Feature/OPED

5 Strategy Ideas for Your Company’s Finances

Effective financial management is essential for the long-term success of your company. Implementing wise financial methods will assist you in preserving stability, enhancing profitability, and achieving your growth goals, whether you run a startup or an existing business. This post will examine five strategies to improve your company’s finances and promote long-term success.

-

Diversify Your Revenue Streams

Your company can be susceptible to the ups and downs of the market and the economy if it depends on a single source of revenue. It is necessary to diversify your revenue streams if you want to reduce the impact of this risk. Investigate the possibility of expanding your product or service offerings in ways consistent with your core skills and attractive to the customers you want to attract. You will be less reliant on a single source of revenue if you diversify your portfolio and use the different consumer groups and marketplaces you get access to as a result.

For instance, a company developing software could diversify its revenue streams by providing complementary consulting services or developing bespoke software solutions for specialized industries. Both of these options are examples of niche markets. This strategy enables the company to capitalize on its expertise while also producing different income streams.

-

Implement Effective Cash Flow Management

It is essential for the long-term financial health of any company to keep a positive cash flow at all times. By practicing effective strategies for managing cash flow, such as obtaining financial assistance like the edg grant Singapore, you can ensure that your company has sufficient liquidity to pay its obligations, seize chances for expansion, and weather unexpected problems.

Managing your cash flow properly can be accomplished, in part, by optimizing the terms under which you get paid. Negotiate favourable conditions with suppliers and vendors, such as extended payment periods or discounts for early payments, and then take advantage of those arrangements. In addition, make sure you keep a tight eye on your accounts receivable and swiftly follow up with any past-due payments. You can help reduce the number of late payments and enhance your cash flows by implementing efficient systems for billing and collecting payments.

-

Invest in Technology and Automation

Embracing technology and automation is one of the most effective ways to drastically improve your financial procedures, enhance efficiency, and cut expenses. Investing in sophisticated accounting software, financial management systems, and customer relationship management (CRM) platforms can assist you in automating tedious operations, enhancing accuracy, and gaining useful insights into your company’s financial health.

For instance, implementing an integrated financial management system to centralize your accounting, budgeting, and forecasting procedures. It gives you real-time visibility into your financial data, allowing you to make educated decisions and improve resource allocation. You can save time and divert your attention to more strategic activities if you automate repetitive chores such as expense monitoring, invoicing, and financial reporting.

-

Monitor Key Financial Metrics

It is vital to consistently monitor key financial parameters to effectively manage your company’s finances. These metrics provide vital insights into the functioning of your organization and can assist you in identifying areas of improvement and making decisions based on accurate information.

The return on investment (ROI), the cash conversion cycle, the gross profit margin, and the net profit margin are some of the most important financial measures to monitor. You will be able to determine the profitability of your products and services, the overall financial health of your company, and prospects for both cost reduction and revenue expansion by analyzing these variables.

-

Seek Professional Financial Advice

Small and medium-sized businesses (SMEs) can find it difficult to understand the financial landscape. If you want to make smart choices regarding your finances, getting professional financial counsel can give you the experienced help and insights you need.

You can get the services of a professional financial advisor or a reputable service provider like Certinia to analyze your current financial strategy, pinpoint areas in which your company could benefit from enhancements, and create individualized plans of action.

Service providers can streamline your finances and operations and assist you in analyzing your financial statements, optimizing your tax planning, finding funding options, and developing a long-term financial roadmap consistent with your business goals. While a financial advisor can offer specialist advice on financial planning and forecasts, risk management, and tax planning.

Conclusion

For your organization to succeed and last, it is essential to implement sound financial practices. You can improve your financial situation and promote growth by diversifying your sources of income, maximizing your cash flow, utilizing technology and automation, keeping an eye on important financial indicators, and getting professional assistance. Remember that staying ahead in the always-changing business environment requires adaptability and ongoing progress.

Feature/OPED

The Role of the Stock Market in Nation Building: Imperatives for an Inclusive Capital Economy

By Adedapo Adesanya

Nigeria’s stock market has crossed a milestone that demands attention. With total market capitalisation reaching N151.327 trillion as at June 2026, the Nigerian Exchange Limited (NGX) has not only consolidated its position as Africa’s second-largest bourse, but it has also demonstrated something more consequential: that domestic capital, when properly mobilised, is a credible engine of national development.

Nation building is rarely a singular act. It accumulates through institutions that function, capital that circulates, and citizens who believe the system works for them. Few institutions make that case as visibly as a thriving stock exchange. The market is no longer just a barometer of investor sentiment. It is an active participant in Nigeria’s development.

The quality of any capital market ultimately reflects the quality of the companies it hosts. Markets create national wealth most effectively when they provide long-term capital to productive enterprises that expand industrial capacity, create jobs, deepen local supply chains and generate enduring shareholder value.

Earlier in the year, President Bola Tinubu had commended the NGX Group, corporate Nigeria, market operators and investors for propelling NGX past the historic N100trn market capitalisation mark, describing the milestone as a strong indicator of renewed investor confidence and economic recovery.

He said: “The Nigerian capital market stands at the heart of our ambition to build a one-trillion-dollar economy. It is the engine through which long-term finance must be mobilised to power critical sectors – from infrastructure to housing, technology, energy and industrial growth.”

Nigeria has increasingly demonstrated this through home-grown corporate champions such as the Dangote Group, whose decades-long investments across strategic sectors illustrate how patient enterprise-building and capital market development can reinforce one another. Strong companies strengthen strong markets, and strong markets, in turn, provide the capital needed to build even stronger companies.

But numbers, however impressive, are only part of the story. The more compelling narrative lies in who is now participating and how. The explosion in retail participation over the past two years is inseparable from digital infrastructure.

Data by the Central Securities Clearing System (CSCS) shows 151,749 new brokerage accounts were opened in just the first five months of 2025. Between 2019 and November 2025, over 2.1 million new retail investment accounts were established, the strongest growth in seven years. This is not incidental. It is the direct result of deliberate technological positioning by market operators and regulators, and one of the more underappreciated contributions to national economic inclusion, the companies on the stock market.

Nigeria’s investing demographic is shifting, and the market must shift with it. A largely young, mobile-first population does not respond to traditional channels. They discover financial products on social media, transact via apps, and make decisions based on peer influence as much as professional advice. The 56 per cent year-on-year increase in retail equity investment to N981 billion in the first seven months of 2025 reflects this generational pivot.

Yet gaps remain. Women, smallholder entrepreneurs and low-income earners across tier-2 and tier-3 cities are underrepresented. Instruments like the Federal Government Savings Bond, accessible from as little as N5,000, demonstrate that appetite exists beyond the traditional investor class. The challenge now is sustained financial literacy, culturally relevant messaging, and last-mile digital infrastructure that meets these segments where they are. Broadening that base is not just good market development; it is nation-building in its most practical form.

Sustaining confidence in the capital market requires a functioning compact between four critical actors. Regulators must maintain the credibility they have worked on to rebuild. Reforms, including foreign exchange unification, banking recapitalisation, and NGX demutualisation, have restored institutional trust. That momentum cannot be squandered.

Financial institutions must do more than offer products; they must offer pathways. Education, simplified onboarding, and genuinely accessible advisory services are not optional add-ons. They are the infrastructure of a participatory economy.

Listed companies have a responsibility that extends beyond quarterly earnings. They must consistently demonstrate transparency, sound corporate governance, operational excellence and long-term value creation. Companies that invest patiently in productive assets while rewarding shareholders over time help deepen confidence in the market and encourage wider public participation. The experience of leading Nigerian enterprises, including companies within the Dangote Group, shows that sustained investment in the real economy can simultaneously create industrial capacity, support national development and deliver enduring value to investors.

At $117 billion, NGX’s capitalisation represents only about 35 per cent of GDP. Mature markets typically exceed 100 per cent. Closing that gap will require more quality listings, particularly from the productive sectors of the economy, where long-term capital can translate into long-term national growth.

Finally, technology providers must treat financial inclusion as a design constraint, not an afterthought. Connectivity gaps, low digital literacy, and transactional friction are not user problems. They are product problems.

Domestic investors now account for 77.79 per cent of total market activity, a structural shift that makes the market less exposed to global sentiment swings and more reflective of domestic economic conviction. That is a nation beginning to fund its own future.

As Nigeria seeks to build a more inclusive capital economy, the objective should not simply be to increase the number of investors. It should be to increase the number of successful Nigerian businesses capable of attracting long-term investment. Every globally competitive indigenous company that chooses transparency, governance and broad-based ownership strengthens both the capital market and the country’s economic resilience. The relationship is mutually reinforcing: vibrant companies deepen the market, while a vibrant market empowers the next generation of national champions.

The foundation exists. What comes next depends on whether all stakeholders can sustain the coordination that has made this growth possible and go further. A participatory capital economy is not an aspirational language. In Nigeria today, it is an unfinished project moving steadily in the right direction.

By Blaise Udunze

It is considered that in every organised society, the home is supposed to be a place of security. It should be where families find peace after a hard day’s work, where children grow, where dreams are nurtured, and where the pressures of life temporarily fade away. This narrative comes with keen interest, having witnessed that for millions of Nigerians, home has become the country’s newest economic battlefield. This is fast becoming the experience for the vast majority of Nigerians.

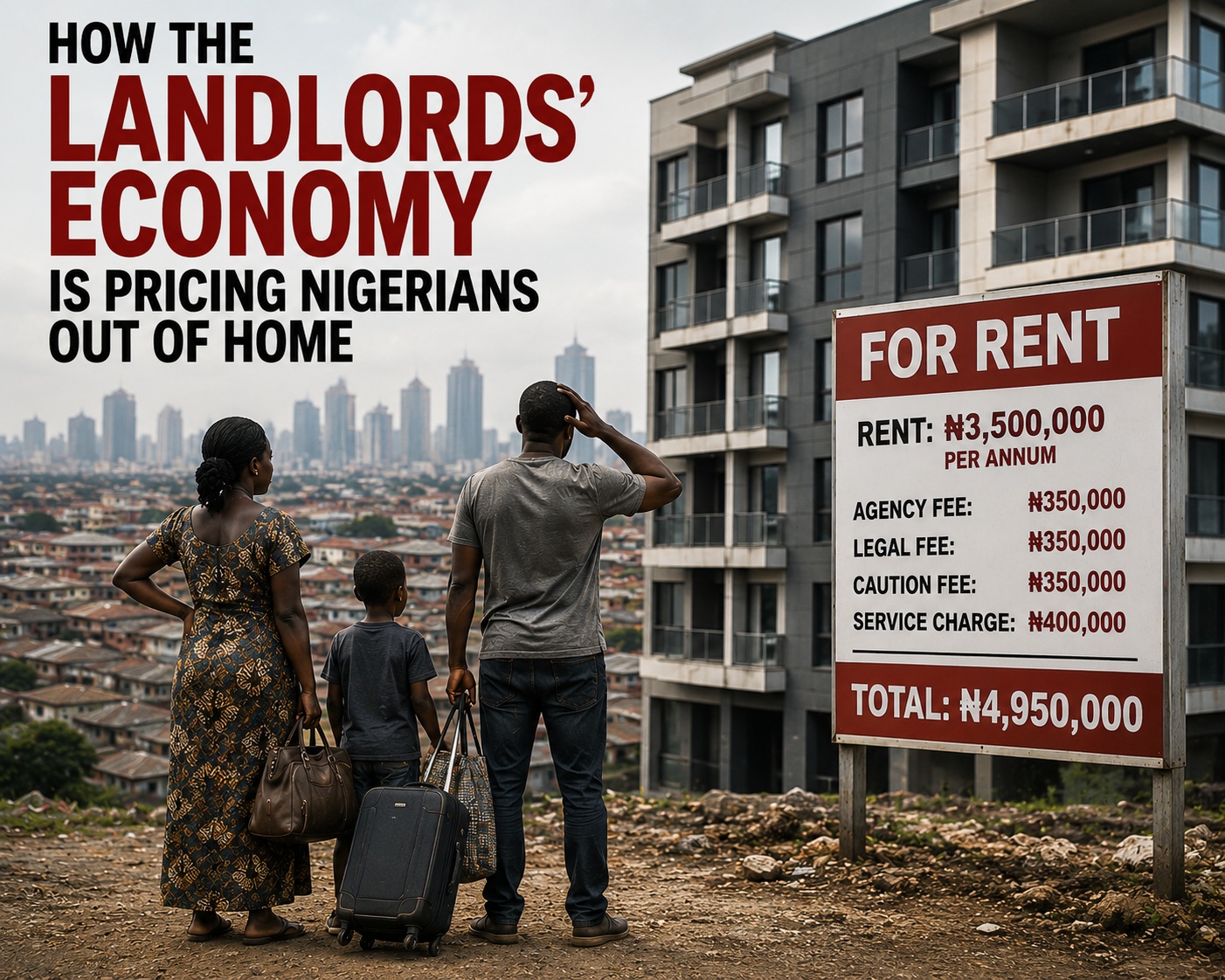

Across the length and breadth of Nigeria, citizens are deeply lamenting the skyrocketing rent. Regrettably, this has become one of the fastest-rising costs of living. An unexpected trend which has become a huge concern is that currently apartments that were rented for N700,000 or N1 million just a few years ago are now advertised for N3 million, N5 million or even higher. Amidst this bizarre development, do you know that they are often without significant improvements to the property itself? One key troubling development is that recent estimates suggest that house rents in many Nigerian cities have surged by between 100 and 300 per cent over the last two years, a pace that far exceeds the country’s official inflation rate and has placed unprecedented pressure on households already struggling with rising food, transportation and energy costs.

Landlords, through estate agents, increasingly demand one or two years’ rent upfront. Tenants are expected to pay 10 per cent of the principal rent toward agency fees, legal fees, agreement charges, caution deposits, and, in most cases, the service charge (which appears to be higher), security levies, and utility-related costs before receiving the keys. In many cases, these additional charges add hundreds of thousands or even millions of naira to the advertised rent, making the total cost of securing accommodation far beyond the reach of average-income earners. Equally disturbing is the unchecked exploitation by agent marauders, who prey on desperate house seekers by imposing outrageous and often illegal fees that further deepen Nigeria’s housing crisis. What should ordinarily be a routine life event has become a financial ordeal.

Nigeria’s housing crisis is no longer simply a property story. It has evolved into an economic emergency with profound implications for families, businesses, public health and national development.

The Federal Government’s National Housing Data Technical Committee estimates that Nigeria faces a housing deficit of approximately 15 to 20million homes. At the same time, millions of existing houses are considered structurally inadequate and lack access to essential infrastructure. If this figure is something to consider, anyone would know that these figures reveal two overlapping crises. First, this shows that millions of Nigerians cannot find decent accommodation, whilst millions more live in overcrowded, unsafe or poorly serviced housing.

At the same time, Nigeria’s population continues to expand rapidly, with cities absorbing hundreds of thousands of new residents every year.

One of the challenges is that urbanisation has consistently outpaced housing development, widening the gap between supply and demand while, predictably, rents continue to rise and affordability continues to decline.

Remarkably, housing experts generally recommend that households should spend no more than 30 per cent of their income on accommodation. For many Nigerian families, that recommendation has become almost impossible to achieve.

Teachers, nurses, journalists, police officers, civil servants, young bankers, entrepreneurs, artisans and other middle-income earners increasingly devote more than half of their annual income to rent alone. For many, housing has become the single largest financial obligation, leaving very little for every other necessity of life.

After paying landlords, food budgets shrink. Healthcare is postponed. Children are transferred to less expensive schools. Retirement savings disappear. Business investments are suspended. Vacations become unimaginable luxuries. The rent bill has become the first expense families think about and the last financial burden they can escape.

The effects extend far beyond individual households. This is totally outrageous, as financial analysts have long observed that when accommodation consumes a disproportionate share of disposable income, consumer spending across the economy inevitably weakens.

Families postpone replacing household appliances. Vehicle purchases are delayed. Furniture sales decline. Restaurants receive fewer customers. Clothing retailers experience lower patronage. Small businesses lose purchasing power from consumers whose earnings are now tied up in rent. The result is a vicious economic cycle in which rising housing costs suppress consumption, reduce business activity, and ultimately slow economic growth.

Behind every rent increase lies a deeply personal story. Consider a fictional but representative family whose experience mirrors that of countless Nigerians. The aspect of receiving notice that the annual rent for their modest two-bedroom apartment would rise from N1.2 million to N3 million comes with uneasiness. At this point, the Blessings’ family had spent months desperately searching for an alternative.

Unable to afford the increase and harassment from the landlord, they eventually relocated nearly 30 kilometres away from their former neighbourhood. The consequences were immediate. Their children had to change schools. The family’s daily commuting time doubled. Transportation costs rose sharply. Family time disappeared.

The father now leaves home before sunrise and returns late at night. The mother spends more each month commuting than she once spent on groceries. Their financial burden has not disappeared. It has merely shifted from rent to transportation and also deals with other issues like epileptic power supply and flooding, especially during this rainy season.

Unfortunately, such stories are no longer exceptional. They have become increasingly common across Nigeria’s major cities. Perhaps no demographic feels this pressure more acutely than young professionals.

Come to think of it, graduates entering the workforce quickly discover that entry-level salaries cannot support decent accommodation close to their workplaces. You would also see many remaining with their parents far longer than anticipated. Other effects include seeing them share apartments with several unrelated adults to reduce costs, whilst some endure daily commutes lasting three or four hours because affordable housing exists only in distant suburbs.

The fact is that the consequences extend beyond inconvenience because long commuting hours reduce productivity, increase fatigue, heighten stress levels and significantly diminish quality of life. Another aspect of this, which is discouraging, is that for many talented young Nigerians, financial independence, home ownership and family formation are becoming increasingly distant aspirations. Several interconnected forces explain why rents continue to climb so aggressively.

Inflation has significantly increased the cost of cement, steel, roofing sheets and virtually every construction material required to build houses. The depreciation of the naira has made imported building materials substantially more expensive. No doubt, from recent findings, there are clear indications that there is a significant increase in the prices of building materials. Let us see the period between 2024 to 2026, Cement: N6,500 – N13,000; blocks: N600 – N1100; 30T of sand: N165,000 – N250,000; 30T of granite: N530,000 – N780,000; rebars (iron) ton: N850,000 – N1,150,000 amongst others. To be fair, it is a known fact that high interest rates have increased borrowing costs for developers, while land acquisition remains prohibitively expensive in many urban centres. The very question at heart is, how has this recent development significantly impacted the apartments built five years ago and beyond?

The government has made it difficult to the point that obtaining development approvals can be slow and costly. Developers also contend with multiple taxes, infrastructure levies and rising labour costs before construction even begins. No doubt, these expenses inevitably find their way into rental prices. But one question keeps running through the minds of many, which is, how do these directly impact apartments built many years back? The truth is that market realities alone do not explain every increase.

In many locations, speculative pricing has taken hold. Some landlords have raised rents far beyond what can reasonably be attributed to maintenance or inflation, taking advantage of overwhelming demand and the severe shortage of available accommodation.

The inability of many Nigerians to purchase homes has further intensified the pressure on the rental market. Inflation, high mortgage rates and limited access to long-term housing finance have pushed home ownership beyond the reach of millions, forcing them to remain tenants for much longer than planned. This should be blamed on the government of the day, as more people compete for a limited supply of rental properties, landlords possess even greater leverage to increase prices.

Housing insecurity is also producing a less visible but equally damaging consequence for deteriorating mental health.

The constant fear of eviction, the uncertainty surrounding annual rent reviews and the enormous pressure of raising large lump sums every one or two years create persistent psychological stress.

Think of the impact of parents’ worry about disrupting their children’s education. Young couples postpone marriage because they cannot afford accommodation. Family disagreements increasingly revolve around financial pressures. Consider the part of many Nigerians who quietly or secretly or unknowingly battle anxiety, emotional exhaustion and depression arising from the struggle to secure decent housing.

None of these psychological costs clearly appear in official economic statistics, but the truth is that they profoundly affect productivity, family stability and overall well-being. It is equally obvious that the crisis is also affecting employers and businesses.

Workers forced to travel long distances arrive at work exhausted. Traffic congestion consumes valuable productive hours each day. It turns out that companies increasingly struggle to retain staff who relocate in search of affordable accommodation. Also, know that many employers face mounting pressure to increase housing allowances simply to remain competitive.

All these call for a balancing as employees demand higher wages to offset escalating living costs, further increasing operating expenses for businesses already contending with inflation, unstable exchange rates and rising energy prices.

Housing affordability is therefore no longer merely a social concern. It has become a business and national competitiveness issue.

Though Nigeria is not alone in confronting housing affordability challenges, its recent trend calls for attention. Across Africa, rapid urbanisation continues to outpace housing supply.

For this reason, Kenya has introduced ambitious affordable housing programmes aimed at expanding supply, although implementation challenges remain; this can’t be compared to Nigeria’s current situation. Ghana is not left out of the equation as it continues to battle a significant housing deficit. Ghana is also grappling with the irony of completed homes that remain unaffordable for many citizens. South Africa, despite possessing a relatively more developed mortgage market, continues to experience severe affordability pressures in cities such as Johannesburg and Cape Town.

Nigeria’s situation, however, is intensified by its enormous population, rapid urban expansion, limited mortgage penetration and one of Africa’s largest housing deficits.

Nigeria has witnessed successive governments introducing affordable housing initiatives, mortgage schemes and public-private partnerships which fails before implementation. While these programmes represent positive intentions, delivery has consistently fallen far behind growing demand.

Housing experts argue that meaningful reform requires far more than constructing a limited number of housing estates.

Nigeria must simplify land acquisition processes, reduce infrastructure costs, expand mortgage accessibility, improve planning approvals, encourage private-sector investment in affordable housing and strengthen incentives for developers willing to build homes for middle- and low-income earners.

Improving housing data is important, but accurate statistics alone cannot reduce rents. Effective implementation remains the country’s greatest policy challenge.

Let’s consider some of these salient points proffered by urban planners who insist that Nigeria’s housing crisis cannot be solved exclusively through market forces. According to them, governments at all levels must invest strategically in infrastructure and create financing mechanisms that reduce development costs. To further help reduce the housing gap, they encourage the construction of affordable rental housing rather than focusing disproportionately on luxury developments.

The truth is that if housing continues to consume an ever-growing share of household income, consumer spending, investment and long-term economic growth will remain constrained. Another key barrier that must be addressed quickly, as highlighted by researchers, is inflation, limited housing finance, weak regulatory enforcement and inconsistent policy implementation, which happen to be major bottlenecks to affordable housing delivery.

One key question that yearns for answers is whether it is not obvious to the government and other stakeholders that housing is far more than concrete walls, roofing sheets and painted ceilings? The fact is that shelter, as the meaning implies, shapes educational outcomes, influences public health, determines productivity, strengthens families, supports social mobility and contributes directly to national competitiveness.

At this stage, it is a complete shame and at the same time an irony that a nation where hardworking teachers, nurses, journalists, entrepreneurs, artisans, security personnel and civil servants cannot comfortably afford decent shelter risks weakening its middle class, widening inequality and undermining sustainable economic growth.

If the truth must be told, Nigeria’s rent crisis is therefore not merely about landlords and tenants. For a fact, it is about the future of work, family stability, economic opportunity and social justice. Clearly, it is about whether millions of hardworking citizens can enjoy the dignity that comes with secure and affordable housing.

The mistake all along, which must be eschewed, is that a country’s progress is being measured solely by the number of luxury estates it builds or the height of its skyscrapers. More importantly, it should also be measured by whether ordinary citizens can afford a safe place to call home without sacrificing their children’s education, healthcare, savings or future aspirations.

If this is not adequately addressed, this rent trap will persist until affordable housing becomes a genuine national priority backed by bold reforms and sustained implementation; millions of Nigerians will continue facing an impossible choice, which would invariably lead them to surrender their financial future to keep a roof over their heads or abandon the comfort, security and dignity that every family deserves.

Concerned stakeholders shouldn’t continue to believe that the true cost of Nigeria’s rent crisis is therefore measured only in naira. It is measured in postponed dreams, delayed marriages, fractured families, declining productivity, abandoned ambitions, struggling businesses and the quiet erosion of hope among citizens who work tirelessly every day but find the simple promise of a decent home slipping further beyond their reach.

Blaise, a journalist and PR professional, writes from Lagos and can be reached via: bl***********@***il.com

By Blaise Udunze

Daily, the world watches Nigeria through a familiar lens in what appears to be a gory situation. Especially in cases when the news headlines tell stories of farmer-herder clashes, bandit attacks, kidnappings, villages reduced to ashes or deserted by the dwellers, as thousands of Nigerians have been displaced across states such as Zamfara, Plateau, Benue, Niger, Kaduna and Nasarawa. Subliminally, this is about to become a similarly ugly occurrence in southwestern Nigeria, which is fast becoming obvious if not nipped in the bud quickly.

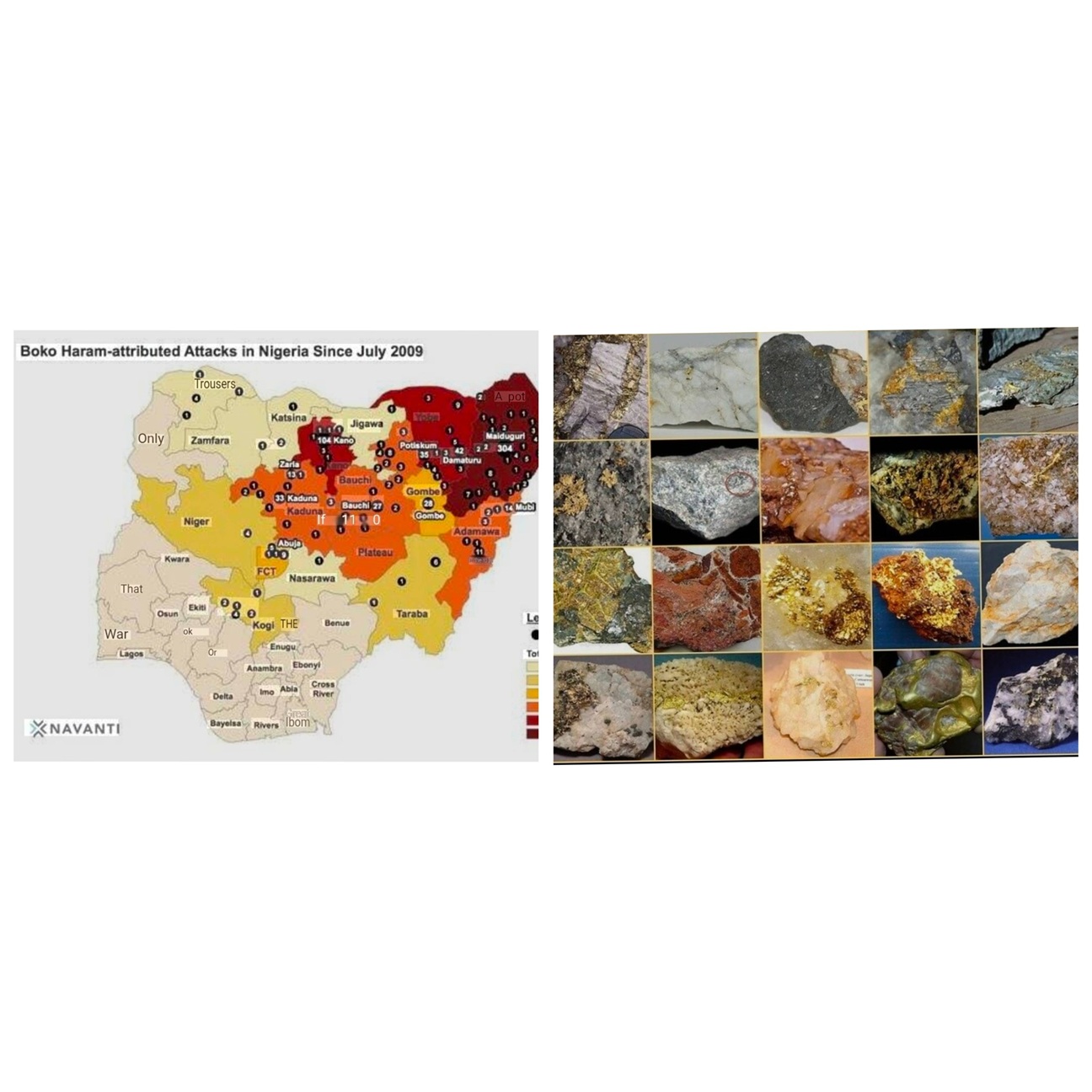

Recorded data have shown that bandits, Boko Haram, and others killed over 190,000 Nigerians in 17 years and displaced 3.7 million people.

A human rights organisation, the International Society for Civil Liberties and Rule of Law (Intersociety), in its fearful revelation, has said that no fewer than 190,150 Nigerians have been killed by bandits, Boko Haram insurgents, and suspected armed herdsmen between July 2009 and March 19, 2026, as this calls for concern.

The dominant explanations often point to ethnic tensions, religious divisions, climate change, shrinking grazing routes or weak security institutions. No doubt, those factors are certainly part of Nigeria’s complex security crisis. Yet another question deserves serious examination.

What if, in some locations, the violence is also serving another purpose? What if some of the territories experiencing repeated displacement are the same places sitting atop some of Nigeria’s most valuable mineral deposits? More importantly, if such a pattern exists, who benefits when communities disappear?

Of a truth, these questions are uncomfortable, but undeniably they deserve careful investigation rather than dismissal.

For ages, Nigeria has been naturally endowed, and it is estimated to be rich in enormous significant reserves of gold, lithium, uranium, tin, columbite and other strategic minerals increasingly sought after in the global transition to clean energy technologies. As international demand for battery minerals continues to rise, these resources have become far more valuable than they were only a decade ago.

If one overlays publicly available geological information with maps showing persistent violence, some observers argue that striking geographical overlaps appear in several regions. Such overlaps alone cannot establish causation. Correlation is not proof of conspiracy. However, they raise questions worthy of independent scrutiny.

One issue attracting increasing attention and adequately yearns for answer is whether prolonged insecurity may inadvertently or deliberately create conditions that make mineral extraction easier.

Under Nigeria’s Nigerian Minerals and Mining Act 2007, mineral resources belong to the Federal Government, while mining rights are granted through licences and leases. Community engagement and land access are expected to form part of the licensing process, although implementation varies depending on circumstances. This raises an important policy question.

What happens when the communities expected to participate in those processes have already fled because of violence?

Displacement changes the dynamics of land ownership, consent and access. While no evidence automatically proves that attacks are orchestrated to facilitate mining, the sequence of violence followed by renewed commercial activity in some locations deserves closer examination by regulators, lawmakers and investigative journalists.

In conflict studies, researchers have long observed that wars often generate economic winners alongside humanitarian losers. Could elements of Nigeria’s insecurity also be producing economic beneficiaries?

Reports over the years have documented concerns about illegal mining operations across parts of northern Nigeria. Government agencies themselves have repeatedly acknowledged that criminal networks profit from the country’s vast mineral wealth. The unresolved question is whether isolated criminality has, in some instances, evolved into more sophisticated alliances involving political influence, financial interests and international supply chains. If so, the implications extend far beyond Nigeria.

Invariably, it is clearly known that lithium has become one of the world’s most strategic commodities, powering electric vehicle batteries and renewable energy storage systems. Gold has always remained one of the safest global investment assets during periods of uncertainty. Meanwhile, it is well confirmed that the global appetite for these minerals creates enormous financial incentives.

Suppose violent displacement reduces resistance to extraction. Suppose shell companies subsequently acquire mining interests. Suppose minerals then leave Nigeria through legitimate-looking export documentation while their true value remains understated.

These scenarios remain allegations unless supported by verifiable evidence. Yet they outline a framework that investigators may wish to test rather than ignore. Financial crime experts frequently identify trade mis-invoicing as one of the most common methods of illicit financial flows worldwide.

Could Nigeria’s solid minerals sector be vulnerable to similar practices? If valuable lithium ore is deliberately but inaccurately described as lower-value material on export documents, substantial wealth could potentially leave the country without reflecting its true market value. Likewise, if unrefined gold exits through privileged channels with limited scrutiny, questions naturally arise about oversight, transparency and accountability over criminal activities which have continued to stunt and disrupt the country’s socio-economic growth and at the same time cause carnage.

Such possibilities are not accusations against any particular institution or company. Rather, they illustrate why stronger monitoring systems are increasingly essential. Another question concerns logistics.

With the high level of criminal activities, industrial mining requires heavy machinery, diesel supplies, transportation networks and specialised personnel. These are not operations that can remain invisible indefinitely.

If certain territories are genuinely too dangerous for security agencies, how do industrial-scale extraction activities reportedly continue in some remote locations? If they do, who protects those operations? Who authorises their movement? Who verifies what is extracted? Who ensures royalties and export revenues reach public coffers? These are governance questions that demand institutional answers.

Equally important is the international dimension. Minerals extracted in Nigeria ultimately enter global supply chains. Gold may pass through international refining hubs before entering financial markets. Lithium may become part of battery manufacturing destined for electric vehicles, which are being sold across Europe, North America and Asia.

One known fact is that consumers purchasing products containing these minerals rarely know the full story of where they originated.

Increasingly, however, investors and governments are demanding ethical sourcing standards that trace minerals from extraction to final manufacture.

A critical factor that must be taken into cognisance is that if insecurity is creating opportunities for illegal or unethical extraction anywhere in the world, multinational companies have responsibilities alongside national governments, of which the onus falls on the Nigerian government.

Transparency cannot stop at the mine gate. Nor should accountability end at national borders. Another issue requiring attention concerns beneficial ownership.

Across many jurisdictions, shell companies can obscure the identities of individuals ultimately controlling commercial assets. If politically exposed persons or powerful business interests are hidden behind complex corporate structures registered offshore, identifying beneficiaries becomes significantly more difficult. This challenge is hardly unique to Nigeria.

Findings showed that from Latin America to Central Africa and Southeast Asia, resistant corporate networks have frequently complicated efforts to combat corruption and illicit resource extraction. That is precisely why open corporate registries, beneficial ownership databases and transparent mining licence disclosures are becoming global governance priorities. For Nigeria, the stakes could hardly be higher.

The country stands at the centre of the world’s emerging critical minerals economy. The Nigerian government can’t feign ignorance of the fact that, when handled transparently, these resources could finance infrastructure, education, healthcare, and industrial development for generations.

In no way would the government claim not knowing that when handled poorly, they risk becoming another chapter in the well-documented “resource curse,” where extraordinary natural wealth coincides with persistent poverty, insecurity and institutional weakness.

The ultimate challenge, therefore, is not simply about mining. It is about governance. It is about whether public institutions possess both the independence and capacity to ensure that natural resources benefit citizens rather than narrow interests. It is about whether conflict zones receive genuine peacebuilding efforts instead of becoming forgotten frontiers. And it is about whether international markets demand accountability with the same enthusiasm they demand raw materials.

None of these questions should be answered through speculation. They require rigorous investigations, forensic financial analysis, satellite imagery, mining license audits, customs records, beneficial ownership disclosures and courageous journalism.

They require governments willing to open their books. They require international cooperation capable of tracing money across borders. Most importantly, they require asking questions that have too often remained unasked.

Perhaps Nigeria’s security crisis is exactly what it appears to be: a tragic convergence of historical grievances, weak institutions, criminality and environmental pressures. Or perhaps, in some places, another layer of economic incentive deserves closer scrutiny.

Until those questions are thoroughly investigated, one possibility will continue to linger. Maybe the world’s attention has been fixed on the blood spilt above ground, while too little attention has been paid to the extraordinary wealth lying beneath it.

Blaise, a journalist and PR professional, writes from Lagos and can be reached via: bl***********@***il.com