World

Amid Russia-Ukraine Crisis, Trans-Saharan Gas Pipeline Offers Hope for Europe

By Kestér Kenn Klomegâh

Europe is still looking for reliable alternative sources of energy especially gas, as its energy relations fell nosedive with Russia. It has been exploring energy sources from the Asian region down to Africa. But while African energy sources exist, it largely lacks the infrastructure to transport it up to Europe. And transporting gas would have to go across borders which requires some kind of regulations and clearance agreements between the African countries.

The Trans-Saharan gas pipeline (also known as the NIGAL pipeline and Trans-African gas pipeline) was first proposed back in the 1970s. The inter-governmental agreement on the pipeline was signed by the Energy Ministers of Nigeria, Niger and Algeria on 3 July 2009 in Abuja. It has not materialized, among many factors, due to lack of finance and multiple complicated government bureaucracy. But Europe’s demand is pushing for fixing some solutions and resolving obstacles to realize this project.

Nigerian authorities said that Russia’s Gazprom has negotiated with Nigeria about its possible participation in the project. Experts described this interest as a business strategic step to gatekeep and control the flow of gas from Africa into Europe. Russia would be interested in tactically delaying the project. Its aim is to be the leading supplier, and any other competitors must be placed under tight monitoring and control.

Charles Robertson, Global Chief Economist at Renaissance Capital, questioned in an email discussion how Russia can heavily invest in Africa’s energy sector, especially in the exploration and production of oil and gas to be exported to Europe.

“Russia or Kazakh oil competes with Libyan, Angolan or Nigerian oil. Russia or Kazakh gas competes with Algerian or Egyptian gas. Russia can supply food – but that’s mainly needed by north Africa,” he wrote, and concluded: “By forging strong cooperation, the European Union (EU) has more of the industrial machinery that Africa might need to industrialize, although Chinese machinery may be more appropriate for the technical level of industry in Africa.”

Russian companies have exited mega-projects in Zimbabwe, and also went out from Botswana, Cameroon and Sierra Leone. Russians were not chosen after the project bidding process in Mozambique. There are, therefore, other reliable potential foreign corporate investors such as Indian company GAIL, France’s Total S.A., Italy’s Eni SpA and Royal Dutch Shell have expressed interest in participating in the project.

Differences exist though. According to the Algerian Energy Minister Chakib Khelil – “only partners that can bring something to the project, not just money, should be there. On the other side, Energy Ministers of Algeria and Nigeria have said that “if things go well, there will be no need to bring international oil companies into the project” and “if the need for partnership in the project arises, not every partner will be welcome on board on the project.”

Mahamane Sani Mahamadou, Minister of Petroleum for the Republic of Niger; Mohamed Arkab, Minister of Energy and Mines, Algeria, and Chief Timipre Sylva, Minister of State for Petroleum Resources of Nigeria as well as the Director Generals of National Oil Companies (NOCs) of the three African countries held thorough discussions on the implementation of the multi-billion Trans-Saharan Gas Pipeline (TSGP) in June 2022, in Abuja, capital of the Federal Republic of Nigeria.

According to reports, a Steering Committee made up of the three Ministers and Director Generals of the NOCs, established during the two-day meeting, will be responsible for updating the feasibility study for TSGP and will meet at the end of July 2022 in Algiers to discuss how to progress with the TSGP project.

The Ministry of Petroleum of Niger commends all parties for this significant step, viewing both the establishment of the taskforce and roadmap as key drivers towards making the TSGP a reality. With energy poverty increasing across the African continent due to limited investments in energy projects, delays in exploration, production and infrastructure rollout, the Covid-19 pandemic and global energy transition-related policies, the TSGP project will bring in a new era of energy reliability for Africa.

With the 4,128 km pipeline running from Warri in Nigeria to Hassi R’Mel in Algeria via Niger, the pipeline will not only create a direct connection between Nigeria and Algeria’s gas fields to European markets but will bring significant benefits to Niger.

With over 34 billion cubic meters of gas, Niger, in its own rights, also has the potential to become a gas exporter, and with Europe expanding energy ties with Africa, the TSGP project will mark a new era of improved regional cooperation in Africa, enhancing gas monetization and exports while scaling up Niger-exports to Europe via Algeria.

Meanwhile, with the pipeline making headway, opportunities for the country to increase domestic gas utilization on the back of new reserves from Niger and Nigeria have arisen. With Niger seeking to improve electricity access and ensure energy affordability through increased exploitation of gas, the TSGP initiative will be a game-changer.

The pipeline will enable up to 30 billion cubic meters of natural gas to be traded yearly enhancing regional and international energy trade, enabling Niger to expand the role of natural gas in its energy mix and address energy poverty.

The efforts of Afreximbank for the creation of an African Energy Bank is a huge testimony of how Africa can enhance cooperation and leverage domestic solutions to optimize its oil and gas market, notes Sebastian Wagner, Executive Chair of the Germany Africa Business Forum. “What we want to see is African financiers rallying towards supporting the rollout of TSGP. Increased oil and gas exploration, production and assets development is what will bring Africa out of energy poverty by 2030,” Wagner acknowledged in comments.

With gas emerging as the energy of the future, the $13 billion TSGP projects could lead to socioeconomic growth by unlocking massive investments across the energy sector. It will simultaneously help create jobs in various industries including energy, petrochemicals and manufacturing whilst optimizing energy production and positioning Africa as a global energy hub.

The pipeline will start in the Warri region in Nigeria and run north through Niger to Hassi R’Mel in Algeria. In Hassi R’Mel the pipeline will connect to the existing Trans-Mediterranean, Maghreb–Europe, Medgaz and Galsi pipelines.

These supply Europe from the gas transmission hubs at El Kala and Beni Saf on Algeria’s Mediterranean coast. The length of the pipeline would be 4,128 kilometres (2,565 mi): 1,037 kilometres (644 miles) in Nigeria, 841 kilometres (523 miles) in Niger, and 2,310 kilometres (1,440 miles) in Algeria.

Reports say the pipeline is to be built and operated in partnership between the NNPC and Sonatrach. The company would include the Republic of Niger. Initially, NNPC and Sonatrach would hold a total of 90% of the shares, while Niger would hold 10%.

The annual capacity of the pipeline, previously estimated at US$10 billion, would be up to 30 billion cubic meters of natural gas. The pipeline was originally expected to be operational by 2015. In the year 2019, the project is still in the prospecting phase. Now, it is unknown what next as there are also safety concerns about the project itself and the future practical operations.

Nigeria, Niger and Algeria are among the least secured areas in the region because of various active terrorist movements that destabilize all technical processes and construction of gas pipelines across Africa. However, the Trans-Saharan gas pipeline is still seen as an opportunity to diversify the gas supplies to the European Union.

By Adedapo Adesanya

Credit ratings agency, S&P Global Ratings, has restored the African Export-Import Bank (Afreximbank) to investment grade, nearly 12 years after its last assessment, citing the entity’s countercyclical lending record and strong shareholder support.

The BBB+ rating with a stable outlook is one notch above Moody’s Baa2 and comes months after Afreximbank severed ties with Fitch Ratings.

The lender accused the agency of misjudging its mission, following a downgrade to junk status amid disagreements over the bank’s role in debt restructurings for Ghana and Zambia. Fitch subsequently withdrew its ratings entirely and flagged governance concerns.

S&P said in a statement on Thursday that Afreximbank’s record as a countercyclical lender and its substantial shareholder support served as rationale for its rating. Credit ratings often guide the costs of capital for a borrower.

The lender’s total assets, S&P noted, had expanded to $42.3 billion by the end of 2025, up from $7.1 billion in 2015.

S&P said it did not incorporate preferred creditor status into its assessment because Afreximbank provides almost 80 per cent of its loans to private-sector entities.

However, it acknowledged that Afreximbank, alongside other institutions, had experienced prolonged payment arrears in recent years, notably following the defaults and debt restructurings in Ghana and Zambia.

S&P noted that Afreximbank said in December that it had come to an agreement with Ghana on its $750 million loan, but that the lender had not announced a resolution with Zambia.

The agency warned that further sovereign restructurings could weigh on Afreximbank’s asset quality.

S&P’s assessment described Afreximbank’s governance and management as “adequate”, saying the inclusion of two independent directors and the African Development Bank (AfDB) as a permanent board member provided institutional oversight.

It noted that while increasing participation of private-sector investors through Class D shares could influence the bank’s risk appetite, Class A shareholders retained veto rights over big institutional changes, balancing potential risk.

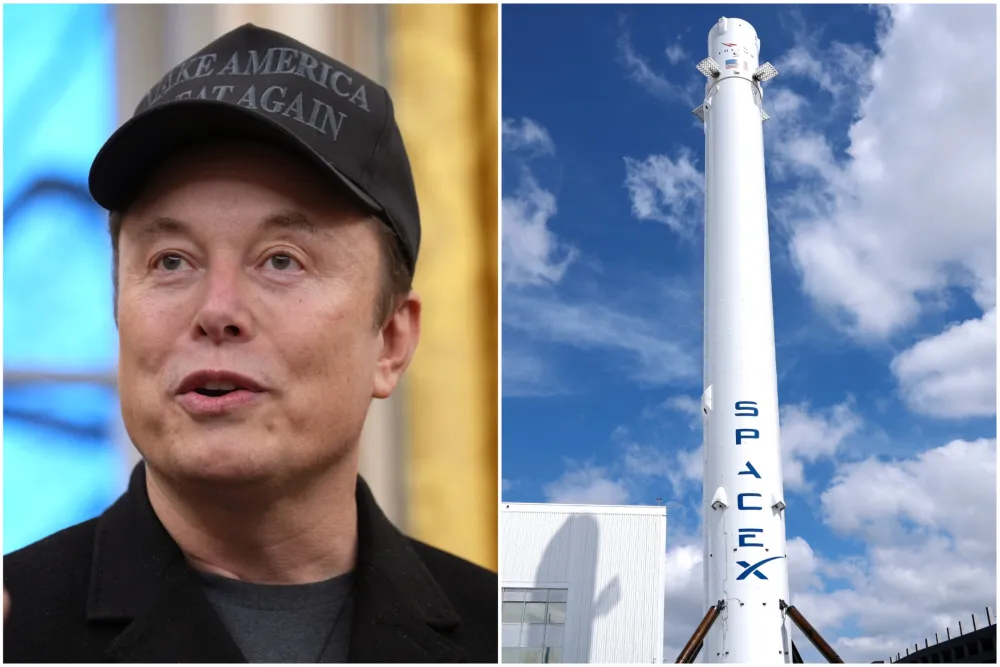

By Adedapo Adesanya

Mr Elon Musk, the world’s richest man, is now a trillionaire as his SpaceX rose 11 per cent in its Nasdaq debut on Friday, lifting its valuation to about $1.96 trillion as investors piled into the world’s largest initial public offering (IPO).

The stock opened for trading at $150 compared with the IPO price of $135 per share.

The landmark listing cemented Mr Musk’s status as the first trillionaire ever and propelled SpaceX into the ranks of the world’s most valuable companies

The listing is being used as a benchmark of what is to come for the market ahead of forthcoming IPOs for AI heavyweights Anthropic and OpenAI.

The record IPO is a culmination of Mr Musk’s long-held ambitions in space and technology.

Most of Musk’s wealth now rests with SpaceX, where he holds a stake worth roughly $866 billion. Along with Tesla and the rest of his properties, his net worth will exceed $1.1 trillion when the stock begins trading on Friday.

At a quoted $75 billion, the deal’s proceeds were more than double those of Saudi Aramco’s record-setting 2019 IPO.

The valuation could rise further should underwriters exercise their right to sell additional shares, a decision typically made within 30 days after the offering.

Although SpaceX may have to wait for entry into the S&P 500, its expected fast-track inclusion in the Nasdaq 100 will soon make it a major holding for passive funds and ETFs that track the index, creating a fresh source of demand for its shares.

It will take about a month before it gets added to that index under Nasdaq’s new fast-entry rules, as opposed to a typical wait of as much as a year.

SpaceX said its market opportunity spans $28.5 trillion, a figure it called the largest in human history.

Mr Musk, 54, was born in Pretoria, South Africa, to a Canadian mother and South African father. He attended the University of Pennsylvania, graduating in 1997.

He took over as Tesla’s CEO in 2008. Beyond Tesla and SpaceX, Mr Musk has co-founded five other companies, including tunnelling startup The Boring Company and brain implant maker Neuralink.

By Kestér Kenn Klomegâh

Under the presidential decree, authorising an initiative to tap the best brains and professionals from abroad to integrate into Russian society, the Agency for Strategic Development plans to hold its first Bridge Awards, which honour the contributions of foreign citizens and repatriates who have made a definitive life choice in favour of Russia. The Bridge Awards was founded by entrepreneur Philip Hutchinson and public figure Guy Eames.

Launched in February 2026, the competition for the awards has attracted a lot of potential candidates from more than 40 countries competing for victory across 12 categories. The highest number of applications came from the United States, totalling 18. There are also a number of candidates from Europe, Asia, and Africa. The “Business” category proved to be the most geographically diverse, drawing applicants from 12 countries.

The Bridge Awards recognise the valuable contributions of foreign citizens and repatriates to the Russian society. It is also dedicated to raising awareness, recognising achievements, and building strong connections with the international community.

According to the official reports made available, among the winning applicants and world-renowned celebrities for the Business Category were Sammy Manoj Kotwani, President, Indian Business Alliance; President, SITA/Indian National Cultural Centre; President, Overseas Friends of BJP Russia; and Founder, Imperial Tailoring Company.

In this conversation, Sammy Kotwani talks about how he has lived and worked in Russia for more than three decades, his entrepreneurial achievements, and his contributions to Russian society. Here are the interview excerpts:

What really motivates you to participate in the first competition for Bridge Awards?

For me, the Bridge Awards are not only a competition. They are a recognition of a life journey. I have lived and worked in Russia for more than three decades. Russia gave me the opportunity to build my business, serve the Indian community, promote Indian culture, and create real business connections between India and Russia.

My motivation is very simple: I want to show that a foreign citizen can love Russia, respect its people, contribute to its economy, and at the same time remain deeply connected to his own roots and motherland.

Through the Indian Business Alliance, through cultural activities, through India–Russia business forums, through meetings with governors and regional leaders, my work has always been to build bridges — not only between governments, but between people, entrepreneurs, regions, cultures, and families.

So, when I heard about the Bridge Awards, I felt that this platform represents exactly what I have tried to do for many years: turn friendship into action, and respect into real cooperation.

You were selected by the Jury for the business category. What are the implications of this category?

Being selected in the business category is a very meaningful honour because business is where friendship becomes practical.

India and Russia already have strong political trust, historic goodwill, and a strategic partnership. But the real question today is: how do we convert this goodwill into trade, investment, joint ventures, logistics solutions, industrial cooperation, and regional development?

That is why the business category is important. It recognises those who are not only speaking about cooperation, but actually working on the ground to make it happen.

For me personally, it reflects the work of the Indian Business Alliance in connecting Indian entrepreneurs with Russian regions, supporting business missions, encouraging investment, discussing opportunities with governors, and identifying practical sectors such as textiles, pharmaceuticals, logistics, food processing, energy, technology, education, tourism, and skilled manpower.

This category is not only about personal achievement. It is about responsibility. It means we must continue to create platforms where Indian and Russian businesses can meet, trust each other, and build long-term partnerships.

Do you think the “Time to Live in Russia” programme has good future prospects for foreign citizens who choose to relocate and live in Russia?

Yes, I believe the “Time to Live in Russia” programme has strong future potential, provided it remains practical, transparent, and welcoming.

Many foreign professionals, entrepreneurs, investors, teachers, doctors, engineers, cultural workers, and skilled specialists are looking for countries where they can build a meaningful life. Russia has space, resources, education, culture, business opportunities, and strong regional potential.

But relocation is not only about visas or documents. A person who comes to Russia needs guidance, integration, language support, business orientation, community support, and confidence that he or she can build a stable future.

This is where such a programme can become very powerful. If it helps talented foreigners understand Russia better, settle smoothly, respect Russian society, and contribute to the economy, then it can become a serious instrument of international cooperation.

From the Indian perspective, I see strong potential. Many Indians are skilled in technology, medicine, education, trade, textiles, pharmaceuticals, engineering, hospitality, and entrepreneurship. If the right mechanism is created, India and Russia can benefit greatly from this human bridge.

How would you characterise the International Bridge Awards by the Agency for Strategic Initiatives and decreed by President Vladimir Putin?

I would characterise the Bridge Award as a timely and visionary initiative. In today’s world, countries need more than formal diplomacy. They need people who understand both sides, who can translate culture into trust, and trust into practical cooperation.

The Bridge Award gives recognition to such people — foreign citizens and repatriates who have chosen Russia not only as a place to live, but as a place to contribute.

For me, this award carries a very important message: Russia values those who sincerely work for its development, its international friendships, and its multicultural society.

The involvement of the Agency for Strategic Initiatives gives the award a serious institutional direction. It shows that this is not just a symbolic gesture, but part of a larger vision — to make Russia a place where international talent, entrepreneurs, cultural leaders, and public figures can participate in national development.

I believe this award can become a powerful platform for public diplomacy. It can show the world that Russia is open to sincere partners, serious professionals, and people who are ready to build, not just observe.

For me, as an Indian who has lived in Russia for many years, the word “bridge” is very personal. A bridge connects two banks. It allows people to cross, meet, understand, and build together. That is exactly what India and Russia need today—more bridges, more trust, more implementation, and more human connection.

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism10 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz3 years ago

Showbiz3 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn