Economy

How the Nigerian Economy is Reacting to the Global Crisis

The COVID-19 pandemic is still in full swing. Since the early months of 2020, it has been affecting countries on all continents.

Nigeria is no exception, despite the relatively low death toll. Here is how the global crisis has influenced the national economy so far.

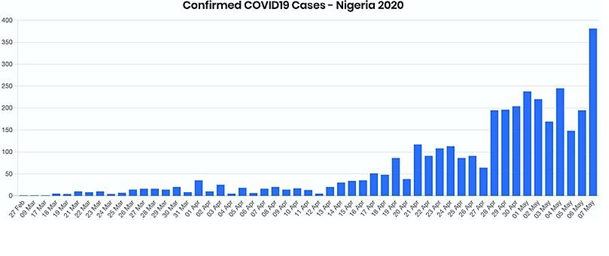

Current Statistics on COVID-19

As of this writing, Nigeria has 4,399 confirmed cases and 143 deaths. This is incomparable to the six-digit figures observed in the US, but the numbers are still growing. Developing countries, in general, have seen relatively few cases, although the danger is still very real.

Declaring of the pandemic sent shock waves across financial markets in early March. However, it is not the only cause of downtrends. In fact, negative dynamics began even before the outbreak. Forecasts of global GDP in 2020 were quite dismal, with only 2.5% growth. The outlook for the emerging markets was especially gloomy.

The Preceding Troubles

Even before the crisis, the local government had a lot to grapple with. The country was still recovering from the oil shock of 2014, and GDP growth was limited — just 2.3% in 2019. The figure was later changed to just 2% by the International Monetary Fund, as a result of oil price collapse and fiscal restrictions.

The debt profile was yet another reason for alarm. According to recent estimates, the debt service-to-revenue ratio stands at 60%. The dismal situation with oil prices is likely to send the figures further down. All these factors should be considered when evaluating the nation’s response to the pandemic.

Key Policy Changes

The Central Bank of Nigeria (CBN) has implemented a fiscal stimulus package. The support scheme provides a credit of 50 billion naira for small and medium-sized businesses, as well as households affected by the crisis. The healthcare industry has been provided with a loan of 100 billion naira. The manufacturing segment has received 1 trillion naira.

Secondly, the institution revised its interest in interventions. The rate has been almost halved, now fixed at 5%. Since March 1, all intervention facilities are put on hold by a one-year moratorium.

Another major issue is the collapse of global demand for crude. Oil is one of the country’s key sources of revenue and foreign exchange. The sharp decline has caused significant damage. Officially, the rate was adjusted from 306 to 360 naira.

Household Consumption: Looming Decrease

Experts predict households to reduce consumption due to several reasons. Spending will be mostly limited to the most essential goods and services. This is inevitable because:

- The population are restricted in movement, either partially or fully;

- Predictions of future income are discouraging, especially for workers in the gig and informal economy;

- The gradual erosion of wealth, but actual and expected, is observed due to downtrends on the stock market and in home equity.

In such desperate times, the population will be looking for alternative sources of income. Online trading, which has recently been embraced by the nation, may see significant growth. For many consumers, it may offer the only source of profit.

FXTM, an international MetaTrader 5 broker, expects more accounts to be opened by residents of Nigeria. The range of instruments includes currency pairs, stocks, CFDs, and other derivatives. Through a licensed broker, these may be traded in Nigeria legally.

Investments by Firms

These are expected to shrink due to the pandemic. It is not yet clear how long it will last, what effect the policies will have, and how economic players will react. The overall turmoil in the finance markets reflects unfavourable market sentiments.

In the realm of stocks, the country has seen a dramatic collapse. The Nigerian Stock Exchange has recorded the deepest fall since 2008. Investors have been hit hard. Given the general uncertainty surrounding the pandemic, and the joyless profit outlook, firms are unlikely to pursue any long-term investment schemes.

Government Expenditure: Projections of Growth

Government spending is predicted to expand as more stimulus packages are released. The measures should compensate for the drop in consumer spending. At the same time, fiscal deficits may soar. This will be exacerbated by the oil prices.

Nigeria is heavily dependent on oil. The commodity accounts for 90% of the country’s exports. The national budget for 2020 was built around predictions of $57 per barrel. However, the price of Brent has been fluctuating around $29 since early April. Since March, the government has already cut its planned expenditure.

A Wake-Up Call?

Overall, Nigeria is bound to experience the dramatic effects of the pandemic and lockdown measures. Despite the government’s efforts to help key industries, its resources are limited. The crash of oil prices is detrimental to the health of the national economy. It remains to be seen whether policymakers can learn from their mistakes and diversify the country’s revenue in the future.

By Aduragbemi Omiyale

African leaders have been advised to focus on economic integration through industrialisation, as this would make the continent a formidable force in the global market.

This charge was given by the Minister of State in the Tanzanian President’s Office responsible for Planning and Investment, Prof. Kitila A. Mkumbo, during a visit to the Dangote Petroleum Refinery and Petrochemicals in Lagos.

“Africa now needs economic liberation, and that can only come through industrialisation,” he said, describing Mr Aliko Dangote as Africa’s leading industrialist whose investments are increasingly extending beyond Nigeria to support development across the continent.

He added that Tanzania looks forward to working with Dangote Group as part of a broader vision of accelerating Pan-African industrialisation and strengthening regional manufacturing capacity.

The Minister also highlighted the importance of local refining capacity in improving Africa’s energy security, particularly in light of recent disruptions in global oil markets.

Referring to the impact of tensions around the Strait of Hormuz on global fuel prices, he said increased refining capacity from facilities such as the Dangote Petroleum Refinery would help cushion African economies against external shocks.

According to him, affordable and reliable energy remains one of the most important drivers of economic development, noting that expanded refining capacity across the continent would contribute significantly to lowering energy costs and improving the quality of life for millions of Africans.

The Tanzanian delegation was in Nigeria to follow up on discussions held earlier this year between President Samia Suluhu Hassan and Mr Dangote regarding the expansion of Dangote Group’s investment footprint in Tanzania.

The East African nation reaffirmed its commitment to deepening economic cooperation with Dangote Group, expressing strong interest in attracting new investments in fertiliser production, energy and industrial infrastructure to support the country’s long-term development agenda.

“We have come here to make a follow-up on what they deliberated with our President in terms of further Dangote investments in Tanzania,” Mr Mkumbo said.

By Aduragbemi Omiyale

One of the leading brewers and beverage companies listed on the Nigerian Exchange (NGX) Limited, Champion Breweries Plc, has expressed its commitment to strengthening its market position.

The beer maker gave this assurance while reacting to its financial performance for the first half of 2026, which was strong, driven by solid commercial performance, improved operational efficiencies, and the successful expansion of its business portfolio following the acquisition of EnjoyBev B.V.

In the period under review, the organisation boosted its growth platform through strategic investment, delivered resilient operating performance, and successfully transitioned to a new group structure.

Its revenue reached N35.73 billion, while second-quarter revenue amounted to N21.37 billion. Operating profit stood at N6.17 billion, and profit after tax attributable to the group was N2.65 billion, with second-quarter profit after tax of N1.76 billion.

The firm also successfully completed the acquisition of an 80 per cent equity interest in EnjoyBev B.V., strengthened its capital base through a successful capital raising programme that increased shareholders’ equity to N69.08 billion, and maintained full compliance with NGX free float requirements, with free float increasing to 25.72 per cent as of June 30, 2026.

“The first half of 2026 marks a defining chapter in Champion Breweries’ journey. We have not only delivered a strong operating performance but also successfully transformed our business into a broader beverage group with an expanded platform for sustainable growth.

“While higher finance costs associated with our strategic investment programme impacted profitability during the period, our underlying business remains strong.

“The combination of disciplined commercial execution, continued investment in our brands and route-to-market capabilities and improving operational efficiency positions us well for future growth.

“We remain focused on creating long-term value for shareholders, strengthening our market position, and capturing the opportunities presented by our expanded business platform,” the acting chief executive of Champion Breweries, Mr Rasheed Adebiyi, said.

For businesses operating across borders, payments are no longer simply the final step in a transaction. The way money moves can influence where a company sells, how quickly it can enter a new market, and how easily customers can complete a purchase. As digital payment methods become more diverse, businesses are adjusting not only their checkout options but also the way payment processes fit into wider operations.

This shift is particularly visible in international commerce. A company can now serve customers in multiple markets without relying on a single payment method or a traditional physical presence in each location. Digital payments have become part of the infrastructure that supports increasingly distributed business models.

A More Connected Payment Environment

Global commerce has created a more complicated payment environment. Customers in different countries may have very different expectations about how a purchase should be paid for. Some markets rely heavily on cards, while others have seen rapid adoption of digital wallets, bank-based payment methods, or other local alternatives.

For businesses, this variety creates both opportunities and practical challenges. Offering payment options that customers recognize can reduce friction during a transaction, while supporting several markets may require businesses to work with different payment technologies and providers.

Digital payments have therefore become closely connected to market expansion. A company entering a new country does not only need to consider demand for its products or services. It also needs to understand how customers in that market prefer to pay and whether its existing payment setup can accommodate those expectations.

More Choices for Businesses and Customers

The growth of digital payments has expanded the range of choices available on both sides of a transaction.

Consumers can increasingly choose between cards, digital wallets, bank transfers, mobile payment methods and other forms of electronic payment. Businesses, meanwhile, can select from different technologies and payment providers depending on their markets and operational requirements.

This development has changed the role of payments in the customer experience. Payment is no longer necessarily treated as an isolated technical process that begins only after a purchasing decision has been made. The available options can influence whether a customer completes a transaction in the first place.

For international businesses, flexibility can be particularly important. A payment method that is familiar and convenient in one market may be less relevant in another. Supporting a broader selection can allow businesses to adapt their payment experience without changing the underlying product or service.

The Rise of Alternative Payment Models

Traditional card and bank-based payments remain important, but the digital payments landscape has expanded beyond these established methods. Digital wallets, account-to-account payments, mobile solutions and cryptocurrency have all contributed to a broader definition of what a digital transaction can look like.

Cryptocurrency remains a smaller part of the overall payments landscape, but it has created another category of payment technology for businesses to consider. Specialized solutions such as BitHide can provide businesses with tools for handling crypto payments as part of their broader payment operations.

The significance of this development is not necessarily that every business will adopt cryptocurrency. Rather, it demonstrates how the payment landscape continues to diversify. Businesses operating internationally can increasingly choose from different models instead of relying on a single approach across every market.

Payments Are Becoming Part of Business Operations

As payment systems become more digital, their role increasingly extends beyond accepting money from customers. Payment processes can interact with accounting, order management, customer records and other parts of a company’s digital operations.

This is particularly relevant for businesses with large transaction volumes or customers in multiple countries. Manual payment processes can become difficult to manage as the number of transactions, currencies and payment methods increases. Digital systems can help businesses organize these processes within a wider operational framework.

The result is a gradual shift in how companies think about payments. Instead of treating payment processing as a separate function, businesses are increasingly considering it alongside other elements of their digital infrastructure.

This does not mean that every company needs a complex payment setup. The appropriate approach depends on the business model, target markets, transaction volumes and types of customers involved. For some companies, a small number of established payment methods may be sufficient. Others may need a more flexible arrangement because of the markets they serve.

Adapting to Different Markets

One of the more important changes brought by digital payments is the ability to adapt payment experiences to different markets.

International businesses often face differences in consumer behavior, financial infrastructure and preferred payment methods. A payment strategy that works well domestically may therefore require adjustments when a company expands internationally.

Digital payment technology can make these adjustments more practical, but it does not remove the need for local market knowledge. Businesses still need to understand customer preferences, applicable requirements and the practical costs associated with different payment methods.

This makes payment strategy part of international expansion rather than an issue that can be addressed only after a new market has been entered.

What Comes Next for Global Businesses

The digital payments market is likely to continue becoming more diverse as businesses and customers adopt new ways of moving money. The important change may not be the replacement of one payment method by another, but the growing ability to combine different methods according to the needs of a particular business or market.

For global companies, this creates an emphasis on adaptability. Payment systems need to support the way a business operates rather than becoming a limitation on where and how it can sell.

Digital payments are consequently becoming more than a convenient alternative to cash or traditional payment processes. They are increasingly connected to international commerce, customer experience and day-to-day business operations. As payment options continue to develop, companies that can adapt their payment strategies to different markets will be better positioned to operate in an increasingly digital global economy.