Feature/OPED

South Africa Lacks Energy Power in Emerging Multipolar World

By Kestér Kenn Klomegâh

South Africa undoubtedly boasts its power and integrity on the global stage. South Africa is known as the first economic power in Africa and as a staunch member of many international organizations. It maintains significant regional influence and is a member of the African Union, the Commonwealth of Nations, the BRICS and the G20. With an estimated 62 million (as of 2023) people of diverse cultural origins, South Africa’s economy is sustained by both local and foreign businesses. Today, it has to struggle with power outages, unsuccessful in meeting both domestic and industrial power requirements in the country.

Unlike most of the African countries, South Africa’s economy is the most industrialized and technologically advanced, the second largest economy in Africa, after Egypt and Nigeria. South Africa has a very large energy sector and is currently the only country on the African continent that possesses a nuclear power plant. The country’s primary electricity generator is Eskom, the utility is the largest producer of electricity in Africa.

Eskom’s latest energy availability factor (EAF) data reveals that mismanagement, corruption, poor maintenance, and sabotage caused power station breakdowns. Due to severe mismanagement and corruption at Eskom, the company is $22 billion in debt and unable to meet the demands of the South African power grid. It has resulted in load shedding to prevent a failure of the entire system when the demand for electricity strains the capacity of Eskom’s power-generating system.

China’s Factor in the South African Energy Crisis

China has contemplated support for the South African energy crisis since 2011 it joined BRICS. The latest development was in August 2023 during the 15th BRICS summit held in Johannesburg, South Africa signed a raft of deals with China to help it overhaul its creaky energy sector including upgrading its nuclear power plant as the government seeks to ease a severe energy crisis hobbling the economy.

The agreements, signed with Chinese power companies on the sidelines of the BRICS summit, include upgrades to the electricity transmission and distribution network. “We are moving at the speed of the fastest, we are not going to move at the speed of the slowest,” Electricity Minister Kgosientsho Ramokgopa after signing the deals. China’s power transmission grid network, generation capacity and renewable energy plants are the largest in the world and were set up in a short time and it is this expertise South Africa wanted to learn from, Ramokgopa said.

South Africa’s state utility Eskom has a power supply shortfall of around 4,000 megawatts (MW), accounting for a tenth of its installed capacity and resulting in record power cuts. Its transmission capacity is highly constrained, preventing any alternative power sources from coming online. The bulk of its distribution infrastructure – an array of thousands of transformers and substations supplying power to households – often burns out leading to long hours without power.

China will help to extend the life of Eskom’s coal-fired power plants, offer technology to cut emissions at a lower cost than available elsewhere globally and China might also set up transformer and solar PV panel manufacturing facilities in the country, Ramokgopa said. It will also help South Africa upgrade its nuclear power plant, he added.

President Cyril Ramaphosa noted that China, its biggest trading partner, would supply emergency power equipment worth 167 million rand ($8.9 million) and a grant of around 500 million rand for the power sector, without giving timelines.

According to an April 2024 report from Boston University’s Global Development Policy Center and the African Economic Research Consortium, China has a unique opportunity to drive forward an energy revolution in Africa, but it must first reverse nearly two decades of neglect of green power investments there. Beijing has emerged as the continent’s biggest bilateral trading partner since the start of the century and has financed billions of dollars worth of large-scale infrastructure projects.

In 2021, China’s President Xi Jinping said the country would not build new coal-fired power projects abroad, pledging to deal with climate change by supporting the development of green and low-carbon energy. Although Africa’s green energy potential is one of the highest in the world, Chinese lending and investment have so far provided relatively little support for the continent’s energy transition.

Lending for renewables, such as solar and wind, from China’s two main development finance institutions constituted just 2% of their $52 billion of energy loans from 2000 to 2022, while more than 50% is allocated to fossil fuels. “Given current economic challenges and future energy opportunities, China can play a role in contributing to Africa’s energy access and transition through trade, finance and FDI (foreign direct investment),” the report said.

Chinese development finance institutions have been focused on investing in the extraction and export of commodities to China and in electrification projects. Chinese lending has targeted many of the same sectors that produce the oil and minerals that flow back to China. At least eight hydropower projects financed by the Export-Import Bank of China (CHEXIM), which represent 26% of all hydropower lending, are intended to support the extraction of various metals.

“Although this track has led to export revenues for African economies, African countries are not yet receiving the full benefits of renewable energy technologies,” the report said. In 2022, fossil fuels accounted for around 75% of total electricity generation in Africa and about 90% of energy consumption, the report said.

South Africa and across the rest of Africa, energy has become crucial. Without sustainable energy flow, industrialization is impossible. At the BRICS-Africa Outreach and BRICS Plus Dialogue, China’s leader Xi Jinping made concrete proposals which included: China to launch the Initiative on Supporting Africa’s Industrialization. China plans to harness resources for cooperation with Africa and support Africa in its manufacturing sector, industrialization and economic diversification. China plans to channel more resources into investment and finance industrialization.

Russia’s Renewable Energy Pledges

South Africa and Russia have excellent relations. The nuclear energy deal between South Africa and Russia has dominated official discussions over the years. Under Jacob Zuma, Russian President Vladimir Putin signed a deal estimated at $76 billion to build Russian-run nuclear energy plants. Until today, that deal remains unrealizable and worse still mentioned in speeches as part of a bilateral agreement. But in the latest developments, South Africa from explicit indications unreservedly supports Russia’s ‘special military operation’ in Ukraine. During Johannesburg’s 15th BRICS summit held in August 2023, nuclear power pledges, with high enthusiasm, were renewed.

Russian Ambassador to South Africa Ilya Rogachev renewed the official pledge that Russia would help South Africa solve the problem of energy shortages. “The Russian Federation is a world leader in the field of nuclear technology. If we talk about cooperation between Russia and South Africa in this area, joint work on expanding nuclear generation in the country can play a key role in solving the problem of electricity shortages in South Africa and can lay the foundation for energy independence and technological sovereignty of the Republic of South Africa,” the diplomat told the local Russian media.

According to him, Russian companies work with advanced technologies and are ready, for their part, to offer expertise and competencies within the framework of appropriate tender procedures. Russia is ready to cooperate in the supply of fuel for nuclear power plants, the construction of new large and small nuclear capacities, the development of floating plants, the construction of a new research reactor, the development of nuclear medicine and so forth. Russia has the desire to strengthen South Africa’s energy security, and in particular, is ready to exchange useful key practices in the field of energy production, distribution and utilization.

European Union and South Africa’s Energy Cooperation

At least in 2021, the European Union has supported its concern over South Africa’s energy difficulties. Even far earlier European Union members have contributed financially. The governments of South Africa, France, Germany, the United Kingdom and the United States of America, along with the European Union, have in November 2021 announced a new ambitious, long-term ‘Just Energy Transition Partnership’ to support South Africa.

According to European Commission President, Ursula von der Leyen, the European Union kick-started the Just Energy Transition Partnership with South Africa, a first-of-its-kind global initiative for accelerating a just energy transition, and would also outline measures undertaken by the government of South Africa for long-term energy transition. EU is working with a concrete programme at the full cost of $8.5 billion, in addition to what the World Bank Board approved for Eskom, the South African energy Sector.

The President of the United States of America, Joseph R. Biden, said: “The United States is proud to partner with the Government of South Africa and the members of the International Partners Group to support South Africa’s just transition to a cleaner energy future. We welcome the comprehensive JET Investment Plan and fully support South Africa’s economy-wide energy transformation. Our support for South Africa’s clean energy and infrastructure priorities, which include efforts to provide coal miners and affected communities the assistance that they need in this transition, will help South Africa’s clean energy economy thrive.”

BRICS New Development Bank

Much praised BRICS (Brazil, Russia, India, China and South Africa) New Development Bank was established in 2015 to compete with other multilateral development banks such as the World Bank and IMF. As a multilateral development bank to mobilize resources for infrastructure and sustainable development projects in emerging markets and developed countries, it has so far limited scope of operations. It dreams of supporting developing countries, but it cannot under the circumstances and is far behind the status of the IMF and World Bank. While the IMF has offices across Africa, the NDB has only a skeleton staff in Russia and South Africa.

Although Bangladesh, Egypt, Uruguay and the United Arab Emirates also joined as members, the NDB still cannot simply compete with the already established multilateral financial institutions. In 2018, the Board of Directors of the New Development Bank approved two infrastructure and sustainable development projects in South Africa and China, with both loans aggregating $600 million. In addition, the NDB offered financial assistance during the coronavirus pandemic. With energy difficulties, there has been no report indicating loans to support South Africa’s energy sector. In future, developing countries craving to become members of BRICS should not expect any development finances from the BRICS (Brazil, Russia, India, China and South Africa) New Development Bank.

World Bank’s Contribution to South Africa’s Energy Sector

Last October 2023, the World Bank approved a $1 billion loan to support South Africa’s energy sector currently experiencing worse conditions including inadequate funds for overhauling, renovation and upgrading. That the World Bank’s loan, at least, would pull South Africa out of its persistent energy crisis that has adversely hit industrial production.

“The loan endorses a significant and strategic response to South Africa’s ongoing energy crisis and the country’s goal of transitioning to a just and low carbon economy,” the World Bank said in its report. But the South African government has often said it needs nearly $80 billion over the next five years to fund its transition to greener energy sources. Energy experts have consistently suggested that South Africa undergo some necessary reforms in its energy sector to address and consequently overcome regular power cuts that have curbed economic growth and industrial production.

South Africa is not the only country experiencing energy shortage and crisis. Energy poverty is pounding some Southern African countries. Nearly all African countries are suffering from acute power deficits. Appreciably China, Russia and other external countries, at least, have shown their uttermost unique contributions to consolidate relations and save South Africa, whose diverse internal problems turn complicated but highly boasts its image as Africa’s economic power on the international stage. With extreme prestige, the United States, Europe, BRICS and the G20 consistently chuckle at the African National Congress (ANC), President Cyril Ramaphosa and the entire population of South Africa.

Feature/OPED

How Governor Uba Sani’s Sustain Agenda is Rewriting Kaduna’s Agricultural Metamorphosis

By Sani Abdulrazak, PhD

Governance ascends into telos when the hands that feed the nation work with sustained hope rather than uncertainty. The farmer is indeed relieved when he no longer gauges the farming season through the prism of survival or rising cost of fertiliser, but by the promise of a better harvest and a pathway to prosperity. Truth is, rural communities are only fundamentally satisfied when their fertile lands marry deliberate government intervention. This government intervention in agriculture is not in mere promises, speeches, or ceremonies, but in flourishing fields, fuller warehouses and improved livelihoods. At the very core of Governor Uba Sani’s SUSTAIN agenda is strengthening the bedrock upon which food security and economic prosperity are built: agriculture. His approach has been less of bombast and more of stewardship, allowing the sector to emerge from years of uncertainty into one of resurgence.

The agricultural sector of Kaduna State over the past three years reveals a government that has chosen investment over rhetoric. Pinpointing agriculture as the oxygen of the state’s economy, the administration has committed unprecedented resources to this very pertinent sector. The agricultural budget rose from barely ₦1.48 billion in 2023 to ₦74.2 billion in 2025, before exceeding ₦100 billion in the 2026 budget, making Kaduna one of the few states committing over 10 per cent of its annual expenditure to agriculture. These allocations represent an explicit declaration that meaningful agricultural transformation begins with deliberate investment. They equally reflect the prudence and resolve to position Kaduna not merely as a producer of crops but as an agricultural colossus. What once appeared a distant aspiration is gradually taking the shape of a tangible renaissance, built not on ephemeral promises but on carefully hewn policies and enduring commitments.

The most conspicuous manifestation of this administration’s intervention has been its direct support for farmers. Admittedly, farming has become increasingly expensive across the country lately, yet Kaduna state responded with one of the largest agricultural support programmes by distributing 15,000 metric tonnes of fertiliser, equivalent to about 500 truckloads, free of charge to over 120,000 farmers across the 23 local government areas. Through the “Tallafin Noma programme”, an additional 69,000 smallholder farmers received improved maize seeds and agrochemicals to increase productivity. These interventions have reduced production costs for thousands of farming households while strengthening food production at a time when food security remains a national concern. Such interventions are not mere statistics; they are a bulwark against rural poverty, a catalyst for productivity and a harbinger of renewed confidence. For many farmers, government support has become the linchpin upon which an abundant harvest now rests.

Governor Uba Sani understands that the true promise of modern agriculture lies not only in cultivation but also in the value created after the harvest. The commencement of the Kaduna Special Agro-Industrial Processing Zone marks an important shift from exporting raw produce to processing agricultural commodities within the state. Complementing this is the construction of Northern Nigeria’s first Agricultural Quality Assurance Centre, designed to certify agricultural produce for local and international markets. Together, these initiatives promise to reduce post-harvest losses, attract private investment, create employment opportunities and improve the competitiveness of Kaduna’s agricultural products beyond Nigeria’s borders. They equally represent a conscious effort to build an agricultural ecosystem, a lasting edifice of productivity whose impact will reverberate far beyond the present generation. The vision is transformative as it is audacious, replacing dependence with self-sufficiency and creating a confluence where farming, industry and commerce intersect.

Mechanisation and rural agricultural support have also received renewed focus. The procurement of tractors and farm implements, the provision of irrigation pumps, power tillers, fertilisers, and crop protection chemicals to farmer cooperatives, alongside continued investment in rural and farm-to-market roads, shows an understanding that productivity improves when farmers are supported with the right tools and infrastructure. Easier access to markets not only reduces transportation costs but also minimises post-harvest losses, ensuring that farmers reap greater value from their labour. These investments have become the fulcrum upon which rural prosperity increasingly turns, replacing archaic practices with innovative solutions and galvanising communities to embrace modern agriculture. They stand as an obelisk of thoughtful governance, a testament to the belief that development flourishes where opportunity is deliberately cultivated.

Superlatives are in short supply when describing Governor Uba Sani’s three years in office, and even more so when one attempts to capture the magnitude of his agricultural revolution. Among the promises he made was to revive agriculture as the engine of Kaduna’s economy, and, as always, he has kept his promise. We’ve always known he would; the challenges, though, are far from over, but every meaningful reform must navigate its own labyrinth of challenges. Yet the administration’s trajectory remains steadfast, its achievements too palpable to dismiss even to the staunch critics. It would be germane to etch in our minds that history, that impartial arbiter of leadership, may ultimately remember this administration as one that rekindled the state’s agricultural zenith and restored dignity to farming for generations to come.

Sani Abdulrazak, PhD, is a writer, researcher and public affairs analyst based in Zaria, Kaduna State

Feature/OPED

The Role of the Stock Market in Nation Building: Imperatives for an Inclusive Capital Economy

By Adedapo Adesanya

Nigeria’s stock market has crossed a milestone that demands attention. With total market capitalisation reaching N151.327 trillion as at June 2026, the Nigerian Exchange Limited (NGX) has not only consolidated its position as Africa’s second-largest bourse, but it has also demonstrated something more consequential: that domestic capital, when properly mobilised, is a credible engine of national development.

Nation building is rarely a singular act. It accumulates through institutions that function, capital that circulates, and citizens who believe the system works for them. Few institutions make that case as visibly as a thriving stock exchange. The market is no longer just a barometer of investor sentiment. It is an active participant in Nigeria’s development.

The quality of any capital market ultimately reflects the quality of the companies it hosts. Markets create national wealth most effectively when they provide long-term capital to productive enterprises that expand industrial capacity, create jobs, deepen local supply chains and generate enduring shareholder value.

Earlier in the year, President Bola Tinubu had commended the NGX Group, corporate Nigeria, market operators and investors for propelling NGX past the historic N100trn market capitalisation mark, describing the milestone as a strong indicator of renewed investor confidence and economic recovery.

He said: “The Nigerian capital market stands at the heart of our ambition to build a one-trillion-dollar economy. It is the engine through which long-term finance must be mobilised to power critical sectors – from infrastructure to housing, technology, energy and industrial growth.”

Nigeria has increasingly demonstrated this through home-grown corporate champions such as the Dangote Group, whose decades-long investments across strategic sectors illustrate how patient enterprise-building and capital market development can reinforce one another. Strong companies strengthen strong markets, and strong markets, in turn, provide the capital needed to build even stronger companies.

But numbers, however impressive, are only part of the story. The more compelling narrative lies in who is now participating and how. The explosion in retail participation over the past two years is inseparable from digital infrastructure.

Data by the Central Securities Clearing System (CSCS) shows 151,749 new brokerage accounts were opened in just the first five months of 2025. Between 2019 and November 2025, over 2.1 million new retail investment accounts were established, the strongest growth in seven years. This is not incidental. It is the direct result of deliberate technological positioning by market operators and regulators, and one of the more underappreciated contributions to national economic inclusion, the companies on the stock market.

Nigeria’s investing demographic is shifting, and the market must shift with it. A largely young, mobile-first population does not respond to traditional channels. They discover financial products on social media, transact via apps, and make decisions based on peer influence as much as professional advice. The 56 per cent year-on-year increase in retail equity investment to N981 billion in the first seven months of 2025 reflects this generational pivot.

Yet gaps remain. Women, smallholder entrepreneurs and low-income earners across tier-2 and tier-3 cities are underrepresented. Instruments like the Federal Government Savings Bond, accessible from as little as N5,000, demonstrate that appetite exists beyond the traditional investor class. The challenge now is sustained financial literacy, culturally relevant messaging, and last-mile digital infrastructure that meets these segments where they are. Broadening that base is not just good market development; it is nation-building in its most practical form.

Sustaining confidence in the capital market requires a functioning compact between four critical actors. Regulators must maintain the credibility they have worked on to rebuild. Reforms, including foreign exchange unification, banking recapitalisation, and NGX demutualisation, have restored institutional trust. That momentum cannot be squandered.

Financial institutions must do more than offer products; they must offer pathways. Education, simplified onboarding, and genuinely accessible advisory services are not optional add-ons. They are the infrastructure of a participatory economy.

Listed companies have a responsibility that extends beyond quarterly earnings. They must consistently demonstrate transparency, sound corporate governance, operational excellence and long-term value creation. Companies that invest patiently in productive assets while rewarding shareholders over time help deepen confidence in the market and encourage wider public participation. The experience of leading Nigerian enterprises, including companies within the Dangote Group, shows that sustained investment in the real economy can simultaneously create industrial capacity, support national development and deliver enduring value to investors.

At $117 billion, NGX’s capitalisation represents only about 35 per cent of GDP. Mature markets typically exceed 100 per cent. Closing that gap will require more quality listings, particularly from the productive sectors of the economy, where long-term capital can translate into long-term national growth.

Finally, technology providers must treat financial inclusion as a design constraint, not an afterthought. Connectivity gaps, low digital literacy, and transactional friction are not user problems. They are product problems.

Domestic investors now account for 77.79 per cent of total market activity, a structural shift that makes the market less exposed to global sentiment swings and more reflective of domestic economic conviction. That is a nation beginning to fund its own future.

As Nigeria seeks to build a more inclusive capital economy, the objective should not simply be to increase the number of investors. It should be to increase the number of successful Nigerian businesses capable of attracting long-term investment. Every globally competitive indigenous company that chooses transparency, governance and broad-based ownership strengthens both the capital market and the country’s economic resilience. The relationship is mutually reinforcing: vibrant companies deepen the market, while a vibrant market empowers the next generation of national champions.

The foundation exists. What comes next depends on whether all stakeholders can sustain the coordination that has made this growth possible and go further. A participatory capital economy is not an aspirational language. In Nigeria today, it is an unfinished project moving steadily in the right direction.

By Blaise Udunze

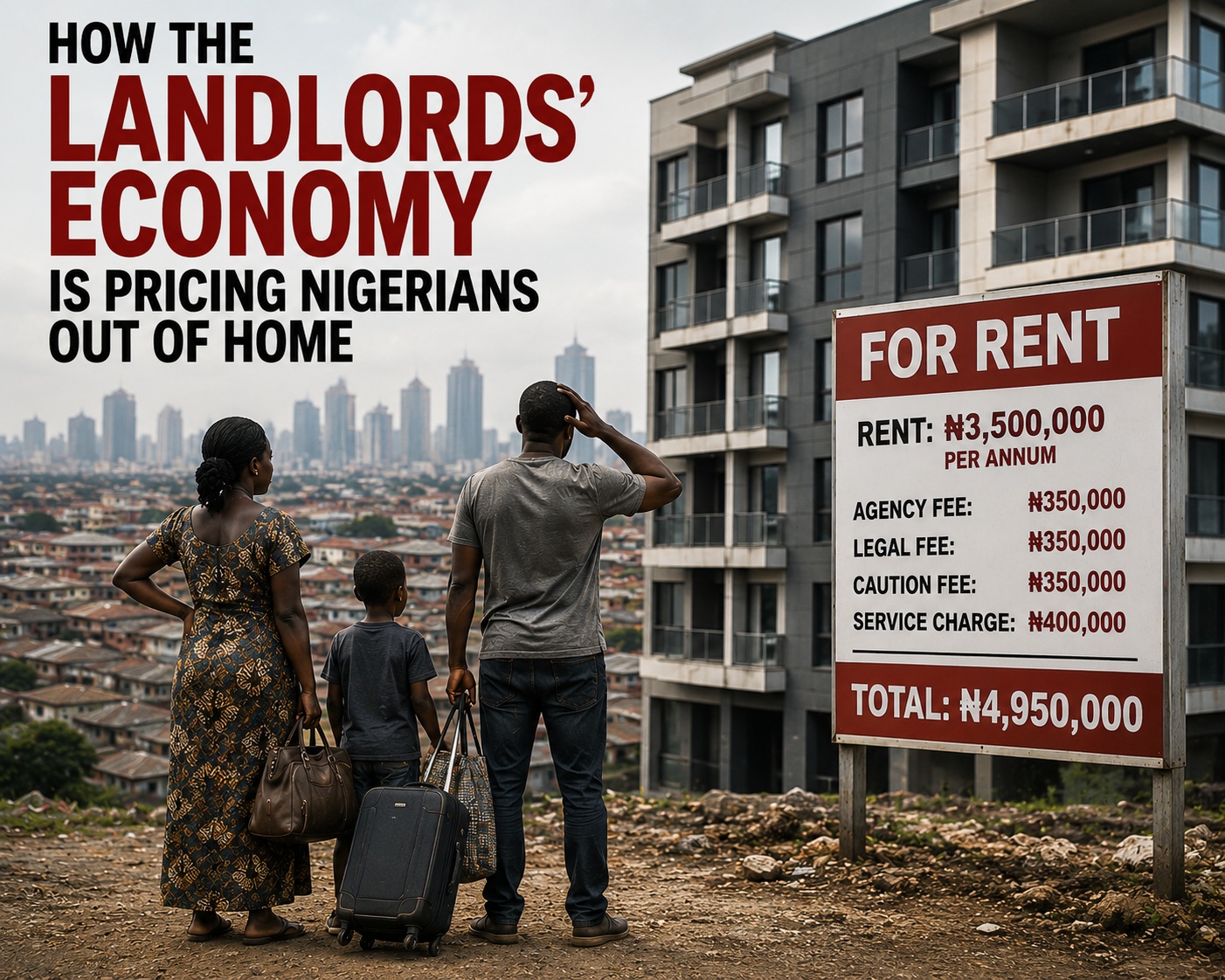

It is considered that in every organised society, the home is supposed to be a place of security. It should be where families find peace after a hard day’s work, where children grow, where dreams are nurtured, and where the pressures of life temporarily fade away. This narrative comes with keen interest, having witnessed that for millions of Nigerians, home has become the country’s newest economic battlefield. This is fast becoming the experience for the vast majority of Nigerians.

Across the length and breadth of Nigeria, citizens are deeply lamenting the skyrocketing rent. Regrettably, this has become one of the fastest-rising costs of living. An unexpected trend which has become a huge concern is that currently apartments that were rented for N700,000 or N1 million just a few years ago are now advertised for N3 million, N5 million or even higher. Amidst this bizarre development, do you know that they are often without significant improvements to the property itself? One key troubling development is that recent estimates suggest that house rents in many Nigerian cities have surged by between 100 and 300 per cent over the last two years, a pace that far exceeds the country’s official inflation rate and has placed unprecedented pressure on households already struggling with rising food, transportation and energy costs.

Landlords, through estate agents, increasingly demand one or two years’ rent upfront. Tenants are expected to pay 10 per cent of the principal rent toward agency fees, legal fees, agreement charges, caution deposits, and, in most cases, the service charge (which appears to be higher), security levies, and utility-related costs before receiving the keys. In many cases, these additional charges add hundreds of thousands or even millions of naira to the advertised rent, making the total cost of securing accommodation far beyond the reach of average-income earners. Equally disturbing is the unchecked exploitation by agent marauders, who prey on desperate house seekers by imposing outrageous and often illegal fees that further deepen Nigeria’s housing crisis. What should ordinarily be a routine life event has become a financial ordeal.

Nigeria’s housing crisis is no longer simply a property story. It has evolved into an economic emergency with profound implications for families, businesses, public health and national development.

The Federal Government’s National Housing Data Technical Committee estimates that Nigeria faces a housing deficit of approximately 15 to 20million homes. At the same time, millions of existing houses are considered structurally inadequate and lack access to essential infrastructure. If this figure is something to consider, anyone would know that these figures reveal two overlapping crises. First, this shows that millions of Nigerians cannot find decent accommodation, whilst millions more live in overcrowded, unsafe or poorly serviced housing.

At the same time, Nigeria’s population continues to expand rapidly, with cities absorbing hundreds of thousands of new residents every year.

One of the challenges is that urbanisation has consistently outpaced housing development, widening the gap between supply and demand while, predictably, rents continue to rise and affordability continues to decline.

Remarkably, housing experts generally recommend that households should spend no more than 30 per cent of their income on accommodation. For many Nigerian families, that recommendation has become almost impossible to achieve.

Teachers, nurses, journalists, police officers, civil servants, young bankers, entrepreneurs, artisans and other middle-income earners increasingly devote more than half of their annual income to rent alone. For many, housing has become the single largest financial obligation, leaving very little for every other necessity of life.

After paying landlords, food budgets shrink. Healthcare is postponed. Children are transferred to less expensive schools. Retirement savings disappear. Business investments are suspended. Vacations become unimaginable luxuries. The rent bill has become the first expense families think about and the last financial burden they can escape.

The effects extend far beyond individual households. This is totally outrageous, as financial analysts have long observed that when accommodation consumes a disproportionate share of disposable income, consumer spending across the economy inevitably weakens.

Families postpone replacing household appliances. Vehicle purchases are delayed. Furniture sales decline. Restaurants receive fewer customers. Clothing retailers experience lower patronage. Small businesses lose purchasing power from consumers whose earnings are now tied up in rent. The result is a vicious economic cycle in which rising housing costs suppress consumption, reduce business activity, and ultimately slow economic growth.

Behind every rent increase lies a deeply personal story. Consider a fictional but representative family whose experience mirrors that of countless Nigerians. The aspect of receiving notice that the annual rent for their modest two-bedroom apartment would rise from N1.2 million to N3 million comes with uneasiness. At this point, the Blessings’ family had spent months desperately searching for an alternative.

Unable to afford the increase and harassment from the landlord, they eventually relocated nearly 30 kilometres away from their former neighbourhood. The consequences were immediate. Their children had to change schools. The family’s daily commuting time doubled. Transportation costs rose sharply. Family time disappeared.

The father now leaves home before sunrise and returns late at night. The mother spends more each month commuting than she once spent on groceries. Their financial burden has not disappeared. It has merely shifted from rent to transportation and also deals with other issues like epileptic power supply and flooding, especially during this rainy season.

Unfortunately, such stories are no longer exceptional. They have become increasingly common across Nigeria’s major cities. Perhaps no demographic feels this pressure more acutely than young professionals.

Come to think of it, graduates entering the workforce quickly discover that entry-level salaries cannot support decent accommodation close to their workplaces. You would also see many remaining with their parents far longer than anticipated. Other effects include seeing them share apartments with several unrelated adults to reduce costs, whilst some endure daily commutes lasting three or four hours because affordable housing exists only in distant suburbs.

The fact is that the consequences extend beyond inconvenience because long commuting hours reduce productivity, increase fatigue, heighten stress levels and significantly diminish quality of life. Another aspect of this, which is discouraging, is that for many talented young Nigerians, financial independence, home ownership and family formation are becoming increasingly distant aspirations. Several interconnected forces explain why rents continue to climb so aggressively.

Inflation has significantly increased the cost of cement, steel, roofing sheets and virtually every construction material required to build houses. The depreciation of the naira has made imported building materials substantially more expensive. No doubt, from recent findings, there are clear indications that there is a significant increase in the prices of building materials. Let us see the period between 2024 to 2026, Cement: N6,500 – N13,000; blocks: N600 – N1100; 30T of sand: N165,000 – N250,000; 30T of granite: N530,000 – N780,000; rebars (iron) ton: N850,000 – N1,150,000 amongst others. To be fair, it is a known fact that high interest rates have increased borrowing costs for developers, while land acquisition remains prohibitively expensive in many urban centres. The very question at heart is, how has this recent development significantly impacted the apartments built five years ago and beyond?

The government has made it difficult to the point that obtaining development approvals can be slow and costly. Developers also contend with multiple taxes, infrastructure levies and rising labour costs before construction even begins. No doubt, these expenses inevitably find their way into rental prices. But one question keeps running through the minds of many, which is, how do these directly impact apartments built many years back? The truth is that market realities alone do not explain every increase.

In many locations, speculative pricing has taken hold. Some landlords have raised rents far beyond what can reasonably be attributed to maintenance or inflation, taking advantage of overwhelming demand and the severe shortage of available accommodation.

The inability of many Nigerians to purchase homes has further intensified the pressure on the rental market. Inflation, high mortgage rates and limited access to long-term housing finance have pushed home ownership beyond the reach of millions, forcing them to remain tenants for much longer than planned. This should be blamed on the government of the day, as more people compete for a limited supply of rental properties, landlords possess even greater leverage to increase prices.

Housing insecurity is also producing a less visible but equally damaging consequence for deteriorating mental health.

The constant fear of eviction, the uncertainty surrounding annual rent reviews and the enormous pressure of raising large lump sums every one or two years create persistent psychological stress.

Think of the impact of parents’ worry about disrupting their children’s education. Young couples postpone marriage because they cannot afford accommodation. Family disagreements increasingly revolve around financial pressures. Consider the part of many Nigerians who quietly or secretly or unknowingly battle anxiety, emotional exhaustion and depression arising from the struggle to secure decent housing.

None of these psychological costs clearly appear in official economic statistics, but the truth is that they profoundly affect productivity, family stability and overall well-being. It is equally obvious that the crisis is also affecting employers and businesses.

Workers forced to travel long distances arrive at work exhausted. Traffic congestion consumes valuable productive hours each day. It turns out that companies increasingly struggle to retain staff who relocate in search of affordable accommodation. Also, know that many employers face mounting pressure to increase housing allowances simply to remain competitive.

All these call for a balancing as employees demand higher wages to offset escalating living costs, further increasing operating expenses for businesses already contending with inflation, unstable exchange rates and rising energy prices.

Housing affordability is therefore no longer merely a social concern. It has become a business and national competitiveness issue.

Though Nigeria is not alone in confronting housing affordability challenges, its recent trend calls for attention. Across Africa, rapid urbanisation continues to outpace housing supply.

For this reason, Kenya has introduced ambitious affordable housing programmes aimed at expanding supply, although implementation challenges remain; this can’t be compared to Nigeria’s current situation. Ghana is not left out of the equation as it continues to battle a significant housing deficit. Ghana is also grappling with the irony of completed homes that remain unaffordable for many citizens. South Africa, despite possessing a relatively more developed mortgage market, continues to experience severe affordability pressures in cities such as Johannesburg and Cape Town.

Nigeria’s situation, however, is intensified by its enormous population, rapid urban expansion, limited mortgage penetration and one of Africa’s largest housing deficits.

Nigeria has witnessed successive governments introducing affordable housing initiatives, mortgage schemes and public-private partnerships which fails before implementation. While these programmes represent positive intentions, delivery has consistently fallen far behind growing demand.

Housing experts argue that meaningful reform requires far more than constructing a limited number of housing estates.

Nigeria must simplify land acquisition processes, reduce infrastructure costs, expand mortgage accessibility, improve planning approvals, encourage private-sector investment in affordable housing and strengthen incentives for developers willing to build homes for middle- and low-income earners.

Improving housing data is important, but accurate statistics alone cannot reduce rents. Effective implementation remains the country’s greatest policy challenge.

Let’s consider some of these salient points proffered by urban planners who insist that Nigeria’s housing crisis cannot be solved exclusively through market forces. According to them, governments at all levels must invest strategically in infrastructure and create financing mechanisms that reduce development costs. To further help reduce the housing gap, they encourage the construction of affordable rental housing rather than focusing disproportionately on luxury developments.

The truth is that if housing continues to consume an ever-growing share of household income, consumer spending, investment and long-term economic growth will remain constrained. Another key barrier that must be addressed quickly, as highlighted by researchers, is inflation, limited housing finance, weak regulatory enforcement and inconsistent policy implementation, which happen to be major bottlenecks to affordable housing delivery.

One key question that yearns for answers is whether it is not obvious to the government and other stakeholders that housing is far more than concrete walls, roofing sheets and painted ceilings? The fact is that shelter, as the meaning implies, shapes educational outcomes, influences public health, determines productivity, strengthens families, supports social mobility and contributes directly to national competitiveness.

At this stage, it is a complete shame and at the same time an irony that a nation where hardworking teachers, nurses, journalists, entrepreneurs, artisans, security personnel and civil servants cannot comfortably afford decent shelter risks weakening its middle class, widening inequality and undermining sustainable economic growth.

If the truth must be told, Nigeria’s rent crisis is therefore not merely about landlords and tenants. For a fact, it is about the future of work, family stability, economic opportunity and social justice. Clearly, it is about whether millions of hardworking citizens can enjoy the dignity that comes with secure and affordable housing.

The mistake all along, which must be eschewed, is that a country’s progress is being measured solely by the number of luxury estates it builds or the height of its skyscrapers. More importantly, it should also be measured by whether ordinary citizens can afford a safe place to call home without sacrificing their children’s education, healthcare, savings or future aspirations.

If this is not adequately addressed, this rent trap will persist until affordable housing becomes a genuine national priority backed by bold reforms and sustained implementation; millions of Nigerians will continue facing an impossible choice, which would invariably lead them to surrender their financial future to keep a roof over their heads or abandon the comfort, security and dignity that every family deserves.

Concerned stakeholders shouldn’t continue to believe that the true cost of Nigeria’s rent crisis is therefore measured only in naira. It is measured in postponed dreams, delayed marriages, fractured families, declining productivity, abandoned ambitions, struggling businesses and the quiet erosion of hope among citizens who work tirelessly every day but find the simple promise of a decent home slipping further beyond their reach.

Blaise, a journalist and PR professional, writes from Lagos and can be reached via: bl***********@***il.com