Banking

How FairMoney is Powering the Next Generation of Nigerian SMEs

By James Edeh

SMEs are widely regarded as the engine of economic growth. According to the Small and Medium Enterprises Development Agency of Nigeria (SMEDAN), in 2025, Nigerian SMEs continued to anchor the economy, representing approximately 96% of all businesses. These enterprises contributed over 48% to Nigeria’s GDP and accounted for between 84% of total employment. However, while the vast majority of SMEs play a vital role in national development, only a small minority have access to formal credit or the financial literacy required to scale and meet eligibility requirements.

FairMoney Microfinance Bank (MFB), a leading technology-enabled bank in Nigeria, is supporting national financial inclusion objectives and bridging the gap by providing solutions that directly assist small and medium-sized enterprises (SMEs). It does this not only by providing access to financing but also by offering efficient payment processing options that help SMEs scale up financially.

Access to Capital

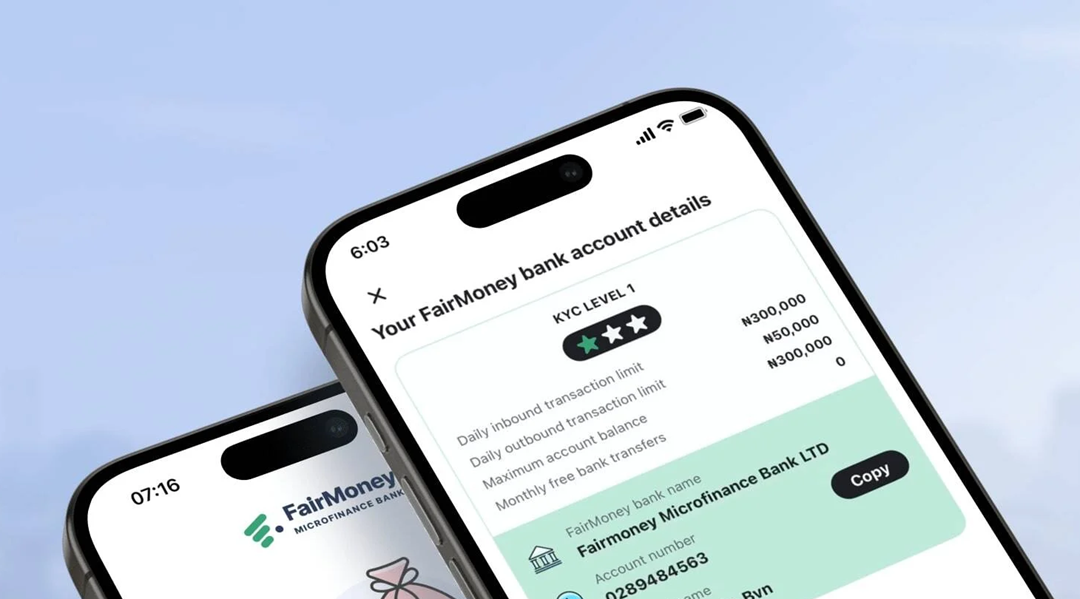

Securing a loan through FairMoney MFB offers a streamlined path for Nigerian SMEs to transform potential into performance. By prioritising digital speed and accessibility, the microfinance bank enables eligible business owners in Nigeria to secure up to ₦5,000,000 without physical collateral; however, access remains subject to credit assessment. This rapid disbursement creates a real opportunity for entrepreneurs to act on time-sensitive growth prospects, whether that means restocking inventory ahead of a peak season, fulfilling a sudden large-scale order, or upgrading essential equipment. To improve their eligibility for higher loan amounts, SMEs simply need to increase their engagement with the FairMoney ecosystem; banking and managing finances directly through the app after an initial application using their BVN and business details.

Beyond the Bank Statement

Alternative credit scoring is the engine that allows FairMoney MFB to leverage broader data sets to better inform credit decisions for a wider range of SME customers. FairMoney MFB doesn’t just look at a bank statement; it looks at potential. By utilising Alternative Credit Scoring powered by advanced data analytics and machine learning, FairMoney MFB assesses creditworthiness based on non-traditional data, such as app usage patterns, transaction velocity, and digital footprints – with customer consent and in accordance with Nigerian data protection requirements. This approach opens the door for businesses with limited formal financial histories to access real growth opportunities that were previously out of reach. For the Nigerian SME, this presents the opportunity to scale from small-scale survival to ambitious expansion, securing the funding necessary to innovate and compete based on the real-time strength of their operations.

Smarter Savings

True business growth requires a shift from simple borrowing to disciplined wealth management, and FairMoney MFB empowers SMEs with a suite of specialised products designed to ensure their capital works as hard as they do. Through FairTarget, entrepreneurs can define specific financial milestones, such as purchasing equipment or securing a larger office, and automate their progress toward reaching them. For operational liquidity, FairSave offers a high-interest savings account where funds remain accessible while earning daily interest, while FairLock provides long-term stability by allowing businesses to secure surplus funds at premium interest rates, protecting capital from impulsive spending. Together, these features transform FairMoney MFB from a lender into a comprehensive financial partner to SMEs that fosters both immediate scalability and long-term fiscal health.

POS Systems

FairMoney MFB’s Point of Sale (POS) systems provide Nigerian SMEs with a robust infrastructure to accept online, mobile, and in-person payments seamlessly. By transitioning from a cash-only model to a multi-channel payment system, businesses can significantly reduce operational risks such as theft and accounting errors while expanding their reach to a nationwide customer base. This digital shift unlocks real-life opportunities for growth. A local retailer can move beyond foot traffic to sell to customers across the country via the web, while service providers can offer “Pay with Transfer” or card options that cater to the growing demographic of cashless consumers.

Every digital transaction creates a verifiable financial trail within the FairMoney MFB app, which the bank uses to build a more accurate credit profile for the merchant. This means that simply by making it easier for customers to pay, SMEs could potentially improve their credit profile and gain access to more competitive pricing needed for long-term expansion.

Maintaining detailed financial records has transitioned from a best practice to a regulatory necessity for SMEs. The current landscape, influenced by the Nigeria Revenue Service (NRS), increasingly values verifiable digital records as a means of supporting eligibility assessments for small business tax holidays. Maintaining such records through record keeping can facilitate compliance with requirements for exemptions, such as the 0% Company Income Tax (CIT) rate for businesses with an annual turnover below ₦100 million. Without accurate, time-stamped digital trails, including structured e-invoices and clear transaction histories, SMEs risk not only losing these vital fiscal reliefs but also facing significantly sharper penalties for late filing or non-compliance.

Beyond tax, streamlined records bridge the information gap that often hinders access to credit; by presenting a “financial compass” of real-time cash flow and profitability, business owners can prove their creditworthiness to partners, turning their compliance into a strategic tool for securing the capital needed to scale in an increasingly formalised market. FairMoney MFB continues to serve as a dynamic partner in an SME’s journey toward long-term scalability and financial stability.

James Edeh is the Head of Compliance at FairMoney Microfinance Bank

By Adedapo Adesanya

The Nigeria Deposit Insurance Corporation (NDIC) has commenced the process of paying insured deposits to customers of the 46 microfinance banks whose operating licences were revoked by the Central Bank of Nigeria (CBN).

In a statement issued on Wednesday by the Head of Communication and Public Affairs Department, Mrs Hawwau Gambo, the corporation said it had been appointed the official liquidator of the failed banks following the CBN’s revocation of their licences, which took effect on July 1, 2026.

The NDIC said its appointment was in line with the provisions of the Banks and Other Financial Institutions Act (BOFIA) 2020 and the NDIC Act 2023.

The organisation said the affected banks have ceased to operate as licensed financial institutions and are no longer authorised to carry out banking business in Nigeria.

“The NDIC has commenced the process of the orderly closure of the failed banks with their immediate takeover, verification and payment of insured sums to eligible depositors,” the statement said.

It added that depositors and the general public would be informed of subsequent steps in the liquidation process, warning members of the public against conducting transactions with any of the affected banks following the revocation of their licences.

It also cautioned individuals against removing, concealing or tampering with the assets, records or properties of the failed institutions, noting that such actions could amount to a breach of the law and attract sanctions.

Business Post earlier reported that the CBN revoked the operating licences of the 46 microfinance banks after determining that they no longer met the regulatory conditions required to continue operations.

According to the apex bank, the affected institutions were sanctioned for various regulatory breaches, including insufficient assets to meet liabilities, operating without approval, prolonged inactivity, failure to commence business within the stipulated period and failure to maintain the minimum capital required by law.

The apex bank said the action forms part of its efforts to strengthen financial sector stability, protect depositors and ensure compliance with banking regulations.

The affected institutions are spread across several states, including Lagos, Kano, Abia, Kaduna, Kebbi, Ogun, Niger, Plateau, Rivers, Delta, Benue, Cross River, Ondo, Osun, Anambra, Oyo, Bayelsa, Abuja and Akwa Ibom.

By Modupe Gbadeyanka

Entries for the 2026 edition of the flagship innovation initiative of Wema Bank Plc, Hackaholics, themed Powering Possibilities, opened on Wednesday, July 1.

At a press conference yesterday at its head office in Lagos, Wema Bank said all young Africans with creative tech-driven solutions across Financial Inclusion, Healthcare, Digital Transformation, Education, Sustainability, Social Impact and Future of Work can apply for the programme.

It was stressed that each application is to be made via the portal at hackaholics.wemabank.com, under one of three tracks: The Startup Pitch Competition, Hackathon and the newly introduced Social Impact track.

After the closure of the application window, Hackaholics 7.0 will then proceed on a national tour, which will touch 10 pitch centres across the six geopolitical zones of Nigeria. Each pitch centre will serve as a hub for innovators within the region to pitch their creative solutions and get the opportunity to secure the top spot in their pitch centre, and ultimately, proceed to the grand finale where the winners will be announced.

“As we launch Hackaholics 7.0 today, we are opening up a new phase of opportunities for more Nigerian youth to challenge themselves, explore their creativity and become startup founders.

“I encourage every young Nigerian with a passion for innovation to leverage the opportunity that we have carefully curated through Hackaholics and get ahead of the curve in today’s dynamic work landscape.

“Together, we can continue to build an ecosystem where innovation flourishes, opportunities expand, and young people are empowered to create solutions that shape the future,” Wema Bank’s Divisional Executive for Business Support, Mr Tajudeen Bakare, stated.

Also speaking, the chief executive of Wema Bank, Mr Moruf Oseni, said, “At Wema Bank, we believe that institutions have a responsibility that extends beyond providing commercial services.

“We have a responsibility to create meaningful opportunities, provide the right resources, enable innovation to thrive, and support the ecosystems that will shape today’s youth as well as tomorrow’s economy. This sense of responsibility is what has driven the evolution of Hackaholics from inception to date.

“With Hackaholics, we have, and we are investing in the next generation of innovators, inspiring innovation that will impact lives, strengthening Nigeria’s innovation ecosystem and giving youth a platform to make meaningful use of their creativity; and the numbers continue to speak volumes.”

Launched in 2019, Hackaholics is Wema Bank’s youth- and tech-focused initiative designed to serve as a platform for young Africans with creative, game-changing, tech-driven ideas and products to bring their ideas to life.

Since its launch, Hackaholics has discovered thousands of groundbreaking solutions, supported over 10,000 startups, engaged 50,000 participants, developed over 100 solutions from scratch and disbursed $500.0 million in grant prizes to dozens of winners whose remarkable solutions have earned a top spot in the past 6 editions.

By Aduragbemi Omiyale

The operating licenses of 46 microfinance banks in the country have been revoked by the Central Bank of Nigeria (CBN).

A statement on Wednesday from the banking sector regulator disclosed that the action followed failure by the affected small lenders to comply with regulatory requirements.

The central bank said it had to enforce its powers under Sections 12 and 13 of the Banks and Other Financial Institutions Act (BOFIA), 2020, to withdraw the licenses of the banks.

“The revocation of the licenses is part of the Bank’s ongoing efforts to safeguard the stability of the financial sector, protect depositors, and ensure that licensed institutions comply with current laws and regulatory requirements,” a part of the circular dated Wednesday, July 1, 2026, and signed by the acting Director of the Corporate Communications Department of the CBN, Mrs Hakama Sidi-Ali, stated.

The apex bank listed five violations by the 46 microfinance banks, including insufficient assets to meet liabilities, closure of operations without the CBN’s approval, inactivity and cessation of financial intermediation, failure to commence operations within 12 months of licence approval, and failure to maintain minimum capital funds unimpaired by losses.

Another part of the notice disclosed that, “The revocation was approved by the Governor of the Central Bank of Nigeria, Mr Olayemi Cardoso, following the banks’ failure to meet the regulatory requirements for continued operation as licensed financial institutions.”

The affected financial institutions are;

| S/NO | MFB | CATEGORY | STATE |

| 1 | Minji-Se Churchill MFB | Tier 1 | Rivers |

| 2 | Merchant MFB | Tier 2 | Abia |

| 3 | Janmaa MFB | Tier 1 | Kwara |

| 4 | Busu MFB | Tier 2 | Niger |

| 5 | Gold MFB | Tier 1 | Lagos |

| 6 | Zain MFB (foremerly Dawakin Tofa MFB) | Tier 2 | Kano |

| 7 | Bompai MFB | Tier 1 | Kano |

| 8 | Ajwa MFB (Formerly Gezawa) | Tier 2 | Kano |

| 9 | NOW NOW DIGITAL MFB | Tier 2 | Kano |

| 10 | Crystabel Microfinance Bank | Tier 1 | Bayelsa |

| 11 | Chanelle MFB | State | Lagos |

| 12 | Abia SME MFB | Tier 1 | Abia |

| 13 | Kamba MFB | Tier 2 | Kebbi |

| 14 | Iwade MFB | Tier 2 | Ogun |

| 15 | Winview MFB | Tier 1 | Abuja |

| 16 | Zuru MFB | Tier 2 | Kebbi |

| 17 | Minjibir MFB | Tier 1 | Kano |

| 18 | Shanono MFB | Tier 2 | Kano |

| 19 | Sumaila MFB | Tier 2 | Kano |

| 20 | Rimin Gado MFB | Tier 2 | Kano |

| 21 | Mwaghavul MFB | State | Plateau |

| 22 | Sycamore MFB | Tier 2 | Kano |

| 23 | TOFA MFB | Tier 2 | Kano |

| 24 | Safegate MFB | Tier 1 | Lagos |

| 25 | Creekline MFB | Delta | Tier 2 |

| 26 | Bestar MFB | Tier 1 | Oyo |

| 27 | Livingspring MFB | Tier 1 | Cross River |

| 28 | Apple MFB | Tier 2 | Ogun |

| 29 | Stanford MFB | State | Uyo |

| 30 | Frontline MFB | Tier 2 | Anambra |

| 31 | Zafec MFB | Tier 2 | Kaduna |

| 32 | Supreme MFB | Tier 1 | Lagos |

| 33 | Bejin-Doko MFB | Tier 2 | Niger |

| 34 | Kanopoly MFB | Tier 1 | Kano |

| 35 | Bellbank MFB formerly Tsanyawa | Tier 2 | Kano |

| 36 | Yeneng MFB | Tier 2 | Plateau |

| 37 | Creditville MFB | Tier 1 | Lagos |

| 38 | MBAG MFB | Tier 1 | Lagos |

| 39 | STRAIGHT SAHARA MFB | Tier 1 | Benue |

| 40 | OURPASS MFB | Tier 2 | Ondo |

| 41 | VERDANT MFB | Tier 1 | Lagos |

| 42 | BASAWA MFB | Tier 2 | Kaduna |

| 43 | CASHA MFB | Tier 2 | Abuja |

| 44 | ESTEEM MFB | Tier 2 | Kano |

| 45 | ENTERPRENEUR MFB | Tier 1 | Lagos |

| 46 | AVANTUS MFB | Tier 2 | Osun |

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism10 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz4 years ago

Showbiz4 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn