Economy

MasterCard Partners Varsity on Mobile Biometrics in Financial Services

By Modupe Gbadeyanka

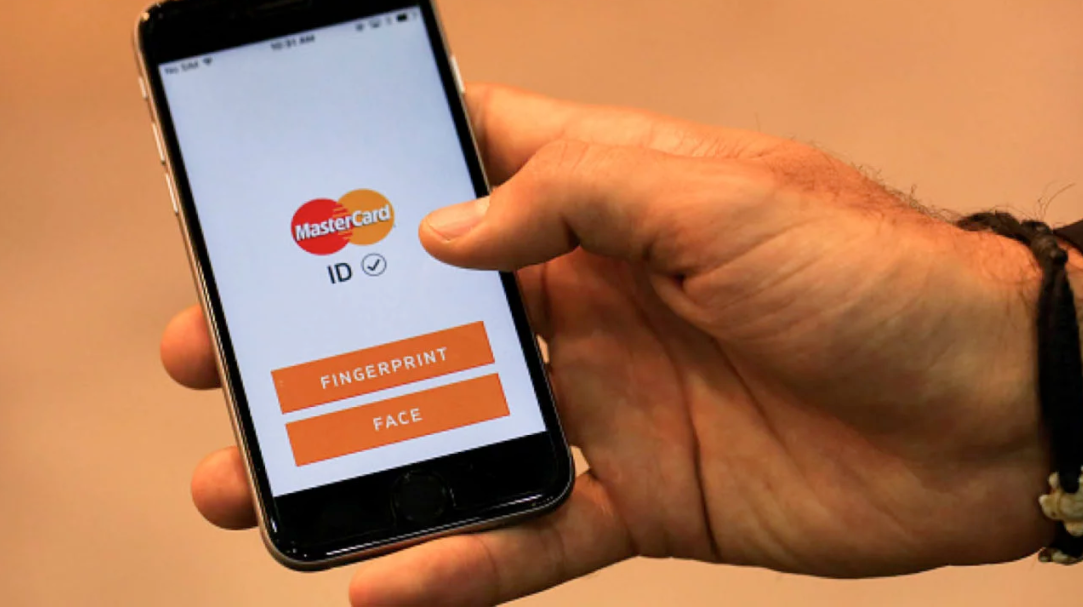

People unlock their phone and, increasingly, shop and pay with the touch of their finger. They don’t get locked out when they forget a password because it has been replaced with a simpler, more secure option, mobile biometrics.

Whether using a fingerprint, an iris scan or a “selfie” to confirm identity, banks see biometric technology as a way to provide greater convenience and security to customers as they use their accounts.

But, it’s still early days in mobile biometrics, and a new report from MasterCard and the Department of Computer Science at the University of Oxford highlights a big barrier.

Only 36 percent of relevant banking executives feel they have adequate experience to deliver.

To overcome this knowledge gap, ‘Mobile Biometrics in Financial Services: A Five Factor Framework’ explores this fast-evolving technology landscape and provides bank executives with guidelines to successfully bring mobile biometrics to life. Simply put, they need to focus on Performance, Usability, Interoperability, Security and Privacy.

Some of these factors are more visible to the consumer, having a real impact on user experience, while others operate behind the scenes. But, long-term success for a bank requires that they address all factors equally to protect against threats.

The framework can help financial service companies avoid the trap of focusing only on the ones their customers see.

“Biometric authentication has a lot of potential, but it is important to address the objectives of each of the Five Factors when designing solutions. Working together with MasterCard enables us to solve for realistic threats to the industry with the best technical and scientific ideas. Users will need consistency, quality and assured security for this technology to thrive,” said Professor Ivan Martinovic, Department of Computer Science at the University of Oxford.

Mr Ajay Bhalla, president, Global Enterprise Risk & Security, MasterCard, commented on the research initiative in a blog published today, saying, “Effective mobile biometrics melt into the broader experience of consumer-centric financial services, giving people the power to instantly access their financial information or make a payment. They’re driving the trend toward a password-free future where digital identity is all about who we are, not what we remember.”

Considering that global sales of smartphones are expected to reach $400 billion by next year, people everywhere will increasingly have access to the tool that makes mobile biometrics possible.

Banks see that as an opportunity, and with initiatives like the collaboration with the University of Oxford and pioneering biometrics solutions like MasterCard Identity Check Mobile, MasterCard is a partner to deliver widespread and responsible adoption of mobile biometric solutions in financial services.

As Bhalla continued, “This framework is fundamental to accelerating the deployment of mobile biometrics for consumers and industry alike, but collaboration is key. We can only achieve this if industry, academia, governments and technology vendors understand and contribute to the evolution of the Five Factor Framework for mobile biometrics.”

“MasterCard and Oxford have done important work in exposing some of the root causes for the inconsistent adoption of mobile biometrics in financial services,” said Ravin Sanjith, Program Director: Intelligent Authentication, Opus Research. “We expect the Five Factor Framework to become an indispensable aide for industry professionals and decision makers to have better informed, strategic discussions that drive towards more efficient and successful high-scale implementations.”

An Opus Research synopsis of the research contains a breakdown of the critical issues financial service companies need to address to successfully guide their businesses through the biometric journey, ensuring they’re making the right decisions every step of the way. The white paper is now available here.

In addition, a webinar on the Five Factor Framework will be hosted by Opus, in collaboration with MasterCard, on July 11.

By Adedapo Adesanya

NASD Over-the-Counter (OTC) Securities Exchange remained in the negative territory after it further depreciated by 0.64 per cent on Friday, July 24, despite recording four price gainers.

The NASD Security Index (NSI) dropped 27.4 points at the close of business to settle at 4,294.75 points versus the previous day’s 4,383.48 points, while the market capitalisation gave up N16.49 billion to end at N2.577 trillion, in contrast to the N2.594 trillion it ended a day earlier.

The bourse was down during the session amid heavy sell-offs, with the volume of transactions skyrocketing by 693.9 per cent to 2.99 million units from Thursday’s 377,635 units.

Equally, the value of trades went up by 71.6 per cent to N69.4 million from N40.4 million, and the number of deals increased by 41.0 per cent to 55 deals from the preceding day’s 39 deals.

Great Nigeria Insurance (GNI) Plc remained the most active stock by value on a year-to-date basis, with 3.4 billion units worth N8.4 billion, trailed by Infrastructure Credit Guarantee (Infracredit) Plc with 2.3 billion units sold for N6.5 billion, and Central Securities Clearing System (CSCS) Plc with 75.6 million units traded for N5.4 billion.

GNI Plc was also the most active stock by volume on a year-to-date basis, with 3.4 billion units exchanged for N8.4 billion, trailed by Infracredit Plc with 2.3 billion units transacted for N6.5 billion, and Resourcery Plc with 1.1 billion units valued at N415.7 million.

The market ended the session with four price gainers and two price losers, led by FrieslandCampina Wamco Nigeria Plc, which lost N7.44 to trade at N136.19 per share compared with the previous day’s N143.63 per share, and CSCS Plc, which declined by N1.64 to N93.63 per unit from N95.27 per unit.

But MRS Oil gained N13.50 to sell at N148.50 per share versus N135.00 per share, Afriland Properties Plc advanced by 56 Kobo to N17.41 per unit from N16.85 per unit, UBN Property Plc surged by 18 Kobo to N1.93 per share from N1.75 per share, and Food Concepts Plc climbed by 1 Kobo to N2.50 per unit from N2.49 per unit.

By Dipo Olowookere

Nigeria’s stock exchange succumbed to profit-taking on Friday, losing 0.19 per cent when the closing gong was hit at 4 pm.

Shares in the banking and energy sectors influenced the decline suffered by the Nigerian Exchange (NGX) Limited during the session, as they respectively closed lower by 0.40 per cent and 0.04 per cent.

The industrial goods index was flat yesterday, while the insurance counter gained 0.68 per cent and the consumer goods space chalked up 0.25 per cent. The gains by these two segments could not keep Customs Street in the green territory at the close of business.

As a result, the All-Share Index (ASI) retreated by 474.00 points to 247,357.40 points from 247,831.40 points, and the market capitalisation decreased by N306 billion to N159.588 trillion from N159.894 trillion.

Presco dropped 10.00 per cent during the trading day to close at N2,070.00, Thomas Wyatt crumbled by 9.93 per cent to N3.63, Trans-Nationwide Express plunged by 8.44 per cent to N2.82, Royal Exchange slipped by 7.86 per cent to N1.29, and LivingTrust Mortgage Bank shrank by 7.32 per cent to N3.80.

On the flip side, C&I Leasing improved by 9.48 per cent to N6.35, Cornerstone Insurance rose by 9.09 per cent to N6.00, RT Briscoe jumped by 8.61 per cent to N13.25, Honeywell Flour expanded by 7.38 per cent to N17.45, and Africa Prudential increased by 6.98 per cent to N13.80.

Despite the poor performance, the local bourse recorded a positive market breadth index after finishing with 35 price gainers and 25 price losers, representing strong investor sentiment.

It was a relatively quiet market on Friday, as the activity level dropped, with the trading volume down by 27.72 per cent to 565.5 million units from 782.4 million units, and the trading value contracted by 46.89 per cent to N29.9 billion from N56.3 billion, while the number of deals executed by investors soared by 16.03 per cent to 53,688 deals from 46,273 deals.

Access Holdings was the busiest stock for the session, with a turnover of 128.0 million units sold for N3.8 billion, First Holdco transacted 35.4 million units worth N4.3 billion, Chams exchanged 34.8 million units valued at N154.3 million, Zenith Bank traded 30.4 million units for N3.9 billion, and UBA sold 30.4 million units worth N1.5 billion.

By Adedapo Adesanya

The Naira marked a whole week of appreciation against the United States Dollar on Friday, July 24, further gaining N5.67 or 0.41 per cent to close at N1,362.09/$1 in the Nigerian Autonomous Foreign Exchange Market (NAFEX) compared with N1,367.76/$1 it ended on Thursday.

Equally, the local currency appreciated against the Pound Sterling in the official FX market yesterday by N10.83 to trade at N1,813.62/£1 versus the preceding day’s N1,824.45/£1, and improved against the Euro by N7.68 to settle at N1,549.10/€1, in contrast to the N1,556.78/€1 it was exchanged a day earlier.

However, at the parallel market and GTBank forex counter, the Nigerian currency remained unchanged against the greenback during the session at N1,400/$1 and N1,379/$1, respectively.

The Central Bank of Nigeria (CBN) buffer has been strengthened with sustained foreign portfolio inflows and robust foreign reserves, which stand above $52 billion.

The apex bank’s policy signals that the Naira will be stronger in the near term, with Nigeria clearing hurdles with FX reforms and settlement of all backlogs.

However, some traders expect that pressure may come due to foreign-currency buying from fuel importers as they make Dollar purchases to build inventories.

Meanwhile, Bitcoin (BTC), in the digital currency landscape, trimmed recent gains as it fell by 2.3 per cent to $63,787.73.

The weak action in the AI momentum trade is feeding through to crypto as well.

Further, Cardano (ADA) dropped 3.7 per cent to close at $0.1615, Solana (SOL) dipped by 2.8 per cent to $73.71, Ripple (XRP) crashed by 2.3 per cent to $1.08, Ethereum (ETH) slid by 1.9 per cent to $1,851.58, Dogecoin (DOGE) retreated by 0.8 per cent to $0.0694, Binance Coin (BNB) contracted by 0.7 per cent to $564.18, and TRON (TRX) lost 0.5 per cent to trade at $0.3292, while the US Dollar Tether (USDT) and the US Dollar Coin (USDC) traded flat at $1.00 each.