Economy

How I Went Bankrupt Because of Abacha’s Death—Tonye Cole

Nigeria is a nation that knows all too well what damage dictatorships can do. Between 1966 and 1999, the country saw several military coups, culminating in Sani Abacha seizing power. From 1993 to 1998, Abacha’s rule marked a period of oppression, inflation and poverty. As a business owner, the main objective was to stay afloat.

For those brave enough to speak out against the regime, the punishment was either death by hanging or prison. Atrocities were commonplace in an atmosphere of desolation. In 1998, when Abacha died, Tonye Cole, the Co-Founder of Sahara Group, remembers it like yesterday.

“I remember exactly where I was when Abacha died. I remember people jubilating and singing and it was as if an air of relief had happened. I remember my partner had just got married and we were closing a major transaction so he delayed his honeymoon and stayed in Lagos. It is one of those moments in life where you remember key places you were. And the first expression was that of relief from everybody and then the next day reality set in,” says Cole.

“I remember exactly where I was when Abacha died. I remember people jubilating and singing and it was as if an air of relief had happened. I remember my partner had just got married and we were closing a major transaction so he delayed his honeymoon and stayed in Lagos. It is one of those moments in life where you remember key places you were. And the first expression was that of relief from everybody and then the next day reality set in,” says Cole.

Tonye Cole for the first time in years, hope dispelled despair. Cole was invested and happy.

“My partners and I had been working for three years and pushing ourselves really hard. We just got to the point where we were establishing ourselves as a business. Everything seemed to be going right. We had been working on an oil transaction and collected our allocation to load the products. At that point, all the brokers who we collected our oil allocation from had been paid by us. This is what you call betting on the horse. We had taken everything we owned and put it on this single deal,” says Cole.

Cole believed there was nothing more to be done but wait for the return on investment. Then the new government cancelled every contract that was issued by the Abacha administration.

The three young men had pumped everything they had earned for the past two years into the deal. Overnight, Cole and his partners went bankrupt. The trio had invested $400,000 of their savings in the supply and distribution of oil contracts from their new venture. For Cole, this was not the first time he lost everything. The first time was the catalyst for him to take control of his own fate. Ironically, he was hitting rock bottom again.

“If you are an entrepreneur, you are going to get bad days and if you are a successful one you are going to get even more bad days. As young people, this was all we had. People had collected their commission and nobody wanted to help us. We knew we had nothing to lose. Everything was gone. The good thing was that we had records and payment to brokers and their assignments they had given us. So we put the files together and walked into the office of a man we had never met before. We waited until we had an opportunity to speak to him and we locked the door,” says Cole.

It was 2PM on a Monday. The drive to the office of Mallam Lawan Buba, Group Executive Director, Commercial and Investment, Nigerian National Petroleum Company (NNPC), was a quiet one with all three men contemplating the gravity of what had just happened. Cole remembered advice his father, Patrick, had given him years ago. He told his son to spend five years working and learning from different companies before embarking on his own business venture. Cole had already served the five years but, in hindsight, he wondered if an additional five years could have saved him from this catastrophe.

Cole and his partners spent weeks trying to secure an appointment with the man seated in front of them that day. As Cole stood in Buba’s office, a fleeting fear gripped him. They had leveraged their one good relationship with the company’s secretary to get this appointment and if things did not go according to plan, not only would they still be bankrupt but the secretary could lose her job as well. Cole tried to read the expression on the face of Buba and drew a blank. He then regained his composure and approached the man who had the power to change their destiny.

The trio made their impassioned plea to Buba, the man responsible for the allocation of oil contracts. They showed him their legitimate contracts, payments made and financial records for the past three years. Cole took a cue from his father’s days running for president of Nigeria and gave a fervent speech on why they believed they could make a difference by creating employment and establishing an indigenous oil business, one of the first of its kind.

Buba listened to their plea and told them to wait. That was the end of the journey; there was nothing more the young entrepreneurs could do. As they left, it occurred to Cole that this could be the end of a lifetime of hard work.

“Failure teaches you a lot. As an entrepreneur I am not afraid of failure but I must learn from it,” says Cole.

During the two-hour trip back home, Cole’s life flashed before him.

Cole had three major influences growing up. His creative side was nourished by his mother, who was a journalist for one of the leading publications in Nigeria. From his father, Cole learned the skills of diplomacy and how to be a mediator on account of his role as an ambassador to Brazil. From his stepmother, Cole was given the foundations of the Christian faith upon which he built his life principles. Born in January 1967 in Port Harcourt, the capital of Rivers State, Cole and his family relocated to Anambra State during the civil war. Cole had a nomadic existence, shuffling between guardians. He learned to be self-sufficient and stumbled into his career by what he calls divine intervention.

“I ended up studying architecture because the subjects I had taken for O-levels in secondary school aligned more with the profession. I went to the University of Lagos to study architecture and then found that it was something that was perfectly suited for me. It rewards extreme hard work and punishes laziness to a fault. You had to imagine things and create it in your mind long before it comes on paper,” says Cole.

After university, Cole joined Brazilian architectural firm Grupo Quattro SA where he oversaw the construction of the new Palmas city developments in Tocantins, Brazil. This was a slight deviation from his plan to work for himself.

“When I was in university, we had already set up a business where I created architectural drawings and designs for different companies and teachers, as well as perfecting their existing designs,” he says.

Cole’s father influenced his decision to go to Brazil and leave.

“I have this belief and patriotic zeal in Nigeria and I believe we all have a role to play. My father had decided to run for the presidency in Nigeria and I decided to relocate to help him with his campaign,” he says.

Back in Nigeria, Cole Joined EMSA S.A. – one of Brazil’s largest engineering firms. He was the head of operations and business development in the country.

“They needed someone in Nigeria who could speak Portuguese and someone they could trust to implement a World Bank project. I now had this job, which was an engineering job, and it involved traveling around the country meeting government officials and business development. I had a wonderful salary at an expatriate rate, a company car and all the corporate perks. I had no interest at this point to do anything entrepreneurial. I was very comfortable,” says Cole.

Nigeria had just fallen under Abacha’s military regime. The initial hope and excitement turned to gloom. Almost overnight, the military started throwing people in jail. Riots ensued all over the country, leading to the exit of foreign businesses, like EMSA, from the Nigerian economy. The company signed off all the contracts and instructed Cole to liquidate everything.

“I said to myself ‘I am never leaving my fate in another person’s hands again,’” says Cole.

Prior to this, Tope Shonubi and Ade Odunsi had teamed up to start a new business venture in the burgeoning oil industry. Cole had turned down the offer to join the team in favour of his hefty salary and company perks. The offer was made once again, and now finding himself unemployed, Cole accepted. It was the birth of the Sahara Group, a leading private power, energy, gas and infrastructure conglomerate established two years before the end of Abacha’s rule in 1998.

All of this led to Cole walking out of the office of Buba, the man with their oil contracts. A week later, they got a call promising to reinstate their cancelled contracts over one year. Cole learned a valuable lesson.

“Don’t rely on one product and one country. In 1998, we got some of our contracts back and by 1999 we were in Ghana and then subsequently in Côte d’Ivoire, the United Kingdom, Switzerland, Singapore and the UAE.”

Today, the Group has around 20 operations across the energy sector with 660 employees. Sahara began as a facilitator in the oil sector, acting as a middleman between producers, marketers and traders. This year marks their 20-year anniversary and there is a lot to celebrate. The company has diversified into utilities, real estate, farming and infrastructure. Among its many developments is the $400-million Lekki power project in Lagos.

“When we came in there were not a lot of people in the business of trading and exploration of oil. When you talk about someone in the oil business back then, the most they would be were petrol station owners. We were the first pioneers to come into this aspect of the business,” says Cole.

Being trailblazers served the company well. The first major break happened about a year and a half after the company started. A major tool in the oil trade is the ability to have a letter of credit, popularly known as an LC. This is a guarantee taken on by a bank to make payments on behalf of the client, provided certain terms are met.

As brokers, Cole and his team will get allocations and trade them off to those who had an LC and then get their commission from the deal and plough it back into the business. For the initial period, Sahara could not open an LC, which was a major stumbling block for its growth.

“We couldn’t even open a dollar account in the beginning because the banks did not trust Nigerian businesses and this is a dollar denominated business. So we had to use a lot of innovation to get LCs. We asked our international clients to open an account for us so we could receive the payments, which they did with ease and secondly, we made sure that any LCs our clients opened, was done in our name,” says Cole.

Another major breakthrough happened when financial giant BNP Paribas approached the firm after two years of trading and helped them to finally open an LC in the company’s name.

As Cole turns 49 this year, he is slightly nostalgic when asked about his success in the oil business. He takes a deep breath and, for the first time during his interview, the charismatic and energetic entrepreneur assumes an almost vulnerable disposition as he talks of his multimillion-dollar empire.

“I am not sure I will be anywhere I am without my wife. She has allowed me to work and to be able to do what I do. I travel a lot and the ability to come in and go out without anybody being as clingy and commanding has been very helpful. Family wise, she makes me look good with everybody in my family because she is the one who keeps in touch with everyone. She is my perfect complement,” he says.

Cole met the love of his life 22 years ago at university. She was 16 going on 17 and he was in his third year of studies at the age of 18. Cole spent two years trying to convince his wife that he was the perfect match for her and years later, with three children, he calls her the glue that holds everything together.

Success can be fleeting. It has been a number of years since the company almost went bankrupt. In those days, the focus was on staying afloat as a business. Today, the Sahara Group has set up a foundation with a mandate of helping 12 million people in the next four years. The company contributes 5% of its profit to the foundation, which has worked with international not-for-profit organizations to eradicate Guinea worm disease, cataracts and cleft palates.

Faced with a global drop in oil prices, a resurgence of Boko Haram in the north of Nigeria and conflict in the Niger Delta, the West African nation’s economy is facing economic and social challenges. For Cole, his fate is firmly back in his hands. He has a much better understanding of the industry he operates in.

“We are in a boom and bust business, so these challenges are all part of life. We know when it is high and when it is low. Once oil prices are low you adjust immediately as an organization. You look at waste and how to cut it. We try as much as possible not to cut staff, we talk to them and let them understand that they need to be a lot more efficient in the things they do. It is all about planning ahead,” he says.

As Cole looks to the future, he sums up the strategy that has served him well so far.

“Let people think you have 10, act like you have only one but make sure you have 100.”

By Adedapo Adesanya

Manufacturers are yet to benefit from relief on the burden of multiple taxes and levies despite the enactment of the Nigeria Tax Act 2025, according to the Manufacturers Association of Nigeria (MAN).

The association, in its Manufacturers CEO Confidence Index (MCCI) report for the second quarter of 2026, said manufacturers continued to face multiple tax collectors and regulatory agencies during the period.

Director-General of MAN, Mr Segun Ajayi-Kadir, said the new tax law, which was expected to reduce the burden of multiple taxation, had yet to deliver the intended benefits.

“Manufacturers complained that they were still met with multiple tax collectors and regulators in Q2 2026. It follows that the implementation of the Nigeria Tax Act 2025 is yet to achieve its objective of relieving manufacturers of the burden of taxes and levies,” he said.

According to the report, Nigeria’s business environment remains largely unsupportive of manufacturing growth, with local sourcing of raw materials emerging as the only indicator that recorded noticeable improvement.

MAN, however, warned that the gains in local sourcing could be undermined by worsening insecurity in parts of the country.

The association attributed the improvement largely to persistent foreign exchange constraints, which have forced many manufacturers to source inputs locally.

Despite this, it said excessive regulation and multiple taxation continue to weigh heavily on manufacturers.

The report showed that manufacturers recorded a modest increase in sales volume during the second quarter, but rising production, distribution and logistics costs continued to erode profitability.

It added that capacity utilisation, production levels, investment and employment remained broadly unchanged during the review period.

MAN further observed that although recent foreign exchange reforms had helped stabilise the naira, inadequate foreign currency supply remained a major constraint to manufacturing operations.

Other key challenges identified in the report include poor infrastructure, high production costs, raw material shortages and unfavourable trade policies.

The association said the findings underscore the continued pressure on manufacturers despite recent fiscal and foreign exchange reforms, stressing the need for more effective implementation of policies aimed at improving the operating environment for the real sector.

By Adedapo Adesanya

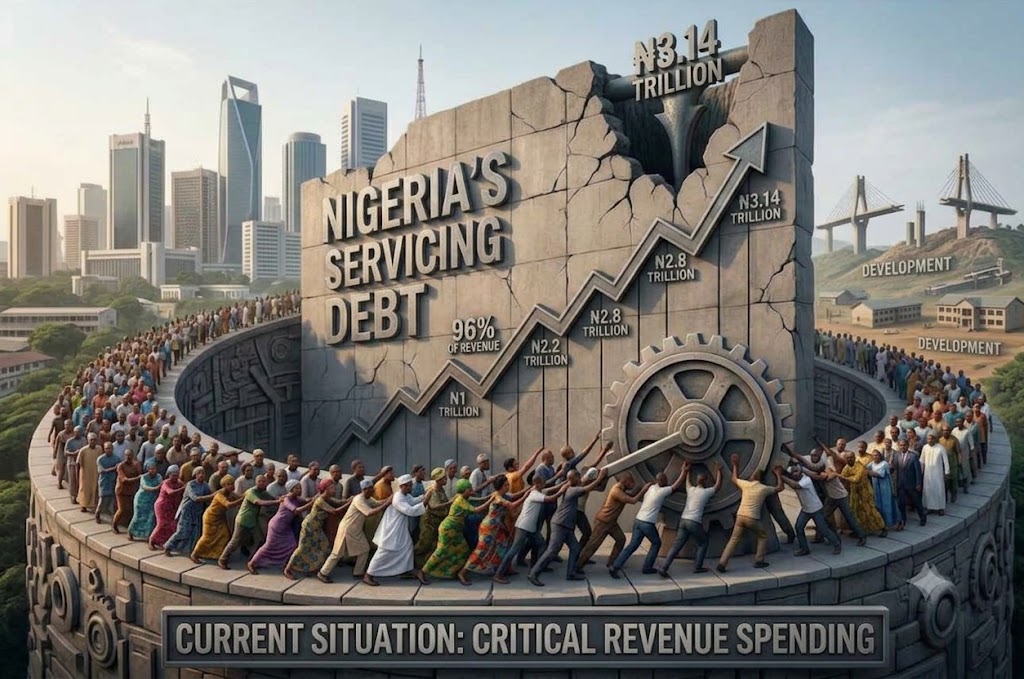

The federal government spent N3.14 trillion on servicing its domestic debt in the first quarter (Q1) of 2026, according to the Debt Management Office (DMO).

The figure, contained in the DMO’s latest domestic debt service report for Q1 2026, comprised N2.97 trillion in interest payments and N169.68 billion in principal repayments.

According to the report, the government spent N741.82 billion on domestic debt service in January before the figure rose to N967.67 billion in February.

Debt service increased further to N1.43 trillion in March, bringing total spending for the quarter to N3.14 trillion.

The March figure represented a 47.7 per cent increase from the N967.67 billion recorded in February and was 92.7 per cent higher than the N741.82 billion spent in January.

The debt office said interest payments accounted for approximately 94.6 per cent of the total domestic debt service during the quarter.

Treasury bills accounted for the largest share of interest payments at N1 trillion, while interest payments on Federal Government bonds stood at N1.96 trillion.

The government also paid N4.24 billion in interest on FGN savings bonds during the period.

The debt management body said the principal component of the debt service comprised N169.68 billion in repayments on local-denominated promissory notes.

Overall, domestic debt service rose significantly throughout the quarter, with March alone accounting for nearly half of the N3.14 trillion spent between January and March.

By Aduragbemi Omiyale

The Director-General of the Securities and Exchange Commission (SEC), Mr Emomotimi Agama, has outlined how the Federal Capital Territory Administration (FCTA) can leverage Nigeria’s capital market to raise long-term funds for critical infrastructure projects instead of relying solely on annual budgetary allocations.

According to Mr Agama, the capital market offers the FCT a sustainable financing model for roads, rail, housing, water, transport and other infrastructure through instruments such as infrastructure bonds, green bonds, real estate investment trusts (REITs), asset recycling and tokenised municipal securities.

Speaking at the Abuja Business and Investment Summit and Expo (ABIE 2026) in Abuja, the SEC chief noted that Abuja’s development demonstrates that economic growth is driven by investment, stressing that “cities are not built by budgets alone. Cities are built by capital markets.”

He advised the FCT to establish a long-term infrastructure bond programme backed by dedicated revenue sources such as ground rents, tenement rates, tolls, parking fees and land-use charges, noting that this would enable the territory to finance major projects without overburdening annual budgets.

“A budget can only spend what a single year has collected. A bond can spend what 30 years will collect,” Mr Agama said, explaining that infrastructure projects generate long-term economic value that can be used to service debt over time.

The SEC boss said the territory could also access cheaper financing through green and sustainability-linked bonds for projects including mass transit, light rail, solar-powered street lighting, waste-to-energy facilities and water infrastructure.

He further proposed the creation of an FCT Real Estate Investment Trust to unlock value from Abuja’s extensive property portfolio while giving ordinary Nigerians an opportunity to invest in the city’s real estate market.

Mr Agama also urged Abuja Investments Company Limited (AICL) to consider listing some of its businesses or establishing a listed infrastructure fund, saying this would raise capital without increasing government debt while improving corporate governance and transparency.

On the long-abandoned Millennium Tower project, he said the estimated over N400 billion completion cost should not be viewed as a budgetary burden but as an investment opportunity that could be financed through a special purpose vehicle and offered to investors via the capital market.

“The question is not whether Nigeria can afford the Millennium Tower. The question is whether we will let ordinary Nigerians own it,” he said.

Mr Agama further proposed an asset recycling programme under which completed income-generating public assets, including terminals, markets, commercial properties and the International Conference Centre, could be securitised or concessioned to institutional investors, with proceeds reinvested in new infrastructure.

He also called on the FCT to pioneer a regulated tokenised municipal bond programme that would allow citizens to invest as little as N10,000 through mobile phones in specific infrastructure projects.

According to him, the recently enacted Investments and Securities Act (ISA) 2025 has strengthened the legal framework for sub-national governments to access the capital market while providing enhanced investor protection and clearer regulation of digital assets.

Mr Agama disclosed that Nigeria’s capital market has grown significantly, with total market capitalisation exceeding N217 trillion as of May 2026, comprising about N160.5 trillion in equities and N56.7 trillion in bonds.

He said recent reforms, including the migration to a T+1 settlement cycle and regulatory measures to deepen market participation, have improved market efficiency and strengthened investor confidence.

The SEC DG assured the FCTA of the commission’s readiness to provide technical support for structuring and registering capital market instruments, saying the agency would work closely with the territory to unlock financing for infrastructure projects.

He added that Nigeria’s capital market remains critical to mobilising domestic savings for national development, insisting that “money is not scarce; delivery capacity is scarce, and financing follows delivery capacity.”