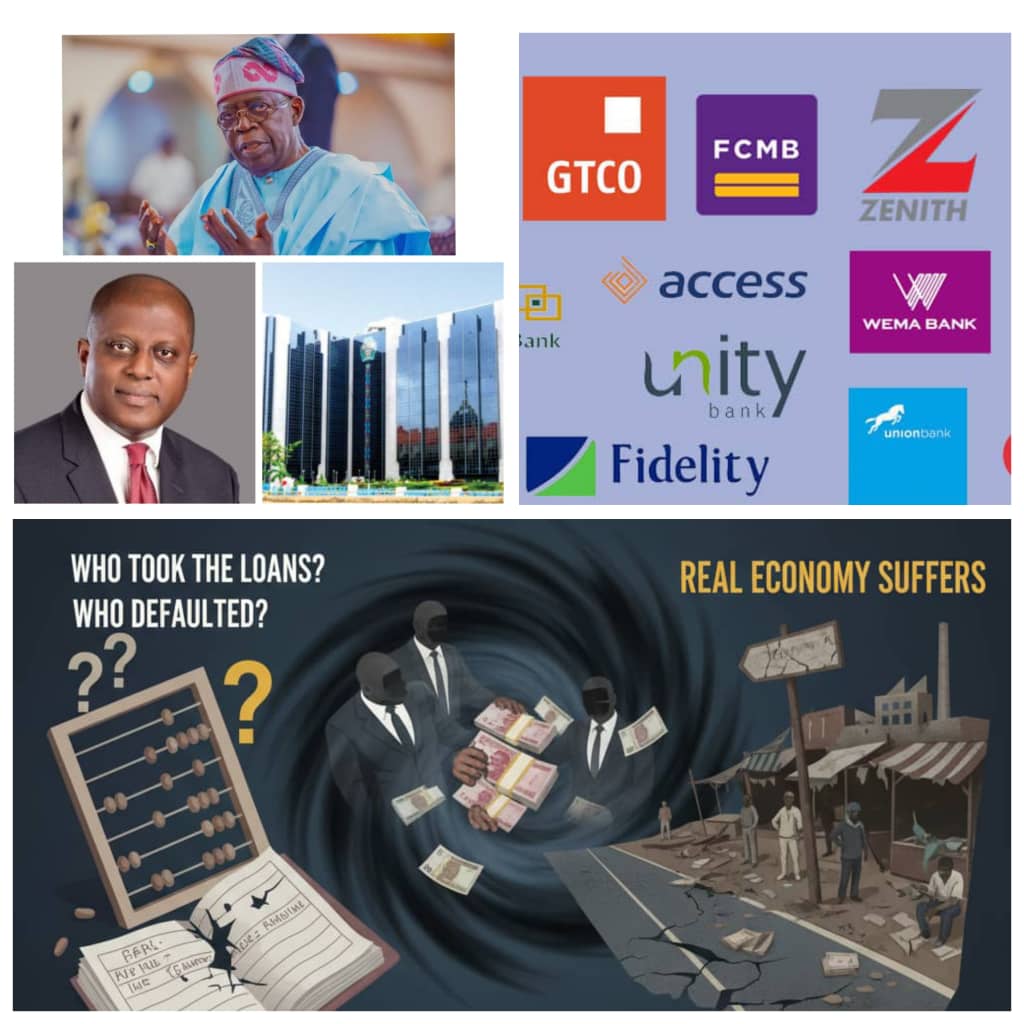

Feature/OPED

Banks’ N1.96trn Black Hole: Who Took the Loans, Who Defaulted, and Why the Real Economy Suffers

By Blaise Udunze

Nigeria’s banking sector has entered a season of reckoning. Eight of the nation’s biggest banks have collectively booked N1.96 trillion in impairment charges in just the first nine months of 2025 which represents a staggering 49 percent increase from the N1.32 trillion recorded in the same period of 2024.

Behind these figures lies a deeper question that speaks to the very soul of Nigerian finance on who received these loans that have now turned sour? Were they the small and medium enterprises (SMEs), entrepreneurs, and job creators that fuel real economic growth, or were they politically connected insiders and corporate giants whose failures are now being quietly written off at the expense of the public trust?

The Central Bank of Nigeria (CBN) is unwinding its pandemic-era forbearance regime, a policy that allowed banks to restructure non-performing loans and delay recognizing potential losses. It was a relief measure meant to protect the economy during the COVID-19 shock. But as the CBN begins to phase out this regulatory cushion, the hidden weaknesses in many banks’ balance sheets are now coming to light.

The apex bank has since placed several lenders under close supervisory engagement, restricting them from paying dividends, issuing executive bonuses, or expanding offshore operations until they meet prudential standards. Those that have satisfied the conditions are being gradually transitioned out ahead of the full forbearance unwind scheduled for March 2026. This shift, though painful, is forcing banks to confront the true state of their loan books and the picture emerging is anything but flattering.

A review of financial statements of Nigeria’s top listed banks reveals the distribution of impairment charges as of the third quarter of 2025.

– Zenith Bank Plc leads the pack with an eye-popping N781.5 billion in impairments, a 63.6 percent jump from N477.8 billion in 2024. Most of this amount to about N711 billion which occurred in the second quarter of 2025, driven by losses on foreign-currency loans and the end of regulatory forbearance. The bank’s gross loans declined by 9 percent to N10 trillion, and though its non-performing loan (NPL) ratio improved to 3 percent, that was largely due to massive write-offs.

– Ecobank Transnational Incorporated (ETI) followed closely, provisioning N393.7 billion, up 47 percent year-on-year. Inflation, exchange-rate volatility, and macroeconomic stress in Nigeria and Ghana all contributed to loan-quality deterioration. Its total loan book stands at N21.1 trillion, with a modestly improved NPL ratio of 5.3 percent.

– Access Holdings Plc posted impairments of N350 billion, representing a 141.5 percent surge year-on-year. About N255 billion of this came from loans to corporate entities and organizations, while the rest were loans to individuals. The bank cited changing macroeconomic conditions, inflationary pressures, and continued regulatory adjustments as the main culprits.

– First HoldCo reported N288.9 billion, up 68.6 percent from N171.4 billion a year earlier. The bank attributed the spike to revaluation losses and write-downs of legacy exposures in the energy and trade sectors. Notably, about N100 billions of this was incurred in the third quarter alone.

– United Bank for Africa (UBA) saw a dramatic improvement, cutting impairments from N123.5 billion to 56.9 billion, thanks to recoveries of N50.4 billion. The bank’s proactive loan-book management and collateral recoveries were credited for this performance.

– Guaranty Trust Holding Company (GTCO) posted N69.8 billion, up slightly from N63.6 billion last year. The group wrote off a key oil-and-gas exposure but maintained strong profitability, with pre-tax return on equity (ROAE) of 39.5 percent.

– Stanbic IBTC Holdings Plc recorded N11.6 billion, a sharp 80 percent decline year-on-year following recoveries of N16.3 billion on previously impaired loans.

– Wema Bank Plc, with N11 billion in impairments, reported one of the lowest provisioning levels in the industry, despite 30 percent loan growth.

Altogether, these eight banks have set aside almost N2trillion in provisions to cover potential losses, a sum roughly equivalent to Nigeria’s entire federal capital expenditure for 2025.

There have been recent claims of a modest level of loan growth that is not commensurate with the overall expansion of the banking system’s balance sheet. Data from MoneyCentral shows that the combined total loans of the nine banks stood at N65.37 trillion as of September 2025, representing a 7.42 percent increase from N60.86 trillion in 2024. This contrasts sharply with a 52.63 percent surge in combined loans recorded in the 2024 financial year and a 32.64 percent increase in 2023, according to data gathered by MoneyCentral.

The underlying question, therefore, is which sectors of the economy are actually benefiting from this reported loan growth?

The real puzzle behind these numbers is who actually received these loans that are now being impaired. While banks have long positioned themselves as engines of private-sector growth, evidence suggests that much of their lending goes to a narrow base of corporate borrowers, politically connected elites, and oil-and-gas companies. These sectors offer large-ticket deals and quick interest earnings but also carry enormous risk.

In contrast, the SME sector, which employs more than 80 percent of Nigeria’s workforce, continues to face credit starvation. Many small businesses are forced to rely on expensive informal loans or personal savings because banks deem them too risky. The pattern is clear that banks chase safety and short-term profits over inclusive growth. When their big corporate bets fail, they write them off through impairment charges, but the cumulative effect is that real economic activity suffers while the credit system grows more fragile.

Another dimension to the problem is the banking industry’s heavy investment in government securities. Over the past two years, Nigerian banks have channeled N20.4 trillion into treasury bills, bonds, and other fixed-income instruments, reaping risk-free returns rather than funding productive ventures. This “securities trap” is profitable for banks but disastrous for the economy. Instead of financing factories, farmers, or tech innovators, banks earn easy money by lending to government thereby crowding out private investment and weakening the transmission of credit to the real sector. When interest rates rise or currency values swing, the market value of these securities falls, forcing banks to record mark-to-market losses that translate into impairment charges. Thus, the same safety net that shields banks from loan risk ends up creating financial volatility of its own.

Beyond macroeconomic challenges, Nigeria’s banks are also grappling with homegrown problems like insider abuses, weak corporate governance, and ineffective risk management. Past crises in the banking sector, from the 2009 consolidation fallout to the 2016 oil-sector shock, reveal a consistent pattern: directors and senior executives often have outsized influence over loan approvals, sometimes extending credit to themselves or politically exposed entities without proper collateral or due diligence. These insider-related loans frequently turn toxic, hidden under layers of restructuring and accounting manoeuvres until a regulatory audit forces exposure.

The recent impairments may well reflect a new cycle of these historical sins as loans extended under pressure, influence, or misplaced optimism, now coming home to roost as the CBN tightens oversight. Corporate-governance codes exist, but enforcement remains uneven. Some banks continue to operate “relationship banking,” were loyalty trumps prudence. The lack of whistleblower protection, combined with weak internal-audit independence, further compounds the problem. Until boards and regulators impose real consequences for reckless lending, the system will continue rewarding the wrong behaviour and punishing taxpayers and shareholders in the long run.

At its heart, impairment is a measure of how well banks anticipate and manage risk. A rise in impairments signals that too many loans were made without properly assessing the borrower’s ability to repay, or that risk models failed to adjust to changing macroeconomic conditions. Several banks blamed their losses on exchange-rate volatility and inflation, but these are hardly new risks in Nigeria’s economic environment. The fact that impairments ballooned even as profits remained high suggests that risk-management frameworks were reactive rather than preventive which focused on compliance rather than foresight. In some cases, the sheer scale of provisioning, such as Zenith’s N781 billion or Access’s N350 billion, points to systemic underestimation of credit risk.

Every naira written off as an impairment represents not just a failed loan but a lost opportunity for the real economy. N1.96 trillion could have funded tens of thousands of new small businesses, millions of jobs, and critical infrastructure projects. Instead, these funds are trapped in the closed circuit of banking losses or vanish into opaque corporate failures. This has broader implications: as banks absorb losses, they tighten lending criteria, making it harder for genuine borrowers to access loans. High impairments signal instability, discouraging foreign investors and depositors, while credit flow dries up, productivity and job creation suffer. The result is a paradoxical economy where banks post impressive profits yet the productive sector languishes.

If there is a silver lining, it is that some banks, notably UBA, Stanbic IBTC, and Wema Bank are demonstrating improved loan-recovery strategies, more disciplined credit models, and a stronger focus on risk-weighted assets. Their experiences prove that impairment is not inevitable; it is the outcome of choices like governance, culture, and accountability. For others, the current round of provisioning should serve as a wake-up call to rethink their business models, diversify exposures, and strengthen compliance culture.

To its credit, the CBN’s forbearance unwind is a critical step toward transparency. By compelling banks to recognize their true loan losses and restricting dividend payouts until they meet prudential standards, the regulator is forcing a long-overdue cleansing of the system. However, reform must go deeper than technical compliance. The CBN must enforce public disclosure of insider-related loans, tighten penalties for concealment, and promote lending to productive sectors through targeted incentives. For instance, a tiered capital framework could reward banks that extend a higher proportion of credit to SMEs and manufacturing, while imposing stricter capital charges on speculative or insider-related lending.

Nigeria’s banking sector has shown resilience through crises, from the global financial meltdown to oil-price collapses. But resilience should not become an excuse for complacency. The N1.96 trillion impairment charges of 2025 are more than a balance-sheet adjustment; they are a mirror reflecting structural flaws in lending culture, governance, and the alignment between finance and development. To rebuild trust and relevance, banks must reorient lending toward real-sector growth, invest in credit analytics and risk intelligence that anticipate shocks, enforce transparency in board-level loan approvals and insider exposures, and collaborate with regulators to design sustainable credit frameworks for SMEs. Above all, there must be a moral recalibration of banking purpose from chasing short-term profits to fueling long-term national prosperity.

The spike in impairment charges does not mean Nigeria’s banks are collapsing. Rather, it signals an industry confronting its hidden fragilities. As the forbearance curtain lifts, the system has a chance to reset to clean up bad debts, rebuild credibility, and reconnect finance with development. But that opportunity will be wasted if the same patterns persist: insider lending, governance lapses, and a preference for easy returns over real investment. Until these issues are confronted head-on, the question will continue to echo through boardrooms and regulatory halls are Nigerian banks truly financing growth or merely recycling risk and protecting privilege? Only transparency, discipline, and a renewed sense of purpose can answer that question in the affirmative.

Blaise, a journalist and PR professional writes from Lagos, can be reached via: bl***********@***il.com

By Sani Abdulrazak, PhD

The fundamentality of securing our lives and property, especially in Northern Nigeria, cannot be overemphasised. Any other responsibility comes after this for a responsible government. Sadly, for close to two decades, Northern Nigeria has been a gallows of despair, rape, and death. From banditry and freelance killings that scratch, pierce, and are ruining the North West, to the bloody insurgency that barks and bites in the North East, to farmers-herder conflicts in the North Central, leaving behind a scorching trail of rancour and sorrow of unimaginable proportion for millions, Kaduna State was one of the worst-hit states in terms of banditry and kidnappings, ethno-religious conflicts, and freelance killings.

But in the last three years, the state has metamorphosed into one of the most peaceful in the region via the Kaduna Peace Model. More so, the recent endorsement of the Kaduna Peace Model by the Human Rights Writers Association of Nigeria (HURIWA) deserves thoughtful examination rather than unquestioning acceptance. HURIWA’s position has brought renewed attention to Kaduna State’s approach to conflict management and peacebuilding. The endorsement raises an important policy question: Has Kaduna developed a governance model capable of reducing conflict in a sustainable manner, and if so, why have other northern states not moved to adapt it? These questions deserve answers rooted in facts rather than political loyalties.

The phrase “Kaduna Peace Model” does not point to or refer to a single law, policy document, or institutional framework. Rather, it describes an evolving approach that combines conventional security operations with community engagement, dialogue among stakeholders, collaboration with traditional and religious institutions, support for security agencies, conflict mediation, and development interventions in communities affected by violence. Instead of relying exclusively on military responses, the approach seeks to address some of the social and political conditions that often sustain insecurity. Whether this amounts to a distinct governance model remains open to debate. Nevertheless, it reflects a broader understanding that lasting peace requires more than the deployment of armed personnel. Security may suppress violence temporarily, but durable peace depends equally on trust, inclusion, justice, and economic opportunity.

The next question is unavoidable: Has the approach worked?

The evidence suggests that Kaduna today presents a different security picture from that of three years ago, although not an entirely peaceful one. Around 2023, the state remained one of Nigeria’s most violence-affected regions. Conflict trackers documented frequent attacks, kidnappings, and communal violence, with 85 recorded conflict incidents resulting in 261 fatalities in the final quarter of 2023 alone. Entire communities lived under constant fear, farming activities were disrupted in several local government areas, and many roads within the state became synonymous with insecurity.

Recent years, however, indicate a significant degree of improvement in almost all parts of the state. Some communities have resumed agricultural activities, commercial movement has improved along previously troubled corridors, and government engagement with local communities has become more visible. These developments suggest that violence has, in almost all areas of the state, reduced in intensity. Yet such observations should not be mistaken for a declaration of victory.

A meaningful assessment, however, goes beyond casualty figures alone. It must also consider whether displaced persons have returned home, whether schools operate without interruption, whether farmers cultivate their lands without fear, whether markets function normally, and whether citizens genuinely perceive improvements in their daily security. Peace, as we know it, is not merely the absence of gunfire; it is the restoration of ordinary life.

It is within this context that HURIWA’s endorsement should be understood.

Civil society organisations play an important role in recognising promising governance practices, encouraging innovation, and stimulating public debate. Their endorsements can influence policy conversations and encourage governments to learn from one another. However, endorsements are neither official certifications nor substitutes for independent evaluation. Every governance model, regardless of who praises it, must remain open to scrutiny, evidence, and continuous improvement.

The larger question, therefore, is whether the Kaduna experience can be replicated elsewhere across Northern Nigeria.

It is a fact that certain principles underlying the Kaduna approach are broadly applicable. Community dialogue, cooperation between government and traditional institutions, investment in local peacebuilding, and stronger collaboration with security agencies are strategies that have relevance beyond Kaduna’s borders. But due to the non-uniformity and complexity of the hydra-headed nature of insecurity across Northern Nigeria, it becomes almost impossible for the model to work across the whole of Northern Nigeria. The security dynamics of Kaduna differ from those of Zamfara, Katsina, Sokoto, Niger, Benue, Plateau, or Borno. Banditry, communal conflicts, terrorism, farmer-herder disputes, and transnational criminal networks vary significantly in their causes and manifestations. A strategy that succeeds in one environment cannot simply be copied into another without adjustment.

This probably explains why other northern governors have not simply adopted what is popularly described as the Kaduna Peace Model. Effective governance is context-specific. Every state possesses different demographic realities, institutional capacities, historical grievances, and security challenges. Replication without adaptation risks producing disappointing outcomes. If northern states are to draw lessons from Kaduna’s experience, several adjustments are necessary. Independent conflict assessments should precede policy adoption. Local governments must become stronger partners in peacebuilding. Traditional and religious leaders should be integrated into structured dialogue mechanisms rather than informal consultations alone. Reliable security data should guide decision-making, while transparent monitoring systems should measure outcomes beyond political narratives. Economic recovery, youth employment, and access to justice must complement security interventions if peace is to endure.

Despite its widely acknowledged contributions to reducing insecurity and fostering dialogue over the past three years, the Kaduna Peace Model is not without significant shortcomings. One of its most notable weaknesses is the absence of a clearly documented framework that defines its philosophy, guiding principles, operational structure, implementation strategy, monitoring indicators, and evaluation mechanisms. Consequently, much of what is described as the “Kaduna Peace Model” exists in practice rather than in a codified, replicable document, making independent assessment, institutional continuity, and adaptation by other jurisdictions difficult. Furthermore, the model remains heavily dependent on the commitment of the incumbent political leadership, raising concerns about its sustainability beyond the current administration. While it has contributed to stabilising many communities, it has yet to comprehensively address the underlying structural drivers of conflict, including competition over natural resources and historical grievances, and questions persist regarding transparency, measurable performance indicators, accountability, and the extent of participation by women, youth, victims, and other marginalised groups. These limitations suggest that although the model has demonstrated practical value, its long-term effectiveness would be strengthened through formal documentation, institutionalisation, a robust implementation framework, and regular independent evaluation.

Possibly the greatest lesson from Kaduna is not that it has discovered a perfect formula for peace. No society has. Rather, it demonstrates that conflict management increasingly demands governance approaches that extend beyond military deployments alone. Therefore, HURIWA’s endorsement should not be viewed as the conclusion of the conversation but as its beginning. Whether the Kaduna Peace Model becomes a genuine reference point for other states will depend less on public commendation than on rigorous evidence, independent evaluation, and its ability to produce durable improvements in the lives of ordinary citizens.

In governance, therefore, the true measure of peace is not the number of endorsements the Kaduna Peace Model receives. It is the number of lives it has protected, the communities restored, and the confidence with which citizens wake each morning believing that tomorrow will be safer than yesterday.

Sani Abdulrazak, PhD, is a writer, researcher and public affairs analyst based in Zaria, Kaduna State

Feature/OPED

$40bn Net Reserves, Record Wealth, Relentless Poverty: Who Is Nigeria’s Economy Serving Today?

By Blaise Udunze

No doubt, it was a welcome announcement that Nigeria’s net foreign exchange (FX) reserves have surged by an astonishing 1,233 per cent from about $3 billion to over $40 billion. This would ordinarily be the kind of economic milestone that inspires optimism, coupled with gross external reserves of about $52.52 billion, which are sufficient to finance roughly 11 months of imports of goods and services. Penultimate week, the Governor of the Central Bank of Nigeria (CBN), Olayemi Cardoso, presented the development at the end of the 306th meeting of the apex bank’s Monetary Policy Committee (MPC) as evidence that its reforms are working.

It is no surprise that around the same period, one would say that another important economic event occurred with the government sharing more money than ever before with the federal, state, and local governments, as the Federation Account Allocation Committee (FAAC) distributed a record N2.55 trillion, representing an increase of N250 billion over the N2.3 trillion shared in the preceding month.

Of course, the official figures are impressive numbers. Yes, anyone would conclude that the economy is becoming stronger, more stable and better positioned for growth. While this suggests stronger public finances, it also raises the question of whether these larger allocations are producing tangible improvements in the lives of ordinary Nigerians. More interesting is that another set of figures tells a completely different story.

According to the World Bank’s newly approved Country Partnership Framework for Nigeria, 61 per cent of Nigerians now live below the poverty line, while about 79 per cent are either poor or vulnerable to falling into poverty. More than 139 million Nigerians live below the poverty line. Over 86 million people lack access to electricity, while millions of young Nigerians enter the labour market every year with little prospect of decent employment.

The contradiction could not be starker. If reserves are rising, government revenues are increasing, and governments at all levels are receiving record allocations, why are the lives of ordinary Nigerians becoming more difficult?

This is the question policymakers must answer not with statistics, but with tangible improvements in the lives of citizens. If government agencies engineering these figures must know, these are not merely economic statistics; they are the lived realities by which citizens judge any government.

Foreign exchange reserves are not an economic trophy. They are a means to an end. Strong reserves are expected to stabilise the currency, reassure investors, strengthen the country’s ability to withstand external shocks and create an enabling environment for investment, production and employment.

But reserves alone do not feed families nor would they reduce their housing rents. They do not lower transport fares. They do not reduce school fees. They do not make healthcare affordable. Nor do they automatically create jobs.

Ultimately, this is to say that the success of macroeconomic reforms must be measured not by the strength of the CBN’s balance sheet but by the wellbeing of the Nigerian people.

Historically, unlike our dear country, countries that consistently build substantial foreign exchange reserves do so on the back of strong economic fundamentals. The fact is that they maintain sustained trade surpluses, export diversified products, attract large volumes of long-term foreign direct investment (FDI), develop globally competitive manufacturing industries and continuously improve productivity.

Nigeria, unfortunately, still struggles on nearly all these fronts. The country’s export earnings remain overwhelmingly dependent on crude oil. Non-oil exports remain relatively insignificant. Value-added manufacturing exports are weak. Another area that raises concern is agriculture, which continues to export mostly raw commodities rather than higher-value processed products despite being known previously as the country’s mainstay. With all these so-called developments, Nigeria still imports refined petroleum products, machinery, pharmaceuticals, industrial inputs and even food that could be produced locally.

This naturally raises an uncomfortable but legitimate question that requires an answer. Yes, it would be necessary to ask: How exactly has Nigeria grown and accumulated over $40 billion in net foreign exchange reserves without the structural fundamentals that typically support such reserve growth?

The apex bank has continued to credit exchange-rate reforms, improved transparency, stronger investor confidence and increased diaspora remittances. Well, it would be said that these achievements deserve recognition.

However, they do not completely explain the scale or, more importantly, the sustainability of the reserve accumulation.

Nigeria has not consistently recorded the large trade surpluses associated with countries that rapidly accumulate reserves. Oil production remains below historical capacity. Export diversification remains limited. Ease of doing business continues to be constrained by multiple taxation, infrastructure deficits, insecurity, policy uncertainty, logistics bottlenecks and unreliable electricity.

Without addressing these structural deficiencies, reserve accumulation risks becoming more financial than productive.

Equally important is the question of foreign direct investment. Governor Cardoso has argued that improved macroeconomic stability is attracting foreign investors. That may well be true. But confidence alone does not build factories.

The real question is how much fresh FDI has actually entered Nigeria’s productive sectors? How much has gone into manufacturing? How much into agro-processing? How much into export-oriented industries capable of generating sustainable foreign exchange earnings and creating jobs?

If reserve growth is being driven largely by short-term portfolio investments attracted by high interest rates rather than long-term productive investment, then Nigeria remains vulnerable. Portfolio investors can exit as quickly as they entered whenever global financial conditions change.

The unarguable fact is that foreign direct investment, by contrast, creates factories, expands production, develops supply chains and creates lasting employment. Nigeria desperately needs more of the latter.

The CBN also points to diaspora remittances as a growing source of reserve accumulation, projecting inflows of approximately $1 billion every month before the end of the year. Again, this is encouraging.

Again, the country will not be tired of asking questions because several of these questions deserve closer examination. How much of these remittances represent genuinely new inflows rather than funds previously routed through informal channels? Come to think of it, how much of these remittances finance productive investments instead of household consumption? Can diaspora remittances realistically become a permanent substitute for export competitiveness?

No economy has ever industrialised on remittances alone. A nation cannot sustainably depend on the sacrifices of its citizens abroad while failing to create opportunities for them at home.

Beyond the reserve figures lies another troubling contradiction. This is more disturbing because every month, FAAC distributes unprecedented sums to governments across Nigeria. Yet again, with daily regret, the average Nigerian struggles with deteriorating public services.

Honestly speaking, it has become so frustrating that the majority of the people who yearn for pleasant or attractive experiences are struggling as roads remain poor, public hospitals remain overstretched, schools continue to decline, electricity remains unreliable, water infrastructure remains inadequate, and youth unemployment remains widespread. Worst still, think of the cases as the nation continues to grapple with rising inflation, worsening poverty, declining purchasing power, struggling businesses and persistent insecurity.

One major contradiction is that if revenues continue rising while poverty deepens, then one unavoidable question must be asked: Where is the money going? Another pertinent question: How can the citizens be surrounded by water and still suffer from thirst or soap lather in their eyes?

This has been the predominant worry in the minds of many even as the World Bank itself acknowledges this disconnect. While praising recent macroeconomic reforms for improving fiscal stability, strengthening foreign reserves and restoring investor confidence, it concludes emphatically that the gains have not translated into meaningful improvements in living standards.

Ironically, despite the claims of declining inflation, it continues to erode purchasing power. Social protection remains weak. Most Nigerians remain trapped in low-productivity informal employment.

One contradicting and astonishing step taken recently is nowhere more evident than in the Central Bank’s monetary policy. Consider this: despite a marginal decline in headline inflation to 15.91 per cent in June 2026, the Monetary Policy Committee retained the benchmark Monetary Policy Rate (MPR) at 26.5 per cent, alongside a 45 per cent Cash Reserve Ratio (CRR) for commercial banks.

The decision reflects understandable caution. The CBN remains concerned that escalating geopolitical tensions in the Middle East could increase global energy prices, worsen imported inflation and reverse recent gains in price stability.

From a monetary policy perspective, this caution is defensible. But from the standpoint of businesses and households, the consequences are profound. An interest rate of 26.5 per cent inevitably translates into prohibitively expensive bank lending.

The ripple and adverse effects have led to manufacturers struggling to finance expansion. Another tough aspect is seeing the small and medium-sized enterprises, the backbone of employment generation, find access to affordable credit increasingly difficult. Entrepreneurs postpone investments. Factories delay expansion. Potential employers reduce hiring. Economic growth slows.

Ironically, while it is understandable that high interest rates may help stabilise inflation and attract foreign portfolio inflows that support reserves, it should be made known that they simultaneously suppress domestic investment, production and job creation.

In other words, the same policies helping strengthen the country’s macroeconomic indicators may also be constraining the real economy. Even the celebrated decline in inflation deserves closer scrutiny.

The national inflation rate may have eased marginally to 15.91 per cent, but this national average masks severe hardship across much of the country, which continues to create perpetual pain.

How best can this be figured out if data from the National Bureau of Statistics show that 19 states and the Federal Capital Territory recorded inflation rates exceeding 30 per cent, with Niger State above 42 percent and Kogi State exceeding 41 per cent?

Food inflation continues to rise, driven by increases in the prices of tomatoes, pepper, beef, yams, garri and other staple foods.

Businesses themselves remain unconvinced. The Organised Private Sector has welcomed the marginal moderation in inflation but insists that prices remain painfully high for both consumers and businesses.

Leaders of small business associations argue that market realities tell a different story from headline statistics. For millions of Nigerians, inflation is not measured by percentages. It is measured by empty shopping baskets. By reduced meal portions. By businesses shutting their doors. By families withdrawing children from school. By postponed medical treatments.

From a theoretical standpoint, macroeconomic stability is undoubtedly necessary. Without it, sustainable development is impossible. But it would also be agreed that macroeconomic stability alone is not sufficient. It can be argued further that economic reforms must eventually improve household incomes, reduce poverty, expand productive employment and raise living standards.

Otherwise, they risk becoming reforms that look impressive in economic reports but remain invisible in everyday life.

The truth remains that with the current situation, Nigeria therefore stands at a critical pivotal moment and the decisions taken now will determine its future.

The current reserve position should not become a destination for celebration but a foundation for deeper structural transformation. The country must diversify exports beyond crude oil. Strengthen manufacturing. Promote value-added agricultural exports. Improve electricity supply. Reduce the cost of doing business. Expand logistics infrastructure. Attract long-term productive investment.

In addition, support local industries with affordable financing. Strengthen institutions. Improve governance and ensure greater accountability for public spending. Only then will rising reserves translate into rising prosperity. Only then will record FAAC allocations produce visible development. Only then will macroeconomic stability become household stability.

The ultimate measure of economic success is not the number of dollars held in the Central Bank’s vaults. It is whether parents can afford school fees and housing rent. Whether young graduates can find decent jobs. Whether businesses can borrow, produce and expand. Whether families can afford food without sacrificing nutrition. Whether citizens feel that economic growth includes them.

Until those questions receive positive answers, one uncomfortable question will continue to linger. Who Is Nigeria’s Economy Serving Today?

Blaise, a journalist and PR professional, writes from Lagos and can be reached via: bl***********@***il.com

By Henry Obiekea

Nigeria’s banking industry is entering one of the most significant transformation periods since the 2005 banking consolidation exercise. The Central Bank of Nigeria’s (CBN) ongoing recapitalisation programme is more than a regulatory requirement—it is a strategic investment in the country’s financial future. If implemented successfully, it has the potential to strengthen financial stability, deepen credit access, improve investor confidence, and support a more inclusive and resilient economy.

In March 2024, the CBN announced new minimum capital requirements for commercial, merchant and non-interest banks. Under the new framework, international commercial banks are required to maintain a minimum paid-up capital of ₦500 billion, national commercial banks ₦200 billion, and regional commercial banks ₦50 billion. Merchant banks are required to hold ₦50 billion, while national and regional non-interest banks are required to maintain ₦20 billion and ₦10 billion respectively. The policy reflects the realities of today’s economy, where inflation, currency depreciation and expanding financial demands have significantly altered the capital required to support sustainable banking operations.

Many institutions have responded through rights issues, public offers, private placements, mergers and acquisitions in pursuit of the revised capital requirements. Beyond regulatory compliance, the exercise is already encouraging stronger governance, better capital planning and increased investor participation within Nigeria’s financial markets.

The recapitalisation conversation, however, extends beyond deposit money banks. The CBN has also introduced revised capital requirements for microfinance banks, recognising the critical role they play in extending financial services to underserved individuals, nano businesses and small enterprises. As the financial landscape becomes increasingly digital, stronger capital bases will enable these institutions to invest in technology, cybersecurity, risk management and product innovation while maintaining public confidence.

For Nigeria’s rapidly growing fintech ecosystem, although they are subject to different licensing frameworks depending on their operations, the broader regulatory direction is equally clear. Institutions that facilitate payments, tech-enabled banking, lending and savings are expected to maintain governance, capital and consumer protection standards appropriate to their respective licensing frameworks. This evolution is essential as fintechs continue to account for a growing share of financial transactions and provide services to millions of previously underserved Nigerians. Collectively, these reforms present a unique opportunity to reshape Nigeria’s financial ecosystem.

A stronger banking sector creates stronger economic outcomes. Well-capitalised financial institutions are better positioned to finance infrastructure, manufacturing, agriculture, housing and technology. They possess greater capacity to absorb economic shocks, support long-term lending and withstand periods of market volatility. More importantly, they can extend larger volumes of prudently underwritten credit to businesses that create jobs and stimulate economic growth.

For small and medium-sized enterprises, which contribute significantly to Nigeria’s GDP and employment, improved access to financing remains one of the greatest growth enablers. Recapitalisation should not be assessed solely by stronger balance sheets, but also by the extent to which additional capital supports productive economic activity.

Despite remarkable progress over the last decade, millions of Nigerians remain underserved by formal financial institutions. Expanding financial inclusion requires complementary approaches across commercial banks, microfinance banks, fintechs and other regulated financial institutions. Achieving meaningful inclusion requires collaboration across commercial banks, microfinance banks, fintech companies and regulators. Each institution serves different customer segments, yet all contribute towards a common objective: bringing more Nigerians into the formal financial system.

At FairMoney Microfinance Bank, recapitalisation aligns with our continued investment in responsible lending, digital banking capabilities, sound risk management and financial inclusion. We believe technology can complement prudent credit assessment and help extend access to financial services for eligible individuals and businesses.

As the recapitalisation programme progresses, success should ultimately be measured by broader outcomes: stronger institutions, deeper financial inclusion, increased SME financing, enhanced consumer confidence and sustained economic growth. Capital itself does not transform economies; how that capital is deployed does.

The Federal Government and the Central Bank of Nigeria have introduced reforms aimed at strengthening the long-term resilience of the financial sector. Continued implementation of these reforms will be important in supporting financial stability and sustainable sector growth. These decisions require vision, consistency and regulatory discipline. While the adjustment process may present short-term challenges for some institutions, the long-term benefits for financial stability, investor confidence and economic development far outweigh the costs.

Nigeria possesses one of Africa’s most dynamic financial services sectors. With stronger capital foundations, responsible innovation and continued collaboration between regulators and financial institutions, the country is well positioned to build a banking ecosystem capable of supporting its development ambitions, empowering millions more individuals and businesses, and supporting inclusive economic development over the long term.

Henry Obiekea is the Managing Director of FairMoney Microfinance Bank

Pingback: What Nigerian Banks Don’t Want You to Know About Taking a ₦100,000 Loan - FinanceKI