Feature/OPED

CBN’s 303rd MPC Meeting: A Technocratic Victory, an Economic Setback, and a Missed Opportunity on Nigeria’s Real Crisis

By Blaise Udunze

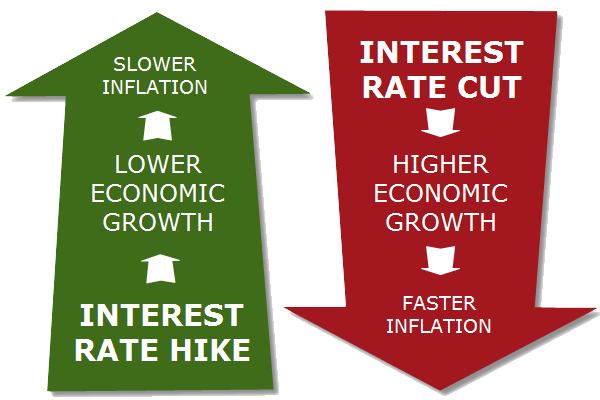

The Central Bank of Nigeria (CBN) 303rd Monetary Policy Committee (MPC) meeting arrived at a time of unprecedented tension within the Nigerian economy. The country has not faced a more difficult convergence of challenges for more than a decade in the area of crushing food inflation, unrelenting insecurity, slowing growth, weak purchasing power, a fragile exchange rate, and rapidly eroding business confidence, as these are the current realities.

Yet, against this troubling backdrop, the MPC chose to retain the Monetary Policy Rate (MPR) at 27 percent, kept the Cash Reserve Ratio (CRR) at a record-high 45 percent, held the Liquidity Ratio (LR) at 30 percent, and adjusted the asymmetric corridor, making it more reflective of technocratic cautions than economic realities

With the tense atmosphere, boldness, contextual sensitivity, and human-centric policymaking are required to douse the challenges. Instead, what Nigeria received was another round of technocratic orthodoxy, at a time when orthodoxy has clearly failed.

Why This MPC Meeting Matters More Than Any in Recent Memory

The importance of the 303rd MPC meeting cannot be overstated. It occurred at a time when:

– Nigeria’s food inflation remains structurally high, driven mainly by insecurity, not excess liquidity.

– Banditry, farmer-herder conflicts, kidnapping, and terrorism have made farming a high-risk activity across the North-East, North-West, North-Central, and increasingly the South, which has created an environment where fear, uncertainty, and instability have become the daily reality for millions of Nigerians.

– Growth has slowed, reflecting a tightening credit environment and collapsing consumer demand, while households spend 70-80 percent of income on food, according to industry surveys.

– Private-sector credit is shrinking, while government borrowing is expanding.

– The naira, though stabilising, remains vulnerable.

Given these realities, the MPC was expected to signal a shift, however modest, toward a more growth-supportive stance. Instead, it doubled down on tight policy.

Many analysts interpret this as a sign that the CBN is more committed to defending the naira and preserving the appearance of stability than responding to the lived experiences of citizens and businesses.

The CBN’s Insecurity Blind Spot: Food Prices Cannot Fall When Farmers Are Running for Their Lives

One of the biggest ironies in Nigeria today is the insistence by some policymakers that food prices are “declining” or that inflation is “moderating,” even as insecurity remains the biggest structural threat to price stability.

This contradiction reveals the central tension of Nigeria’s current economic moment; the macro indicators are improving, but the real economy, especially the food system, is collapsing under insecurity.

Recently, the United Nations World Food Programme (WFP) issued a stark warning that 35 million Nigerians are projected to face severe food insecurity by the 2026 lean season, which is the highest number ever recorded. Why? Because insurgent attacks are intensifying. Farmers are being killed or kidnapped. Entire communities are paying “harvest taxes” to armed groups.

Today, we witness farmers abandoning thousands of hectares of farmland. Irrigation systems, seeds, and inputs are inaccessible in conflict zones. This creates a vicious cycle as:

– insecurity reduces agricultural production,

– Reduced production pushes food prices up,

– Rising food prices fuel inflation,

– inflation erodes purchasing power,

– poverty deepens,

– insecurity worsens.

Yet the MPC communique did not mention this core driver of inflation in any meaningful way.

Instead, it continued to frame inflation as a monetary problem; something interest rates alone can fix. This is not only analytically flawed; it shows a more dangerous misdiagnosis that will prolong Nigeria’s food crisis.

The Hidden Question: Are Nigeria’s Inflation Numbers Truly Reliable?

A quiet but growing debate is emerging within the financial community about Nigeria’s inflation numbers and macroeconomic figures being massaged.

Dr. Tilewa Adebajo, CEO of CFG Advisory, put it bluntly, “Zero rate cut suggests the CBN MPC may not be totally confident in the NBS recent inflation numbers at 16 percent.”

This suspicion is not unfounded. Considering the recent realities facing the citizens, Nigerians are spending more on food than at any time in the last two generations. Staple prices such as rice, yams, garri, and beans are still high in almost every major market. Transport, rent, fuel, and electricity costs remain on the high side. Businesses report that operating expenses have not declined by any meaningful margin. Yet official inflation fell sharply to 16.05 percent.

It is mathematically difficult for headline inflation to fall significantly when food inflation, which is the most dominant component, continues to rise due to insecurity, logistics disruptions, and energy costs. This mismatch has forced many economists to ask: what exactly is being measured, and is the methodology still credible? For households already on the brink, numbers that suggest “improvement” feel not only inaccurate but insulting.

The Disconnect Between Governance and Lived Experience

This is where Nigeria’s economic narrative collapses, as the statistics may suggest progress, but households feel worse off than ever. This is why growing segments of society describe government optimism as tone-deaf.

A country cannot be “on the right path” when its citizens cannot afford rice, cannot fuel their generators, cannot pay transport fares, and cannot access credit to expand their businesses.

This disconnect exposes what many call the technocratic illusion, which is overly relying on models, spreadsheets, and monetary tenets in a country where insecurity, not excessive demand, is driving inflation. It reflects a divide between governance and reality, data and hunger, stability and survival.

Tight Monetary Policy: A Victory for Banks, a Defeat for the Real Economy

While the CBN insists that its tight stance is essential for price stability, analysts warn that the costs are becoming unbearable. Dr. Muda Yusuf argues that even a small rate cut of 25 to 50 basis points would have signaled a commitment to growth. Instead:

– Lending rates remain between 33 percent and 45 percent, suffocating SMEs.

– Credit to the private sector fell from N75.9 trillion to N72.5 trillion in just one month.

– Government borrowing is rising, crowding out real-sector lending.

– Manufacturers have cut production, citing financing conditions.

– Job creation is slowing, especially in youth-led sectors.

Banks, meanwhile, are reporting stronger margins and higher interest income. The question is no longer whether tight policy fights inflation. The question is whether Nigeria’s economy can survive its side effects.

The Naira: Stability Built on Fragile Foundations

The CBN’s main justification for maintaining the high MPR is to attract foreign portfolio investment (FPI), support the naira, and avoid destabilizing capital outflows. But this stability is fragile. FPIs are temporary “hot money.” They disappear at the slightest global shock.

Nigeria has suffered the consequences of relying on this route in 2014, 2018, 2020, and 2022. A sustainable naira requires:

– More domestic production

– Higher exports

– Better security

– Improved energy supply

– and a functional agricultural sector.

None of these received priority mention in the MPC deliberations.

The Real Test of Reform Is in People’s Lives, Not in Abuja’s Spreadsheets

Nigeria’s macroeconomic gains are being celebrated abroad. But hunger, joblessness, and despair are expanding at home. This is the irony of the current moment:

– Inflation is easing, yet hunger is rising.

– FX reserves are improving, yet insecurity is deepening.

– Subsidies are gone, yet the fiscal space they were meant to create is invisible.

– Reforms have stabilised numbers, but not people.

The World Bank’s October 2025 report warned that Nigeria’s progress means nothing if human welfare remains in decline. The success of reforms must now be measured not by GDP or FX reserves, but by how many Nigerians can afford to eat, work, and live with dignity.

A Missed Opportunity, Again

The 303rd MPC meeting should have been a turning point, a recognition that Nigeria’s inflation crisis is rooted in insecurity and supply shocks, not excess liquidity. Instead, the committee delivered technical caution, policy defensiveness, and an over-reliance on interest rate orthodoxy.

Nigeria needs a monetary policy that understands where the real crisis lies, in the abandoned farmlands, the unsafe highways, the displaced farming communities, and the markets where food prices rise weekly.

Without confronting this, Nigeria will continue to win macroeconomic battles while losing the war for human survival.

The Path Nigeria Must Chart to End Insecurity, Food Inflation, and Economic Stagnation

Nigeria’s 303rd MPC meeting made one thing clear that the country cannot escape its economic turmoil through monetary tightening alone. Interest rates cannot secure farms, rebuild supply chains, or put food on the table. What Nigeria needs now is a decisive, coordinated strategy that goes beyond the narrow lens of inflation targeting.

– First, security must become the cornerstone of price stability.

Food inflation will not recede until farmers can return to their lands without fear. A National Agro-Security Task Force merging military units, agro-rangers, police, intelligence agencies, and vetted community guards must secure farmlands and food corridors. Without safety in the agricultural belt, every other policy becomes cosmetic.

– Second, the CBN must adopt a dual mandate: price stability and growth.

Nigeria’s rigid monetary stance is suppressing credit, killing jobs, and suffocating production. Lowering the CRR to a realistic 25-30 percent and providing targeted single-digit loans to SMEs and manufacturers is essential for economic revival. Monetary policy must support growth, not stifle it.

– Third, Nigeria must rebuild trust in its economic data.

Doubts about inflation figures erode confidence. Modernizing NBS data-collection methods through digital analytics, satellite tools, and transparent audits is crucial. No country can chart a path out of crisis with unreliable statistics.

– Fourth, structural reforms must address cost-push inflation at its root.

Nigeria’s inflation is driven by high production costs despite poor roads, expensive power, weak logistics, and inefficient transport systems. Repairing agricultural roads, expanding rail freight, investing in cold-chain infrastructure, and boosting industrial power supply will reduce costs and unlock productivity.

– Fifth, the country must build an export-driven economy.

Stable exchange rates come from production, not high interest rates. Tax incentives for exporters, fully functional Special Economic Zones, and improvements in customs efficiency will help Nigeria attract stable capital and grow non-oil exports.

– Sixth, social protection must expand to shield vulnerable households.

Targeted food vouchers, transport subsidies, and school feeding programs are necessary to cushion families from economic shocks. Reform without social protection is a recipe for social unrest.

– Finally, Nigeria needs a whole-of-government Economic War Room.

Security agencies, economic ministries, the CBN, the NBS, and the private sector must collaborate in real time to track inflation drivers, coordinate responses, and prevent policy contradictions. Economic management must become proactive, not reactive.

Stability Must Translate to Human Welfare

The 303rd MPC meeting signaled caution, but what Nigeria needs is direction. It needs clarity, boldness, and policies rooted in the lived realities of millions. Monetary tightening has achieved what it can; the next phase requires confronting insecurity, energizing production, restoring data credibility, and building a growth-driven economy.

Nigeria cannot tighten its way out of this crisis. It must reform, secure, produce, and most importantly, protect its people. If not, the nation will continue to win statistical battles while losing the war for human survival.

Blaise, a journalist and PR professional, writes from Lagos, can be reached via: bl***********@***il.com

Ever noticed how easy it is to get a movie in Nigeria, sometimes before or right after it hits cinemas? For decades, films, music, and series have circulated in ways that felt almost natural; roadside DVDs, download sites, and streaming hacks became part of how we consumed entertainment. It became the default way people experienced content.

But what many don’t realise is that what feels normal for audiences has real consequences for the people behind the screen. As Nigeria’s creative industry grows into a serious economic force, piracy isn’t just a “shortcut” anymore; it’s a drain on the very lifeblood of creativity.

The conversation hit the headlines again with the alleged arrest of the CEO of NetNaija, a platform widely known for downloadable entertainment content. Beyond the courtrooms, the story reopened an important question: how did piracy become so normalised, and why should we care now?

Filmmaker Jade Osiberu put it into perspective in a post that resonated across social media: for many Nigerians, pirated CDs and downloads were simply the most accessible way to watch films. Piracy didn’t just appear from nowhere. It grew because legal options were limited, streaming platforms scarce, and affordability a challenge. In other words, piracy is as much a story about opportunity and access as it is about legality.

The cost of this convenience is real. Every illegally downloaded or shared film chips away at revenue that sustains the people who create it. Producers risk their own capital to tell stories, actors and crew rely on fair compensation, and distributors and cinemas lose income when pirated copies hit screens first. Over time, this doesn’t just hurt profits; it erodes confidence in investing in new projects and threatens the ecosystem that allows Nigerian creativity to flourish.

Piracy is also about culture and necessity. Many audiences never intended harm; they simply wanted stories in a system that didn’t always make legal access easy. Streaming services were limited or expensive, internet access was spotty, and distribution was weak outside major cities. Piracy became the default, and generations grew up seeing it as normal. But what was once a practical workaround has now become a barrier to sustainable growth.

This is where enforcement comes in. Legal action, like the NCC’s intervention against NetNaija, isn’t about pointing fingers at audiences; it’s a reminder that creative work has value and that infringement carries consequences. It’s about sending the message that the people who write, produce, act, and edit these stories deserve protection. Enforcement alone isn’t enough, though. Without accessible, affordable legal alternatives, audiences will naturally gravitate back to piracy.

The bigger picture is this: Nollywood is no longer just a local industry. It’s a global player, employing thousands, creating cultural influence, and generating revenue across multiple sectors. Its growth depends not just on talent, but on a system that rewards creators, protects their work, and builds a sustainable ecosystem.

Piracy may have been normalised in the past, but its consequences today are impossible to ignore. It threatens livelihoods, investment, and the future of stories that define Nigeria culturally and economically. Understanding its impact isn’t about shaming audiences or vilifying platforms; it’s about valuing the people behind the content, the stories themselves, and the industry’s potential.

The real question isn’t just whether piracy is illegal. It’s whether Nigeria is willing to build an entertainment ecosystem where creators thrive, stories get told properly, and audiences can enjoy them without undermining the very people who made them possible. Until that happens, the cost of convenience will keep being paid by someone else, and it’s the people who create the magic.

By Timi Olubiyi, PhD

The ongoing tensions in the Middle East may seem geographically distant from Nigeria, but the economic effects are already being felt in very real and personal ways across many countries, including Nigeria, even though light at the moment. For ordinary Nigerians, the impact shows up in rising fuel prices, which are already happening. So, we may be experiencing increased transportation fares, higher food costs, and a volatile naira if the unrest continues. Remember, the electioneering and campaign season is almost here politicians may face a far more complex environment than in previous cycles. With the current reality, voters may have less patience, interest and may be more economically stressed, and more focused on immediate survival than long-term projections, which the elections stand for.

The first and most immediate effect of global tension anywhere is usually a spike in crude oil prices due to fears of supply disruption. Ordinarily, this should appear like a positive impact for Nigeria as an oil-exporting country because higher oil prices should increase government revenue, but the benefit is often limited by our production challenges, oil theft, pipeline vandalism, and largely the pegged Organisation of the Petroleum Exporting Countries (OPEC) output quotas. In reality, Nigeria may not produce enough oil to fully take advantage of the high prices that may arise. At the same time, higher global oil prices generally increase the cost of imported refined fuel, shipping, insurance, and manufactured goods. Since Nigeria still imports a dominant and significant portion of what we consume from abroad, these higher global costs may quickly translate into domestic inflation if the trend continues, and this can happen because it is an external force beyond control. The result will be painful, though small businesses will struggle even more with operating expenses, transport costs, and transaction costs will climb further. Already, many households are battling many challenges,s but the current reality will have their purchasing power shrinking even more. Inflation in Nigeria is not just a statistic; it is the daily reality of families and businesses who must continue to spend even more for the same needs and services. In an economy where food inflation is already high, any additional imported inflation would worsen hardship and deepen poverty levels.

Another major effect is on foreign exchange stability, and campaign financing itself could also be affected in the coming elections if the global tension is not tamed early enough. Whenever global tensions rise, investors move their funds to safer markets, and this often weakens emerging market currencies, and the Naira is not immune. A weaker naira makes imports even more expensive, which could further fuel inflation. It may also increase the cost of servicing Nigeria’s external debt, putting more pressure on government finances. The global uncertainty that we will experience in the coming weeks to months may likely reduce foreign portfolio investment in Nigerian equities and bonds. Investors may prefer to wait and see how things unfold. This cautious sentiment would slow capital inflows to the capital market and into our economy, and the outcome is better imagined. Companies that rely heavily on imported raw materials are especially vulnerable to exchange rate volatility that will come with the current reality.

If tensions in the Middle East escalate further, for instance, through a broader regional conflict involving major oil producers or a prolonged disruption of key shipping routes, oil prices may even surge further sharply, global inflation could intensify, and financial markets could become more volatile. In such a scenario, Nigeria might see temporary revenue gain,s but inflation could accelerate faster than income growth in my opinion. The naira could face renewed pressure, and interest rates might remain high as monetary authorities attempt to control inflation. Poverty levels could worsen in real time because, as real wages fail to keep pace with rising prices, the number of people living below the poverty line increases. Youth unemployment, already a concern, may increase if businesses cut back on hiring due to uncertainty or think of reducing staff numbers. In extreme cases, prolonged global instability could even disrupt remittance flows and compound domestic economic stress when expectations are not met.

However, within this difficult environment lies an opportunity. Global instability reinforces an important lesson: Nigeria must reduce its vulnerability to external shocks. Overdependence on crude oil exports leaves the country exposed to geopolitical events thousands of kilometres away. True resilience will come from diversification of the revenue base. The government must accelerate investment in local refining capacity to reduce dependence on imported petroleum products. Strengthening domestic agriculture is critical to reducing food imports and improving food security, but most important ensure security. Supporting small and medium enterprises as well, through access to credit, low-interest loans and infrastructure can stimulate local production and job creation. Fiscal discipline is also essential; any windfall gains from higher oil prices should be saved in stabilisation funds, invested in infrastructure, education, healthcare, and technology, rather than consumed through recurrent expenditure. Strengthening foreign exchange management through improved export diversification, including non-oil exports such as agro-processing, solid minerals, and services, will help stabilise the naira over time.

For businesses, the path forward requires adaptation and sourcing all required resources locally where possible, hedging against currency risks, investing in energy efficiency, and building financial buffers. The era of predictable global markets is over; volatility is becoming the norm rather than the exception.

Ultimately, the unfolding tensions in the Middle East serve as both a warning and a call to action for Nigeria. The warning is clear: as long as the economy remains heavily tied to crude oil exports and imports of essential goods, distant conflicts will continue to shape domestic hardship. The call to action is equally clear: build a more diversified, production-driven, and self-reliant economy. If tensions escalate, Nigeria will feel the shockwaves through higher inflation, higher cost of fuel pump price, currency pressure, and deeper poverty. But if reforms are sustained and strategic investments prioritised, Nigeria can transform global uncertainty into a catalyst for structural change. The future will depend not on whether oil prices rise or fall, but on whether Nigeria uses each episode of global tension as an opportunity to strengthen economic resilience, protect vulnerable citizens, and build a stable foundation for long-term growth and prosperity. Good luck!

How may you obtain advice or further information on the article?

Dr Timi Olubiyi is an expert in Entrepreneurship and Business Management, holding a PhD in Business Administration from Babcock University in Nigeria. He is a prolific investment coach, author, columnist, and seasoned scholar. Additionally, he is a Chartered Member of the Chartered Institute for Securities and Investment (CISI) and a registered capital market operator with the Securities and Exchange Commission (SEC). He can be reached through his Twitter handle @drtimiolubiyi and via email at dr***********@***il.com for any questions, feedback, or comments. The opinions expressed in this article are solely those of the author, Dr Timi Olubiyi, and do not necessarily reflect the views of others.

By Blaise Udunze

The past recurring conflicts on other continents and the current developments in the Middle East are a clear reminder to the world that energy markets are deeply linked to conflict and uncertainty, as experienced across the globe today. The rise in geopolitical tensions with Iran, Israel, and the United States has led to a sudden increase in global crude oil prices. Some individuals may question what business the war has with Nigeria. Economically, yes, as one of Africa’s major oil producers, Nigeria finds itself in a delicate position amid the current global situation. Since it can gain financially when global crude oil prices skyrocket and this is so because the same increase can create economic challenges locally. The price of Brent crude has jumped to $109.18 per barrel, crossing the $100 mark for the first time in more than five years.

The country is getting a temporary fiscal boost, knowing fully well that prices now surpass the benchmark used in the 2026 national budget. The high oil prices gain is further amplified by two major domestic policy shifts, as the first is the removal of fuel subsidy projected to free nearly $10 billion annually for public investment, and a new Executive Order by President Bola Tinubu aimed at boosting oil and gas revenues flowing into the Federation Account by eliminating wasteful deductions allowed under the Petroleum Industry Act. The combination of these developments could significantly increase government revenue over the next few years, but history shows that such windfalls, if not well managed, often go toward short-term spending rather than creating lasting national wealth.

Moreover, our lingering concern today is that Nigeria as a country has experienced this pattern before, and it often brings instability. One of such examples is the 2022 Ukraine conflict, when oil prices spiked above $100 per barrel.

Obviously, during such a period, countries that export oil will suddenly receive a large and sudden increase in revenue from the sale of crude oil. The truth is that if such a windfall is managed well, it can be used to build stronger and diversify their economies beyond oil. Unfortunately, Nigeria has always told a different story as these opportunities were frequently lost to weak fiscal discipline, rising recurrent expenditure, and limited investment in productive assets. The global conflict, in its real sense, could become an opportunity, even though there are risks inherent. Just like any prudent country, Nigeria can use any short-term benefits (like higher oil revenues) to strengthen its economy for the future.

At the heart of this opportunity lies the need for disciplined fiscal management, if the government will tread in line with this call. It is now time for the policymakers to understand that extra money from oil prices should not be wasted, as it has become a tradition to spend through the regular government expenditures. It is high time the government saved and invested the extra funds it gained wisely rather than spending them all immediately. Nigeria’s fiscal vulnerability has often been exposed whenever oil prices fall or global demand weakens. Establishing strong buffers through sovereign savings mechanisms can protect against such volatility. A significant portion of the windfall should therefore be directed into strengthening the country’s sovereign wealth structures and stabilisation funds. This resonates with our subject matter: Can Nigeria convert Oil Windfall into Economic Strength? This rhetorical question is directed to those at the helm of affairs because, by saving during periods of high prices, Nigeria can build reserves that help sustain public spending during downturns without excessive borrowing.

Closely linked to fiscal buffers is the issue of public debt. Nigeria’s debt servicing obligations have continued to rise in recent years, and the current development might be the answer. The debt has continued to place pressure on government revenues and limit fiscal flexibility. Alarming is the fact that the public debt is projected to have surpassed N177.14 trillion by the end of 2026, which is driven by the budget deficit in the 2026 Appropriation Bill.

The truth is that one sensible response to the current situation would be to use some of the unexpected revenue from higher oil prices to pay off loans (debts), especially those with high interest costs. This would reduce future financial burdens on the government and help it spend on development later. The fact is that debt reduction, if the government can quickly address it, also signals fiscal credibility to investors and international financial institutions, thereby strengthening the country’s macroeconomic reputation.

Beyond fiscal stability, Nigeria must recognise that oil windfalls provide a rare opportunity to accelerate strategic infrastructure investment. In today’s world, infrastructure remains one of the most critical constraints on Nigeria’s economic growth. The cost of doing business in Nigeria has been a serious palaver, and it has continued to discourage and scare investment. This is informed by various structural deficiencies, such as inadequate electricity supply and congested transport corridors, as well as weak logistics networks. The question again, can Nigeria convert Oil Windfall into Economic Strength? This is because the truth is not unknown to leaders, but they have continued to deliberately stay away from the fact that channelling windfall revenues into transformative infrastructure projects can therefore yield long-term economic dividends.

Power sector development should be a top priority. Reliable electricity remains the backbone of industrial productivity and economic expansion. Over the years, a well-known fact is that despite various reforms, Nigeria continues to struggle with an epileptic power supply that forces businesses to rely heavily on expensive diesel generators and has posed a double challenge that comes with noise and atmospheric pollution. The nation is tired of the regular audio investment, but strategic investment in power generation, transmission, and distribution infrastructure would significantly reduce operating costs for businesses that translate into manufacturing and encourage new investment across multiple sectors in the country.

Transportation infrastructure also deserves sustained attention, and if nothing is done, the mass commuters will reap nothing but pain. Nigeria’s highways, rail networks, and ports require large-scale modernisation to support efficient trade and mobility. The unexpected extra income from high oil prices, if used carefully for long-term national benefit, can be used to build transport networks that move food and goods from farms and factories to markets and ports. Businesses today are very much dependent on transportation; hence, improved logistics not only facilitates domestic commerce but also strengthens Nigeria’s position as a regional economic hub in West Africa.

Another critical area for deploying oil windfalls is economic diversification. The over-emphasised dependence of Nigeria on crude oil exports has long exposed the economy to external shocks.

Any rise or fall in global oil prices has an immediate impact on Nigeria’s government revenue since oil exports are a major source of government income, foreign exchange availability, and macroeconomic stability follow suit. To break this cycle, Nigeria must invest aggressively in sectors capable of generating sustainable non-oil income and abstain from the unyielding roundtable discussion of diversification without implementation.

With vast arable land and a large labour force, Nigeria has the capacity to become a global agricultural powerhouse; hence, this is to say that agriculture offers enormous potential in this regard. However, productivity remains constrained by limited mechanisation, inadequate irrigation, and poor storage facilities. If the government intentionally invests in modern agriculture and the systems that support it, the country can produce more food, create jobs via agricultural value chains (from production to processing, storage, transportation, and marketing), while earning more from agricultural exporting.

Manufacturing and industrial development represent another pathway to long-term economic resilience, but this sector has been starved of any tangible investment. Unlike Nigeria, countries that successfully convert natural resource wealth into sustainable prosperity typically invest heavily in industrial capacity. The government should be deliberate in using the extra revenues from the high oil prices to invest in building industrial zones, strengthening hubs, and encouraging the transfer of technologies that will fast-track the production of goods within Nigeria, instead of relying on imports. The unarguable point is that the moment Nigeria invests in industries and production of goods locally instead of buying them from other countries, it becomes better able to manufacture and export products that have higher economic value.

One critical aspect that calls for concern is that strengthening Nigeria’s foreign exchange reserves represents another important avenue for deploying excess oil revenues. The truth, which applies to every economy, is that adequate reserves enhance the country’s ability to stabilise its currency during external shocks and support the operations of the Central Bank of Nigeria in maintaining monetary stability, and this part must not be treated with kid gloves. Given Nigeria’s history of foreign exchange volatility, this is another opportunity to know that building strong reserves can significantly improve investor confidence and macroeconomic resilience.

Human capital development must also remain central to any long-term strategy for managing oil windfalls. A country’s greatest asset is not merely its natural resources but the productivity and innovation of its people, and in Nigeria, more attention has been placed on the former. For so long, Nigeria’s budget allocation has told this story, as the government has been glaringly complacent in investing in quality education, healthcare systems, technical training, and research institutions, which can unlock enormous economic potential. If the government aligns with the necessities, Nigeria’s youthful population represents a demographic advantage that can only be realised through sustained investment in human development.

Investment from the higher oil prices should be channelled to the educational sector, and more emphasis should be placed on science, technology, engineering, and vocational skills that align with the demands of a modern economy. Strengthening universities, technical institutes, and research centres can foster innovation, entrepreneurship, and technological advancement. Similarly, improving healthcare infrastructure enhances workforce productivity and reduces the economic burden of disease. Will the government ever shift reasonable investment to these sectors?

Another strategic use of all the categorised oil windfalls is the expansion of social protection systems that shield vulnerable populations during economic shocks. What is unbeknownst to the government is that while infrastructure and industrial investments drive long-term growth, social protection programs help ensure that economic gains are broadly shared. Helping the poor, creating jobs for young people, and supporting small businesses can make society more stable and grow the economy from the ground up.

Lack of transparency and accountability has been anathema that has hindered the progress of growth in Nigeria. The right implementation will ultimately determine whether Nigeria successfully transforms this oil windfall into lasting prosperity. Public trust in government fiscal management has often been undermined by corruption, waste, and non-transparent financial practices. Once there are clear frameworks for managing windfall revenues, this becomes essential. Also, if it is monitored by neutral institutions that are not controlled by politicians, while information about spending is made available to the populace, the media, and the National Assembly supervises how the funds are spent, it will translate to what benefits the country instead of short-term political interest.

A section of the economy that calls for action is the need to improve the efficiency of government institution capacity within agencies responsible for revenue management, budgeting, and project execution. It is a well-known fact that when government institutions are strong and effective, public money is less likely to be wasted, stolen, or misused, and investments produce measurable economic outcomes. This institutional strengthening should include digital financial systems, procurement transparency, and improved project monitoring mechanisms.

Nigeria’s policymakers must immediately put in place clear fiscal rules governing the use of oil windfalls. This will help define how excess revenues are distributed between savings, infrastructure investment, debt reduction, and social programs, and this will also help Nigeria prevent the politically driven spending patterns that have historically undermined effective resource management.

Another question confronting Nigeria is not whether oil prices will rise again in the future, but whether the country will finally break the cycle of squandered windfalls. It is to the country’s advantage that the current crisis has pushed oil prices above the budget benchmark, creating a temporary revenue advantage, but it must be noted that temporary advantages become transformative only when they are guided by deliberate policy choices and long-term vision.

Nigeria possesses immense economic potential. With a large domestic market, abundant natural resources, and a vibrant entrepreneurial population, the country is well-positioned to achieve sustained growth. This potential requires disciplined management of national wealth, particularly during periods of resource windfalls.

The common saying that a word is enough for the wise is directed to policymakers to understand that, if managed wisely, the current surge in oil revenues could strengthen fiscal buffers, modernise infrastructure, diversify the economy, and invest in human capital. The obvious here is that the investments would not only protect Nigeria against future oil price volatility but also lay the foundation for a more resilient and prosperous economy.

The lesson from global experience, as it has always been, is that resource windfalls do not automatically translate into national prosperity. Nigeria’s leaders must understand that, without exception, countries that succeed are those that convert temporary commodity gains into permanent economic assets. Nigeria now stands at such an intersection, which requires turning crisis-driven oil gains into strategic investments; the nation can transform a moment of geopolitical turbulence into an opportunity for lasting economic resilience and national wealth.

Blaise, a journalist and PR professional, writes from Lagos and can be reached via: bl***********@***il.com

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism10 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz3 years ago

Showbiz3 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn