Economy

Wives of Detained Binance Executives in Nigeria Seek Intervention

By Aduragbemi Omiyale

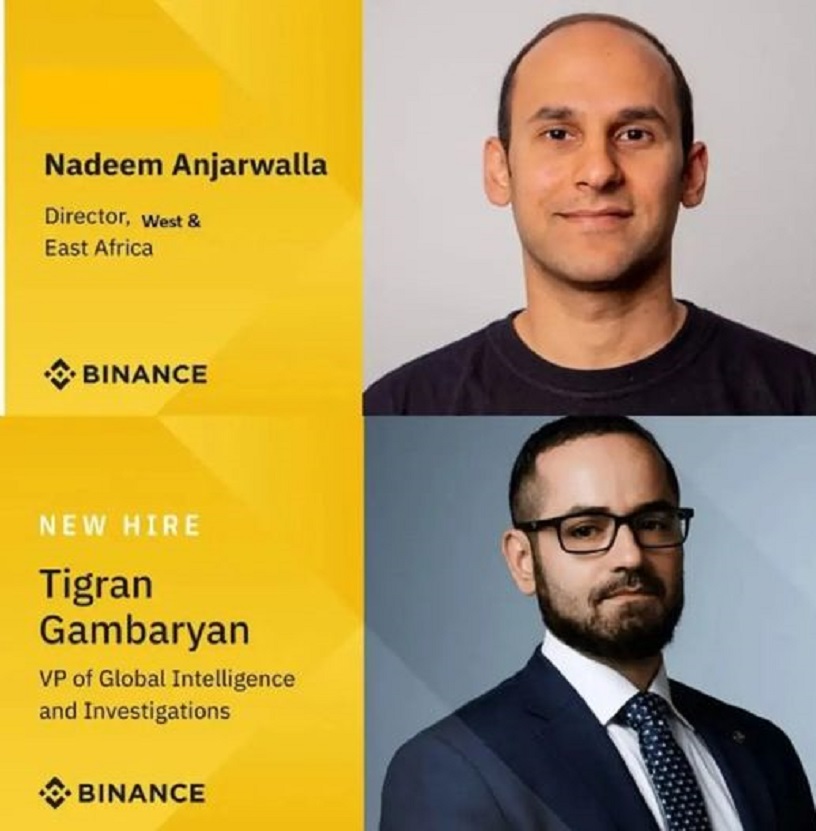

The detention of two executives of Binance, a popular cryptocurrency exchange platform, by the Nigerian government has continued to generate reactions.

Last month, on the invitation of the local authorities, Mr Tigran Gambaryan, an American citizen, and Mr Nadeem Anjarwalla, a British-Kenyan national, flew into the country but were immediately held by the Office of the National Security Adviser (ONSA).

The government accused the company of allowing its platform to be used for manipulating the country’s foreign exchange (FX) market, weakening the value of the domestic currency, the Naira.

Binance was later forced to stop the use of Naira transactions on its crypto exchange and a few days ago, a court in Abuja directed the firm to hand over trading data of its Nigerian users to the Economic and Financial Crimes Commission (EFCC).

On Wednesday, March 20, 2024, the federal government took Mr Gambaryan and Mr Anjarwalla to court to secure an order to keep them for additional days after the expiration of an original order on March 12, but the court adjourned the matter to Friday, April 5 for hearing.

Worried that her husband may have to remain in custody till the next hearing, which coincidentally is the fifth birthday of their son, Mrs Yuki Gambaryan appealed to the federal government to release her husband to rejoin them and continue his “good work” at Binance.

“Tigran was only supposed to be away from us for a very short trip and now over 3 weeks later we have no idea when we will see him again.

“I don’t know what to tell our two children who rush to the door every time they hear a car, eagerly hoping that their father has finally returned from a very long work trip.

“Tigran is globally recognized for his work in law enforcement and many of his peers would say that Tigran’s continuous efforts are what keep cryptocurrencies safe and clean.

“Please let him come home to continue this good work. The longer that our husbands are away from our families, the harder it is becoming for us to go about our daily lives.

“We are asking you from the bottom of our hearts and with the deepest respect that you please release them so that our families can be complete once again,” she pleaded.

On her part, Mrs Elahe Anjarwalla lamented that her husband is unable to witness the first birthday of their son today, Thursday, March 21, 2024, because of his incarceration in Abuja.

She has asked the British and Kenyan governments to intervene in the matter and secure the release of her husband.

“I am completely heartbroken. I was holding on to the hope that Nadeem would be home in time to celebrate our son’s first birthday together and I am devastated this won’t be happening.

“Nadeem has no authority to make high-level decisions at Binance and I am once again asking from the bottom of my heart that the Nigerian authorities please allow him and Tigran to return home whilst they continue their discussions with Binance.

“I am also calling on the British and Kenyan governments to do more to get Nadeem back home to us. Please, we just want this nightmare to end,” she said.

Business Post reports that the international passports of Mr Gambaryan and Mr Anjarwalla were seized by the Nigerian authorities when they arrived in the country on February 26, 2024.

By Adedapo Adesanya

The NASD Over-the-Counter (OTC) Securities Exchange closed flat on Wednesday, August 5, as the market witnessed weaker trading activity with only two deals executed.

In the midweek session, the volume of securities exchanged by investors dropped 99.9 per cent to 802 units from the 1.6 million units recorded on Tuesday. The value of securities further decreased by 99.6 per cent to N208,240 from the preceding session’s N47.6 million, and the number of deals significantly went down by 93.9 per cent to two deals from the 33 deals recorded a day earlier.

Great Nigeria Insurance (GNI) Plc remained the most traded stock by value on a year-to-date basis, with 3.4 billion units worth N8.4 billion, followed by Infrastructure Credit Guarantee (Infracredit) Plc with 2.3 billion units sold for N6.5 billion, and Central Securities Clearing System (CSCS) Plc with 76.9 million units transacted for N5.5 billion.

GNI Plc was also the most active stock by volume on a year-to-date basis, with 3.4 billion units exchanged for N8.4 billion, followed by Infracredit Plc with 2.3 billion units traded for N6.5 billion, and Resourcery Plc with 1.1 billion units valued at N415.7 million.

There were no price gainers or losers yesterday.

As a result, the market capitalisation stood unmoving at N2.739 trillion, while the NASD Security Index (NSI) remained unchanged at 4,563.96 points.

By Adedapo Adesanya

The Naira slid against the US Dollar by N2.28 or 0.17 per cent in the Nigerian Autonomous Foreign Exchange Market (NAFEX) on Wednesday, August 5, to N1,363.85/$1 from N1,362.55/$1.

The local currency also declined against the Pound Sterling in the official market during the session by N5.97 to close at N1,837.38/£1 compared with Tuesday’s closing rate of N1,831.41/£1, and against the Euro, it crashed by N6.54 to quote at N1,575.25/€1 versus the preceding session’s N1,568.71/€1.

But at the black market, the Nigerian Naira traded flat against the greenback yesterday at N1,400/$1, and also remained unchanged at the GTBank FX desk at N1,373/$1.

The Central Bank of Nigeria (CBN) says rates have narrowed to below two per cent, while the country’s external reserves have risen above $52.5 billion, reflecting the impact of its ongoing monetary and foreign exchange reforms.

CBN Governor Yemi Cardoso, represented by the Acting Director of Corporate Communications and Investor Relations, Mrs Hakama Sidi-Ali, disclosed this on Tuesday during the CBN Fair in Gombe. He noted that reforms introduced since 2023 had significantly reduced the disparity between the official FX market and the parallel market.

“The Naira continues to strengthen, with the spread between official and Bureau de Change rates now below two per cent,” he said, adding that reserves at $52.5 billion were supported by sustained inflows and renewed investor confidence in the economy.

Interbank FX transactions slid as weaker market activities dropped total Dollar volume exchanged to $75.35 million, a 51.8 per cent decline from $156.23 million in turnover quoted at the previous close.

The deals at the NFEM window also fell as data from the central bank put Wednesday’s quote at 82 from 139.

In the cryptocurrency market, major were down as global risk sentiment softened as a key world equity index slipped and chipmakers fell.

The MSCI All Country World Index snapped a five-day run to fall 0.2 per cent as chipmakers retreated on both sides of the Pacific. South Korea’s Kospi, a bellwether for the AI trade, dropped 4.4 per cent.

Ripple (XRP) depleted by 1.7 per cent to $1.05, Binance Coin (BNB) decreased by 1.0 per cent to $594.87, Cardano (ADA) depreciated by 0.9 per cent to $0.1884, TRON (TRX) shrank by 0.2 per cent to $0.3261, Solana (SOL) crumbled by 0.1 per cent to $74.00, and Dogecoin (DOGE) went down by 0.1 per cent to $0.0697.

On the flip side, Ethereum (ETH) gained 2.3 per cent to trade at $1,911.41, and Bitcoin (BTC) rose by 0.8 per cent to $64,759.28, while the US Dollar Tether (USDT) and the US Dollar Coin (USDC) remained unchanged at $1.00 apiece.

By Dipo Olowookere

The domestic stock exchange rebounded by 0.05 per cent on Wednesday on the back of renewed bargain-hunting by investors, though the level of activity waned.

After bleeding for a few days, the Nigerian Exchange (NGX) Limited heaved a sigh of relief yesterday, as the All-Share Index (ASI) gained 109.41 points to close at 244,912.24 points compared with the previous day’s 244,802.83 points, and the market capitalisation garnered N71 billion to settle at N158.087 trillion versus Tuesday’s N158.016 trillion.

Business Post reports that despite the rebound recorded by Customs Street at midweek, the market breadth index remained negative, as there were 20 price advancers and 29 price decliners, implying bearish investor sentiment.

Linkage Assurance appreciated by 9.94 per cent to N1.77, AVA Capital rose by 9.55 per cent to N10.90, Fortis Global Insurance advanced by 7.69 per cent to N2.80, McNichols gained 7.34 per cent to finish at N5.85, and Coronation Insurance surged by 5.51 per cent to N2.49.

Conversely, Honeywell Flour depreciated by 9.94 per cent to N16.30, PZ Cussons gave up 9.94 per cent to trade at N74.75, Zichis crashed by 9.74 per cent to N20.76, Learn Africa slipped by 9.62 per cent to N9.40, and Neimeth tumbled by 8.33 per cent to N8.25.

The busiest equity was FCMB, with a turnover of 369.2 million units valued at N4.1 billion. Chams transacted 46.7 million units worth N201.8 million, First Holdco transacted 43.5 million units for N5.7 billion, Access Holdings sold 29.8 million units worth N778.0 million, and Linkage Assurance exchanged 19.6 million units valued at N33.5 million.

At the close of transactions, market participants bought and sold 824.1 million units worth N25.5 billion in 48,114 deals, in contrast to the 1.6 billion units sold for N28.7 billion in 54,160 deals a day earlier, showing a shortfall in the trading volume, value, and number of deals by 48.49 per cent, 11.15 per cent, and 11.16 per cent, respectively.