Economy

Tinubu’s Policies Restoring Investor Confidence in Nigeria’s Economy—Dangote

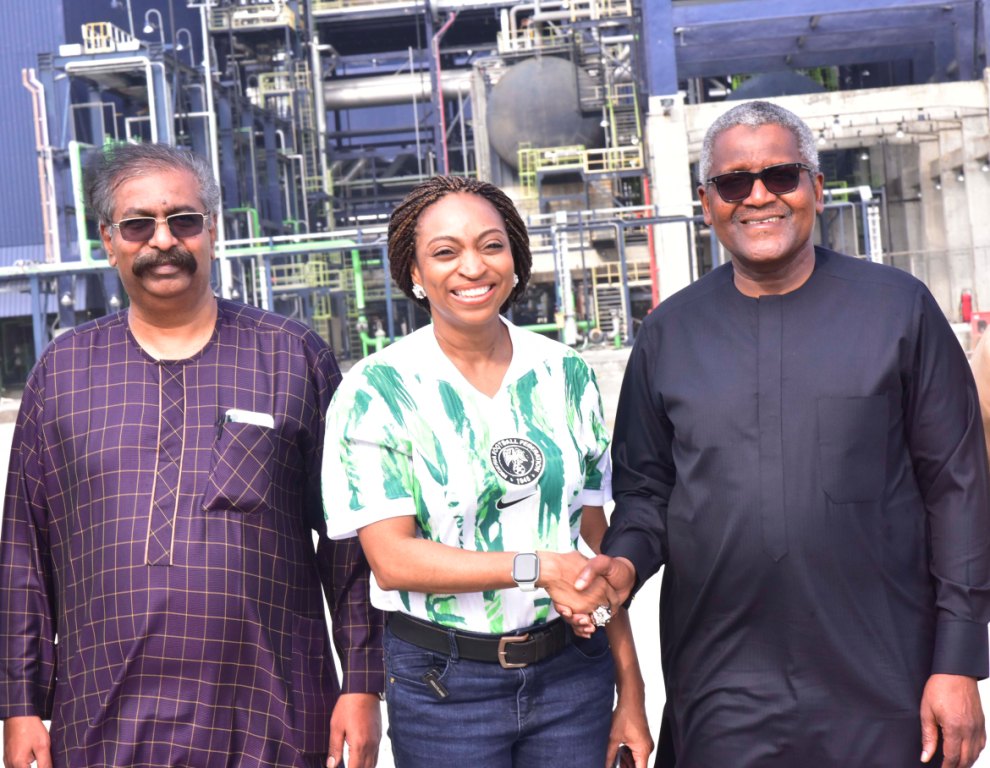

By Modupe Gbadeyanka

President Bola Tinubu has been praised for restoring investor confidence in the economy of Nigeria through his economic policies like the new tax laws, foreign exchange (FX) liberalisation, fuel subsidy removal and others.

The president of Dangote Group, Mr Aliko Dangote, said over the weekend that the Naira-for-Crude initiative and the Nigeria First policy were also bold and transformative steps of the current administration capable of revitalising the economy faster than expected.

“I believe we must sincerely thank His Excellency, President Bola Ahmed Tinubu, for ensuring that there have been improvements in the supply of crude oil. His insistence that all crude oil transactions be conducted in naira has been particularly commendable.

“For us to effectively meet market demand—which we can do—it is essential that crude is priced and purchased in our local currency,” Mr Dangote said when he received the Minister of Industry, Trade and Investment, Ms Jumoke Oduwole, at the $20 billion Dangote Petroleum Refinery and Petrochemicals and Dangote Fertiliser Limited in Lagos.

The businessman also disclosed that the reforms have brought a measure of stability to the naira-to-dollar exchange rate, expressing optimism that the local currency will continue to strengthen in the coming weeks as the effects of the reforms become more visible.

According to him, the improved market predictability has helped investors make sound business decisions and restored confidence in the investment climate.

“We are also beginning to see some stability in the naira-to-dollar exchange rate, which has had a positive impact. There is now less fluctuation, and this has brought a degree of predictability to the market

“For those of us in the business sector, this is a welcome development, as it allows us to plan more effectively. Looking ahead, as market conditions continue to improve, we can expect to see a more favourable exchange rate,” he said

The leading industrialist also commended the federal government for establishing a One-Stop Shop (OSS) initiative to improve coordination among regulatory and security agencies, thereby facilitating smoother operations under the Naira-for-Crude programme.

He emphasized that the OSS had significantly reduced bottlenecks and enabled the real-time resolution of issues, in line with President Tinubu’s directive.

“At present, we are not experiencing any significant issues with loading. All the relevant agencies have been brought together under one roof, including the Navy, NIMASA, NPA, and others. This coordination has greatly improved efficiency. Whenever issues arise, they are promptly addressed through the leadership of the Chairman of the Technical Committee, Mr Zack Adedeji, who is doing an excellent job,” he stated.

The business magnate further disclosed that the refinery is set to launch a new initiative involving the deployment of 4,000 CNG (Compressed Natural Gas) tankers to distribute petroleum products more efficiently and in an environmentally friendly manner. He explained that the move would reduce logistics costs and ensure Nigerians receive products at more affordable prices, closer to their locations.

On her part, the Minister reaffirmed the government’s commitment to promoting domestic investment and addressing the challenges faced by local investors.

“We are here today as a result of President Bola Ahmed Tinubu’s clear focus on domestic investment. As you are aware, we held a Domestic Investment Summit on Monday—the first of its kind. Today, we are gathered at the invitation of Aliko Dangote, a leading investor who has committed an extraordinary amount of resources to Nigeria’s development,” she said.

The Minister hailed the refinery as a landmark project, noting that even governments shy away from initiatives of such scale. She said the administration is demonstrating real support for domestic investors by taking practical steps to reduce constraints and foster growth.

“He has taken on a project of such magnitude—one that even governments often hesitate to undertake. As an administration, we do not take this lightly. We are here to show our full support for him, both as a foremost domestic investor and as a prominent champion of African investment on the global stage.

“Our support is not limited to words; we are demonstrating our commitment through action. We are encouraging other domestic investors by recognising and backing those, like Alhaji Dangote, who put Nigeria first. This is not mere rhetoric—our time, attention, and effort are fully aligned with our priorities,” she said.

By Adedapo Adesanya

The NASD Over-the-Counter (OTC) Securities Exchange closed flat on Wednesday, August 5, as the market witnessed weaker trading activity with only two deals executed.

In the midweek session, the volume of securities exchanged by investors dropped 99.9 per cent to 802 units from the 1.6 million units recorded on Tuesday. The value of securities further decreased by 99.6 per cent to N208,240 from the preceding session’s N47.6 million, and the number of deals significantly went down by 93.9 per cent to two deals from the 33 deals recorded a day earlier.

Great Nigeria Insurance (GNI) Plc remained the most traded stock by value on a year-to-date basis, with 3.4 billion units worth N8.4 billion, followed by Infrastructure Credit Guarantee (Infracredit) Plc with 2.3 billion units sold for N6.5 billion, and Central Securities Clearing System (CSCS) Plc with 76.9 million units transacted for N5.5 billion.

GNI Plc was also the most active stock by volume on a year-to-date basis, with 3.4 billion units exchanged for N8.4 billion, followed by Infracredit Plc with 2.3 billion units traded for N6.5 billion, and Resourcery Plc with 1.1 billion units valued at N415.7 million.

There were no price gainers or losers yesterday.

As a result, the market capitalisation stood unmoving at N2.739 trillion, while the NASD Security Index (NSI) remained unchanged at 4,563.96 points.

By Adedapo Adesanya

The Naira slid against the US Dollar by N2.28 or 0.17 per cent in the Nigerian Autonomous Foreign Exchange Market (NAFEX) on Wednesday, August 5, to N1,363.85/$1 from N1,362.55/$1.

The local currency also declined against the Pound Sterling in the official market during the session by N5.97 to close at N1,837.38/£1 compared with Tuesday’s closing rate of N1,831.41/£1, and against the Euro, it crashed by N6.54 to quote at N1,575.25/€1 versus the preceding session’s N1,568.71/€1.

But at the black market, the Nigerian Naira traded flat against the greenback yesterday at N1,400/$1, and also remained unchanged at the GTBank FX desk at N1,373/$1.

The Central Bank of Nigeria (CBN) says rates have narrowed to below two per cent, while the country’s external reserves have risen above $52.5 billion, reflecting the impact of its ongoing monetary and foreign exchange reforms.

CBN Governor Yemi Cardoso, represented by the Acting Director of Corporate Communications and Investor Relations, Mrs Hakama Sidi-Ali, disclosed this on Tuesday during the CBN Fair in Gombe. He noted that reforms introduced since 2023 had significantly reduced the disparity between the official FX market and the parallel market.

“The Naira continues to strengthen, with the spread between official and Bureau de Change rates now below two per cent,” he said, adding that reserves at $52.5 billion were supported by sustained inflows and renewed investor confidence in the economy.

Interbank FX transactions slid as weaker market activities dropped total Dollar volume exchanged to $75.35 million, a 51.8 per cent decline from $156.23 million in turnover quoted at the previous close.

The deals at the NFEM window also fell as data from the central bank put Wednesday’s quote at 82 from 139.

In the cryptocurrency market, major were down as global risk sentiment softened as a key world equity index slipped and chipmakers fell.

The MSCI All Country World Index snapped a five-day run to fall 0.2 per cent as chipmakers retreated on both sides of the Pacific. South Korea’s Kospi, a bellwether for the AI trade, dropped 4.4 per cent.

Ripple (XRP) depleted by 1.7 per cent to $1.05, Binance Coin (BNB) decreased by 1.0 per cent to $594.87, Cardano (ADA) depreciated by 0.9 per cent to $0.1884, TRON (TRX) shrank by 0.2 per cent to $0.3261, Solana (SOL) crumbled by 0.1 per cent to $74.00, and Dogecoin (DOGE) went down by 0.1 per cent to $0.0697.

On the flip side, Ethereum (ETH) gained 2.3 per cent to trade at $1,911.41, and Bitcoin (BTC) rose by 0.8 per cent to $64,759.28, while the US Dollar Tether (USDT) and the US Dollar Coin (USDC) remained unchanged at $1.00 apiece.

By Dipo Olowookere

The domestic stock exchange rebounded by 0.05 per cent on Wednesday on the back of renewed bargain-hunting by investors, though the level of activity waned.

After bleeding for a few days, the Nigerian Exchange (NGX) Limited heaved a sigh of relief yesterday, as the All-Share Index (ASI) gained 109.41 points to close at 244,912.24 points compared with the previous day’s 244,802.83 points, and the market capitalisation garnered N71 billion to settle at N158.087 trillion versus Tuesday’s N158.016 trillion.

Business Post reports that despite the rebound recorded by Customs Street at midweek, the market breadth index remained negative, as there were 20 price advancers and 29 price decliners, implying bearish investor sentiment.

Linkage Assurance appreciated by 9.94 per cent to N1.77, AVA Capital rose by 9.55 per cent to N10.90, Fortis Global Insurance advanced by 7.69 per cent to N2.80, McNichols gained 7.34 per cent to finish at N5.85, and Coronation Insurance surged by 5.51 per cent to N2.49.

Conversely, Honeywell Flour depreciated by 9.94 per cent to N16.30, PZ Cussons gave up 9.94 per cent to trade at N74.75, Zichis crashed by 9.74 per cent to N20.76, Learn Africa slipped by 9.62 per cent to N9.40, and Neimeth tumbled by 8.33 per cent to N8.25.

The busiest equity was FCMB, with a turnover of 369.2 million units valued at N4.1 billion. Chams transacted 46.7 million units worth N201.8 million, First Holdco transacted 43.5 million units for N5.7 billion, Access Holdings sold 29.8 million units worth N778.0 million, and Linkage Assurance exchanged 19.6 million units valued at N33.5 million.

At the close of transactions, market participants bought and sold 824.1 million units worth N25.5 billion in 48,114 deals, in contrast to the 1.6 billion units sold for N28.7 billion in 54,160 deals a day earlier, showing a shortfall in the trading volume, value, and number of deals by 48.49 per cent, 11.15 per cent, and 11.16 per cent, respectively.