Economy

IMF Charges Nigeria, Others to Deepen Fiscal Buffers Amid Headwinds

By Adedapo Adesanya

The International Monetary Fund (IMF) has called on Nigeria and other African countries to deepen fiscal buffers, adopt context-specific monetary policies, and advance regional economic cooperation in order to cushion the effect of global headwinds and unlock long-term inclusive growth.

The Managing Director of the Bretton Wood institution, Ms Kristalina Georgieva, said this during the launch of IMF’s latest Global Policy Agenda Report titled Anchoring Stability and Promoting Balanced Growth at the ongoing World Bank/IMF Spring Meetings in Washington.

She highlighted the continent’s mixed growth outlook and called for a renewed commitment to structural reforms.

Speaking further on fiscal reforms, she said, “Don’t hide behind excuses, and say we can’t go for more tax because, you can. There is a lot that can be done to broaden the tax base, and a lot that can be done to reduce tax evasion and tax avoidance, using technology, as some countries are doing, to chase the tax dollars, when there is the foundation for that, is a very good thing to do.”

Ms Georgieva pointed out that while Africa remained home to some of the world’s fastest-growing economies, a significant number of low-income and fragile states were increasingly falling behind, especially in the wake of slowing global growth and rising geopolitical risks.

“We have seen over the last years, the African continent having some of the fastest growing economies, but we also have seen low-income countries primarily and among the fragile conflict-affected countries falling further behind, and now this, this is a shock for the continent,” she added.

The IMF chief stated that while the direct effect of trade tariffs on most African countries was minimal, the indirect consequences, particularly, from a slowdown in global growth posed more serious challenges, especially for oil-exporting countries, like Nigeria.

“The direct impact of tariffs on most of Africa, not on all of Africa, but on most of Africa, is relatively small, but the indirect impact is quite significant.

“Slowing global growth means that, all other things being equal, they would see a downgrade. And actually, we have downgraded the growth prospects for the continent, for the oil producers, like Nigeria, falling oil prices create additional pressure on their budgets. On the other hand, for the oil importers, this is a breath of fresh air.

“In other words, different countries face different challenges. If I were to come up with some basic recommendations that apply to Africa, I would say they apply to Nigeria, Egypt, Ghana, and they apply to Cote d’Ivoire.

“First, continue on the path of strengthening your buffer levels. There is still a lot that can be done on the fiscal side, to have strength and to have the buffers for a moment of shock, and don’t use any excuses around,” Ms Georgieva noted.

The IMF managing director urged Nigeria and other governments in Africa to do more to expand their tax base and tackle leakages through digital tools. She warned against copycat monetary policies, urging central banks to respond based on country-specific inflation pressures rather than mimic regional peers.

“On the monetary policy side, we are no more in a place where you can look at the book of the central bank governor of the neighbouring country and say, ‘Oh, they’re doing this, let’s try out the same,’ because you have to really assess domestically, what your inflationary pressures are and do the right thing for your country,” she said.

Ms Georgieva also made a passionate call for Africa to rebrand its global image, stating that corruption and conflict in one country cast a long shadow over the entire region.

“But above all, make it so that the image of the whole continent changes, because now everybody suffers from wrongdoing, from corruption or conflict in one country, it throws a shadow on the rest of the continent. And finally, like Asia, there is a need to deepen inter-regional trade and cooperation, remove the obstacles.”

She also underscored the importance of boosting intra-African trade, comparing the continent’s potential to that of Asia and welcomed World Bank efforts to ease infrastructure barriers to trade.

She added: “Sometimes they are infrastructure obstacles. The World Bank is working on reducing the infrastructure obstacles to broaden trade. Africa has so much to offer the world. They have the minerals, better resources, and a young population. I think that a more unified, more collaborative continent can go a long, long way to be an economic powerhouse.”

By Adedapo Adesanya

Manufacturers are yet to benefit from relief on the burden of multiple taxes and levies despite the enactment of the Nigeria Tax Act 2025, according to the Manufacturers Association of Nigeria (MAN).

The association, in its Manufacturers CEO Confidence Index (MCCI) report for the second quarter of 2026, said manufacturers continued to face multiple tax collectors and regulatory agencies during the period.

Director-General of MAN, Mr Segun Ajayi-Kadir, said the new tax law, which was expected to reduce the burden of multiple taxation, had yet to deliver the intended benefits.

“Manufacturers complained that they were still met with multiple tax collectors and regulators in Q2 2026. It follows that the implementation of the Nigeria Tax Act 2025 is yet to achieve its objective of relieving manufacturers of the burden of taxes and levies,” he said.

According to the report, Nigeria’s business environment remains largely unsupportive of manufacturing growth, with local sourcing of raw materials emerging as the only indicator that recorded noticeable improvement.

MAN, however, warned that the gains in local sourcing could be undermined by worsening insecurity in parts of the country.

The association attributed the improvement largely to persistent foreign exchange constraints, which have forced many manufacturers to source inputs locally.

Despite this, it said excessive regulation and multiple taxation continue to weigh heavily on manufacturers.

The report showed that manufacturers recorded a modest increase in sales volume during the second quarter, but rising production, distribution and logistics costs continued to erode profitability.

It added that capacity utilisation, production levels, investment and employment remained broadly unchanged during the review period.

MAN further observed that although recent foreign exchange reforms had helped stabilise the naira, inadequate foreign currency supply remained a major constraint to manufacturing operations.

Other key challenges identified in the report include poor infrastructure, high production costs, raw material shortages and unfavourable trade policies.

The association said the findings underscore the continued pressure on manufacturers despite recent fiscal and foreign exchange reforms, stressing the need for more effective implementation of policies aimed at improving the operating environment for the real sector.

By Adedapo Adesanya

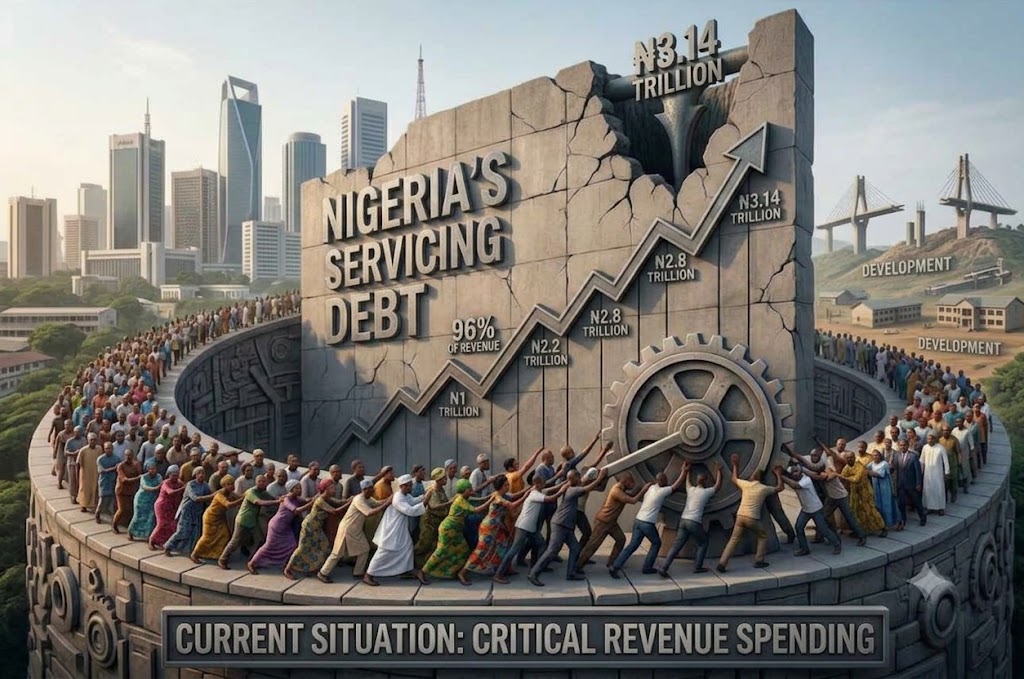

The federal government spent N3.14 trillion on servicing its domestic debt in the first quarter (Q1) of 2026, according to the Debt Management Office (DMO).

The figure, contained in the DMO’s latest domestic debt service report for Q1 2026, comprised N2.97 trillion in interest payments and N169.68 billion in principal repayments.

According to the report, the government spent N741.82 billion on domestic debt service in January before the figure rose to N967.67 billion in February.

Debt service increased further to N1.43 trillion in March, bringing total spending for the quarter to N3.14 trillion.

The March figure represented a 47.7 per cent increase from the N967.67 billion recorded in February and was 92.7 per cent higher than the N741.82 billion spent in January.

The debt office said interest payments accounted for approximately 94.6 per cent of the total domestic debt service during the quarter.

Treasury bills accounted for the largest share of interest payments at N1 trillion, while interest payments on Federal Government bonds stood at N1.96 trillion.

The government also paid N4.24 billion in interest on FGN savings bonds during the period.

The debt management body said the principal component of the debt service comprised N169.68 billion in repayments on local-denominated promissory notes.

Overall, domestic debt service rose significantly throughout the quarter, with March alone accounting for nearly half of the N3.14 trillion spent between January and March.

By Aduragbemi Omiyale

The Director-General of the Securities and Exchange Commission (SEC), Mr Emomotimi Agama, has outlined how the Federal Capital Territory Administration (FCTA) can leverage Nigeria’s capital market to raise long-term funds for critical infrastructure projects instead of relying solely on annual budgetary allocations.

According to Mr Agama, the capital market offers the FCT a sustainable financing model for roads, rail, housing, water, transport and other infrastructure through instruments such as infrastructure bonds, green bonds, real estate investment trusts (REITs), asset recycling and tokenised municipal securities.

Speaking at the Abuja Business and Investment Summit and Expo (ABIE 2026) in Abuja, the SEC chief noted that Abuja’s development demonstrates that economic growth is driven by investment, stressing that “cities are not built by budgets alone. Cities are built by capital markets.”

He advised the FCT to establish a long-term infrastructure bond programme backed by dedicated revenue sources such as ground rents, tenement rates, tolls, parking fees and land-use charges, noting that this would enable the territory to finance major projects without overburdening annual budgets.

“A budget can only spend what a single year has collected. A bond can spend what 30 years will collect,” Mr Agama said, explaining that infrastructure projects generate long-term economic value that can be used to service debt over time.

The SEC boss said the territory could also access cheaper financing through green and sustainability-linked bonds for projects including mass transit, light rail, solar-powered street lighting, waste-to-energy facilities and water infrastructure.

He further proposed the creation of an FCT Real Estate Investment Trust to unlock value from Abuja’s extensive property portfolio while giving ordinary Nigerians an opportunity to invest in the city’s real estate market.

Mr Agama also urged Abuja Investments Company Limited (AICL) to consider listing some of its businesses or establishing a listed infrastructure fund, saying this would raise capital without increasing government debt while improving corporate governance and transparency.

On the long-abandoned Millennium Tower project, he said the estimated over N400 billion completion cost should not be viewed as a budgetary burden but as an investment opportunity that could be financed through a special purpose vehicle and offered to investors via the capital market.

“The question is not whether Nigeria can afford the Millennium Tower. The question is whether we will let ordinary Nigerians own it,” he said.

Mr Agama further proposed an asset recycling programme under which completed income-generating public assets, including terminals, markets, commercial properties and the International Conference Centre, could be securitised or concessioned to institutional investors, with proceeds reinvested in new infrastructure.

He also called on the FCT to pioneer a regulated tokenised municipal bond programme that would allow citizens to invest as little as N10,000 through mobile phones in specific infrastructure projects.

According to him, the recently enacted Investments and Securities Act (ISA) 2025 has strengthened the legal framework for sub-national governments to access the capital market while providing enhanced investor protection and clearer regulation of digital assets.

Mr Agama disclosed that Nigeria’s capital market has grown significantly, with total market capitalisation exceeding N217 trillion as of May 2026, comprising about N160.5 trillion in equities and N56.7 trillion in bonds.

He said recent reforms, including the migration to a T+1 settlement cycle and regulatory measures to deepen market participation, have improved market efficiency and strengthened investor confidence.

The SEC DG assured the FCTA of the commission’s readiness to provide technical support for structuring and registering capital market instruments, saying the agency would work closely with the territory to unlock financing for infrastructure projects.

He added that Nigeria’s capital market remains critical to mobilising domestic savings for national development, insisting that “money is not scarce; delivery capacity is scarce, and financing follows delivery capacity.”