World

COVID-19: BRICS Eyes Deeper Business, Investment Ties

By Kester Kenn Klomegah

On October 28, the BRICS Business Council (Brazil, Russia, India, China and South Africa) during the forum reviewed its joint work for the previous years, discussed at length current business issues and, in particular, tried to choose a path for the future.

Since its establishment, the BRICS Business Council has made its primary task to increase trade and investment among the member countries.

While it has recorded considerable success and positive performance, this year has been different due to the spread of coronavirus. That has not deterred them but rather the BRICS plans to turn the disease-climate into a platform to search for new drivers of trade and economic growth in the subsequent years.

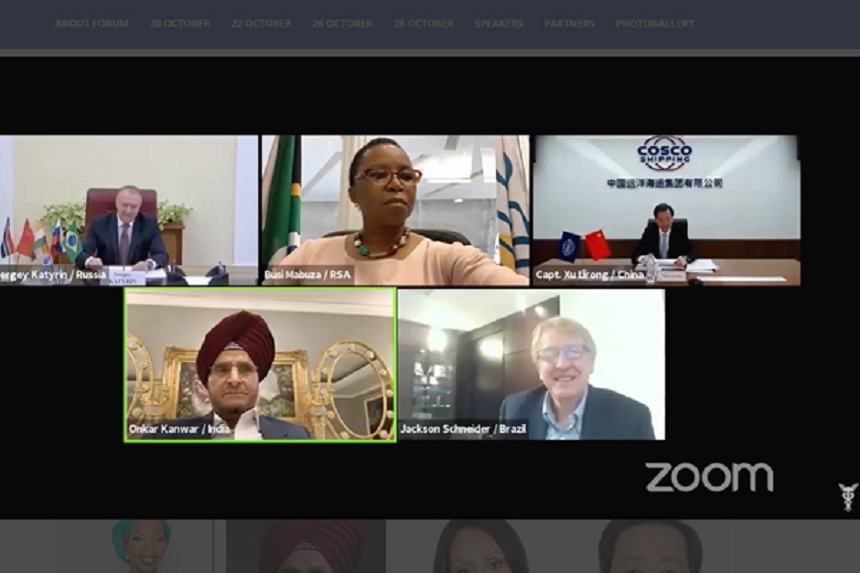

In 2020, Russia holds rotating leadership of the BRICS. Consequently, the meeting was coordinated from Moscow by the head of the Russian chapter of the BRICS Business Council, President of the Chamber of Commerce and Industry of the Russian Federation Sergey Katyrin.

It is worth to explain that the BRICS Business Forum held with the support of the Ministry of Foreign Affairs of the Russian Federation, the Ministry of Economic Development of the Russian Federation and the Ministry of Industry and Trade of the Russian Federation.

Ahead of the opening, Foreign Minister Sergei Lavrov sent a special message of greetings, and Deputy Foreign Minister Sergei Ryabkov addressed the participants.

In his address, Ryabkov noted that by working together, the group could add substantial momentum to the development of trade and investment among members, and in the interests of the population. In assessing the consequences of the pandemic, he urged the group to come up with collective approaches for overcoming them.

“The world economy has entered a recession. Global GDP is shrinking, and so are international trade, investment and demand for key exports. The global value chains are disrupted, while financial markets are in a constant state of turbulence. There are many other problems we face today, and will have to deal with in the future,” he told the participants.

“The crises in the economy and trade could make the world more prone to conflict and seriously undermine international cooperation, further exacerbating the deficit of trust. The gap between the rich and the poor is once again growing. Our common goal is to prevent the most negative scenarios from materializing. Against this unfavourable backdrop, we are witnessing attempts to make a political issue out of the COVID-19 pandemic. We believe that this is the worst thing to do at a time when we need to work together to fend off today’s threats,” Ryabkov pointed out.

According to him, overcoming the economic fallout from the crisis is a priority. In this context, there is the need to focus on restoring the global economy, driving growth and expanding trade, as well as repairing the industrial chains.

He added, “We cannot forget about climate change, sustainable development and the 2030 Agenda for Sustainable Development. I think the BRICS countries will have to look past this horizon to proactively contribute to shaping the long-term global agenda.”

In an optimistic vision for the future, the business community in the five countries has a special responsibility in this regard. Businesses are uniquely equipped to swiftly adapt to a new reality, and create much-needed jobs during major crises like the current one. This is a huge asset. The BRICS governments will continue to support businesses in every possible way. In this context, the BRICS Business Forum and Business Council are essential for devising effective solutions to support micro, small and medium-sized enterprises.

Besides, there were plenary sessions held under the themes COVID-19 and the economic development of the BRICS countries: problems and actions and Challenges and opportunities for sustainable development: pathways to a green economy.

The BRICS countries represent the key economies of their regions and therefore have a special responsibility to develop actions to contain the COVID19 pandemic. They bear the main burden on the development and implementation of a policy of economic recovery from the consequences of the pandemic.

The session “Challenges and Opportunities for Sustainable Development: Pathways to a Green Economy” discussed an agenda for action on climate change and finding ways to sustain economic, industrial and energy development while reducing carbon emissions. The session participants concluded that it is necessary to study carefully the directions of sustainable economic development in the current situation.

Russian Chamber President Sergey Katyrin referenced BRICS Business Forum 2020 as “business marathon” and noted that nine-panel sessions discussed topical areas of cooperation, and these include industry, trade, digital technologies, agriculture, healthcare, energy, ecology and women’s entrepreneurship.

According to forum documents, the three day-forum, both online and offline, brought together about 90 speakers, representatives of government bodies, financial institutions, business and public organizations from all countries of the association. The main topic of the forum this year was “Business Partnership of the BRICS: a Common Vision of Sustainable Inclusive Development” – and that “inclusiveness” refers to the collective efforts to overcome common challenges.

One of the main tasks is updating the Strategy for Economic Partnership of BRICS until 2025, to continue identifying promising directions for developing business cooperation among BRICS countries.

Minister of Industry and Trade of the Russian Federation Denis Manturov highlighted, in particular, some issues of the development of industrial cooperation within the BRICS. The heads of the national parts of the BRICS Business Council – Jackson Schneider (Brazil), Onkar Kanwar (India), Xu Lirong (China), Busi Mabuza (South Africa) – spoke about various issues of interaction and experience in solving urgent problems.

They discussed the impact of the pandemic on industrial production, ways to restore the economies of the BRICS countries, the possibility of digitalization and automation in creating a favourable climate. They also considered the development of women’s entrepreneurship within the BRICS and the role of the Women’s Business Alliance, which began its activities in the year of Russia’s chairmanship in BRICS.

The BRICS Business Council will meet to sum up and approve the annual report on November 10. That will be ahead of the XII BRICS Leaders’ summit scheduled for November 17. The theme of the meeting of the leaders is “BRICS Partnership in the Interests of Global Stability, Common Security and Innovative Growth.”

Russia last chaired BRICS in 2015, held a summit in the provincial city of Ufa. Russia also presided over the group back in 2009, before BRIC turned into BRICS following South Africa’s accession. The five BRICS countries together represent over 3.1 billion people or about 40 per cent of the world population. Kester Kenn Klomegah writes frequently about Russia, Africa and BRICS.

By Adedapo Adesanya

African Export-Import Bank (Afreximbank) has posted a robust financial performance for the 2025 financial year, with total assets and contingencies climbing to $48.5 billion.

This further shows its growing influence in financing trade and development across Africa and the Caribbean.

The Cairo-based multilateral lender, in its audited results released on April 9, reported a 21 per cent surge in total assets from $40.1 billion in 2024, underscoring sustained balance sheet expansion despite global economic headwinds and rating concerns.

Net loans and advances rose by 16 per cent to $33.5 billion, driven by strong disbursements into critical sectors including manufacturing, infrastructure, food security and climate adaptation, areas seen as pivotal to Africa’s long-term economic resilience.

Profitability remained strong, with net income climbing 19 per cent to $1.2 billion, up from $973.5 million in the previous year. Gross income also edged higher by 6.06 per cent to $3.5 billion, reflecting steady revenue growth supported by the bank’s expanding portfolio of trade finance and advisory services.

Afreximbank maintained solid asset quality, with its non-performing loan (NPL) ratio at 2.43 per cent, broadly stable compared to 2.33 per cent in 2024. This performance highlights disciplined risk management even as lending volumes increased across diverse markets.

Liquidity remained a key strength. Cash and cash equivalents rose significantly to $6.0 billion from $4.6 billion, while liquid assets accounted for 14 per cent of total assets, comfortably above the bank’s internal minimum threshold of 10 per cent.

Shareholders’ funds grew 17 per cent to $8.4 billion, supported by the strong profit outturn and fresh equity inflows of $299.4 million under its General Capital Increase II programme. The bank’s capital adequacy ratio stood at 23 per cent, well above regulatory benchmarks, providing a solid buffer for future growth.

Operating expenses increased to $459.2 million from $367.7 million, reflecting staff expansion and inflationary pressures. However, Afreximbank retained cost discipline, with a cost-to-income ratio of 21 per cent, still significantly below its 30 per cent ceiling.

The bank successfully tapped international capital markets, raising over $800 million through Samurai and Panda bond issuances in Japan and China during the year. The move helped counter concerns raised by some rating agencies and reaffirmed Afreximbank’s strong funding access and credibility.

Commenting on the results, Senior Executive Vice President, Mrs Denys Denya, said the performance reflects resilience and strategic execution amid a challenging global environment.

“Despite continuing global geopolitical challenges and disruptions caused by some rating actions, the Group delivered excellent financial performance in 2025,” he said.

He noted that the results cap a decade of transformative leadership under the erstwhile President, Mr Benedict Oramah, with the bank already ahead of most targets under its Sixth Strategic Plan, which runs through 2026.

Mr Denya added that newer subsidiaries, including the Fund for Export Development in Africa (FEDA) and AfrexInsure, are now profitable, contributing to earnings growth and strengthening the group’s diversified structure.

“The Group’s balance sheet is at its strongest level ever, with liquidity levels and capitalisation well above target and good asset quality,” he said.

Afreximbank said it is entering the 2026 financial year with strong momentum, positioning itself to scale impact, deepen trade integration and drive value addition across “Global Africa.”

Return metrics remained stable, with return on average equity at 15 per cent and return on average assets improving slightly to 3.04 per cent, signalling efficient use of capital.

With a fortified balance sheet, rising profitability and sustained investor confidence, Afreximbank said it is firmly on track to consolidate its role as a key engine of trade-led growth across the continent.

By Adedapo Adesanya

Pan-African multilateral financial institution, the African Export-Import Bank (Afreximbank), has approved a $10 billion Gulf Crisis Response Programme (GCRP) to insulate African and Caribbean economies, financial institutions and corporates from the impact of the ongoing Iran war.

The GCRP builds on a series of timely emergency interventions introduced by the lender in recent years, which have helped cushion most economies from the impact of recent shocks such as the commodity shock of 2015/16, the COVID-19 Pandemic of 2020/2021 and the Ukraine crisis of 2023/24.

The latest conflict, which escalated on February 28, 2026, has sent shockwaves through the global economy, with African and Caribbean economies bearing the largest share of the brunt. These impacts specifically affect nations that heavily rely on fuel, fertiliser, and food imports, alongside those exposed to Gulf shipping corridors, investment flows, tourism and remittance inflows.

According to Afreximbank in a statement on Tuesday, GCRP is designed to, among others, sustain essential imports – including fuel, LNG, food, fertiliser, pharmaceuticals – by providing vital short-term Foreign Exchange (FX) and liquidity to support vulnerable member states. It further aims to empower African energy and minerals exporters to capitalise on elevated prices and rerouted trade flows by scaling productive capacity in strategic commodities through pre-export finance, working capital, and inventory financing. Additionally, it provides short-term relief to African and Caribbean member states whose tourism and aviation industries have been adversely impacted by the crisis.

The programme is also designed to build the medium to long-term resilience of African and Caribbean economies against future shocks by scaling productive capacities for producers and exporters of energy, minerals while accelerating the completion of critical energy, port, and logistics infrastructure projects in African and Caribbean member states, delayed by the conflict.

Commenting on the facility, launched on March 31, 2026, Mr George Elombi, President and Chairman of the Board of Directors at Afreximbank, said: “This crisis response programme is in tune with our DNA. We understand how our economies work and the pain points associated with these transitory crises. The programme will support African countries in adjusting smoothly to the crisis while strengthening their resilience to future shocks through interventions that transform the structure of their economies.”

Through GCRP, Afreximbank has already begun taking proactive steps through partnerships with banks and corporates to secure fuel, other energy supplies, fertilisers, and essential food imports, whose supplies have been interrupted by the elongation of the crisis.

Beyond the financing, Afreximbank will spearhead a coordinated regional response in partnership with the UN Economic Commission for Africa (UNECA), the African Union Commission (AUC), the African Continental Free Trade Area (AfCFTA) Secretariat, and the Caribbean Community (CARICOM) Secretariat to strengthen regional coordination on energy security, trade resilience, and supply chain diversification.

By Kestér Kenn Klomegâh

At the plenary session under the theme “Development Through Access to Global Markets” organised during the first International Transport and Logistics Forum held in St. Petersburg, both Russian and African speakers have acknowledged, in their high-quality presentations, the importance of fostering understanding of transport innovations, shifting investment and the possibility of addressing current infrastructure challenges for economic growth.

In promoting comprehensive cooperation in the transport and logistics sphere, Deputy Minister of Transport of the Russian Federation, Dmitry Zverev, stressed that the African continent is one of the fastest-growing regions of the world, demonstrating an average GDP growth rate of 4.5% per year.

According to expert projections, by 2050, Africa’s population will reach 2.5 billion people. To ensure logistical links, it is necessary to build a clear and understandable dialogue with partners, working simultaneously at two levels: at the level of governments, through intergovernmental agreements, and at the level of co-business partnerships. Russian transport corridors guarantee the stability of supplies. Today, there are issues of food security, fertiliser supply and formation of new chains, and other emerging geopolitical challenges facing Africa.

As the guest/main speaker, Zverev explained that Russian companies such as FESCO, RZD, GLONASS and Avtodor are actively involved in this process. This is a unique experience sharing technology and infrastructure solutions in significant volumes. “And frankly, that’s an important image distinction of Russia: we’re not just exporting or selling something – we’re offering technologies and cooperation. Together with technologies, we provide training and prepare national personnel who will work on their transport infrastructure in the future,” asserted Zverev.

Minister of Energy and Infrastructure of the United Arab Emirates, Suhail Mohammed Al Mazrouei, spoke of his country’s decision to invest significant money in the development of its railway infrastructure, with work already underway to connect to Oman by rail and open up new opportunities for freight transportation to Africa and Asia.

“We continue to invest in the development of our country’s logistics network and alternative routes. Russia is an important exporter of raw materials, and development in its regions will contribute to economic growth across the globe. Central Asia is also emerging as a key player, and we are investing in the region’s infrastructure and connecting China to the global economy through Russia and the Middle East,” he said.

Minister Delegate for Maritime Economy of the Ministry of Maritime Economy, Fisheries, and Coastal Protection of the Togolese Republic, Kokou Edem Tengue, spoke of the importance of understanding the African perspective on changing maritime routes as the situation around the Suez Canal and the Strait of Hormuz creates new opportunities for West Africa.

The Port of Lomé, the largest container port in Sub-Saharan Africa, handles approximately 30 million tonnes of goods annually, and its importance for the region is difficult to overstate. “We are actively working with Mali, Burkina Faso, and Niger; the Port of Lomé is a key logistics hub for the landlocked nations of the Sahel,” he said. “It should be noted that Africa relies on chemical fertilisers and grain produced in Russia. We believe that the Port of Lomé could be a part of new sea routes between Africa and Russia.”

In his speech, Minister of Transport of the United Republic of Tanzania, Makame Mnyaa Mbarawa, reported on the active modernisation of the Dar es Salaam port. Previously, the depth of the water was 9–12 meters; now it has increased to 12–15 meters. An increase in the number of operators operating in the port is planned. Thanks to these measures, cargo turnover increased significantly, and ship handling times decreased from 10 days to 2–3. This is an important achievement, after all, speed is a key factor for investors.

However, the port cannot function in isolation; it needs modern rail infrastructure. Tanzania’s government is leading the construction of a new railway to Kigoma, and then into Burundi and south, creating a reliable transportation artery. Dar es Salaam will become a gateway to Burundi, Rwanda, Malawi and Zambia, which depend on cargo flow through this port. Therefore, the development of the port and associated railway is of strategic importance in the region.

“In parallel, the modernisation of the TAZARA railway is going on – a historic artery that requires an upgrade. The private sector is actively involved in this work. After revitalisation, this line will become a key link between Dar es Salaam port and Zambia, he stated. The Government of Tanzania will make every effort to implement these projects and will work closely with the private sector. We invite Russian companies – both state and private – to participate in logistics projects and port infrastructure modernisation.”

As far as road safety in Niger is concerned, the country is facing various challenges that require finding ways to improve the situation, according to the Speaker from Niger, Abdurakhaman Amadou. Within the framework of the discussion, he also noted that an important step was to upgrade the car park and road network. As Niger has no access to the sea, the emphasis is on road traffic to ensure the country’s supply.

“We have access to the port of Lome in the Togolese Republic, which remains neutral towards us. However, the Caton port is closed for us, which created serious difficulties as 80% of our exports and imports passed through it. Recently, the situation has started to improve due to the construction of a railway by Nigeria, which will provide us with access to its ports,” Abdurakhaman informed.

In addition, diplomatic relations with Algeria have been restored after a long hiatus, which opens an exit to the Mediterranean. The conference of Islamic states confirmed the intention to build a grand railway linking Dakar and Djibouti across the entire continent from west to east. This railway will partially pass through Niger, which will be an important step in the development of the region’s transportation infrastructure.

President Vladimir Putin, in a message to participants, organisers, and attendees of the International Transport and Logistics Forum, says that Russia is ready to share its experience through joint science and technology programmes and, of course, by training specialists able to ensure the development of transport and logistics in the 21st century, using a new technological foundation. The Transport and Logistics forum was held for the first time on April 1-3 in St. Petersburg, the second-largest city in the Russian Federation.

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism10 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz3 years ago

Showbiz3 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn