Technology

Strengthening Fintech Ecosystem through Partnerships

“Alone we can do so little; together we can do so much.” This statement aptly describes the success achieved in the financial and payment landscape in Nigeria through the strategic partnership between fintechs and banks in the financial services industry.

Years ago, daring criminals would unleash mayhem on unsuspecting victims coming from banking halls and dispossess them of their valuables. This was because consumers had to move around with cash.

At the time, the majority of the people living in both urban and rural areas were unbanked and did not have access to financial products and services.

But as technology evolved and the digitalization of businesses became imperative to fit current realities, banks had to re-evaluate their service model and operational strategies. The need to transition into a digital wholesale banking system was inevitable.

The adoption of technology in service delivery such as banking, e-commerce, logistics etc. has contributed to the growth of fintech companies. With collaboration, fintechs have increasingly developed solutions that have been deployed across industries to enhance payment collection, efficiency and fund security. These partnerships between the fintechs and industry players have helped to accelerate product innovation, drive growth and provide top-notch solutions across the board.

The partnership between the fintech and the banking community has brought about innovative solutions such as funds transfer, on-demand bank statement, instant transaction alerts, payment authorization, loan request and disbursement, etc. Thanks to these innovative payment solutions, bank customers and account holders do not have to visit the banks often as they can initiate and complete transactions from the comfort of their homes.

Also, fintechs have leveraged partnerships with other service providers, such as power distribution companies (DISCOs), telecoms companies, ride-hailing services and utility companies to strengthen the payment ecosystem. These partnerships have further deepened financial inclusion and increased adoption of digital payment solutions, enhanced access to loans and other financial services such as funds transfer, bill payments, DSTV subscription, airtime recharge, and so on. These partnerships have helped the service providers collect payment seamlessly as well as allowing the customers to pay with ease.

Following these partnerships, Nigeria has witnessed an increase in the adoption of electronic payments over the last few years. Data shows the value of transactions via digital payment platforms, Nigeria Interbank Settlement System Instant Payment System (NIP) and Point of Sales (PoS) terminals rose to N60.34 trillion in the first quarter of 2021. That was a 12.55% increase when compared to the N53.61 trillion achieved in the fourth quarter of 2020.

Taking into cognizance that strategic partnerships help to strengthen payment solutions and are pivotal to economic growth, Africa’s leading digital payment and e-commerce company, Interswitch Group, has collaborated with several companies across industries to provide the broadest set of financial solutions to financial institutions across Africa.

Since its inception, Interswitch has been providing the switching infrastructure that connects different banks in Nigeria to reconcile inter-bank payments and settlements. Its solutions are also used to deliver the technology used for Automated Teller Machines (ATM) and PoS.

Following the acquisition of a minority stake by Visa in Interswitch in 2019, Interswitch is today the most valuable African Fintech business with a valuation in excess of $1 billion hence its recognition as a Unicorn. The partnership with Visa, allowed Fintech Unicorn to expand its digital payment solutions across the continent.

Beyond partnerships with brands, Interswitch has also partnered with governments across the continent to integrate its digital payment solutions to expand its inter-bank settlement capacities. These partnerships have enhanced the digital payment ecosystem, helped shape the much-needed financial transformation as well as boosted the African economy.

According to Tomi Ogunlesi, Group Head, Corporate Marketing, “Over the years, we have been making major strides in delivering world-class financial solutions to customers across the world. Through strategic partnerships, Interswitch has also reached major milestones and deepened access to financial services.”

In furtherance of its commitment to help strengthen the financial services industry, Interswitch recently revamped its developer console to improve the experiences of partners, developers and merchants who seek to integrate with their solutions.

Essentially, this platform enables developers to try out their products before going to the market. The new Interswitch APIs enable developers to create innovative tools and products and provides self-service integration, giving developers the ability to access Interswitch’s product APIs, authentication parameters, sandbox, production keys, documentation and seamless project management.

Indeed, the fusion between Fintechs, banks and other service providers as strategic partners would not only enable them to deliver satisfactory services to their numerous customers, it will help grow the payment ecosystem and also contribute immensely to the growth of the Nigerian economy.

By Modupe Gbadeyanka

A designed-in-house server known as Nathu La has been launched by a global technology company, Zoho Corporation.

Nathu La is engineered with hardware-rooted security at every layer of the stack. Its indigenous IP-driven approach reduces dependency on external entities for security audits, firmware updates, and licensing continuity.

The solution aligns with open-source software principles and reflects Zoho’s broader commitment to building sustainable, secure, and scalable digital infrastructure. It also supports the growing global focus on digital sovereignty, local innovation ecosystems, and high-performance computing capabilities.

The platform was introduced by the company as part of a pivotal step in its journey towards building its full technology stack, from the hardware layer to software applications.

With Nathu La, Zoho has achieved equivalent performance with 12-18 per cent lower power consumption and 20-30 per cent lower total cost of ownership (TCO), thereby reducing inference costs.

The Nathu La server, comprising Intel® Xeon® 6 processors, was developed collaboratively with Intel, leveraging their enablement capabilities and technical expertise.

The design philosophy behind Nathu La is rooted in the Open Compute Project (OCP), emphasising modularity, thermal efficiency, and ease of maintenance. This enables Zoho’s data centres to significantly reduce total cost of ownership and power consumption.

Zoho plans to host its applications on the Nathu La server platform, enabling the company to optimise the full software-hardware stack for its specific workloads, reduce costs, improve performance, and strengthen data governance for its global customers. This will also help bring down inference costs for Zoho’s AI usage.

The Nathu La server motherboard and chassis platform is the result of five years of R&D across hardware, firmware, and systems management. Based on Intel® Xeon® 6 Processors, the server is designed to optimise performance for virtualisation (VM), High Performance Computing (HPC), AI inference, and storage applications. This results in improved performance of Zoho applications for end users.

The server features customised power delivery subsystems, an in-house DC-SCM (Data Centre Secure Control Module) design, and modular chassis options compatible with diverse end-user environments, offering flexibility across deployment types.

All modular components – including the DC-SCM and NIC (Network Interface Card) – were designed in-house by Zoho’s hardware engineering team and assembled through electronics manufacturing partners, enabling tighter integration and quality control across the platform. Over five patents have been filed covering advanced thermal management and cost-optimised server architecture designs.

“Zoho Corporation has invested in building its own technology stack from the ground up over the last three decades. The Nathu La server launch is in line with that goal.

“With our strategy of using contextual, right-sized models, running on our own platform, on our own servers, in our own data centres, we are compounding the benefits accrued from owning and operating our entire technology stack. This ensures that our solutions are more sustainable and accessible for businesses.

“These long-term R&D investments we are making at every layer of the stack are aimed at delivering customer value,” the Country Head for Zoho Nigeria, Mr Kehinde Ogundare, stated.

In 2020, Zoho established a small R&D team in Nagpur, a Tier 2 town in India, focused on projects such as server design and systems engineering.

Members of the Nathu La R&D team include hires from SETU – short for Students’ Engagement for Transformative Upskilling – an initiative designed to build a pipeline of industry-ready engineers, with a focus on advanced learning in Electronics System Design and Manufacturing (ESDM).

By Adedapo Adesanya

The financial technology arm of MTN is mulling a direct shift into lending after bringing on its parent company, MTN Group, as a major investor to help cushion against losses that have plagued the business.

According to MTN Group Fintech chief executive, Mr Serigne Dioum, the company wants to move beyond helping customers access loans through partners.

He said in markets where regulators allow it, MTN wants to lend directly and use its own balance sheet.

“We’ve expanded access to credit for more people, but we also want to move further up the lending value chain,” Mr Dioum told investors at the company’s capital markets day.

“Where appropriate, we will seek licences that allow us not only to facilitate loans but also to lend directly to customers and deploy our own balance sheet.”

This development is expected to create a shift in its current fintech model which provides financial services, including deposits, payments, transfers and digital wallets to individuals and small businesses via digital and mobile‑based platforms.

The company has applied for Payment Solution Service Provider and Payment Terminal Service Provider licences through MoMo PSB, its Nigerian fintech subsidiary. If approved, the licences would allow MTN to handle more payment processing, build merchant payment tools, deploy and manage POS terminals, and reduce its dependence on third-party processors.

Despite the opportunities present in the credit market, direct lending could give MTN a larger share of revenue, but it would also expose the company to credit risk, regulation and tougher competition with banks and digital lenders.

Mr Dioum said only about 4 per cent to 5 per cent of adults have access to formal credit across the African continent. In Nigeria, the funding problem is especially severe.

A 2025 report by the National Credit Guarantee Company said nearly 80 per cent of Nigerian MSMEs lack access to formal credit, while Stears has estimated the country’s MSME financing gap at about $236 billion.

For traders, small shop owners, transport operators and households, access to small loans can determine whether they restock inventory, pay suppliers, cover emergencies or expand a business.

In April, MTN Nigeria announced that its parent firm, based in South Africa, would acquire a 60 per cent stake in MoMo Payment Service Bank Limited (MoMo PSB) and Y’ello Digital Financial Services (YDFS) Limited.

The fintech units are currently loss-making, and this move will help MTN Nigeria to reduce financial risk and share future losses and investment burden. However, it will still keep a significant minority stake (40 per cent).

By Aduragbemi Omiyale

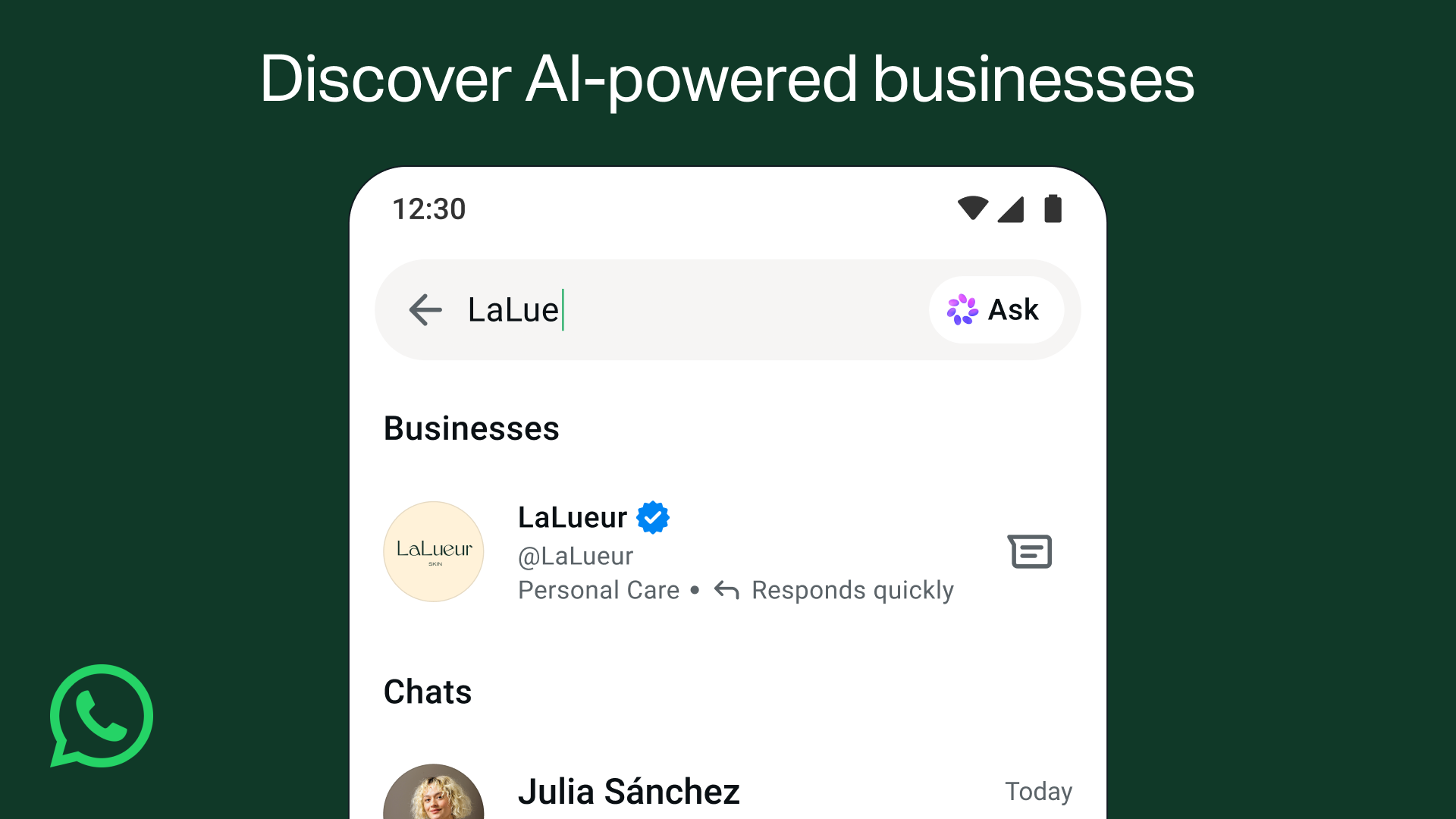

The reach of the Meta Business Agent is being expanded to Instagram and other platforms of the social media giant.

Meta Business Agent is an artificial intelligence (AI) that allows business owners to attend to customers’ needs with ease.

Customers expect instant responses, but no team can be everywhere at once. This innovation handles such without hassles.

It helps businesses to answer questions specific to the business, makes product recommendations from the catalogue, books appointments, qualifies incoming leads, and closes sales.

More than one million businesses are already using a Meta Business Agent on WhatsApp and Messenger to respond to customers around the clock.

“We’re now expanding our Business Agent to businesses big and small globally, so within minutes you can have yours up and running, responding in your customer’s local language using your tone,” Meta said in a statement.

“We’re also expanding these agents to Instagram since businesses connect with their customers there, too. Businesses can activate their Business Agent here. Getting started with the Business Agent is free. In the coming months, businesses will access the agent through our paid subscription offerings, with options for businesses of every size,” it added.

Meta also stated that it is making it simpler for people to discover businesses powered by a Meta Business Agent directly on WhatsApp. It noted that starting soon, people will be able to find businesses by typing their name in the Search bar, or by sharing their phone number or contact card in chats with friends and family. This way, when more customers reach out, they get a quick, helpful response.

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism10 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz3 years ago

Showbiz3 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn