World

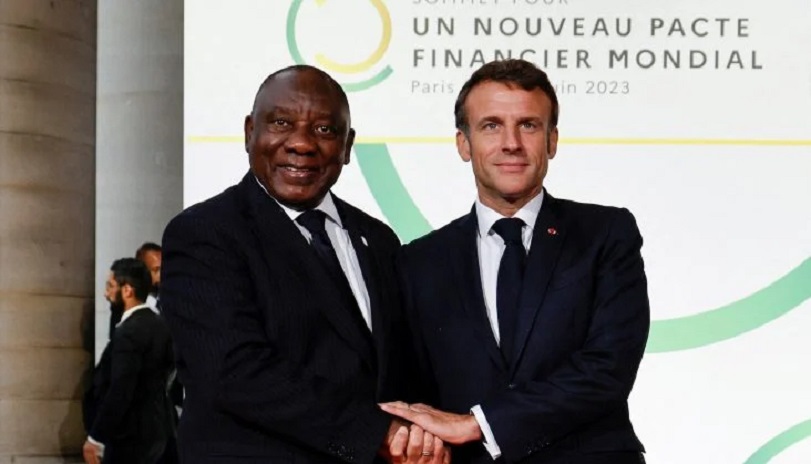

The New Global Financing Pact: Expected Impact on Africa’s Growth and Development

By Kestér Kenn Klomegâh

The Paris Summit on new global financing pact offers some hope for Africa’s development within the context of the geopolitical changes and competition on the continent because extensive investments are needed across various sectors, especially in modernizing its agricultural sector to increase production and value chain.

Increasing agricultural production will help ensure food security and supply necessary raw materials for the industry. The regular collection of raw materials also adds the required value to commodities, thus making them ready for distribution across the continent. This will effectively support establishing a single continental market and promote intra-African trade.

With the rapid changes in the world today, global players are seriously turning their focus on Africa. The central issue is to gain economic influence and further control of the continent’s politics. As already known, the African Continental Free Trade Area (AfCFTA) spans all the states over the following years, and it has the potential to unite more than 1.3 billion people in a $2.5 trillion economic bloc.

It has the potential to generate a range of benefits through supporting trade creation, structural transformation, productive employment and poverty reduction. The AfCFTA opens up more opportunities for both local African and foreign investors from around the world. This is the latest core element or component in post-colonial Africa. It has become the most significant landmark in the history of Africa. We are indeed talking about the official start of this intra-African trading which, of course, signals the commencement of Africa’s journey to market integration.

Those of us in the academia monitoring, researching and analyzing Africa’s development, it beholds again to closely examine the two-day Paris summit, June 22 to 23, and determine the level of its significance and interconnection with this new global financing pact that will benefit Africa. There will be winners and losers; it is both sides of the same coin. African leaders with strategic eyes and brains will become the first and most brilliant beneficiaries; others with the old mindset will only sustain their status as observers and consequently gain nothing for their countries and citizens.

At this point, the summit primarily seeks to rally political leaders and representatives of global financial institutions. The new financing system will address inequality, debt crisis, climate change, international taxes, and special drawing rights. It will be more inclusive and fairer. Therefore, at least, there are solid grounds to rethink the contract between the countries in the Global North and the Global South.

Given geopolitical contradictions and complexities, one more critical point of focus is formulating new pacts and financial modalities to address the current global economic crisis and climate change.

I can only remind you of the global financial institutions. These include the IMF and the World Bank, civil society and the private sector. It will lay the foundation for creating a new global financing system. The new financing system will address inequality, debt crisis, climate change, international taxes, and special drawing rights. It will be more inclusive and fairer.

Most of their conditions are usually unfavourable to many creditors; however, much again depends on the crediting countries’ implementable policies, approaches and economic goals. At this point, we must ponder a few questions: How does the summit fit into a global context defined by the sweeping consequences of persistent economic, climate, health and energy crises, mainly in the most vulnerable countries? What do we expect from the summit, and what next after all these?

Objectives for the Paris Summit: Catherine Colonna, the French Minister of Europe and Foreign Affairs, in a statement on January 6, 2023, noted that the Paris Summit would focus on building a new pact with a Global North and a Global South. According to her, the new arrangement would facilitate vulnerable countries’ access to the necessary finance to address the effects of the current and future crises.

On the same day, the Secretary of State for Development, Francophonie and International Partnerships, Chrysoula Zacharopoulou, and the Permanent Representative of France to the OECD, Amélie de Montchalin, took part in a webinar arranged by the Finance for Development Lab on the issues at stake at the Paris Summit 2023.

In November 2022, on the sidelines G20 Summit and the conclusion of a COP27 Summit with mixed results, French President Emmanuel Macron called for a global conference in Paris in June 2023. Macron announced that the Paris Summit would take stock “of all means and ways of increasing financial solidarity with the Global South.”

Emmanuel Macron’s announcement happened in a particular global context. The climate change crisis particularly threatens the Global South countries, including island states. Thus, the Barbados Prime Minister, Mia Mottley, has led an initiative to finance climate action since COP26. The “Bridge Initiative” focuses on facilitating access to global financing for the countries most vulnerable to climate change. The funding allows them to respond better to climate challenges.

Macron’s announcement aligns with the Bridgetown Initiative. However, the Paris Summit will deliberate on financing issues beyond the climate question, including the fight against poverty. The Covid-19 pandemic, the Ukrainian conflict, and the accompanying consequences have massively shrunk the budgetary and fiscal space for many countries, including Africa. This has affected their ability to finance citizens’ access to basic social needs and services. Consequently, the UNDP observed a human development decline in nine out of ten countries globally in 2022. The fall has mainly come from increased poverty levels and a drop in life expectancy.

AfDB president Dr Akinwumi Adesina will moderate a roundtable discussion about the Alliance for Green Infrastructure in Africa at the Summit for New Global Financing Pact. Seven heads of state will join Akinwumi Adesina. Islamic Development Bank Chairman Muhammad Al Jasser and the European Investment Bank President, Werner Hoyer, will also attend.

The Alliance represents a program by the African Union Commission, the AfDB, and Africa50 with other partners. The platform allows African nations to partner with the private sector to raise $500 million in early-stage combined finance capital. This will catalyze up to $10 billion in green and climate-resilient programs and projects. Its eventual goal is to hasten a transition to net-zero emissions by Africa and for Africa.

The event will promote AGIA as an influential platform. AGIA could accelerate and scale funding Africa’s transformational climate-resilient and greener infrastructure projects to attract new financiers and partners. It will also provide a progress update on the Alliance’s activities since its launch at COP27. The June 22-23 Summit for a New Global Financing Pact is one to anticipate. Many of the deliberations and expected outcomes will no doubt benefit the majority of African nations.

With six round tables, 30 branded events and 50 parallel events and deliberations, there will be a final declaration and communique. Leaders have registered their participation, including the President of Mozambique, Filipe Nyusi, Prime Minister of Barbados, Olaf Scholz, Luis Inacio, the President of Brazil, Lula Da Silva, Germany Chancellor Mia Mottley, Chinese Premier Li Qiang, and US Treasury Secretary Janet Yellen.

Several representatives of international organizations, activists, and philanthropists will also attend. They include AfDB President Akinwumi Adesina, Word Bank President Ajay Banga, UN Secretary-General Antonio Guterres, the European Commission President Ursula Von der Leyen, UN Goodwill Ambassador and activist Vanessa Nakate, co-founder of the Bill & Melinda Gates Foundation and philanthropist Melinda French Gates, among others.

A high-level international steering committee composed of states and international organizations oversees the Paris Summit preparations. It includes France, South Africa, Senegal, the United Arab Emirates, the United Kingdom, the United States, Germany, Barbados, Brazil, Japan, China, India, the United Nations Secretariat, the European Commission, the OECD, the World Bank and the International Monetary Fund.

Civil society campaigns: Ahead of the Summit for a New Global Financing Pact in Paris and the confines of multilateral development bank reforms, the Pandemic Action Network and 19 institutions from around the globe have issued a rallying call for the inclusion of pandemic debt relief clauses in new country lending agreements.

In summary, we expect the summit formulates proposals for innovative financing sources, particularly those from the multilateral development banks. This will ultimately benefit developing countries, including those in Africa. Further, the international institution’s interventions will effectively address and reduce or minimize the vulnerability of economic shocks due to global instability from the pandemic and Russia-Ukraine crisis. We equally expect some reforms in the global financial infrastructure to create a just, sustainable and equitable world.

By Kestér Kenn Klomegâh

In an interview, Senator Mushahid Hussain, President of Pakistan-Africa Institute for Development and Research (PAIDR), explicitly offers a few important insights into the US-Israeli war on Iran and its implications for BRICS+ and Africa. Here are the interview excerpts:

What’s your interpretation of the US-Israel war on Iran, in the context of developments in the Middle East region?

The US-Israel illegal and unwarranted war on Iran was spearheaded by [Benjamin] Netanyahu (Prime Minister of Israel) and actively supported by [Donald] Trump (President of USA) as a Joint Operation with three fundamental goals: a) decimate the Islamic Revolutionary Regime; b) reshape the Middle East as part of Zionism’s ‘Greater Israel’ Project; c) preclude any possibility of establishing a Palestinian State with Jerusalem as its capital.

What is your assessment of Iran’s joining BRICS+ in 2025, China’s and Russia’s roles as members of this association, in this US-Israel war with Iran?

China and Russia have played, by and large, a low-key diplomatic role in supporting Iran but without any active political initiatives. BRICS is divided from within, as India is keen to curry favour with the USA and avoids close association with BRICS since the time that Trump attacked BRICS last year. But China & Russia are clear political beneficiaries of the war as American prestige is at an all-time low, having got entangled in an unwinnable war, resulting in weakening of the US ‘sole superpower’ image.

As an Asian expert, how would you characterise Africa’s reactions? And do you think that reactions were objectively authentic, basing perspectives broadly on Arab and Middle East contributions to Africa’s development?

Africa’s reactions to the war are primarily through the prism of the Global South, viewing Iran as resisting American-Israeli hegemonic designs, as, for example, manifested in two examples: South Africa’s rejection of American pressures to wean South Africa away from its support for Iran. Plus, Somalia joined Pakistan and China in supporting the Russian resolution in the UN Security Council seeking an immediate ceasefire and negotiations to halt the War, despite strident Western/US opposition to the Russian resolution.

By Adedapo Adesanya

The Director-General (DG) of the World Trade Organisation (WTO), Mrs Ngozi Okonjo-Iweala, has said the global trading system is experiencing the worst disruptions in the past 80 years.

The trade body chief warned about the consequences as the WTO ministerial conference opened Thursday in Cameroon.

“The world order and the multilateral system we know has irrevocably changed,” she said, adding: “We cannot deny the scale of the problems confronting the world today.”

The organisation’s 166 members appear deeply divided as trade ministers gather in the Cameroonian capital for the WTO’s top conference, amid global economic turmoil linked to the Middle East war.

Over four days in Yaounde, WTO members will try to revitalise an institution weakened by geopolitical tensions, stalled negotiations, and rising protectionism — against the backdrop of the war in the Middle East, which poses a serious threat to international trade.

“The scale of the problems confronting the world today, even before the conflict in the Gulf, destabilised trade in energy, fertiliser and food,” Mrs Okonjo-Iweala said.

“National governments and international institutions alike have been struggling to navigate rising geopolitical tensions, intensifying climate pressures, and rapid technological change.

“Accompanying these shifts has been an increasingly loud questioning of multilateralism,” she added.

Mrs Okonjo-Iweala said these disruptions were just one symptom of broader upheavals shaking the international order created after World War II to prevent a repeat of the disasters of the first half of the 20th century.

“It feels appropriate that at the moment when the world is in turmoil with conflict in the Middle East, Sudan, Ukraine, and elsewhere, at this time of great disruption and uncertainty, we have gathered in Africa to discuss the road ahead for the global trading system,” she said.

“Africa is the continent of the future.”

WTO ministerial conferences are typically held every two years. The current edition in Yaounde is the second to be held in Africa, after Nairobi (Kenya) in 2015.

By Kestér Kenn Klomegâh

The United States-Israeli war in the Islamic Republic of Iran is shattering Africa’s economic landscape and leaving emotional devastation. Europe is fractured, but completely. France has taken the initiative to create a platform in Nairobi, the capital of Kenya, located in East Africa. More than 2,500 corporate executives from across the continent, spanning 55 African countries, would take up the challenge during a two-day in-depth discussion on the existential threat of the Middle East conflict. Participating business leaders’ engagement over geopolitics, finding new paths to massive new investment, would be the central theme, while expressing commitment to forge new mechanisms for economic cooperation between Africa and France. The high-ranking guests from regional economic blocs are expected to join, teaming up to share practical thoughts and build awareness beyond the current Middle East conflicts and their impact on Europe and Africa.

The common goal: new perspectives on innovation, new business directions in the context of geopolitical threats. Based on Africa’s untapped natural resources and human capital, communicating clearly with business executives and political leaders, high-ranking speakers plan to dissect and design the future. Strengthening Africa’s and France’s economic cooperation forms the irreversible target and will ultimately be incorporated into the conference declaration. Cautious reflection indicated that the relationship between Africa and France is still pragmatic, as both agreed to renew and thoroughly review the existing economic potentials at the two-day conference in Nairobi.

Experts and Conference coordinators told this article’s author that the French government and business circles involved in trade and economic cooperation with African countries were invited to participate, lay out their comprehensive business architecture. Africa and France will focus on the developing manufacturing and extractive industries, setting up special economic zones, energy and transport infrastructure, digitalisation, and the agro-industrial complex—education and training in the sphere of entrepreneurship.

France has already worked out a financial mechanism to support joint business across Africa, while Africa’s financial institutions pledge their commitment, plan corporate strategies and support for joint investments in the localisation of production chains in Africa, which covers both agricultural and mineral processing.

President William Ruto and French President Emmanuel Macron both acknowledged that the strategic pathway should focus on unlocking Africa’s potential, driving sustainable industrialisation, and targeting economic growth across Africa. Harnessing the untapped resources and utilising the huge human resources is France’s priority in consolidating the current bilateral engagement and collaboration.

In a statement, President Ruto underlined tthat he summit reflects a shared commitment to strengthening bilateral ties and deepening multilateral cooperation to advance global goals. The agenda will focus on key areas, including reform of the international financial architecture, energy transition, green industrialisation, the blue economy and connectivity, artificial intelligence, sustainable agriculture, and health. It will spotlight the role of young entrepreneurs, civil society, and international organisations in shaping solutions to pressing global and regional challenges. The May summit is described as part of the renewal of relations between France and Africa, emphasising genuine partnerships and shared progress.

The agenda will focus on key areas, including reform of the international financial architecture, energy transition, green industrialisation, the blue economy and connectivity, artificial intelligence, sustainable agriculture, and health.

In addition to the May summit by France, the European Union countries are increasingly strong economic partners for many African countries. It therefore beholds African leaders and business people to necessarily explore available possibilities and windows that have been opened. The EU has unveiled €300 billion ($340 billion) alternative to China’s Belt and Road initiative — an investment programme the bloc claims will create links, not dependencies.

In an official document, it said the European Commission is examining:

– Support AfCFTA implementation and the green transition;

– Improve trade and investment climate between the EU and Africa;

– Reinforce high-level public-private dialogue;

– Enhance long-term dialogue structures between the EU and African Business Associations;

– Unlock new business and investment opportunities, including in the areas of manufacturing and agro processing, as well as regional and continental value chains development.

It is further included in the joint communication of the European Commission (EC) entitled “Toward a Comprehensive Strategy with Africa”, which sets forth what the EU plans with Africa. The Joint EU-Africa Strategy takes into cognisance the most common interests such as climate change, global security and the achievement of the United Nations Sustainable Development Goals (SDGs).

Just as China, India and the United States, so also France, and other European countries are exploring emerging opportunities offered by the African Continental Free Trade Area (AfCFTA), which provides a unique and valuable access to an integrated African market of 1.5 billion people. In practical reality, it aims at creating a continental market for goods and services, with free movement of business people and investments in Africa.

Looking ahead, France intends to capitalise on Africa’s most transformative economic sectors and make strategic moves by collaborating, as a mutual partnership remains dynamic and adaptable. Despite growing geopolitical tensions, France’s approach and its long-standing ties still offer an alternative partnership model that many African leaders find very appealing.

The challenge for the future will be to ensure these ties evolve in ways that serve Africa’s development needs, while navigating the increasingly complex global politics. As Africa is indiscriminately open for business, on May 11-12, 2026, African and French Heads of State and Government meet together to chart a new path for innovation, growth, and cooperation. Kenya will hold this investment summit for France to position Africa as a key partner in global innovation and economic development while strengthening bilateral ties with France and advancing Africa’s collective agenda on the international stage.

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism10 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz3 years ago

Showbiz3 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn