Banking

FIGURES DON’T LIE! Despite Denial, Stats Show Unity Bank is Troubled, Auditors Raise Red Flag

By Dipo Olowookere

Despite a denial syndicated in the media by Unity Bank Plc over the weekend, financial statements of the bank in the last five years obtained from the Nigerian Exchange (NGX) Limited indicate that the lender is indeed troubled and distressed.

In the syndicated press release, the Central Bank of Nigeria (CBN) was quoted to have said the banking industry, not Unity Bank, was in good health as the “Capital Adequacy Ratio (CAR) and the Liquidity Ratio (LR) both remained above their prudential limits at 15.8 per cent and 38.9 per cent, respectively.

“The Non-Performing Loans (NPLs) at 5.89 per cent in April 2021, showed progressive improvement compared with 6.6 per cent in April 2020.”

“Please forget the denial, it’s just a facing strategy. Did the Central Bank of Nigeria (CBN) ever own up to the fact that First Bank of Nigeria was troubled not until recently when the CBN Governor, [Mr] Godwin Emefiele took drastic actions to save the institution?

“What about the defunct Skye Bank (now Polaris Bank) and many other banks in Nigeria that have been nationalized? You should know that the CBN will want to deny it to prevent panic amongst shareholders and depositors until it is set to take action,” an inside source told our reporter.

A close look at the books of Unity Bank shows that the lender is in dire need of urgent capitalisation if it must eventually survive the CBN hammer.

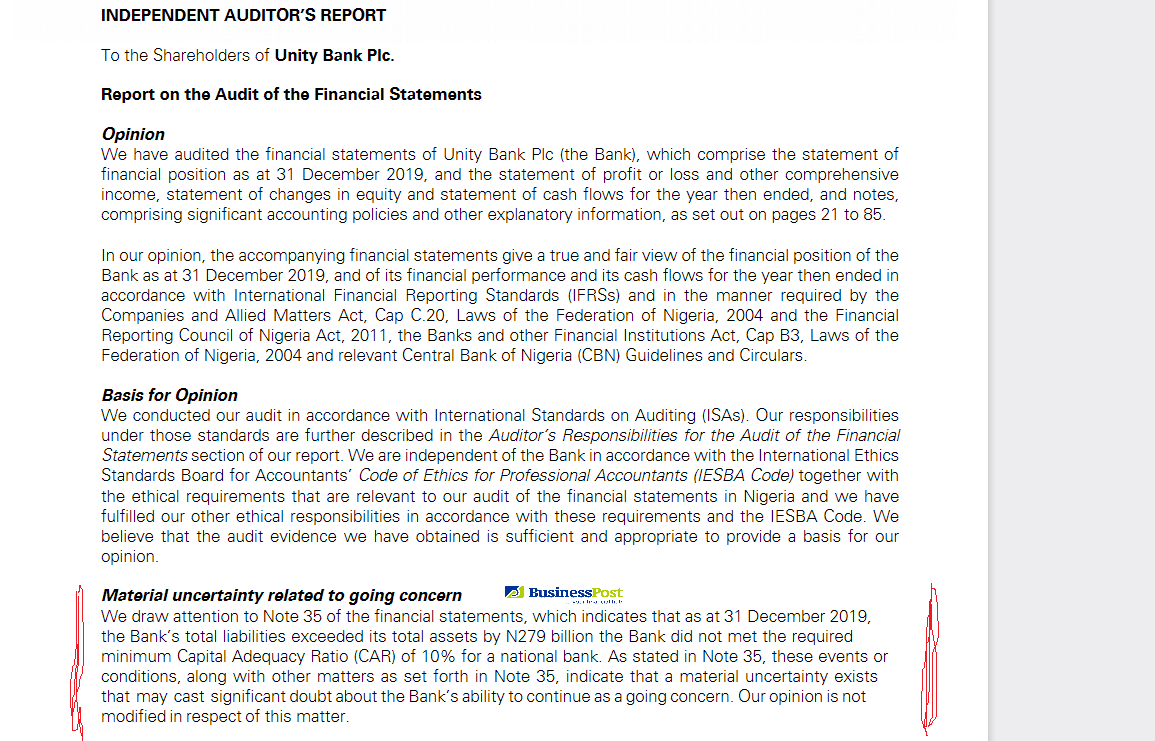

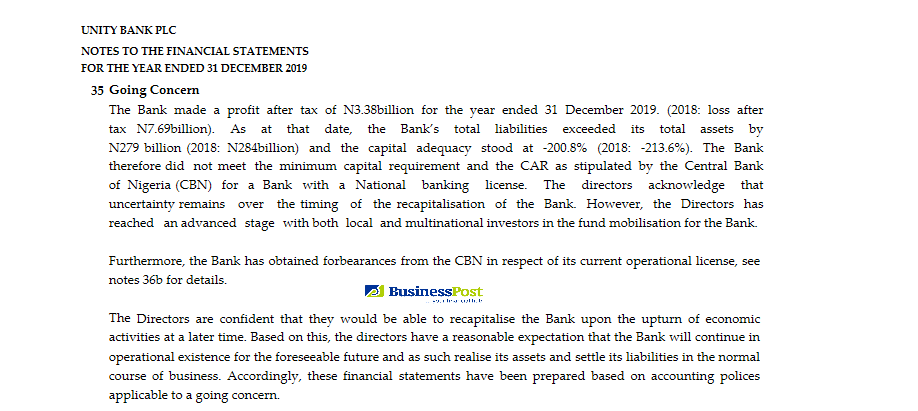

Even the bank’s external auditor, KPMG Professional Services, raised a red flag in 2019 and 2020 on the existence of Unity Bank, when it pointed out that the bank’s total liabilities exceeded its total assets by N279 billion and that the lender did not meet the required minimum CAR of 10 per cent for a national bank.

KPMG had warned that “a material uncertainty exists that may cast significant doubt about the bank’s ability to continue as a going concern.”

However, the board has expressed strong confidence that it would salvage the situation and get the financial institution back on its feet.

In the 2020 reporting year, the auditor again warned about this persistent matter and in the results, it was noted that in the year, Unity Bank only managed a pre-tax of N2.1 billion, lower than N3.4 billion in 2019 and its total liabilities exceeded its total assets by N275 billion versus N279 billion in 2019, with CAR of -101.29 per cent as against -200.8 per cent in 2019).

“The bank, therefore, did not meet the minimum capital requirement and the CAR as stipulated by the CBN for a bank with a national banking license which is 10 per cent.

“The directors acknowledge that uncertainty remains over the timing of the recapitalisation of the bank.

“However, the directors [have] reached an advanced stage with both local and multinational investors in the fund mobilisation for the bank,” the results said.

In the last five years, the performance trend of the financial institution has hardly tickled investors and there have been patches of weaknesses here and there, indicating that all is not well with the bank.

For instance, its profit before tax slumped 82 per cent from N13.639 billion in 2014 to N2.342 billion in 2015. It also dropped by 22 per cent from N2.342 billion in 2015 to N1.816 billion in 2016.

In 2017, the bank had a loss before tax of N14.243 billion compared with the pre-tax profit of N1.816 billion in 2016 and in 2018, in its restated results, the bank recorded a loss before tax of N7.554 billion, but in 2019, it was a pre-tax profit of N3.642 billion and in 2020, it slumped to N2.223 billion.

SEE BELOW BRIEF ANALYSIS OF UNITY BANK’S PERFORMANCES IN THE LAST FIVE YEARS

FY 2016 PERFORMANCE

The 2016 financial year was a tough one for Unity Bank Plc. While it was able to earn more from its core banking operations and its non-core banking activities, there was a decline in the bank’s ability to retain such turnover made to the profit level. Thus, profit declined significantly over the preceding years. As a direct consequence of this, the bank’s profitability ratios (such as profit margin, return on assets, and return on equity) recorded significant declines.

The bank also faced difficulties in the level of its bad loans, as well as its capital adequacy level remained negative.

Unity Bank recorded a higher turnover for its 2016 financial year than it did in its preceding year. For the review year, the bank recorded a 6.6 per cent growth in its turnover (inclusive of interest and discount income, and income from non-banking operations). Such turnover grew to N84 billion from N78.8 billion in the preceding year. This 6.6 per cent increase in gross earnings is as compared to a growth rate of 2.3 per cent in 2015.

However, 2016’s pre-tax profit followed a different path from that of gross earnings, standing at N1.82 billion, down from N2.34 billion in the erstwhile year, and translating into a 22.2 per cent decline rate. After-tax profit followed the same pattern as the pre-tax profit did, declining by as much as 53.5 per cent over the preceding year’s level to N2.18 billion.

Because of lower profits, the bank expectedly recorded worse results in respect to profitability in 2016. The profit margin, for example, dipped to 2.2 per cent in 2016 from 3.0 per cent in December 2015. What this means is that for every N100 earned by the bank in the course of the year, only N2.20 made it to the profit position. This is as compared to N3.00 for the year preceding 2016.

Return on assets (ROA) also recorded a regression. ROA slid to a mere 0.4 per cent in 2016 from 0.4 per cent in December 2015. Analysis shows that every N100 worth of Unity Bank’s assets contributed only 40 kobo to its pre-tax profit in 2016, down from 50 kobo in 2015.

For the 2016 financial year, Unity Bank deployed equity valued at N83.1 billion and for every N100 equity deployed, the bank made a low after-tax profit of N2.60, down from N5.70 in the preceding year.

In 2016, the bank decreased its workforce to 1,954 employees, 172 persons short of the 2,126 in its employ in 2015.

For the 2016 financial year, Unity Bank did not do too well when it comes to capital adequacy, recording a negative risk-weighted capital adequacy level in 2016, as it did in 2015.

As was the case with capital adequacy, the bank did not also do well in 2016 as regards loans classified as non-performing. The proportion of classified loans to the entire loan stock was a high and therefore bad 56 per cent.

The bank gave a lower dividend for its 2016 financial year than it did in 2015. Thus, the retention ratio was 0.67 times, lower than 0.82 times in the preceding year.

Asset turnover for the year was 0.17 times, just a tad slower than the 0.18 times recorded in the prior year, while assets/equity was 5.9 times, as compared to 5.4 times in 2015.

Analysis shows that sustainable growth for 2016 was 1.5 per cent, higher than the 2.3 per cent recorded in 2015. This means that using only the revenue it generates, this bank had the capacity to grow by 1.5 per cent, lower than 2.3 per cent in 2015.

FY 2017 PERFORMANCE

In the 2017 fiscal year, Unity Bank recorded a significant milestone and this was the eventual sale of its toxic loans, comprising commercial, insider-related and intervention loans, to an institutional assets management company, making it have zero NPLs, meaning it was starting afresh.

In its financial statements for the year, the lender explained that this was part of its recapitalisation strategies.

“Consequently, upon payment of the initial consideration by the debt buyer, loans and advances with a gross amount of N436 billion have been derecognized, along with the associated IFRS impairment and Regulatory Risk Reserves,” a part of the results analysed by Business Post showed.

However, this did not stop Unity Bank from recording a loss after profit of N14.9 billion compared with the profit after tax of N2.2 billion in the preceding year.

In the year, according to the results, it was indicated that Unity Bank Plc was initially granted forbearance by the CBN for compliance with the cash reserve ratio when it was set at 33 per cent and the bank had until 2017 built up the reserve as the CBN debited the bank N500 million weekly.

Upon the request of Unity Bank in 2017, the apex bank granted additional forbearance on the cash reserve to provide additional working capital and resolve liquidity bottlenecks and the revised cash reserve ratio was set at 22.5 per cent.

FY 2018 PERFORMANCE

Unity Bank recorded a loss of N7.55 billion in FYE 2018.

In its Q2 2018 results, gross earnings nosedived by 58.72 per cent YoY from N42.35 billion in Q2 2017 to N17.49 billion consequent upon 68.34 per cent decline in net interest income to N7.74 billion in Q2’18 from N24.45 billion in Q2’17.

OPEX dropped from N12.19 billion in Q2 2017 to N10.36 billion in Q2 2018 with a 14.86 per cent decline recorded after growing at a consistent interval to end FY2017 at N24.46 billion. This, however, offsets the margin of the decline in OPEX over net interest income as it averaged at 52.67 per cent in FY2017 compared to 134 per cent recorded in Q2 2018.

In half-year 2018, pre-tax and post-tax profits declined by 77.0 per cent and -76.48 per cent YoY to N535.65 million and N492.80 million, respectively in Q2 2018 compared to the Q2 2017 figures.

Fixed assets went down by 4.73 per cent YoY from N21.19 billion in Q2’17 from N22.23 billion in Q2 2017 while total assets also fell significantly by 59.77 per cent YoY in Q2 2018 and -68.2 per cent in 2017 to N196.75 billion.

However, the Q2 2018 total assets figure represents 25.71 per cent growth over FY 2017 figure. This uptrend is in tandem with the PAT trajectory which turned positive.

Loans and advances to customers increased to N12.78 billion in Q2’18 from N8.96 billion in Q4’17 representing 43 per cent growth.

However, the Q2 2018 loan and advances figure shrank by 95.78 per cent from N302.62 billion in Q2’17 to N12.78 billion in Q2 2018 which, therefore, exacted a toll on the total assets and net assets as indicated by a plummeted ratio of loans to customers to total assets from a high of 64.0 per cent in Q3’17 to 5.7 per cent in Q4’17 and 6.5 per cent Q2’18 respectively and the net assets which ended in the negative of N242.19 billion in 2017 and -N240.08 billion in Q2 2018.

On the back of the decline in after-tax loss recorded in Q4 2017, return on asset declined from 0.51 per cent in Q3’17 to -9.5 per cent in Q4’17 but quickly turned upward on the V curve in Q2 2018 to 0.25 per cent.

The improvement in the bank’s performance in Q2 2018 compared to FY 2017 is at some cost as reflected in the sharp increase in its cost-income ratio from 44.90 per cent in FY 2017 to 93.19 per cent in Q2 2018.

Unity Bank’s share price declined consistently from its 2018 peak of N1.92 attained on February 12, 2018, to halt the bullish run. However, its YTD performance with 70 per cent growth recorded at 90 kobo attained on Tuesday, July 24, 2018, reflects that the stock currently trades low.

FY 2019 PERFORMANCE

Unity Bank’s financial results for 2019 jumped up a little from a loss of N7.69 billion in 2018 to a profit of N3.38 billion, representing a 148.21 per cent growth.

Regardless of the bank’s strong pre-tax profit growth between 2018 and 2019, a few areas of the bank’s operations create a looming shadow of what may appear to be a reversal of the bank’s fortunes.

The fact that the bank has managed to survive three consecutive years of operations with negative shareholders fund above N250 billion annually between 2017 and 2019 raised concerns over the bank’s operational stability, or at least should.

Unity Bank’s LDR ratio rose by 40.37 per cent in 2019 from 17.8 per cent in 2018, however, this was 25 per cent below the CBN’s statutory ratio of 65 per cent advised to banks in Q4 2019.

A perusal of the bank’s financials for 2019 revealed that the growth in its loans to customers was not matched by a corresponding growth in deposits received from customers.

The bank’s loans to customers increased by 135.93 per cent while its deposit from customers increased by 40.63 per cent. The disparity between the growth of loans to customers and deposits from customers raises the question of how Unity Bank was able to increase lending against slow growth in deposits.

The bank’s books suggested that lending in 2019 was financed increasingly by a rise in borrowings. The bank’s borrowings increased by 45.23 per cent between 2018 and 2019, as borrowings rose from N126.21 billion in 2018 to N183.3 billion in 2019.

The bank’s asset quality improved noticeably in 2019 as it sold off the bulk of its toxic assets and cleared up its loan book to allow for a fresh start. Its impairment losses on financial assets declined to N1.92 billion in FYE 2019 from N5.96 billion in FYE 2018.

Though loans to customers rose from N44.1 billion in 2018 to N104.02 billion in 2019, the loan growth was largely intervention loans for Anchors Borrowers’ Programmes (ABP) of the CBN, as its deposits from customers did not record any significant increase between 2018 and 2019.

FY 2020 PERFORMANCE

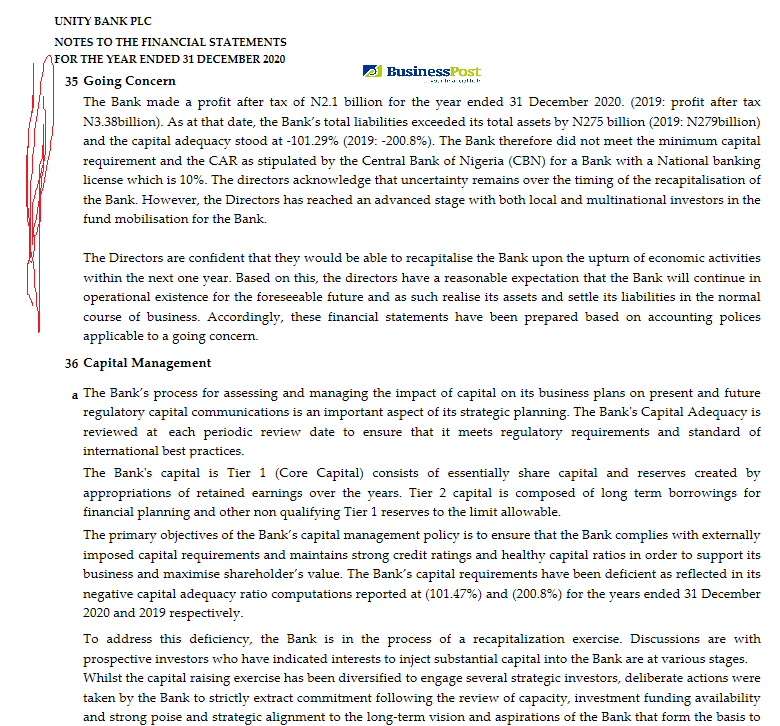

Unity Bank 2020 financial results showed that the lender has not recovered as its profit plunged again over credit and revaluation loss.

The lender’s profit dropped 38 per cent to N2.08 billion compared to N3.38 billion a year before.

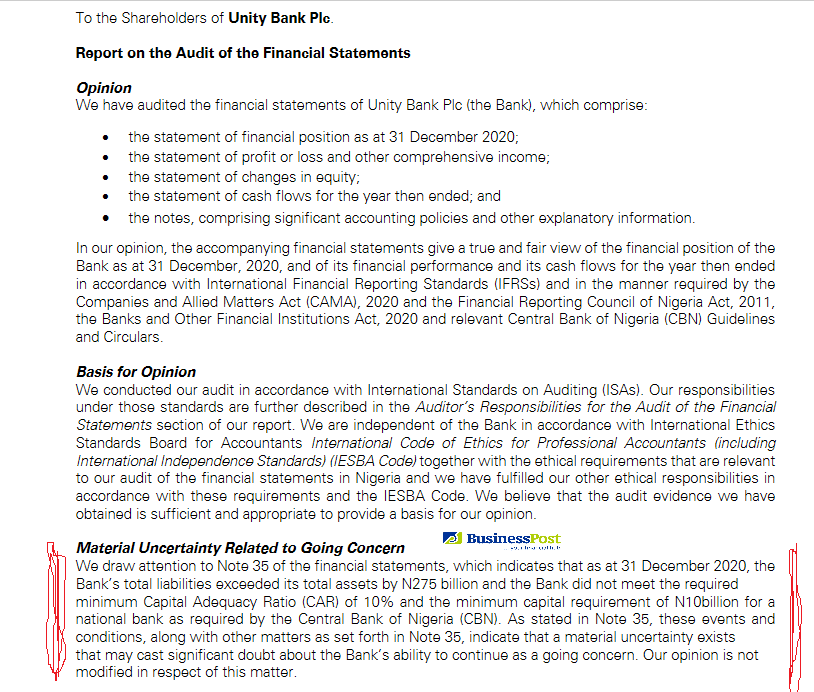

The report of the independent auditors for Unity Bank, KPMG Professional Services, showed that as at December 31, 2020, the total liabilities of the bank “exceeded its total assets by N275 billion and the bank did not meet the required minimum Capital Adequacy Ratio (CAR) of 10 per cent and the minimum capital requirement of N10 billion for a national bank as required by the Central Bank of Nigeria (CBN).”

From the analysis of the results, the total assets of the lender stood at N492.0 billion in the period under review, while the total assets stood at N767.4 billion, with the CAR at -101.29 per cent. These indicators are worrying.

Earnings per share fell 38 per cent to 17.8 kobo per share from 28.9 kobo per share the previous year.

Personnel expenses rose by 10 per cent to N10.4 billion compared to N9.4 billion in 2019, while depreciation of property and equipment dropped to N1.69 billion compared to N1.7 billion in the same period of 2019.

The bank paid N22.1 billion income tax in 2020, a 38 per cent decline compared to N 36.2 billion paid the year before.

There are concerns among shareholders of the lender that there may not be time to achieve these lofty goals as last year, the bank had to receive a N50 billion short term loan from the CBN to meet working capital requirements and this credit facility is expected to mature on September 19, 2021. This loan and others have increased the debt of the financial institution.

A critical look at the financial statements in 2020 showed that Unity Bank is no longer enjoying the patronage of individual and government depositors, except for corporate depositors.

Last year, the deposits from the government reduced to N27.1 billion from N30.9 billion, while the deposits from individuals dropped to N99.1 billion from N123.0 billion.

Only deposits from corporate organisations rose to N230.4 billion from N103.8 billion and this contributed to the increase in the customer deposits of Unity Bank in the year to N356.6 billion from N257.7 billion in 2019.

In the year, Unity Bank said its profit before tax dropped to N2.2 billion from N3.6 billion, while the profit after tax went down to N2.1 billion from N3.4 billion.

Q1 – 2021 PERFORMANCE

Unity Bank’s financial statement for Q1 2021 showed that the lender’s total liabilities of N801.98 billion exceeded its total assets of N521.48 billion by 35 per cent, due to protracted loss history.

In the first three months of this year, it had a retained loss of N371.95 billion, which dragged total equity further down by 2 per cent to a loss of N280.50 billion.

A retained loss is a loss incurred by a business, which is recorded within the retained earnings account in the equity section of its balance sheet.

In the last five years, Unity Bank has been putting up a seesaw performance, recording two consecutive losses in 2017 and 2018, before recovering in 2019 with N28.94 billion post-tax profit.

However, its profit dipped by 38.33 per cent to N2.09 billion in 2020 from N3.38 million it posted in the previous year.

More so, customers were also wary of the safety of their money in Unity Bank, causing its deposits to decline in the first three months of 2021.

The bank customers’ deposits dipped by 2 per cent to N348.34 billion in Q1 2021 instead of N356.62 billion garnered in the prior period last year.

Even fellow lenders cut their deposits in Unity Bank by one per cent to N105.37 billion compared with N106.70 billion in Q1 2020.

Also worrisome was that most of the income lines of the second-tier lender went down during the period under review.

The total revenue dipped by 3 per cent to N11.45 billion, undermined by fee and commission income which decreased by 14 per cent to N1.60 billion (Q1 2020: N1.86 billion) and a net trading loss of N53.48 million recorded as of March instead of N327.87 million it made in the period last year.

However, interest income grew marginally by one per cent to N9.67 billion from N9.61 billion in Q1 2020.

Unity Bank performance in the first three months of this year would have been woeful if not for the other operating income, which was up by a whopping 317 per cent to N233.96 million, lifted specifically by transaction income that rose by 175 per cent during the period.

Its performance was also bolstered by the N65.89 million loan recovery it made against the N429.67 million provision it had to set aside for toxic assets in Q1 2020.

This was the impetus that propelled the lender’s pre-tax profit to rise by 43 per cent to N784.28 million and post-tax profit to uptick by 43 per cent to N721.54 million.

Meanwhile, it was able to cut interest expenses by 11 per cent to N4.86 billion compared with N4.86 billion the bank expended for the same purpose in Q1 2020, but personnel cost rose marginally by one per cent to N2.68 billion.

Unity Bank commenced operations in January 2006 following the merger of nine banks with competencies in investment, corporate and retail banking.

The lender is led by Ms Tomi Sofefun and chaired by Mr Aminu Babangida, with Oluwafunsho Obasanjo, Sam Okagbue, Hafiz Mohammed Bashir, Yabawa Lawan Wabi, Temisan Tuedor, Ebenezer Kolawole and Usman Abdulqadir on the board.

By Adedapo Adesanya

First Holdco Plc has commenced a public offer to raise about N1.4 trillion (approximately $1 billion) after securing approval from the Central Bank of Nigeria (CBN).

The offer, which opened on Monday, involves the sale of 10.4 billion ordinary shares, according to the chief executive of its banking subsidiary, First Bank of Nigeria Limited, Mr Olusegun Alebiosu.

The capital raise follows the company’s earlier plan to transfer about a quarter of its shares to RC Investment Management Ltd., which served as a bridge holder after Barbican Capital Limited exited its investment in the lender amid a prolonged ownership and leadership dispute.

First Holdco had previously indicated that the shares would eventually be offered to the investing public once the necessary regulatory approvals were obtained.

Speaking in an interview with Bloomberg, Mr Alebiosu said proceeds from the offer would strengthen the capital base of First Bank and support the holding company’s expansion strategy.

According to him, the group intends to diversify beyond banking by establishing an insurance underwriting business and a fintech services company.

“The sale is starting today — the reality here is that I am not sure it will stay more than one week based on the pressure we are getting,” Mr Alebiosu said, expressing confidence in strong investor demand.

Investors appeared to respond positively to the announcement, with First HoldCo’s shares climbing as much as 5.9 per cent to a record high during trading on Monday before easing to a 3.1 per cent gain at N133.60 by early afternoon in Lagos.

The lender has been one of the best-performing banking stocks on the Nigerian Exchange (NGX) Limited over the past year, with its share price rising more than fourfold since July 2025, when Barbican Capital’s stake was transferred to RC Investment Management.

The fresh capital injection comes as its largest shareholder, Mr Femi Otedola, continues to strengthen his stake in Nigeria’s oldest bank. With the billionaire holding around a 26 per cent stake in the company, analysts say he has his eyes set on full control once his equity crosses the 30 per cent mark.

By Adedapo Adesanya

One of Nigeria’s top digital banks, PalmPay, has appointed a former executive of the Nigeria Inter-Bank Settlement System (NIBSS), Mr Samuel Oluyemi, as its chief operating officer.

In his new role, Mr Oluyemi will oversee the financial technology company’s operations in Nigeria, where it offers a broad range of digital financial services to individuals and businesses.

Mr Oluyemi will also engage with regulators to ensure the company’s expansion aligns with Nigeria’s financial, digital and social inclusion objectives.

Prior to joining the company, Mr Oluyemi spent more than two decades at NIBSS, where he served as business development lead.

During his tenure, he drove the development of several critical payment infrastructure projects, including the digital validation of Nigerian international passports, e-Dividend Mandate Management System (e-DMMS), and the Electronic Pensions Contribution Collection System (EPCCOS).

Also, he played a key role in the introduction and early adoption of the NIBSS Instant Payment (NIP) platform, Nigeria’s first real-time interbank transfer system launched in 2011, and later supported its extension to other financial institutions.

Mr Oluyemi obtained a master’s degree in Monetary Economics from the University of Ibadan and has participated in several local and international professional training programmes.

Commenting on the appointment, Managing Director of PalmPay Nigeria, Mr Chika Nwosu, said that the company was strengthening its leadership team to support its longterm vision.

By Adedapo Adesanya

Africa’s most valuable fintech, Flutterwave, has signalled that its long-anticipated initial public offering (IPO) remains firmly on the back burner as the company intensifies efforts to transform itself into a licensed financial institution across the continent.

The firm’s chief executive, Mr Olugbenga Agboola, said the firm is focused on building sustainable profitability, diversifying its revenue streams and expanding its banking footprint before considering a stock market listing.

Speaking to The Africa Report, Mr Agboola described an IPO as a future financing milestone rather than an immediate strategic objective.

“An IPO is a financing event, not a strategy,” he said. “We are not holding any pressure to go public. This gives us the flexibility to be patient and ensure when we do list, we’re doing so from a position of strength.”

The comments come as Flutterwave embarks on an acquisition-led expansion strategy aimed at securing banking licences and deeper regulatory access across Africa.

Mr Agboola revealed that the company is currently in the process of acquiring a bank in East Africa, though he declined to disclose the institution or country involved.

The planned acquisition is expected to provide Flutterwave with an established customer base, existing banking infrastructure and regulatory approvals, significantly shortening the time required to enter new financial services markets.

According to Mr Agboola, the company’s expansion priorities include Kenya, Ghana, Rwanda, Tanzania, South Africa and Egypt, while the Democratic Republic of Congo and Ethiopia remain under consideration for future growth.

Rather than building banks from scratch in every market, Flutterwave intends to adopt a mix of acquisitions, licences and strategic partnerships depending on local regulatory conditions.

“The vision is not to form a bank in every country but to ensure that every African business has access to more than financial services,” Mr Agboola said in the interview.

The banking push follows recent regulatory and corporate developments, including the Central Bank of Nigeria’s approval of Flutterwave’s banking licence and the acquisition of open banking startup Mono.

Together, the moves underscore a broader strategy to expand beyond payments and establish new revenue streams in lending, liquidity management and business banking services.

Flutterwave plans to focus on institutional deposits from businesses already using its platform rather than competing aggressively for retail deposits.

The company intends to leverage transaction data from its payments network to provide short-term working capital, merchant financing, invoice discounting and trade finance products for small and medium-sized enterprises.

Mr Agboola disclosed that the bulk of the capital earmarked for banking operations will be directed toward credit support and liquidity buffers, with additional allocations for lending and banking infrastructure.

The strategy reflects a growing trend among African fintech firms seeking banking licences to reduce dependence on traditional financial institutions and gain greater control over settlement, liquidity management and product development.

Despite speculation about a near-term public listing, Mr Agboola maintained that Flutterwave’s immediate focus remains execution and growth.

He noted that the company will only consider an IPO after achieving stronger profitability and establishing scale across its payments, banking and remittance businesses.

In February 2025, he told Bloomberg that Flutterwave would only pursue a public offering after becoming profitable. He also stated in late 2024 that the company was “not in the IPO race.”

Founded in 2016, Flutterwave has processed more than one billion transactions valued at over $40 billion across 35 African countries. The company recently secured fresh funding that lifted its valuation to $3.3 billion, with American blockchain firm Ripple leading the investment round.

For now, however, Flutterwave appears more interested in building the foundations of a pan-African financial institution than rushing to the public markets, positioning banking expansion as the next phase of its growth story while keeping an eventual IPO firmly on the long-term horizon.