Economy

Nigeria: Moody’s Predicts 2.5% GDP Growth in 2017, 4% in 2018

**Affirms Country’s B1 Rating With Stable Outlook

By Modupe Gbadeyanka

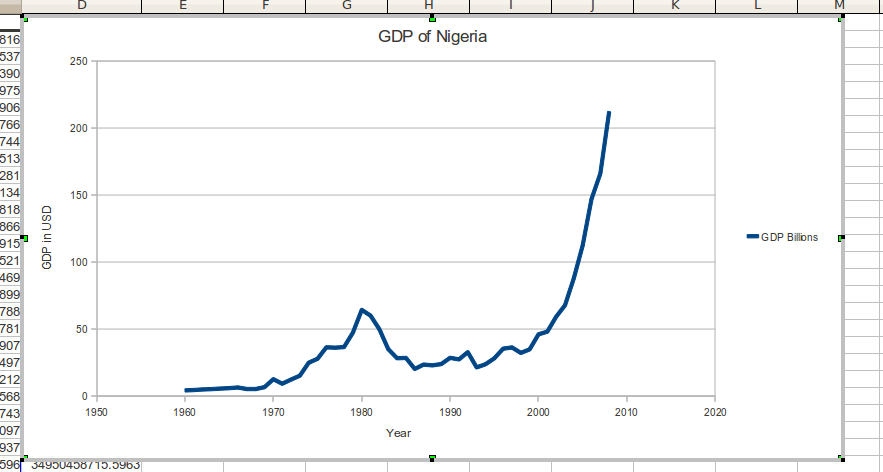

Moody’s Investors Service on Friday affirmed the B1 long-term issuer rating of the government of Nigeria with a stable outlook just as it forecasts that real GDP growth will rise to 2.5 percent in 2017 and accelerate further in 2018 to 4 percent.

The global rating firm disclosed that the key drivers for these were the medium term growth prospects remain robust despite the current challenging environment, with the rebound in oil production helping to rebalance the economy over the next two years; and the government’s balance sheet, which it said remains strong relative to its peers, resilient to the contractionary environment and temporarily elevated interest payments while the authorities pursue their efforts to grow non-oil taxes.

The long-term local-currency bond and deposit ceilings remain unchanged at Ba1. The long-term foreign-currency bond and deposit ceilings remain unchanged at Ba3 and B2, respectively.

Moody’s said it expects Nigeria’s medium term growth to remain robust, driven by the recovery in oil output and also over the near term, it expects Nigeria’s economic growth and US dollar earnings to improve in 2017, supported by a recovery in oil production.

According to Moody’s, after an estimated -1.5 percent real GDP growth in 2016, it forecasts real GDP growth to rise to 2.5% in 2017 and accelerate further in 2018 to 4%. A rebound in oil production to two million barrels per day (mbpd) will, if sustained, enhance economic growth and support the US dollar supply in the economy.

It noted that Nigeria has made significant gains in terms of governance and transparency in the oil sector. Improved availability of data, progress in restructuring the Nigerian National Petroleum Company (NNPC), rising effectiveness of operations at the refineries and a readiness to tackle difficult issues with partners (such as funding issues at the Joint Ventures) speak to a material improvement in the operating environment. The Petroleum Investment Bill (PIB bill), which had been blocked for 8 years in parliament, has been reactivated with a portion of the law drafted and passed by the Senate. Moreover, militant activity in the Niger Delta is set to wane following the resumption of payments from the government, though it will remain a threat to the recovery of the economy.

Moody’s further said the economy is also likely to benefit from the more timely implementation of the 2017 budget than its predecessor and in particular from the increase in capital spending on infrastructure which that will allow.

It also said the scarcity of Dollars, worsened by the soft capital controls imposed by the Central Bank of Nigeria (CBN), is likely to continue to negatively affect important sectors of the economy especially in services and manufacturing sectors.

“We do not expect the current policy mix to significantly change over the short term but a gradual easing of restrictions is possible as foreign currency receipts improve with rising oil production,” the firm said on Friday in a statement obtained by Business Post.

In 2017 and 2018, we expect Nigeria’s balance of payments to move back into surplus, supported by government external borrowings and a falling current account deficit. The latter is quickly reducing, supported by falling imports and increased oil production.

Depreciation of the naira, soft capital controls and current dollar scarcity have been relatively effective at constraining imports. We expect foreign exchange reserves to grow modestly in 2017. While improved foreign investor sentiment should support the rebalancing of the economy over the medium term, with the return of portfolio investors improving dollar liquidity in the country, the continued existence of a parallel, unofficial foreign exchange market is likely to act as a strong deterrent over the near term.

RESILIENT GOVERNMENT BALANCE SHEET STRONGER THAN PEERS’ DESPITE TURBULENCE

Moody’s says it expects the medium-term impact of the oil price shock on Nigeria’s government balance sheet to be contained, and recent erosion of debt affordability to be reversed.

The effect of the recent downturn on the government’s budget sheet has been contained as the authorities have been able to offset the shortfall in revenue with large cuts in capital expenditure. As a result, Moody’s forecasts a budget deficit of 3 percent of GDP in 2016, comprised of a 2 percent of GDP federal government budget deficit and around 1% of arrears split between federal, state and municipality levels of government, it explained.

Moody’s forecasts the federal government deficit to remain around 2% of GDP in 2017 and 2018, with large capital expenditure outlays resuming as the government’s cash flow situation improves. Based on these underlying projections, Nigeria’s balance sheet will continue to compare favourably with peers’, with government debt remaining well below 20% of GDP over the coming years against 55% median for B1-rated peers.

By end-2016, Moody’s estimates the government debt stock will be comprised of 85% domestic borrowing and 15% external debt, resulting in a manageable external debt profile. Government external debt amounts to just 2.9% of GDP, with interest payments set to remain low, at around $330 million dollars per annum. Domestic debt has increased significantly in recent years, reaching its current level of NGN10 trillion. Around 30% of this debt is comprised of costly T-bills, which have increased refinancing risk and interest rate exposure. However, Moody’s expects the ratio of interest payments to government revenues to peak at 20% for general government, and close to 40% of revenues for federal government in 2017.

Although debt service costs are high, Nigeria’s domestic capital market is sufficiently developed to accommodate the yearly public sector borrowing requirements of around NGN5.5 trillion. This is another positive credit feature that distinguishes Nigeria from many similarly rated peers. The country’s banking sector is well-capitalised and liquid and the national pension fund still has additional capacity. Should banking sector liquidity decline, the Central Bank of Nigeria has tools at its disposal to support appetite for government securities, including lowering the cash reserve requirement ratio from its presently high level of 22.5%. However, appetite for government securities remains strong, with all instruments remain oversubscribed.

Moody’s expects the recent increase in debt service costs to prove temporary, as a result of i) the government’ initiatives to expand the non-oil revenue base, and ii) efforts to improve the structure of government debt.

Measures by the Federal Revenue Inland Service are expected to increase non-oil revenue to around NGN4 trillion in 2016 from NGN2.5 trillion in 2015. These include a tax amnesty on penalties and interest on tax liabilities due in 2013, 2014 and 2015. However, not all the initiatives have proven successful: the independent re-appropriation of revenues from the ministries departments and agencies (MDAs) has yielded disappointing results so far. Such outcomes highlight the considerable execution risks inherent in the transition to a less oil-dependent federal budget, and the implications for the government balance sheet should it not meet its objectives.

The government’s medium-term debt strategy should also help to lower the interest burden. The debt strategy is geared towards exchanging costly short-term debt with long-term concessional borrowing. Although a portion of future external borrowings are expected to be raised through the Eurobond markets, this is likely to be complemented with ongoing support from other multilateral institutions including the African Development Bank and the World Bank. The combined effect of these measures should help to bring interest payments/general government revenues down to 16.8% by 2018, from an estimated 19.8% in 2016.

RATIONALE FOR THE OUTLOOK AT STABLE

The stable outlook is driven by Moody’s view that the downside risks posed by the weakening of the country’s fiscal strength, and the external and economic pressures anticipated this year and next, are balanced by Nigeria’s strengths, which exceed those of sovereigns rated below B1. In 2016, Nigeria’s external vulnerability indicator of 31% will remain far below the expected B1 median of 51%, while its debt-to-GDP of 16.6% will remain far below the expected B1 median of 55%. Set against that, its expected debt servicing burden in terms of interest payments to revenue of 19% is more than double the B1 median of 9%. To a large extent, Moody’s believes that this reflects Nigeria’s underdeveloped public sector revenue base, a credit weakness that the administration is attempting to address.

WHAT COULD CHANGE THE RATING UP

Positive pressure on Nigeria’s issuer rating will be exerted upon: 1) successful implementation of structural reforms by the Buhari administration, in particular with respect to public resource management and the broadening of the revenue base; 2) strong improvement in institutional strength with respect to corruption, government effectiveness, and the rule of law; 3) the rebuilding of large financial buffers sufficient to shelter the economy against a prolonged period of oil price and production volatility.

WHAT COULD CHANGE THE RATING DOWN

Nigeria’s B1 issuer rating could be downgraded in the event of 1) a greater-than-anticipated deterioration in the government’s balance sheet or continued erosion of debt affordability, for example resulting from the failure to implement revenue reform; and 2) lower than expected medium term growth, for example as a result of delays in implementing key structural reforms, especially in the oil sector, or continued militancy in the Niger Delta, which undermine the level of oil production over the medium-term.

GDP per capita (PPP basis, US$): 6,184 (2015 Actual) (also known as Per Capita Income)

Real GDP growth (% change): -1.5% (2016 Estimate) (also known as GDP Growth)

Inflation Rate (CPI, % change Dec/Dec): 19% (2016 Estimate)

Gen. Gov. Financial Balance/GDP: -2.9% (2016 Estimate) (also known as Fiscal Balance)

Current Account Balance/GDP: -0.6% (2016 Estimate) (also known as External Balance)

External debt/GDP: 4.2% (2016 Estimate)

Level of economic development: Low level of economic resilience

Default history: No default events (on bonds or loans) have been recorded since 1983.

On 7 December 2016, a rating committee was called to discuss the ratings of the Government of Nigeria. The main points raised during the discussion were: The issuer’s economic fundamentals, including its economic strength, have not materially changed. The issuer’s fiscal or financial strength, including its debt profile, has not materially changed. The issuer’s susceptibility to event risks has not materially changed. Other views raised included: the issuer’s institutional strength/framework, have not materially changed. The issuer’s governance and/or management, have not materially changed.

The principal methodology used in these ratings was Sovereign Bond Ratings published in December 2015. Please see the Rating Methodologies page on www.moodys.com for a copy of this methodology.

The weighting of all rating factors is described in the methodology used in this credit rating action, if applicable.

By Aduragbemi Omiyale

The Stanbic IBTC Bank Nigeria Purchasing Managers’ Index (PMI) for the Nigerian private sector in July 2026 contracted to 52.5 points from 53.4 points in June 2026, a statement made available to Business Post has shown.

This occurred despite the business environment sustaining its growth last month, with an increase in new orders experienced, as inflationary pressures softened, and output and employment modestly rising.

The Head of Equity Research West Africa at Stanbic IBTC Bank, Mr Muyiwa Oni, said the PMI indicated that the private sector recorded its slowest since March 2026, as businesses also increased their input purchasing activity to keep up with current demand requirements and prepare for future workloads.

“Nigerian businesses reported improved customer demand in July while better pricing and new product launches also helped them to capture new orders arising from the increase in demand. These factors helped to keep the private sector activity in an expansionary territory, although this moderated when compared to June,” he was quoted as saying.

It was stated that while input costs increased at their slowest pace in five months, panellists reported higher costs for fuel and raw materials. Selling prices also softened in line with the picture for input costs in July.

Headline inflation eased slightly to 15.91 per cent y/y in June from 15.93 per cent y/y in May, snapping three consecutive months of price increases.

Although July inflation is likely to be higher m/m, it is expected to print lower, likely at 15.72 per cent y/y, primarily driven by favourable base effects from the corresponding period of last year, because there are no expectations of the magnitude of m/m inflation witnessed in July 2025 (1.99 per cent) to materialise this year.

“We retain our 2026 growth forecasts at 4.1 per cent as we see the oil sector growing by 3.45 per cent y/y in 2026, from 8.50 per cent y/y in 2025, while the non-oil sector is likely to grow by 4.11 per cent y/y, from 3.71 per cent y/y in 2025.

“The risks to our outlook include country-wide insecurity which may constrain food production, exchange rate pressures resurfacing, extreme-weather related conditions and higher fertiliser prices impacting crop yield, and a volatile global environment which may affect sentiment and constrain capital flows,” Mr Oni noted.

By Adedapo Adesanya

Sahara Upstream, a Nigeria-focused crude producer, has deployed a new 380,000-barrel tanker to boost exports from the OML 18 block as part of a wider push by domestic operators to invest in infrastructure and lift output and exports for Africa’s biggest oil producer.

The MT D Adesanya, which can hold more than 62,000 cubic metres of crude, will operate alongside the MT D Bayero, receiving crude from shuttle vessels at Bonny Anchorage, one of Nigeria’s main crude export hubs, before transferring it to the FSO Cawthorne storage facility.

Sahara said the tanker would help cut turnaround times, currently about 30 to 48 hours, and support a planned 50 per cent increase in exports from the block’s current level of about 950,000 barrels per month.

The block currently produces about 36,000 barrels per day, according to data from the Nigerian Upstream Petroleum Regulatory Commission (NUPRC), with Sahara targeting output of 60,000 barrels per day.

OML 18 is one of the Niger Delta’s oldest producing assets. It began production in 1970 and contains an estimated 1.5 billion barrels of oil equivalent in reserves.

Shell, Total and Eni sold their combined interests to Eroton in 2015 as part of a broader shift toward domestic ownership in Nigeria’s upstream sector.

This development comes as Sahara Upstream is deepening its exploration and production footprint through Asharami Energy Limited (AEL), its upstream E&P business, which says it is targeting 350,000 barrels of oil per day by 2030 through its subsidiary, Enageed Resources Limited (ERL).

The growth target comes as AEL also marks a major safety milestone, achieving 6 million Lost Time Injury (LTI)-free man-hours in its OML-148 operations — reinforcing the company’s commitment to operational excellence and safety leadership.

According to Asharami Energy, the milestone reflects its ability to execute complex operations safely, in line with Sahara’s Beyond XXX vision, which builds on the group’s 30-year legacy of responsible enterprise while marking its next chapter of impact, innovation, and sustainable growth.

The developments position Sahara Upstream and its subsidiaries among the domestic operators driving increased investment in Nigeria’s oil and gas infrastructure, as the group works to scale up production and exports for Africa’s biggest oil producer.

By Aduragbemi Omiyale

One of the leading energy firms in Nigeria, Aradel Holdings Plc, has expressed its desire to optimise its enlarged portfolio and improve operational efficiency in the second half of 2026.

The company is planning to build on the success it recorded in the first half of the year, where it grew its revenue by 577 per cent to N2.5 trillion from N368.1 billion in H1 2025.

The significant rise in earnings was driven by higher production volumes together with stronger realised crude oil and gas prices, with the average at $90.4/bbl and $2.08/mmscf, respectively.

In the period under review, the Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA) increased by 688 per cent to N1.4 trillion from N176.4 billion in the corresponding period of last year, while the operating profit surged by 789 per cent to N1.1 trillion from N118.6 billion due to higher revenue and crude handling income at N149.8 billion, partly offset by underlift cost and general and administrative costs.

The net cash generated from operations was N975.6 billion between January and June 2026 versus N140.8 billion in the same period of 2025, reflecting the cash generation of the enlarged organisation.

The net debt contracted by 70 per cent on a year-to-date basis to N46.5 billion from N475.1 billion as of December 31, 2025.

Aradel, in the period under consideration, improved its post-tax profit by 30 per cent to N191.0 billion from N146.4 billion, a development that impressed its chief executive, Mr Adegbite Falade, who said, “A firmer price environment supported performance, generating net cash from operating activities of N975.6 billion and a closing cash balance of N1.7 trillion.”

“Our enlarged portfolio provides more opportunities to generate stronger cash flow and returns for shareholders and unlocking that potential is our main focus.

“We reaffirm our full year production guidance of 110 – 140 kboepd and remain committed to operating responsibly in a changing energy landscape and to delivering lasting value for our stakeholders,” he stated.