Economy

Tropical Storm Zeta Pushes Oil Prices Higher

By Adedapo Adesanya

Oil futures finished higher on Tuesday as another major storm cut energy output in the Gulf of Mexico even as the market continued to feel the impact on worsening demand from the ongoing rise globally in COVID-19 cases.

As a result, the price of the Brent crude oil went up by 1.78 per cent or 72 cents to $41.18 per barrel while the United States’ futures, West Texas Intermediate (WTI) crude appreciated by 2.39 per cent or 92 cents to $39.47 a barrel.

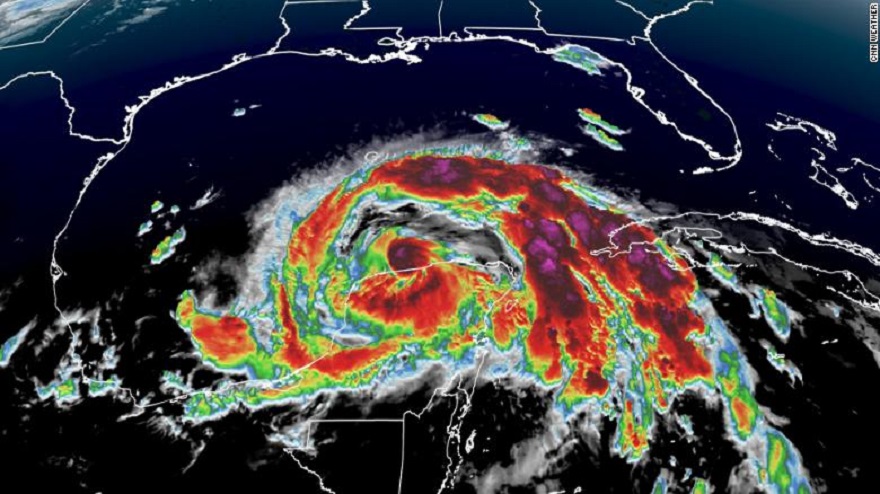

Tropical Storm Zeta in the United States has forced evacuations of offshore production platforms in the Gulf of Mexico.

This hurricane season has caused shutdowns which have put significant pressure on US oil production and pushed it to 9.9 million barrels per day.

The additional support from Tropical Storm Zeta comes at a time when the market is worried about the impact of the second wave of coronavirus.

Zeta is forecast to approach the northern Gulf Coast on Wednesday and make landfall late Wednesday or Wednesday night.

The disruption from the storm will put pressure on oil production in the country as it will keep the total production levels way below the recent 11 million barrels per day in the near term.

The storm-induced bump in prices may be short-lived, however, with demand expected to weaken anew with coronavirus cases rising.

In the latest round of development, Europe’s daily coronavirus related deaths rose by nearly 40 per cent compared with the previous week, the World Health Organization (WHO) said on Tuesday.

Russia reported a daily record of 320 deaths, pushing the tally to 26,589. There has been a sharp increase in Italy too, with 221 fatalities announced in the past 24 hours. The total number of fatalities in Austria went above 1,000 on Tuesday.

Russia has the world’s fourth-highest number of COVID-19 cases after the US, India and Brazil. It recorded another 16,550 infections on Tuesday alone and authorities have now made the wearing of face masks compulsory in all crowded places.

And in Belgium, doctors have been asked to keep working, even if they have the virus because the health system is in danger of being overwhelmed.

With the demand hit expected from this, the market is also facing fire from developments in Libya. The North African country’s production should rebound to 1 million barrels per day in the coming weeks.

This will further complicate efforts by other members and allies of the Organization of the Petroleum Exporting Countries (OPEC) to restrict output.

Business Post had been reported that the alliance known as OPEC+, is planning to increase production by 2 million barrels a day from January after record output cuts this year. That would cut overall reductions to 5.8 million barrels per day, still an enormous amount by the standards of major oil producers, but it may not be enough to offset weak demand.

The latest weekly US oil inventory figures are due on Wednesday and are expected to show rising supplies which will further add to the bearish factors.

By Adedapo Adesanya

The Senate has passed a bill to repeal and re-enact the law establishing the National Insurance Commission (NAICOM), paving the way for the regulatory agency to be renamed the Insurance Regulatory Commission (IRC).

The legislation, titled the Insurance Regulatory Commission (Establishment) Bill, 2026, was passed after the Senate considered and adopted the report of its committee on banking, insurance and other financial institutions.

The Chairman of the committee, Mr Adetokunbo Abiru, the senator representing Lagos East, who presented the report, stated that the proposed legislation was necessary because the existing National Insurance Commission Act of 1997 had become outdated and no longer reflected the realities of Nigeria’s evolving insurance industry or global regulatory standards.

According to the Senate, the decision to change the Commission’s name was informed by the need to eliminate confusion associated with the existing designation and to better reflect the institution’s regulatory mandate within Nigeria’s insurance industry.

The bill also provides legal protection for the commission and its officers against adverse claims arising from the lawful execution of their statutory duties.

However, he noted that the commission’s enabling law had become obsolete, exposing significant regulatory gaps that required urgent legislative intervention.

‘The current National Insurance Commission Act 1997 is outdated and does not adequately address the emerging economic growth, needs and development of the insurance business,” the lawmaker said.

He explained that the new legislation seeks to strengthen the independence of the commission by empowering it to make regulatory decisions without undue influence in the country’s insurance sector.

According to him, the bill also enhances the commission’s authority to exchange information and collaborate with domestic and international regulatory bodies, issue regulations, guidelines, standards and directives on insurance-related matters, and intervene more effectively in financially distressed insurance companies to protect policyholders and preserve financial stability.

This marks yet another move to strengthen the country’s insurance sector following the enactment of the Nigerian Insurance Industry Reform Act (NIIRA) of 2025 and the industry-wide recapitalisation exercise, which will wrap up by July 31.

By Adedapo Adesanya

About 143 companies that successfully passed the technical and prequalification stages of the Nigerian Upstream Petroleum Regulatory Commission’s (NUPRC) 2025 Licensing Round will, today, compete for 50 oil and gas blocks at the commercial bid conference in Abuja, the final stage in the allocation process for the assets.

The commission said only the prequalified companies have been invited to attend the event, which will hold at the Conference Centre of the Transcorp Hilton Hotel, Abuja, stressing that participation is strictly by invitation.

The commercial bid conference will determine the successful bidders for oil and gas assets located across Nigeria’s producing and frontier basins.

The 50 blocks comprise 16 onshore blocks and 18 shallow water blocks in the Niger Delta, one deep offshore block, three onshore blocks in the Benin Basin, four in the Anambra Basin, four in the Chad Basin, and four in the Benue Trough.

According to the commission, the winning bids will be determined through a transparent evaluation process based on clearly defined commercial parameters. These include the signature bonus offered by bidders, the proposed work programme commitment and the level of performance security provided. The final selection will be based on a weighted technical and commercial score.

The licensing round is being conducted under the provisions of the Petroleum Industry Act (PIA) 2021, which requires a transparent and competitive process for the award of petroleum assets.

NUPRC had announced the commencement of the 2025 Licensing Round on November 11, 2025, before opening the online bid portal on December 1, 2025, to enable interested companies to register and participate in the exercise.

To ensure prospective investors fully understood the requirements, the commission organised a pre-bid conference on January 14, 2026, at Eko Hotels and Suites, Lagos. The event provided detailed explanations on the licensing guidelines and bidding procedures to registered participants and other stakeholders.

Registration and submission of prequalification documents closed on February 27, 2026, while the prequalification evaluation was completed on March 16, 2026.

NUPRC disclosed that 286 companies initially submitted applications for prequalification.

Following the evaluation process, 196 companies were cleared to participate in the technical and commercial bid stages.

The prequalified 143 companies eventually submitted a total of 200 bids for the available oil and gas blocks. These companies are now set to compete at the commercial bid conference, where the financial offers will be opened and evaluated to determine the eventual winners.

The licensing round is expected to attract fresh investment into Nigeria’s upstream petroleum sector, boost exploration activities across both producing and frontier basins, increase crude oil and gas reserves, and support the country’s drive to grow production and government revenue.

It also underscores the regulator’s commitment to implementing a transparent, competitive and investor-friendly licensing regime under the Petroleum Industry Act.

By Adedapo Adesanya

The Monetary Policy Committee (MPC) of the Central Bank of Nigeria (CBN) has retained all key monetary policy parameters following the conclusion of its two-day meeting on July 21, 2026, on Tuesday, maintaining its tight monetary policy stance to curb inflation and support macroeconomic stability.

According to the Governor of the apex bank, Mr Yemi Cardoso, who chaired the committee, the Monetary Policy Rate (MPR), which serves as the benchmark interest rate, remains at 26.50 per cent. The MPC also retained the asymmetric corridor around the MPR at +50 basis points and -450 basis points.

In addition, the Cash Reserve Ratio (CRR) for commercial banks was left unchanged at 45.00 per cent, while the CRR for merchant banks remains at 16.00 per cent. The committee also retained the CRR on non-Treasury Single Account (Non-TSA) public sector deposits at 75.00 per cent, with the liquidity ratio at 30.00 per cent.

The decision reflects the apex bank’s continued commitment to containing inflationary pressures through a restrictive monetary policy while safeguarding the resilience of Nigeria’s financial system amid ongoing macroeconomic adjustments.

By keeping all policy tools unchanged, the MPC signalled its intention to continue managing excess liquidity in the banking sector and maintain stability in financial markets.

The move is also expected to provide greater policy certainty for investors and businesses monitoring the country’s monetary policy direction.

The latest decision also means borrowing costs are likely to remain elevated in the near term as the central bank continues to prioritise price stability over monetary easing.

Analysts had expected the CBN committee to retain the rate after Nigeria’s headline inflation came in at 15.91 per cent as of June 2026, marking a slight decline from 15.93 per cent in May.

However, even as overall price growth has moderated significantly compared to previous periods, food inflation remains a persistent challenge, accelerating to 17.52 per cent in June.