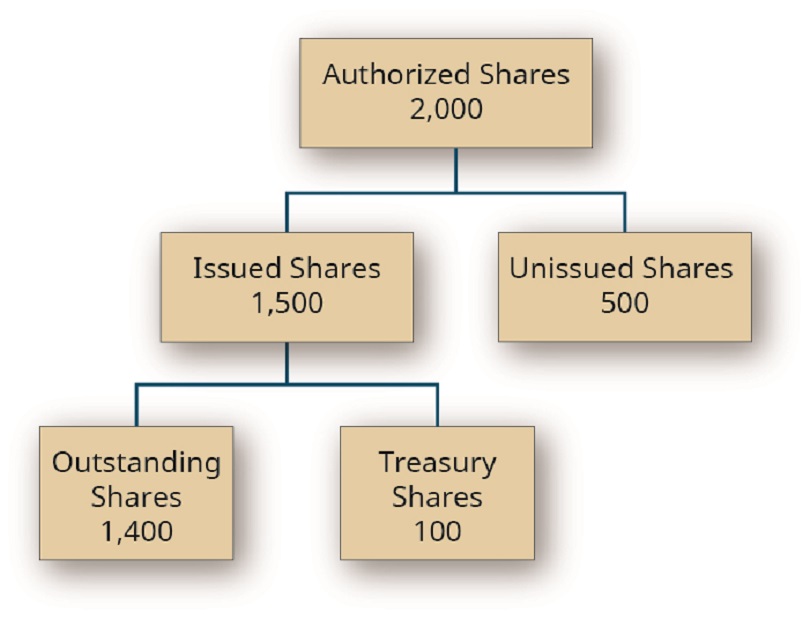

Companies operating in Nigeria, which failed to cancel or issue all their unissued shares to their shareholders before the deadline of December 31, 2022, would be sanctioned alongside their directors.

Business Post reports that the Companies and Allied Matters Act (CAMA) 2020 replaced the authorised share capital in CAMA 1990 with minimum issued share capital.

In the abolished law, organisations were required to issue at least 25 per cent of their authorised share capital, but under the new law, the entire share capital must be fully issued at all times, cancelling the ability of companies to retain unissued shares for future allotments.

This was captured in Section 124 of the law, which said “no company shall have a share capital which is less than its minimum issued share capital and that every company with unissued shares, must not later than six (6) months from the commencement of CAMA 2020, issue shares up to an amount, not below its minimum issued share capital.”

The Corporate and Affairs Commission (CAC), which regulates the registration and running of registered organisations in Nigeria, extended the deadline for the cancellation of all unissued shares of firms to December 31, 2022.

Most companies on the Nigerian Exchange (NGX) Limited held their extraordinary general meetings (EGMs) last year to comply with this new law, but a few did not.

According to a circular issued by the CAC, such erring organisations would be severely sanctioned.

“Further to the notice of the commission dated April 16, 2021, on the extension of the period for existing companies to comply with the requirements of issued share capital under the Companies and Allied Matters Act 2020 and the Companies Regulations 2021 to December 31, 2022, and in line with the last paragraph of the notice, customers and general public are hereby reminded that any application filed in compliance with the requirements after the extended date (being December 31, 2022) shall attract daily default penalty against the company and each officer of the company for every day during which the shares remained unissued after the extended date and in accordance with Regulations 13(2) of the CR,” the notice emphasised.

Recall that in 2021, President Muhammadu Buhari signed the CAMA into law. Many stakeholders applauded the new law because of the innovative changes it brought into play, including making it possible for an individual to establish a company as a sole director.

By Adedapo Adesanya

The oil market slid about 2 per cent on Wednesday after paring deeper losses earlier in the trading session, as Iran reviewed a proposal by the United States to end the war that has disrupted global energy flows.

Brent futures fell $2.27 or 2.2 per cent to settle at $102.22 a barrel, while the US West Texas Intermediate (WTI) crude futures lost $2.03 or 2.2 per cent to trade at $90.32 per barrel.

It was reported that Iran was still reviewing a US proposal to end the war in the Gulf, despite an initial response that was negative, indicating that it had so far stopped short of rejecting it outright.

Pakistan delivered the 15-point proposal on behalf of the US government, and the consideration appeared to signal that at least some figures in Iran may be considering it.

Meanwhile, the White House Press Secretary, Mrs Karoline Leavitt, said President Donald Trump would hit Iran harder if it fails to accept that the Middle East country has been “defeated militarily”.

Currently, the market is facing the biggest-ever oil supply disruption as the US-Israel war has halted shipments of oil and liquefied natural gas through the Strait of Hormuz, which typically carries about 20 per cent of the world’s LNG and crude supply.

Market analysts noted that this has resulted in around 20 million barrels of crude losses daily, or some 500 million barrels, or five full days of global supply, since the war began on February 28. Countries have started rationing fuel use.

India, one of the world’s largest oil consumers, has bought its first cargo of Iranian liquefied petroleum gas in years after the US temporarily removed sanctions.

Meanwhile, Japan has called on the International Energy Agency (IEA) for an additional coordinated release of oil stockpiles, as it seeks to shield consumers from higher energy prices.

In Venezuela, oil production, including condensate and gas liquids, reached 1.1 million barrels per day in March.

Amid these developments, Russia’s major export terminals suspended crude oil and oil products loadings after massive Ukrainian drone attacks sparked blazes. At least 40 per cent of Russia’s oil export capacity has been halted following Ukrainian drone attacks on its energy infrastructure.

The US Energy Information Administration (EIA) said energy firms added 6.9 million barrels of crude into stockpiles during the week ended March 20.

That was higher than the build of 2.4 million barrels reported by the American Petroleum Institute (API) on Tuesday.

By Dipo Olowookere

The Nigerian Exchange (NGX) Limited remained in the green territory on Wednesday after further appreciating by 0.11 per cent, driven by gains in bellwethers like MTN Nigeria, GTCO, and others.

Data from Customs Street showed that the insurance and the consumer goods sectors went up by 0.76 per cent and 0.42 per cent apiece, offsetting the 0.98 per cent loss posted by the banking index and the 0.11 per cent decline suffered by the industrial goods counter. The energy sector closed flat at the close of transactions.

When the closing gong was beaten at midweek, the All-Share Index (ASI) increased by 219.87 points to 200,925.75 points from 200,705.88 points, and the market capitalisation went up by N141 billion to N128.977 trillion from N128.836 trillion.

Investor sentiment remained strong yesterday after the bourse recorded 36 price gainers and 33 price losers, representing a positive market breadth index.

Legend Internet grew by 10.00 per cent to N7.26, Zichis gained 9.93 per cent to settle at N11.40, Premier Paints expanded by 9.93 per cent to N31.00, John Holt improved by 9.79 per cent to N15.70, and Consolidated Hallmark advanced by 6.26 per cent to N5.26.

On the flip side, Fidson declined by 9.97 per cent to N94.85, Austin Laz lost 9.89 per cent to quote at N4.01, Living Trust Mortgage Bank shrank by 7.08 per cent to N4.46, Secure Electronic Technology slumped by 7.04 per cent to N1.32, and Sterling Holdco depreciated by 5.56 per cent to N7.65.

The busiest equity for the day was Wema Bank, which transacted 104.3 million units worth N2.8 billion. Access Holdings traded 42.8 million units valued at N1.1 billion, Zenith Bank exchanged 33.9 million units for N3.6 billion, Zichis sold 26.6 million units worth N221.2 million, and GTCO recorded a turnover of 25.6 million units valued at N2.9 billion.

In all, investors bought and sold 538.0 million units for N25.4 billion in 45,641 deals on Wednesday compared with the 1.3 billion units worth N65.3 billion traded in 89,949 deals on Tuesday, implying a decrease in the trading volume, value, and number of deals by 58.62 per cent, 61.10 per cent, and 49.26 per cent apiece.

By Aduragbemi Omiyale

The federal government, through the Minister of Women Affairs and Social Development, is working together with the Nigerian Exchange (NGX) Group Plc to deepen the participation of women in capital markets.

The Minister of Women Affairs and Social Development, Ms Imaan Sulaiman-Ibrahim, underscored the urgency of inclusion in achieving national economic ambitions.

“The capital market reflects our collective choices, who participates, who has access, and who benefits. Women remain underrepresented in formal finance despite their critical role in Nigeria’s productivity.

“Through strategic partnerships and targeted interventions, we are working to change this narrative and expand opportunities for women across the economy.

“Achieving a one-trillion-dollar economy requires the full participation of Nigerian women,” she said at the closing gong ceremony at the NGX on Tuesday in Lagos.

She said the government was ready to partner with capital market stakeholders to expand financial access and unlock opportunities for women across the country.

Welcoming the Minister, the chairman of NGX Group, Mr Umaru Kwairanga, commended the Ministry’s leadership in promoting women’s development and economic participation.

“Women are central to Nigeria’s economic progress. As we work towards a more inclusive and resilient economy, the capital market remains a vital platform for expanding access to finance, supporting women-led enterprises, and enabling broader participation in wealth creation.

“NGX Group remains committed to partnering with the Ministry to drive sustainable impact and empower the next generation of women leaders,” he stated.

Also speaking, the Director General of the Securities and Exchange Commission (SEC), Mr Emomotimi Agama, emphasised the importance of deliberate inclusion.

“Behind every successful market are women. For Nigeria’s capital market to reach its full potential, we must be intentional about empowering women as active participants.

“Current participation levels do not yet reflect our population or potential. Collaborations like this send a strong call to action for more women across Nigeria to engage with the market and contribute to national growth,” the SEC chief stated.

On his part, the chief executive of NGX Group, Mr Temi Popoola, said, “At NGX Group, we are building a dynamic and inclusive market ecosystem that expands access to investment opportunities and supports diverse participants. Through partnerships such as this, we are unlocking new pathways for women to participate as investors, entrepreneurs, and wealth creators.”

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism10 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz3 years ago

Showbiz3 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn