Economy

CBN To Monitor Dubious Bank Customers

By Dipo Olowookere

Bank customers involved in fraudulent activities will now be placed under the radar of the Central Bank of Nigeria (CBN).

The country’s apex bank disclosed yesterday that it was working out regulatory framework that would enable it either blacklist these set of bank customers or put them on watch-list across the banking industry.

Speaking at the Finance Correspondents Association of Nigeria (FICAN) Bi-Monthly Forum in Lagos, CBN Director, Banking and Payment Systems Department, Mr Dipo Fatokun, said the Bank Verification Number (BVN) it recently introduced would be used to achieve this.

Mr Fatokun explained that the BVN involves capturing of customers’ physiological or behavioural attributes like fingerprint, signature among others which is coordinated by the CBN and banks in collaboration with the Nigeria Interbank Settlement System (NIBSS).

At the event hosted by the CBN, Mr Fatokun, who spoke on the theme ‘Recent Developments in the Electronic Payments System and Implications for Consumers of Electronic Payment Services’ disclosed that data from the apex bank showed that although e-fraud rate in terms of value dropped by 63 per cent last year, after the BVN introduction and improved collaboration among banks via the fraud desks, the total fraud volume rose significantly by 683 per cent within the year compared to 2014 figures.

He further disclosed that Nigeria experienced a total of 3,500 cyber-attacks with 70 per cent success rate and loss of $450 million within the last one year mainly through cross channel fraud, data theft, email spooling, phishing, shoulder surfing and underground websites.

“I want to assure you that the BVN has assisted us a lot in the banking system. It has assisted us to check frauds, and we are working on a framework, that will enable us if not to blacklist customers, because of some legal implications, but at least to watch-list a customer that is identified to have been fraudulent, or have done what he is not supposed to do across the banking sector,” he said.

He said the PSV 2020 strategy is aimed at providing a roadmap for efficient payments system infrastructure that would be nationally utilized and internationally recognized.

“The payments system plays a very crucial role in any economy, being the channel through which financial resources flow from one segment of the economy to the other. In setting out the objectives of the National Payments System (NPS), the goal is to ensure that the system is available without interruption, meet as far as possible, all users’ needs, and operate at minimum risk and reasonable cost,” he said.

He added that the BVN project is jointly undertaken by the CBN in collaboration with the Bankers Committee and remains a strategy of ensuring effectiveness of Know Your Customer (KYC) principles.

“Each Bank customer is given a unique identity across the Nigerian Banking Industry, including Nigeria bank customers in Diaspora,” he said.

The CBN Director said the number of BVN linked to customers’ accounts as at August 23, this year was 36.7 million while the total number of individual customers in the banks was reported as 59.9 million as at the same date.

“Any bank customer resident in Nigeria without a BVN would be deemed to have inadequate KYC while effort is on-going to ensure that customers of Other Financial Institutions (OFIs) such as Microfinance Banks (MFBs) & Primary Mortgage Institutions (PMIs) are brought into the system begin to get their BVNs,” he said.

Mr Fatokun said the e-Payment remains an initiative of CBN under the Payments System Vision 2020 as part of the overall FSS 2020 Strategy adding that one of the CBN mandates is the promotion of a sound financial system (Section 2 (d) of the CBN Act 2007).

He disclosed that Section 47(2) of the CBN Act 2007, stipulates that the CBN shall continue to promote and facilitate the development of efficient and effective systems for the settlement of transactions, including the development of electronic payment systems, adding that the promotion of a sound financial system entails active support for the effectiveness, efficiency and systemic safety of the payments system.

Related articles across the web

By Aduragbemi Omiyale

The Global Banking and Finance Review has named Stanbic IBTC Capital, a subsidiary of Stanbic IBTC Holdings, as the Best Investment Bank in Nigeria for 2026.

The leading financial publication picked Stanbic IBTC Capital for the honour in recognition of its commitment to leadership and excellence in Nigeria’s investment banking sector.

The selection process involves an extensive evaluation of performance across critical metrics, including innovation, client service, financial health, and industry advancement.

Stanbic IBTC Capital’s accolade reflects its strong dedication to delivering capital markets and financial advisory solutions for clients in both the public and private sectors.

The firm has made significant strides in facilitating groundbreaking transactions, offering market-leading expertise in equity, debt, and structured finance, while nurturing the growth ambitions of businesses and institutions across Nigeria.

“We are truly pleased to be acknowledged for our relentless pursuit of excellence in the investment banking arena.

“This honour reflects our commitment to hard work and further establishes the deep trust our clients have in our expertise and service.

“It further motivates us to maintain our dedication to exceptional service, cultivate impactful partnerships, and continue delivering innovative financial solutions that meet our clients’ aspirations,” the chief executive of Stanbic IBTC Capital, Mr Oladele Sotubo, stated.

The Executive Director of Corporate and Transaction Banking at Stanbic IBTC Bank, Mr Eric Fajemisin, on his part, said, “Receiving this esteemed acknowledgement from the Global Banking and Finance Review Awards underscores our commitment to driving innovation and excellence within Nigeria’s investment banking landscape.

“This accolade highlights the significant role our skilled team plays in fostering economic growth and stability.

“We are dedicated to delivering exceptional value to our clients, which not only supports their financial success but also contributes to the broader development of the nation’s financial ecosystem.”

The Global Banking and Finance Review annually celebrates institutions that demonstrate quality, innovation, and contributions to the advancement of banking and financial services worldwide.

Now in its 16th edition, the awards honour organisations that uphold outstanding service standards, strategic execution, and industry leadership.

By Aduragbemi Omiyale

The Governor of Rivers State, Mr Siminalayi Fubara, has presented the 2026 Appropriation Bill to the Rivers State House of Assembly.

The 2026 budget estimate of N1.85 trillion, christened Budget of Resilience for Growth and Development, was presented to the state parliament on Friday.

Mr Fubara stated that the proposed spending for the 2026 fiscal year represents a 24.49 per cent increase over the adjusted 2025 budget, driven by anticipated growth in Federation Account Allocation Committee (FAAC) allocations, derivation revenue and internally generated revenue.

He informed the lawmakers that the state hopes to earn N487.61 billion from internally generated revenue, N936.05 billion from FAAC allocations, derivation funds, Value Added Tax (VAT) and exchange gains, and N382.48 billion from capital receipts, including loans, grants and asset sales.

According to him, N413.11 billion is for recurrent expenditure and N1.405 trillion for capital projects, underscoring his administration’s commitment to accelerating development across the state.

He added that personnel costs would gulp N154.77 billion, while N15.22 billion would fund new recruitments, stating that the budget also provides for pensions, gratuities, death benefits and debt servicing.

Governor Fubara further proposed a 50 per cent increase in overhead expenditure for Ministries, Departments and Agencies (MDAs) to strengthen their operational capacity immediately after the budget is signed into law.

He also stated that the largest allocation under the capital budget is the Works and Infrastructure sector with N533.32 billion, followed by Education with N315 billion and Healthcare with N105.43 billion.

In addition, N41.44 billion is for the Rivers State House of Assembly, N30 billion for the Judiciary, N19.26 billion for Agriculture, N15 billion for Power, N8.5 billion for Chieftaincy and Community Development, N7.98 billion for Sports, N7 billion for Youth Development, N6.5 billion for Women Affairs, and N6.61 billion for Environment and Sustainable Development.

The Governor noted that the budget was designed to sustain economic growth, expand critical infrastructure and improve the welfare of residents, pointing out that it builds on the achievements of his administration despite the challenges experienced by the state.

According to him, the budget prioritises the completion of ongoing road projects, new infrastructure investments, improved education and healthcare services, job creation and expanded economic opportunities for residents.

Describing the proposal as a people-centred budget, he assured Rivers people that every public fund would be judiciously utilised to deliver quality services, attract investment and stimulate inclusive development.

Mr Fubara acknowledged the delayed presentation of the budget and appealed to members of the House of Assembly to give the appropriation bill speedy consideration and passage to facilitate timely implementation.

In his remarks, the Speaker of the Rivers State House of Assembly, Mr Martin Amaewhule, acknowledged that the 2026 Appropriation Bill was presented later than expected but assured the Governor that the legislature would expedite its consideration in the interest of the people of Rivers State.

By Adedapo Adesanya

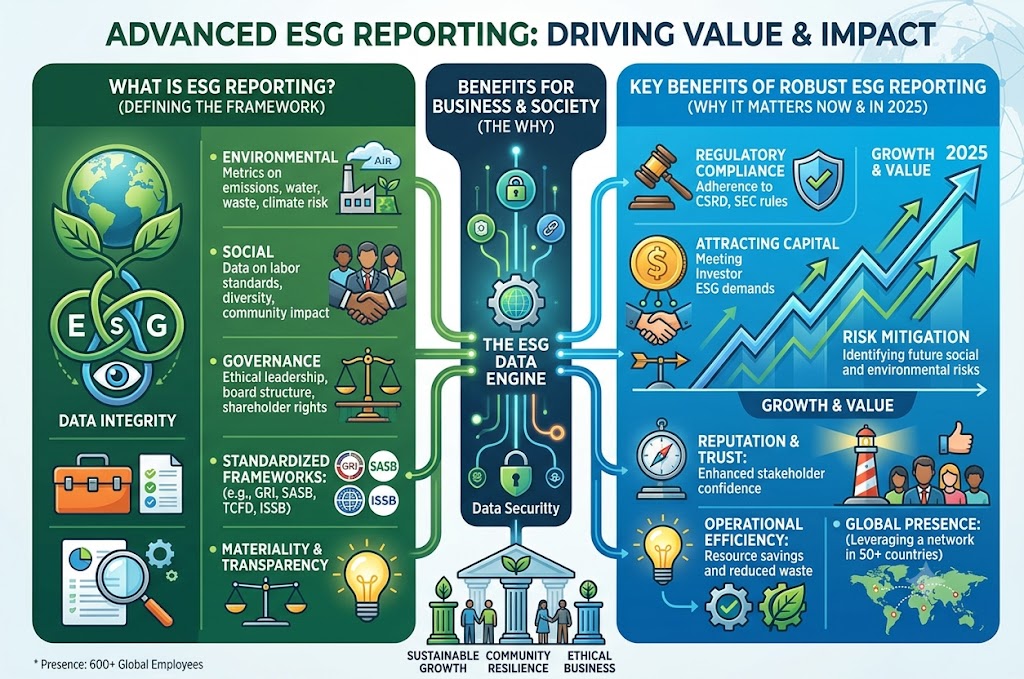

The Securities and Exchange Commission (SEC) has unveiled plans to make sustainability reporting mandatory for large public interest entities from 2027.

This comes as Nigeria moves to align its corporate disclosure framework with global environmental, social and governance (ESG) reporting standards.

The phased implementation will begin with voluntary adoption by early adopters and large public interest entities before becoming mandatory in 2027. The requirement will extend to other public interest entities in 2028 and small and medium-scale enterprises (SMEs) by 2030.

The Director-General of the SEC, Mr Emomotimi Agama, disclosed this at the 2026 Financial Institutions Training Centre (FITC) Sustainability and ESG Conference 3.0, themed ‘Building a Sustainable Africa: Integrating Environmental Stewardship, Social Investment, and Strong Governance for a Prosperous Future’ in Lagos.

Mr Agama said Nigeria’s sustainability disclosure regime is being aligned with the International Sustainability Standards Board (ISSB) framework, including IFRS S1 and IFRS S2, which have emerged as the global benchmark for sustainability reporting.

He said that institutional investors increasingly consider ESG performance a key determinant of capital allocation rather than a peripheral corporate responsibility issue, noting that the price of entry is disclosure.

He said the reforms would strengthen investor confidence and position Nigerian businesses to access global capital markets, where sustainability disclosures are becoming an essential investment requirement.

According to him, Nigeria’s capital market has recorded significant expansion, with market capitalisation growing from about N130 trillion to nearly N160 trillion following recent market reforms, while assets under management have surpassed N9 trillion.

To deepen sustainable finance, Agama said the commission was promoting infrastructure, green and municipal bonds, alongside infrastructure-focused investment funds, to mobilise long-term capital for critical national projects.

He added that the commission would also encourage investments in the blue economy and support financing for the power sector through green energy bonds, project bonds and public-private investment structures.

The SEC chief cited the recent launch of the Nigerian Exchange (NGX) Impact Board as another milestone in advancing sustainable finance and urged companies, regulators and investors to move beyond commitments by embedding sustainability into governance, operations and investment decisions.