Economy

NGX Group to Unveil ‘The Stock Africa is Made of’ Campaign

By Dipo Olowookere

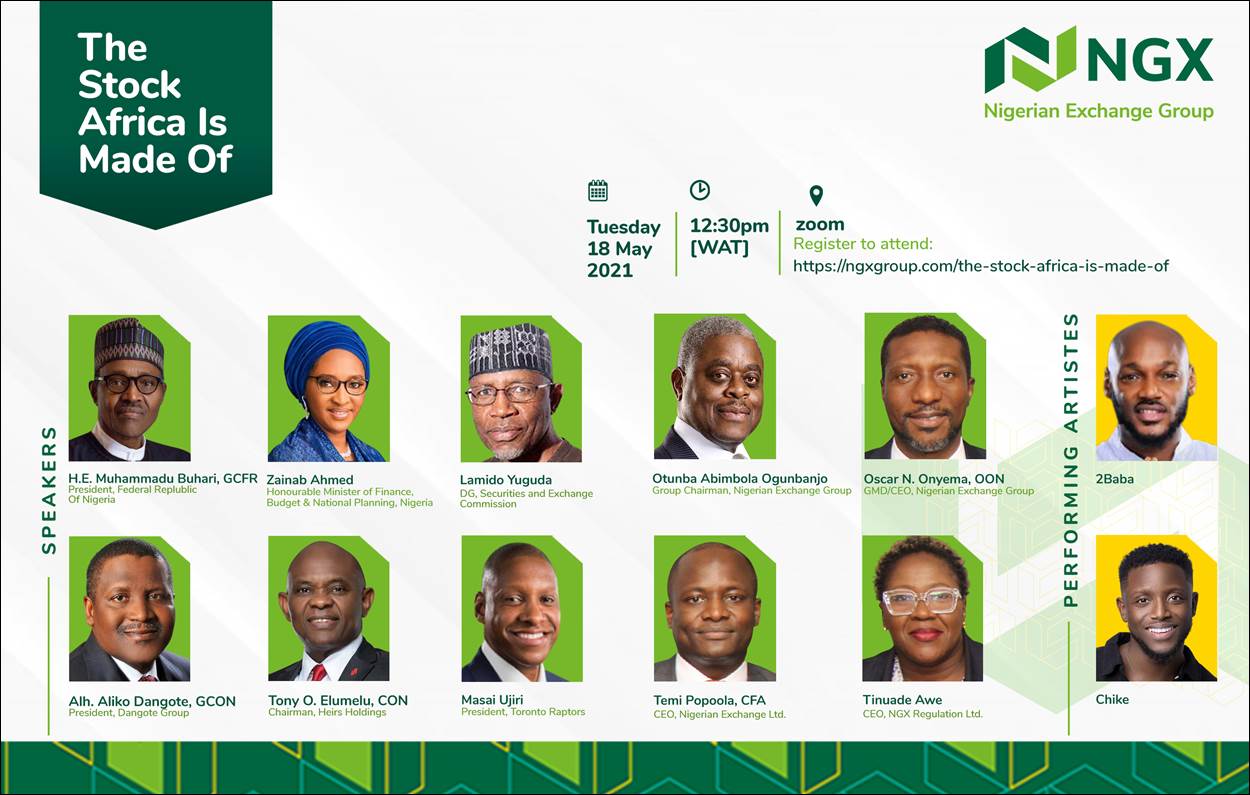

The Nigerian Exchange (NGX) Group Plc will on Tuesday, May 18, 2021, launch a campaign called The Stock Africa is Made of.

This campaign comes on the back of the successful transformation of the defunct Nigerian Stock Exchange (NSE) to the NGX Group and its three subsidiaries – Nigerian Exchange (NGX) Limited, NGX Regulation (NGX RegCo) Limited and NGX Real Estate (NGX RelCo) Limited.

The Stock Africa is Made of was designed to project the NGX Group’s new positioning and commitment to the African financial markets as a leading capital market infrastructure provider, connecting Nigeria, Africa and the world.

The initiative will amplify NGX Group’s new brand identity and spotlight the growth potential of the African continent.

Business Post gathered that the virtual unveiling of the campaign on Tuesday would be moderated by popular broadcaster/compere, IK Osakioduwa, while Innocent 2Baba Idibia and Chike will serenade the guests.

Those expected to grace the occasion are the Chairman of NGX Group, Mr Abimbola Ogunbanjo; Minister of Finance, Budget and National Planning, Mrs Zainab Ahmed; the Director-General of the Securities and Exchange Commission, Mr Lamido Yuguda; and the Chairman of Dangote Group, Mr Aliko Dangote.

Others are the Chairman of Heirs Holdings, Mr Tony Elumelu; the President of Toronto Raptors, Mr Masai Ujiri; the Chief Executive Officer (CEO) of the NGX Limited, Mr Temi Popoola; and the CEO of NGX RegCo, Ms Tinuade Awe.

Also, participants who wish to attend the virtual launch of the campaign can register via https://ngxgroup.com/the-stock-africa-is-made-of.

Speaking ahead of the programme, the CEO of NGX Group, Mr Oscar Onyema, disclosed that, “The Stock Africa is Made of is designed to reinforce the message that we are fully equipped and better positioned to champion the development of new and improved experiences for the benefit of domestic, regional and foreign stakeholders.”

“Built around the new corporate identity, the campaign emphasises the vibrancy and dynamism of NGX Group and its subsidiaries.

“It provides stakeholders with an immersive experience through creative messaging and opportunities for direct engagement with the brand.

“Our goal is not only to celebrate this pivotal point in our journey but to also show our stakeholders that we are ready and able to explore new frontiers in our quest to be the partner and platform of choice for meeting their business, financial and investment objectives,” he added.

By Aduragbemi Omiyale

In the first quarter of its financial year ended June 30, 2026, Airtel Africa Plc showed resilience in the midst of challenging operating environments, churning out strong operating performance with accelerating customer base growth across all segments.

It was observed that the total customer base in Q1 2027 increased by 11.6 per cent to 189 million, with data customers rising by 15.5 per cent to 87.3 million.

In addition, data usage per customer continued its upward trajectory, rising from 7.8 GB to 10.6 GB per month over the past year, translating into a 56.3 per cent increase in data traffic across the network, underpinning a 10.3 per cent growth in constant currency data ARPU. Smartphone penetration was the key enabler of this increased traffic as penetration increased to 51.0 per cent as digital adoption of our services continues.

A look at the financial performance indicated that revenue in reported currency grew by 31.0 per cent to $1.85 billion, reflecting constant currency growth of 21.1 per cent and macroeconomic tailwinds supporting currency appreciation.

All segments continued to see double-digit constant currency revenue growth, with mobile services revenue growing by 19.1 per cent, and mobile money growing by 25.8 per cent.

Across mobile services, voice continued to see strong constant currency growth of 11.2 per cent and data revenue grew by 27.2 per cent.

In East Africa and Francophone Africa, constant currency revenues grew by 17.8 per cent and 18.0 per cent, respectively, while Nigerian revenues grew by 29.8 per cent, fully reflecting the lapping effect of the tariff adjustments which were implemented in the fourth quarter of 2025.

Constant currency EBITDA went up by 24.4 per cent, with reported currency EBITDA of $928 million growing by 36.6 per cent. The Q1’27 EBITDA margin of 50.1 per cent, an increase of 206bps year-on-year, continues to reflect the success of the company’s ongoing cost optimisation programme, despite the recent energy cost inflation arising from geopolitical developments.

The post-tax profit improved to $198 million from $156 million in the prior period, with higher profit after tax in the current period driven by elevated operating profit partially offset by derivative and foreign exchange losses of $6 million in the current period compared to $22 million derivative and foreign exchange gains in the prior period.

Furthermore, Profit after tax was impacted by the recognition of an exceptional finance cost of $37 million following an in-principle settlement reached during the quarter in respect of a commercial dispute in one of the group’s subsidiaries.

Commenting on the results, the chief executive of Airtel Africa, Mr Sunil Taldar, said, “We have started this year with another pleasing performance. Our continued focus on the customer experience translated into accelerating customer base growth across all business segments.

“As we continue to digitise our business, we are streamlining customer journeys, increasing digital adoption and harnessing data and AI to improve service delivery and support a strong, sustainable growth profile.”

By Aduragbemi Omiyale

One of the nation’s top brewers, Guinness Nigeria Plc, is paying an interim dividend of N7 per share to its shareholders for the period ended June 30, 2026.

The funds should, on August 10, 2026, hit the bank accounts of investors whose names appear in the Register of Members as of the close of business on Wednesday, July 29, 2026, a regulatory note from the organisation disclosed.

The firm has informed shareholders who have yet to complete the e-dividend registration to download the Registrar’s E-Dividend Mandate Activation Form, which is also available on its website, so as not to be left out of the cash reward for the first half of this year.

In the first six months of 2026, Guinness Nigeria grew its net profit by 53.33 per cent to N25.3 billion from N16.5 billion in the same period of 2025, amid improved top line and better management of administrative, marketing and distribution costs.

The revenue for the period under consideration rose to N265.0 billion from N237.0 billion, boosted by domestic sales of its products, which accounted for N260.9 billion compared with N237.0 billion a year earlier. The balance was from its export sales. This showed that over 98 per cent of the company’s earnings are from sales in Nigeria.

In the first half of the year, Guinness Nigeria improved its gross profit to N97.5 billion from N89.4 billion in the same period of 2025, as its finance income, arising from financial assets and others, stood at N1.2 billion compared with N110.7 million in H1 of 2026.

By Adedapo Adesanya

The federal government has reaffirmed its commitment to mobilising domestic capital to finance Nigeria’s long-term development, saying stronger local investment will be critical to accelerating economic transformation and attracting private sector participation.

The Minister of Finance and Coordinating Minister of the Economy, Mr Taiwo Oyedele, stated this while speaking at the 6th Annual General Assembly of the Association of Nigerian Development Finance Institutions (ANDFI) in Abuja on Thursday.

The Minister’s remarks were contained in a statement on Friday, July 24, by his Senior Special Assistant on Communications and Press Secretary, Mrs Maryann Duke.

Addressing the conference with the theme, Unlocking Domestic Capital for Development Financing, Mr Oyedele said Nigeria must harness its domestic financial resources and strengthen institutions that can channel capital into productive sectors of the economy.

He noted that despite increasingly difficult global financing conditions, the country possesses substantial domestic savings, institutional assets and private capital that can be leveraged to fund infrastructure, industrialisation, agriculture, housing, innovation and other critical sectors.

According to the minister, domestic capital should not be viewed as an alternative to foreign investment but as the foundation for attracting sustainable international investment.

“Our focus is to build an economy where confidence leads capital. By strengthening macroeconomic stability, deepening our financial markets and empowering development finance institutions to catalyse private investment, we are unlocking Nigeria’s enormous domestic potential to finance inclusive and sustainable growth,” Mr Oyedele said.

He said the federal government’s ongoing economic reforms under the Renewed Hope Agenda are beginning to deliver positive outcomes, including improved investor confidence, stronger external reserves, enhanced revenue generation and renewed international confidence in Nigeria’s economy.

The Minister identified five priority areas for unlocking domestic capital, including expanding investment opportunities for households, deepening institutional capital through pension and insurance assets, strengthening credit enhancement mechanisms, broadening local currency financing through the capital market, and building stronger development finance institutions capable of attracting larger volumes of private investment.

Mr Oyedele also called on development finance institutions to move beyond conventional lending by helping to structure bankable projects, reduce investment risks, support policy reforms and create financing ecosystems that encourage greater private sector participation.

He reaffirmed the Federal Government’s commitment to working with development finance institutions, financial regulators, investors and development partners to develop a financing framework that will support businesses, create jobs, accelerate industrialisation and promote inclusive economic growth across the country.